Justin Sullivan

Thesis

In the June quarter Warren Buffett bought a $3 billion stake in Citigroup (NYSE:C). And investors should not be surprised: Citi trades at deep value multiples and its valuation is materially lagging peers. For reference, with a P/B of x0.55 and a PE Non-GAAP of x6.46 Citi is valued at a relative discount to the industry between 30% to 50%.

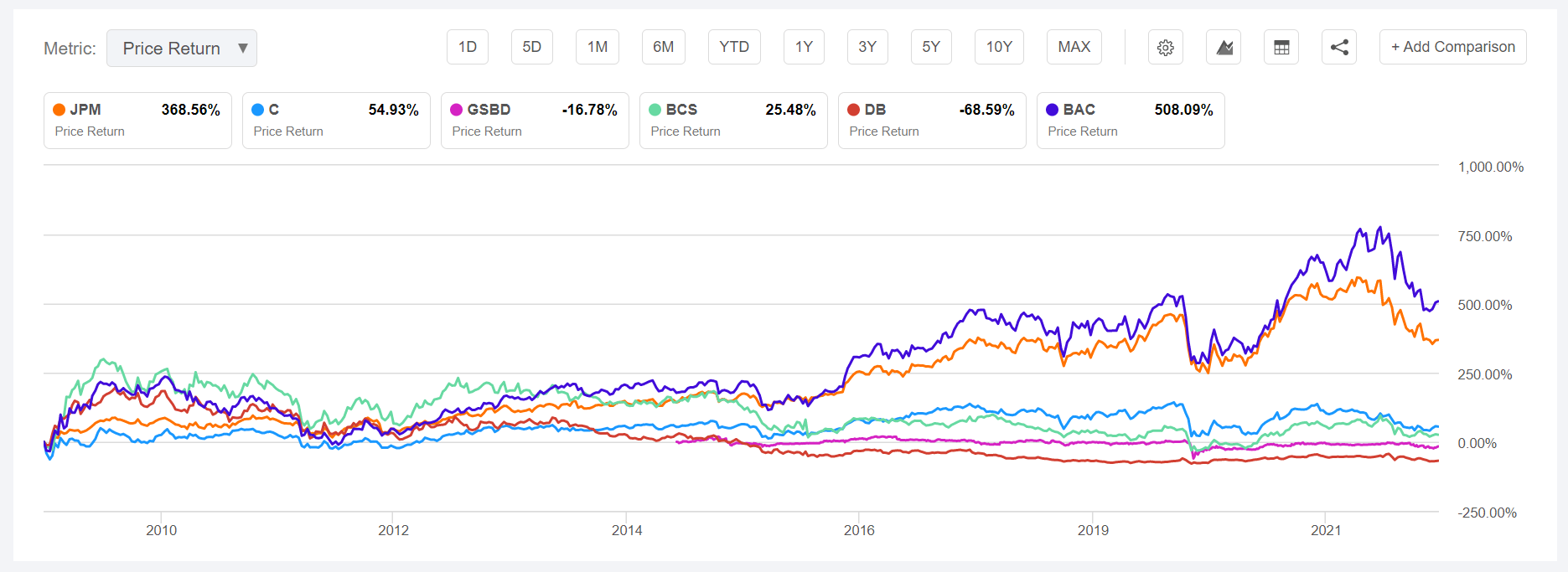

I acknowledge that ever since the financial crisis, Citigroup has strongly underperformed both the market and industry peers. This is likely a reason why sentiment is lagging the bank’s fundamentals. Or in Buffett’s thinking: Investors are still fearful when they actually should be greedy.

Seeking Alpha

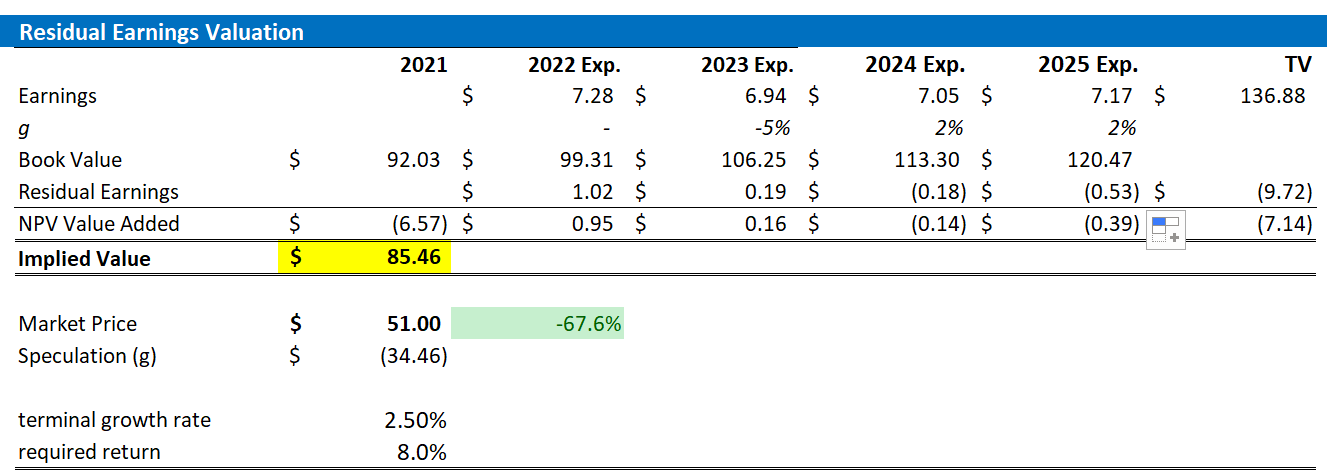

Personally, I believe Citi should trade close to x1 P/B. This estimate would be consistent with my $85.46/share target price that I derived from a residual earnings valuation.

About Citi

Citigroup is a highly diversified financial service company and the fourth biggest bank in the US. The company has approximately 200 million customer accounts globally and total balance sheet size of $2.381 trillion (30 June 2022). Operating in more than 160 countries, Citi has for a long time been considered as the ‘most global’ bank. In 2021, Citigroup has been ranked as number 33 in the Forbes 500 list.

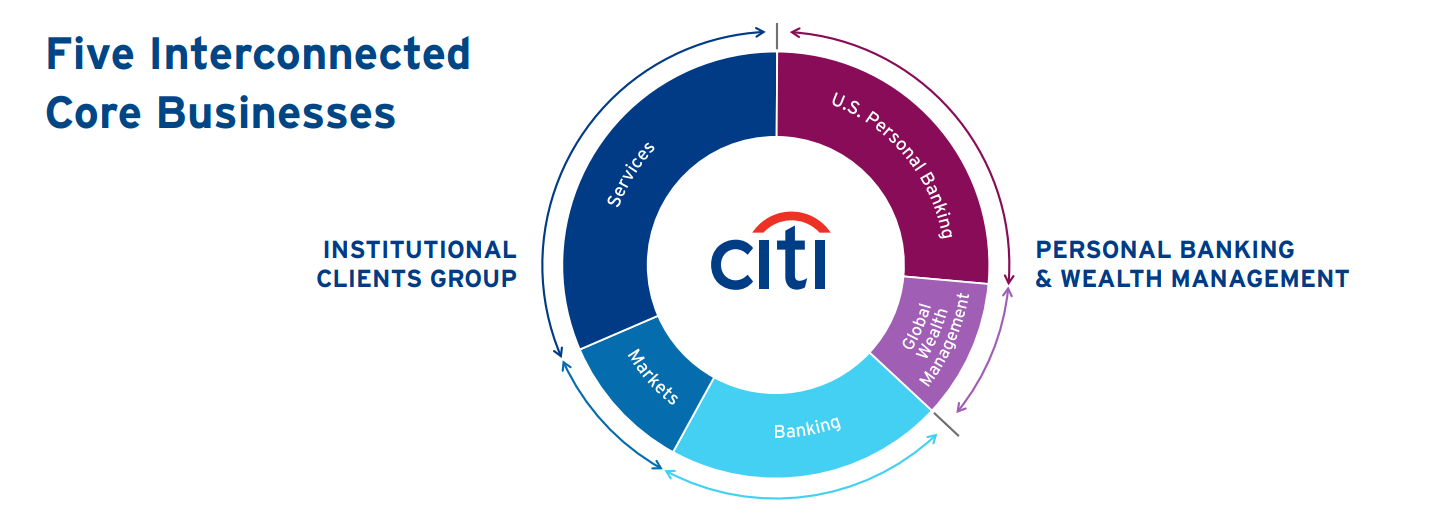

Citi operates multiple banking franchises: As a percentage of revenues, institutional clients group is the most important segment, accounting for about 30% of total sales, followed by US personal banking with 25%, Banking with 20% and Global Wealth Management and Global Markets with about 8-10% each.

Citi investor presentation

Most notably, Citi is a top player in all segments, with #1 in Treasury and Trade Solutions, #3 in Wealth Management in Asia and competitive positioning in investment banking and global markets.

Citi investor presentation

Citi’s highly diversified portfolio strength is very important, I argue, as it protects the bank from economic downturns and markets turmoil to a certain degree. For example, consider the recent past: in an environment of near-zero interest rates and steady markets, Citi’s investment banking and wealth management franchise perform well. In a stressed market, Citi’s global market division is poised to benefit. And rising interest rates support higher income from retail banking.

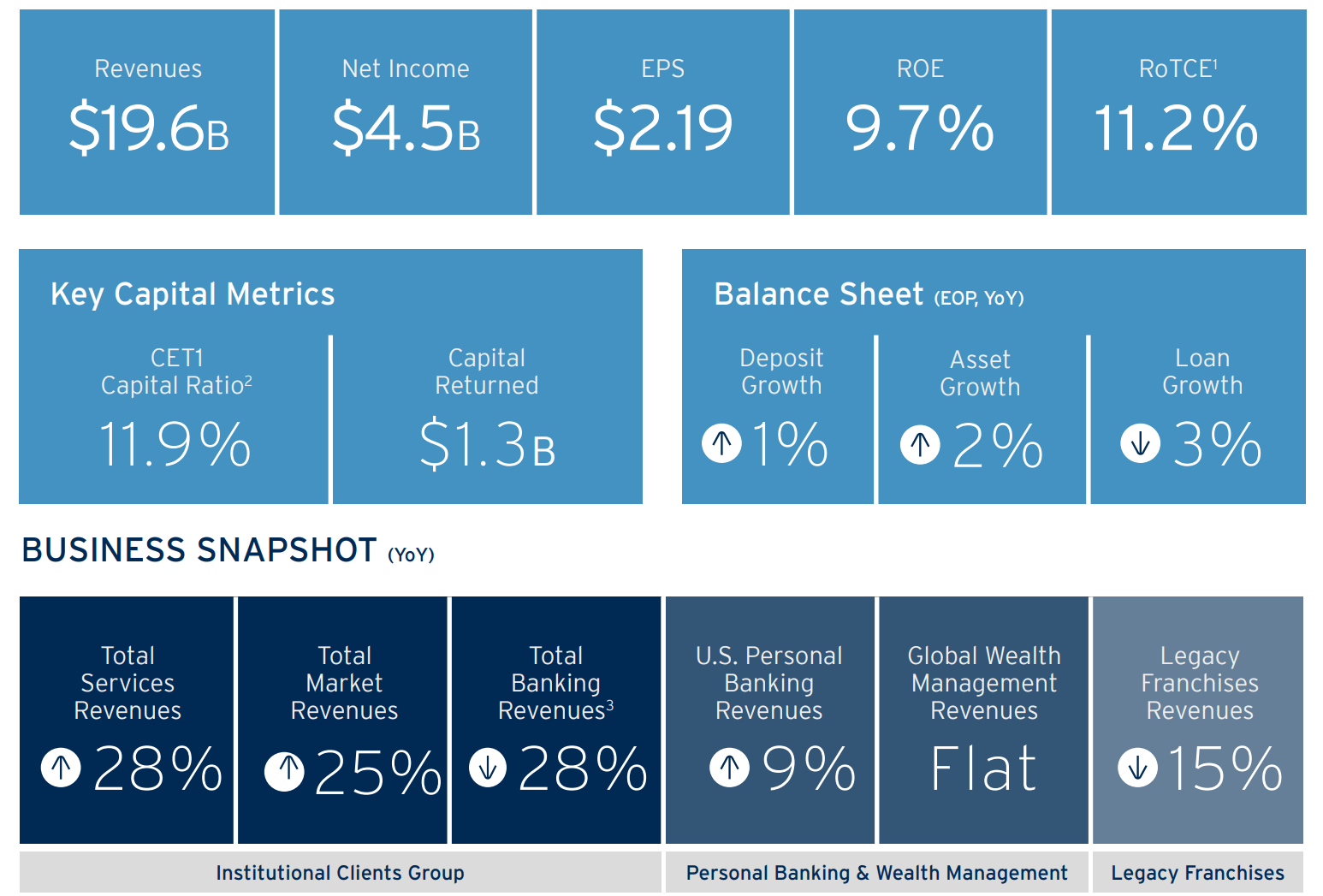

To support Citi’s fundamental attractiveness, consider the June 2022 quarter, which was pressured by a weak macro economy (negative GDP growth). From April to end of June, Citi generated $19.6 billion of revenues and achieved a net-income of $4.5 billion. Notably, almost all business segments grew double digit year over year, except global wealth management which remained flat.

Citi investor presentation

Very Attractive Valuation

Citi stock is very cheap as compared to US banking peers. For reference, Citi trades at a P/E of x7, P/S of x0.8 and a P/B of x0.55, while JPM trades at a P/E of about x10, P/S of about x2.5 and P/B of almost x1.5. Thus, it is fair to say that JPM is almost double as expensive as Citi.

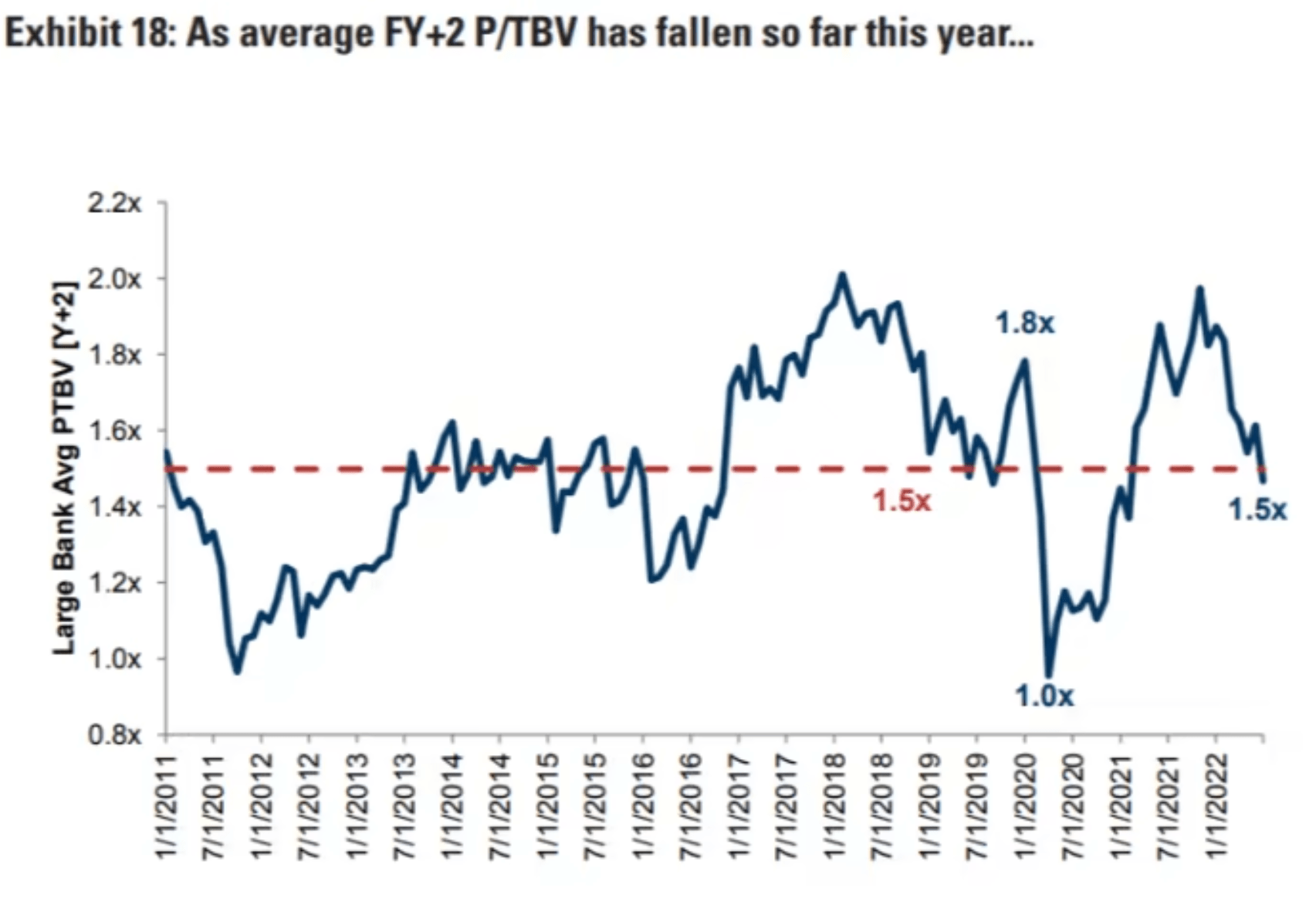

While I think that JPM is fairly valued at x1.5 P/B (a premium is justified for the industry leader), I argue Citi is strongly undervalued. According to research by Goldman Sachs, the cyclical low for bank stocks is usually around the x1 P/B multiple, and the historical average is somewhere around x1.5. That said, Citi currently trades at about half the P/B multiple that investors would expect in a cyclical downturn.

Goldman Sachs Research

Residual Earnings Valuation

In my opinion, banks are prime candidates to be valued with a residual earnings (“RE”) valuation, given that the RE framework anchors on both the income statement and the balance sheet as well as accrual accounting. That said, I apply the following assumptions:

- To forecast EPS, I anchor on consensus analyst forecast as available on the Bloomberg Terminal ’till 2023. In my opinion, any estimate beyond 2023 is too speculative to include in a valuation framework – especially for banks.

- To estimate the cost of capital, I use the WACC framework. I model a three-year regression against the S&P 500 to find the stock’s beta. For the risk-free rate, I used the U.S. 10-year treasury yield as of August 01, 2022. My calculation indicates a fair required return of about 10%.

- To derive Citi’s tax rate, I extrapolate the 3-year average effective tax-rate from 2019, 2020 and 2021.

- For the terminal growth rate, I apply 2% percentage points, less than the 3% nominal GDP growth, which I think is a fair assumption for an industry leader.

Based on the above assumptions, my calculation returns a base-case target price for Citi of $85.46/share, implying material upside of almost 70%.

Analyst Consensus Estimates; Author’s Calculation

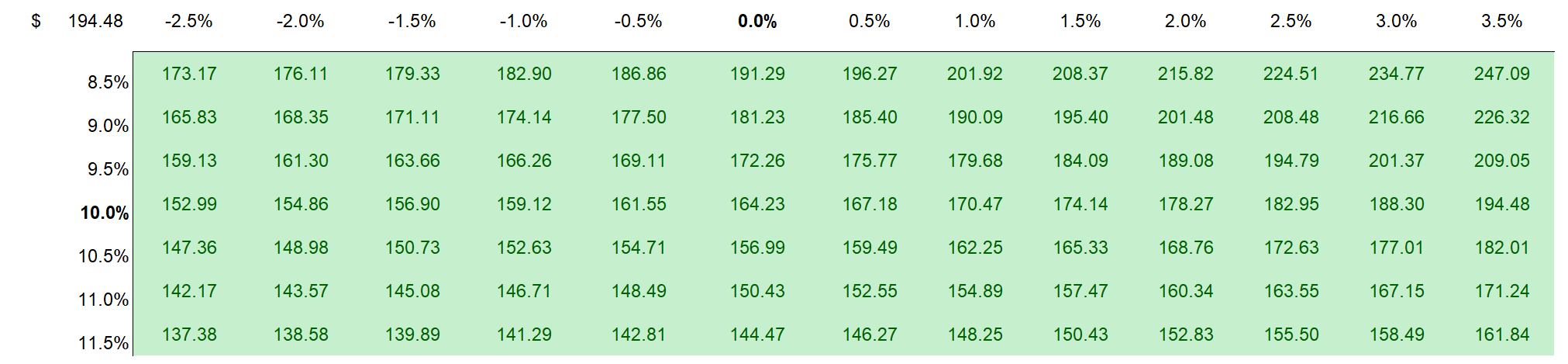

I understand that investors might have different assumptions with regards to Citi’s required return and terminal business growth. Thus, I also enclose a sensitivity table to test varying assumptions. For reference, red-cells imply an overvaluation as compared to the current market price, and green-cells imply an undervaluation.

Analyst Consensus Estimates; Author’s Calculation

Risks

While I believe that investments in banks are less risky than the market implies, the tail-risk exposure is still elevated and if materialized this might depreciate Citi share-price significantly. For reference, take the great financial crisis as an example, which crippled many bank stocks for multiple year, if not decades. In any case, Citi’s 11.2% CET1 ratio should buffer the company for most market stress scenarios. Jane Fraser, Citi CEO, said:

These results (FED stress test) again demonstrate that Citi has the capital to withstand a severe economic downturn. We have capacity to maintain the current common dividend of $0.51 per share in a range of stress scenarios

Conclusion

Given a deeply depressed valuation in combination with attractive fundamentals, I like the risk/reward for Citi. In my opinion, market sentiment is lagging the bank’s potential. As I value the bank based on a residual earnings model, I see about 70% upside. My target price is $85.46/share.

My other articles about US banks:

Be the first to comment