imaginima

Ring Energy (NYSE:REI) just announced an increase in lease holdings due to the closing of the Stronghold acquisition. After the quarter closed, there was the announced special meeting that would allow the company to issue enough common shares for the preferred stock in the deal to convert. So, the outstanding and fully diluted shares will change in the fourth quarter. Even with that detail, the purchase is looking better all the time.

Diamondback Energy (FANG) announced Midland Basin acquisitions. I have long maintained that the profitability in the Midland (and surrounding areas) area is comparable to far more expensive acreage where the company has long made acquisitions and has major operations. The entrance of a top-notch operator into the acquisition game confirms that this acreage is likely to get more valuable in the future. That is very good news for Ring Energy shareholders.

Newly Acquired Acreage

The latest Ring Energy acquisition is fairly cheap to develop. Current prices assure a quick payback period. That makes it very easy to raise production on a relatively low capital budget because the same capital can be used from the quick payback to drill more than one well during a fiscal year.

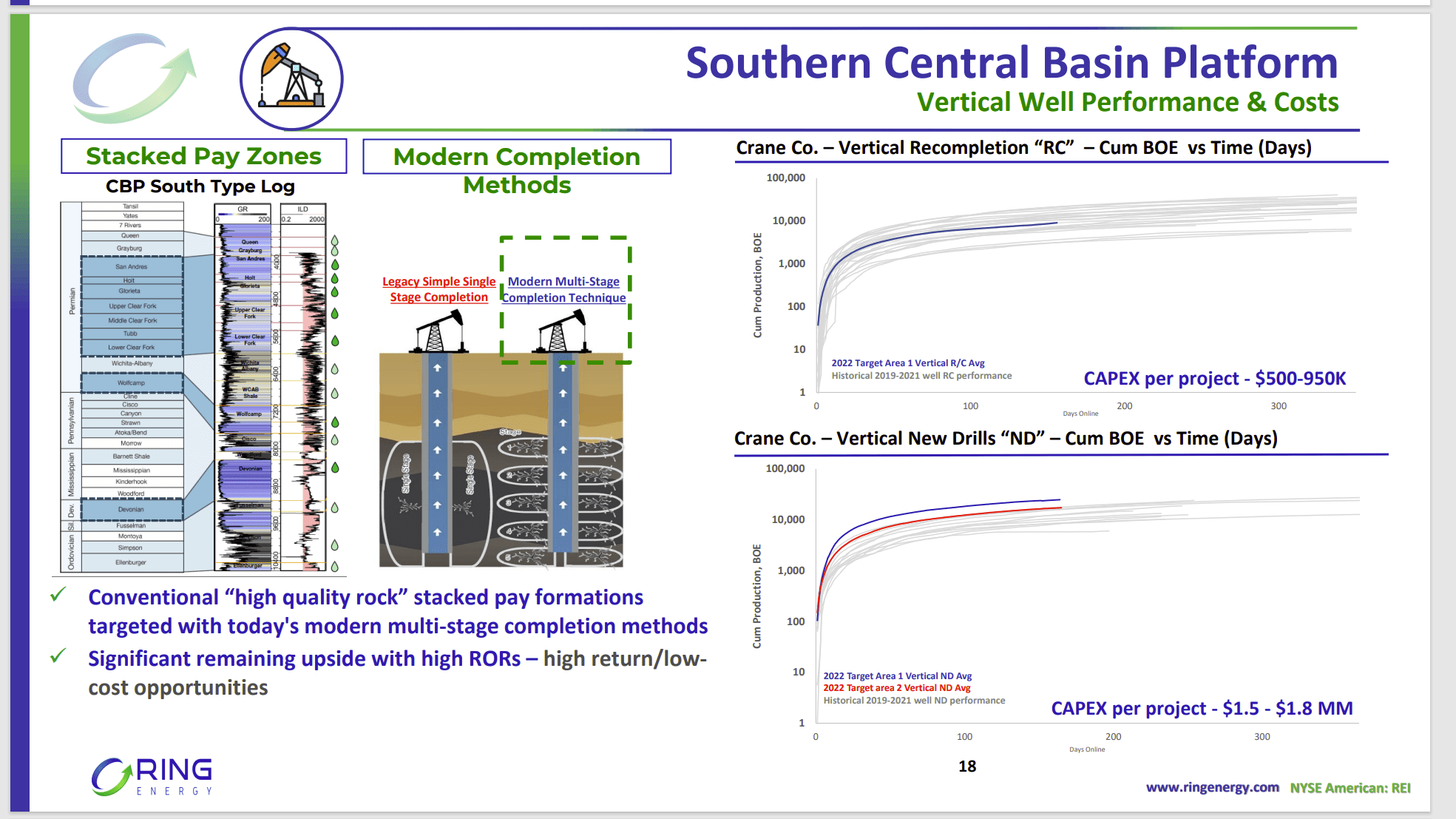

Ring Energy Description Of Stronghold Acreage Advantages (Ring Energy Corporate Presentation December 2022)

The new acreage has a fair number of rework projects where the wells are already drilled and producing but just need modern completion techniques. Since the initial flow rates are similar, it makes sense to target the rework projects where it is feasible to do so. This opportunity undoubtedly made the reduction of capital that was announced a reality.

It probably goes without saying that management will likely at some point consider horizontal wells on this acreage because sometimes horizontal wells have better profitability. But for the time being, this company has a huge advantage over many competitors in that this conventional opportunity is dirt cheap to develop. So, activity can be ratcheted up or down easily.

Legacy Acreage

The company will continue to drill the legacy acreage because that acreage can compete with the newly acquired acreage for capital. Management also mentioned during the conference call that it is better right now to move the drilling rig as indicated to avoid overwhelming the supporting infrastructure in any one place. Then management does not have to invest in more infrastructure right now. This will maximize free cash flow.

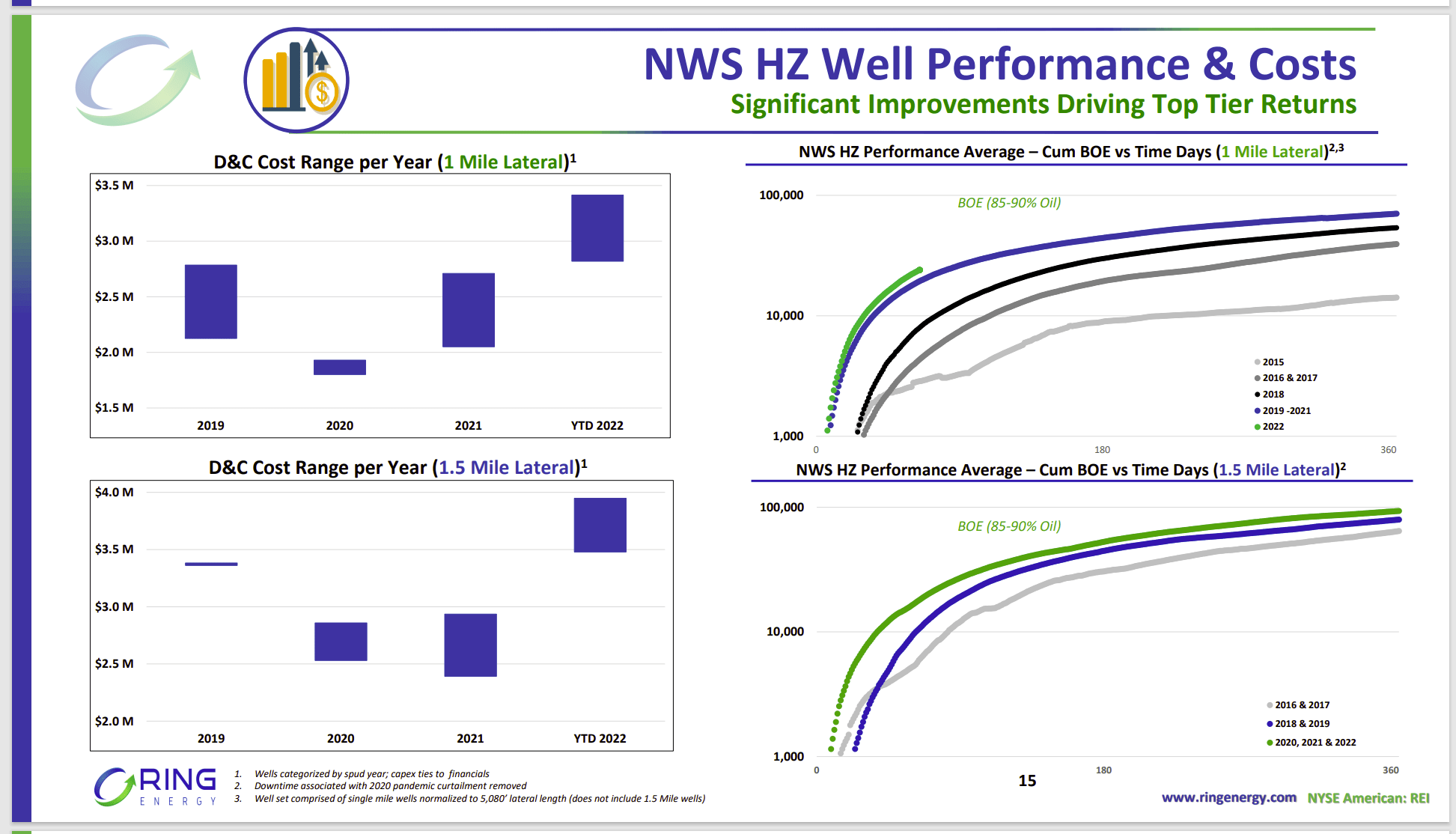

Ring Energy Summary Of Northwest Shelf Acquisition Advantages (Ring Energy Corporate Presentation December 2022)

The Northwest Shelf is the more profitable of the legacy acreage. Wells here also pay back quickly and are relatively cheap as this is considered a conventional opportunity as well. That saves some costs and time when compared to the unconventional. The completion costs shown above are relatively cheap as a result.

These wells have a very long production life of roughly 35 years whereas many unconventional wells are considered to have a production life in the 20-year range for many of the companies I follow. The breakeven point for these wells as a result is very low. Management mentioned the oil price of $25 to $30 depending upon the location and the well type. This is actually a world-class low-cost breakeven price. Many competitors have higher well breakeven prices and they paid a lot more for the acreage.

During the conference call, management stated that they needed an oil price (probably a received price but the conversation was unclear and started by using WTI) in the $50 range. That included the corporate costs because they were not going to drill if the corporation did not make money including the corporate overhead.

The Fine Print

The hiccup or the market worries have centered around finances. Finances before the pandemic were considered conservative. But the company never was able to completely changeover from a startup stage to an operating stage. The very low commodity prices during the pandemic changed the lending attitude toward the debt almost overnight. That made the latest acquisition far more important.

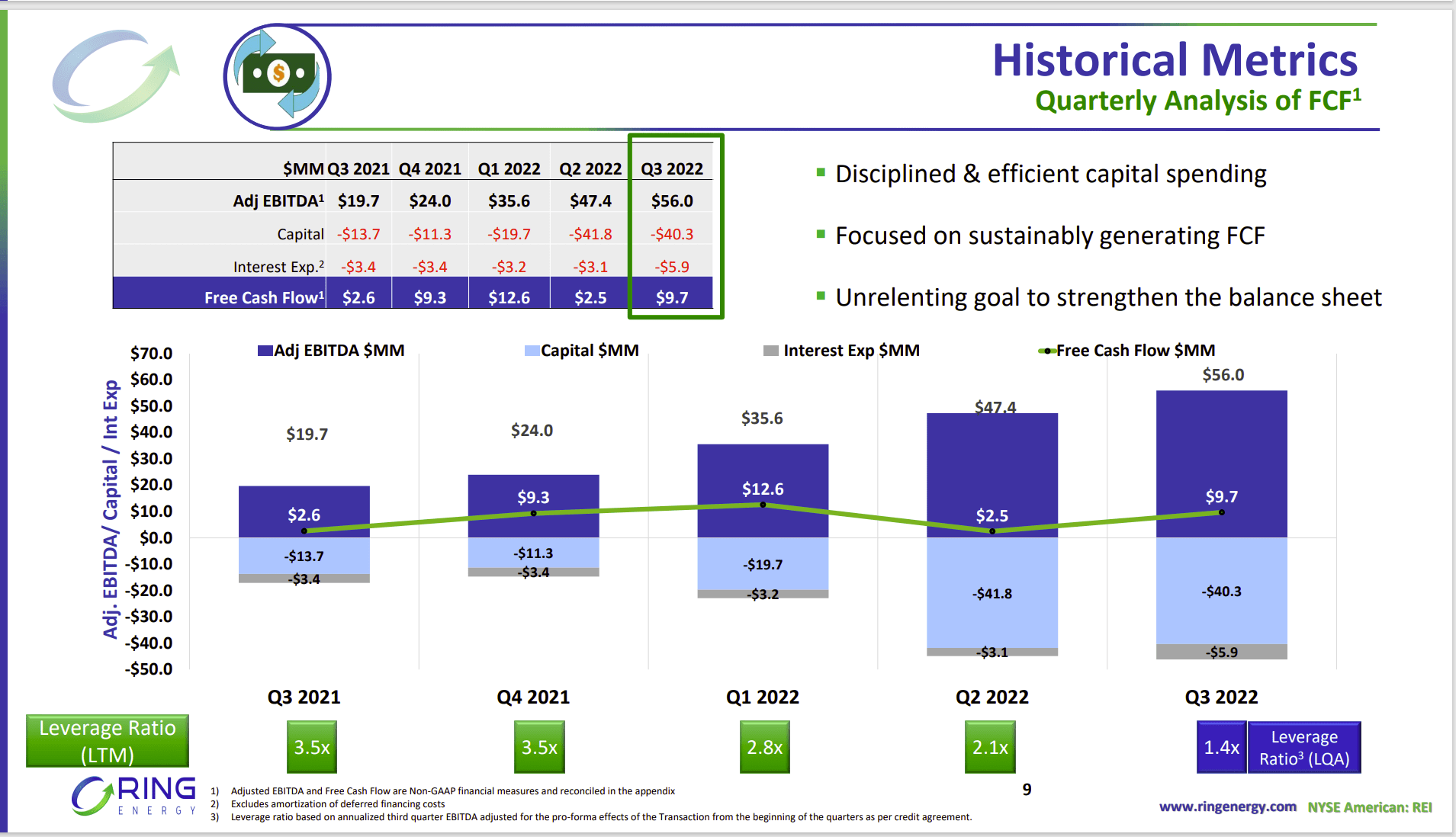

Ring Energy Free Cash Flow History (Ring Energy Corporate Presentation December 2022)

Had the pandemic never occurred, the pathway to free cash flow with very profitable production was straightforward. But lenders clamped down on debt during the pandemic which forced most upstream companies to solely use cash flow from continuing production.

This company actually shut down production completely for a little bit while living off the hedging program for cash flow. That probably did not excite lenders at all. Since the pandemic, there has been an emphasis on living within cash flow. This was a change from drilling until the production was at desired levels to maximize efficiencies and maximize profits. The earnings press release shows the debt balance up about $145 million from the previous quarter in the last fiscal year. The new $435 million balance is all that was needed for the company to basically double production very profitably. Admittedly, this discussion skips the purchase price and some repayments because the general idea here is that the company doubled production without coming close to doubling the debt load.

Combined with the announced capital budget decrease, this new situation implies greater free cash flow going forward to repay debt. Most companies in the current situation of this company will prioritize repaying debt until the debt ratio is considered conservative at considerably lower commodity prices. This strategy matches the new lending market demand for balance sheet repair first regardless of the situation that got the company in the present condition.

But the company has some very cheap projects to maintain production as shown above. Continuing technology advances and some relaxation in the lending market are liable to allow slow production growth that would result in faster repayments.

The Future

The Stronghold acquisition has given Ring Energy management some badly needed breathing room. Production levels doubled the minute the acquisition closed while debt levels did not come close to doubling. Management indicates they will look for more of these kinds of deals. That is exactly the pathway a lot of financially stressed companies are quickly getting the leverage ratios into market accepted ranges.

This company still has the ability to drill its way out of the situation because the wells are very profitable. But that is not likely to happen until management has access to the bond market at reasonable costs. Clearly, that is not the case right now or they would not have the debt on a bank line.

Lending requirements should relax as the economic recovery gets underway. But the market is going to need assurances that the economy will not crash in the future as it did in 2008 and 2020 (not to mention the big price oil decline in 2015). Business and stock prices do well with consistency (even if that consistency is not ideal). Right consistency is the norm. Should a record be established with long-term consistency and predictability, then the lending market will relax to some historical levels. That would allow faster growth for this company.

Probably the most unnoticed possibility is that companies like Diamondback have noticed profitability in the area and are now acquiring acreage. Should that continue, the acreage that this company has could become very valuable given the profitability of the wells drilled.

Be the first to comment