JHVEPhoto

There is a potential doubling down opportunity for Alphabet Inc. (NASDAQ:GOOG) (GOOGL), whose stock is about to complete a double-dip.

Even though there is a risk that Google stock will test its recent low ($83.45), I believe the risk/reward trade-off for Google is extremely compelling, given that Google is the world’s largest search engine and owns extremely valuable digital real estate.

I also believe that the company’s advertising sales will recover in 2023 as advertisers return to the world’s largest digital advertising platform.

Google’s Ad Sales Are Set To Rebound

Google stock hit new lows in October, following the release of third-quarter earnings. The selloff was triggered by growing concerns about Google’s sales growth in a market experiencing advertiser pullback, which resulted in Google reporting only 6.1% YoY growth in 3Q-22. This is the slowest growth rate since 2013, and it is primarily due to lower ad sales.

Google’s ad sales increased only 2.5% YoY in 3Q-22 to $54.5 billion, and advertisers are likely to slow their ad spending into 2023 as uncertainty about a variety of factors, including GDP growth, inflation, and the Ukraine war, lingers in the market.

In the long run, Google provides advertisers with one of the most coveted features of an advertising platform: the Google search engine remains the most popular website in the world, and for that reason alone, Google will continue to be a draw for advertisers, even if they are currently cutting back on ad spending.

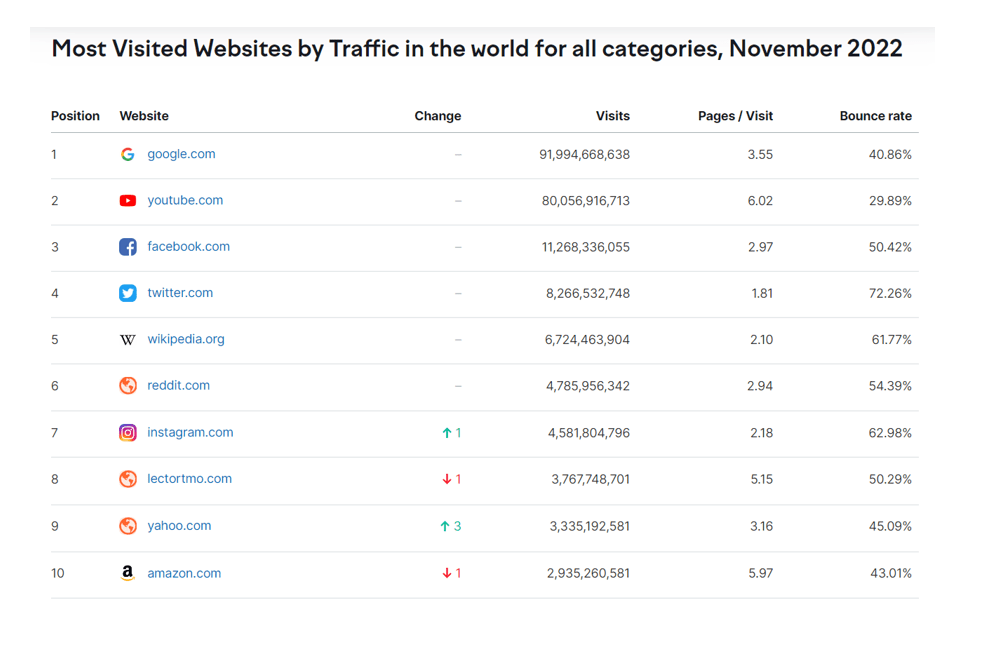

Google also owns the world’s second-most popular website, Youtube.com, giving it a large moat and a significant competitive advantage over other search engines. Google receives approximately 92 billion monthly visits, whereas YouTube receives 80 billion monthly visits. Nothing else, not even Facebook, comes close.

Most Visited Websites (Google)

A company that owns the world’s two most popular websites undoubtedly brings the most advertising value to the table for companies looking to capitalize on this ad opportunity.

Given the massive number of monthly visits, I can’t help but believe that advertisers will return to the platform once they have a better idea of where the U.S. economy is headed in 2023.

Google Is Double-Dipping And I Am Buying

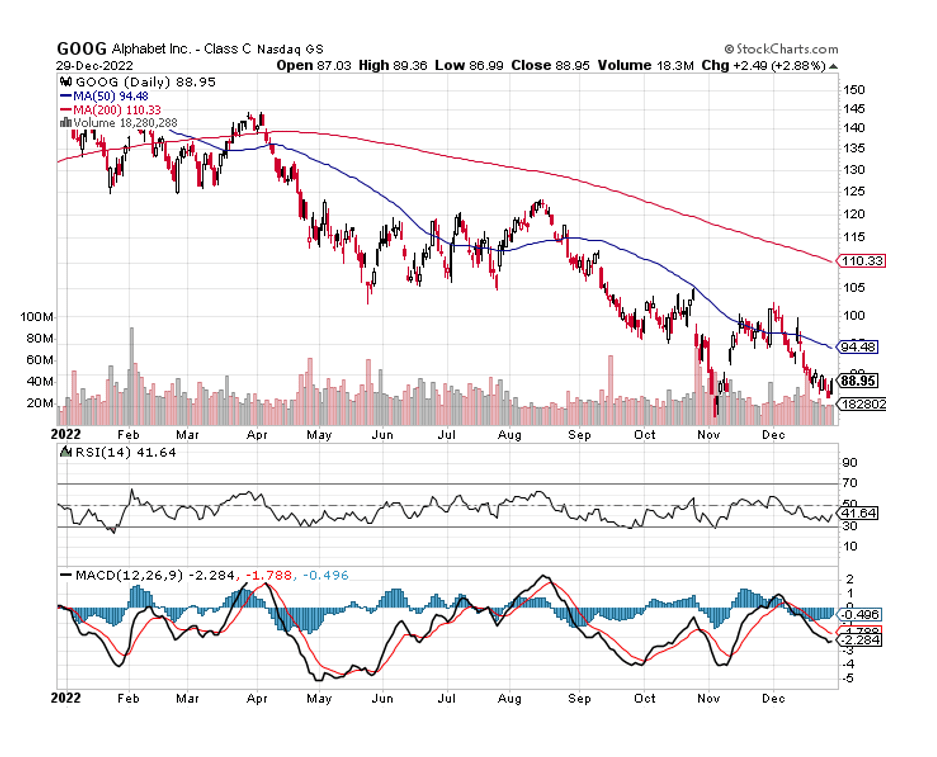

In October, but also in December, Google stock was rejected at the 50-day moving average line. The chart appears to be in the final stages of a ‘double-dip’, which occurs when a stock falls to the same support level twice in a row, only to recover and potentially reward risk-takers with above-average returns.

While it is possible that Google will test its previous low of $83.45, I believe that Google’s wide moat (ownership of the world’s two most visited websites, enormous lead over competition in terms of number of visitors) and attractive valuation make GOOG a very compelling buy right now.

Moving Average (Stockcharts.com)

Google Is A Steal

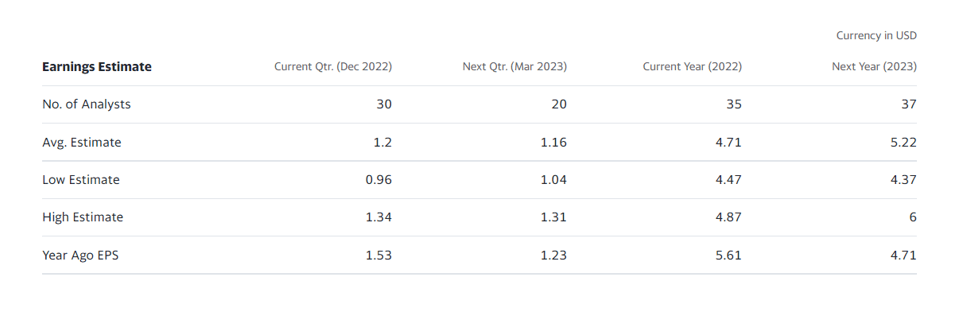

Google is vastly undervalued in my opinion, and the current valuation reflects a very high margin of safety. Google’s average earnings estimate for 2023 has dropped $0.22 per share to now $5.22 per share, implying that the market expects earnings to grow by 11% YoY. With Google stock trading at $87.87 at the time of writing, this estimate translates into a P/E-ratio of 16.8x, which is nothing short of a steal.

Earnings Estimate (Yahoo Finance)

Why Google Could See A Lower Valuation

Google’s advertising sales growth prospects in 2023 are directly related to advertisers’ willingness to spend more money on digital ads. I believe that the advertiser slump that has driven Google stock to a new 52-week low in October is a one-time occurrence because Google operates a massive digital search platform.

The current advertising market downturn is also heavily influenced by inflation, which has caused advertisers to quickly cancel advertising campaigns but does not represent a long-term trend. An increase in optimism in the digital ad space (possibly in 2023) could quickly return advertising dollars to Google.

My Conclusion

I believe that Google’s current chart situation makes it a compelling time to double down on the tech behemoth and potentially profit from an advertising market recovery in 2023.

Google and YouTube are the world’s most visited websites, making them extremely valuable digital real estate. As advertising recovers (for me, this is a question of when, not if), I believe advertisers will return ad dollars to Google and YouTube, and ad sales will rebound strongly.

It would be a huge mistake to write off Google just because ad sales growth has slowed to the single digits in 2022, and the valuation, with a P/E ratio of 16.8x, is quite compelling.

Be the first to comment