PM Images

The iShares Residential and Multisector Real Estate ETF (NYSEARCA:REZ) is a REIT ETF that tracks a lot of key exposures mostly in the US market. There’s a lot of residential exposure, but also some healthcare and specialised exposures. Critically, there’s little office exposure. Overall, the composition of the ETF is good from a real estate perspective, but we just don’t think the time is yet right for real estate. China coming back could put too much pressure on global inflation for rates to ease quickly.

Quick Look at REZ

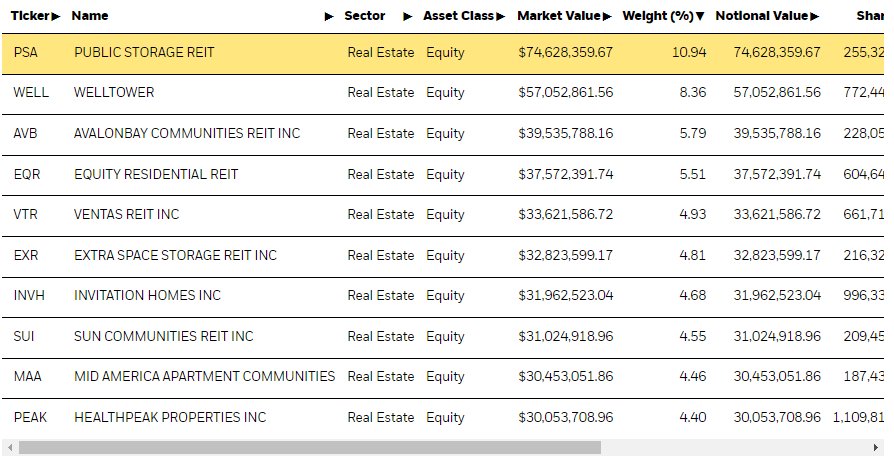

REZ is somewhat skewed to some large holdings in Public Storage REIT (PSA) and Welltower (WELL) which together make almost 20% of the overall exposures.

Top Holdings (iShares.com)

Specialty exposures like PSA aren’t so limited, with 22% of the portfolio allocated to specialty REITs like that. Welltower gets categorised as a healthcare REIT, which make 29% of the overall portfolio. The residential exposures do make the brunt of the exposures at 50%, beginning with AvalonBay (AVB) at 6%.

Expense ratios are rather low at 0.48% and yield is not too bad at 3.37%.

Bottom Line

The lack of office exposures is quite attractive. There is quite a lot of leverage in the office real estate world, and we are not convinced that it will make a total comeback, much like the disrupted retail a decade ago. While that would have been an idiosyncratically unattractive element of the portfolio, REZ cannot hide from the broader issue of rates.

In our previous coverage on the rate situation, we pushed back against commentators who continued to insist inflation was some out-of-control force. Inflation is easing, not least for base effects, but also because of economic pressure in Europe that cannot be fixed with any sort of immediacy. The issue is the easing inflation is also coming from the fact that China has been dormant. This may no longer be the case.

In retiring the COVID-zero policies, and in moving rapidly to protect wealth in the Chinese housing and developer markets, China is beginning to rev up into a higher gear. Years of virtually zero traveling means China will be on the move again, even just to visit families on regional flights, but also as tourists abroad. Commodity demand is going to rise, with China being a massive commodity importer as the local economy restarts fully.

At the same time, activity in China will also mean sickness of vital workers, and supply chain issues from Chinese capacity could reinitiate while demand continues to build. Inventory buildup that has been accomplished across industries thanks to the cooling off of most economies may reverse again, and inflation could come back.

The issue is that the Chinese impact on global commodity markets is sharp. This may cause the Fed to maintain higher rates as supply side pressures begin to remount. Indeed, they have already tried to prep markets that they’d keep rates high, but without a clear economic imperative, markets didn’t necessarily believe them. We think that changes now. Property markets will continue to be under pressure as the rate cycle proves longer than many expect, and we may see another drawdown in equity markets too which will probably hit REITs.

Overall, people may not be considering how the fortunes of China are the misfortunes of the US real estate markets. We would avoid this ETF for now.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment