tianyu wu/E+ via Getty Images

Innospec (NASDAQ:IOSP) manufactures specialty chemicals that are used in fuel additives, agrochemicals, oil refineries, and various fuel manufacturing processes. As the company markets the majority of its products to fuel manufacturers, these chemicals improve fuel efficiency, boost engine performance and reduce harmful emissions.

The company operates majorly in the following segment,

Fuel specialty – where the company provides additives to improve fuel efficiency, which plays a very important role in the automotive, marine, and aviation sectors.

Performance chemicals – through this segment, the company offers technology-based solutions focused on personal care, home care, and agrochemical products.

Oilfield services – the segment manufactures chemicals that are used in the oil and gas production process.

With the aim of developing and acquiring innovative products, the company invests a significant amount of money in acquisitions along with research and development, which further strengthens the business model.

Although the company faces significant competition from various small competitors, the company has gained a significant market share, which shows that the company has some underlying competitive advantage. Innospec also operates in such segments where the company is the only producer of that specific chemical, like the tetra ethyl lead segment; such operations could provide favorable returns resulting from a lack of competition.

Furthermore, as the business performance seems to be improving and the management is actively seeking growth opportunities, the operating results might improve in the upcoming years. But my main concern will be the higher valuation of the stock, which can hamper shareholders’ returns.

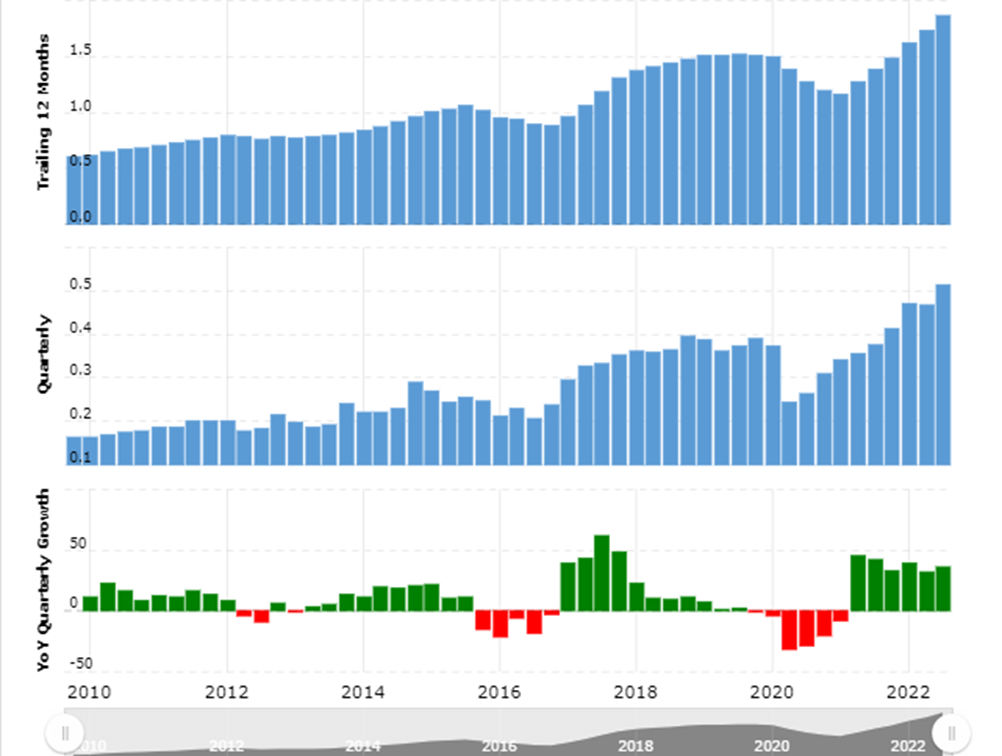

Historical performance

Revenue (macrotrend.net )

Over the period of time, revenue has seen slow but consistent growth; as a result, revenue grew from $776 million in 2012 to about $1.4 billion by 2021. Despite such consistent growth in the business operations, the net profits have remained volatile during the underlying period.

Although the growth in the revenue couldn’t match the growth in the net profits, the company has seen significant improvement in cash flow from operations; as a result, the company has generated huge cash, which has been used for acquisition, debt repayment, and dividends to produce value for the shareholders.

Due to its strong business performance in the last few years, the company has paid down substantially all its debt and become debt free.

In the year 2009, when the industry-wide pricing had dropped, the company had suffered significantly. As a result, the stock price dropped over 86%. Still, since then, as the management kept on adding new products with efficient capital allocation, the stock has turned multi-bagger and has given returns over 35 times to its shareholders in just 12 years. Such a performance is primarily attributed to management efforts and intelligent capital allocation.

Strength in the business model

Management’s capital allocation decisions seem considerably attractive; as a result, over time, the company has produced huge returns to the shareholders despite working in a commodity type of business.

Furthermore, as the company has been spending a considerable amount of money on research and development, launching a new and innovative product might help drive up revenue in the coming years.

Also, the company has become debt free, which provides significant strength to the business model as compared to its peers who are suffering from debt burdens. In my view, Innospec has a substantially strong financial position, which can help the company sustain itself in the business even in adverse economic conditions.

Risk factors

The business model is substantially sensitive to the capital spending by oil and gas companies; any reduction in oil extraction might affect the operating performance. Due to the majority of its revenue coming from sales to oil refineries, historically, the business performance has been considerably volatile and expected to remain volatile in the future.

Improving business profitability in the last few quarters might be attributed to favorable industry dynamics in the oil refining industry. The oil and gas industry is known for its significant volatility in demand and supply; any significant reduction in oil prices and demand might put significant pressure in the company’s margins.

The current stock price seems considerably high for the slow-growing and cyclical stock. If the margins started deteriorating, as seen in the historical business performance, the stock price might collapse. Also, even if the margins sustain at this point, the stock may not offer desirable returns to the shareholders due to its high valuation.

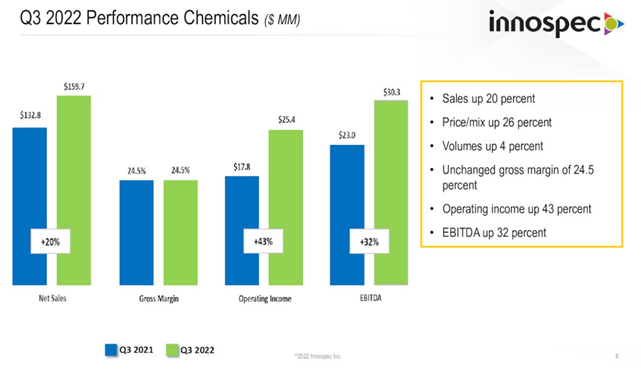

Recent development

Quarterly performance (investors relation )

In the recent quarter, the company has produced over $513 million in revenue as compared to the revenue of $376 million in the same quarter last year; the increase is attributed to favorable pricing and product mix. Also, the company has enjoyed strong profitability resulting from higher margins.

Over the previous nine months, the company has generated huge returns resulting from favorable pricing trends. The investor must consider that, as the company operates in the commodity business, such pricing may not last long.

Also, the company ends the quarter with over $100 million in cash and about $846 million in current assets. Having a debt-free business model with substantial liquid resources has been providing the company with a significant advantage.

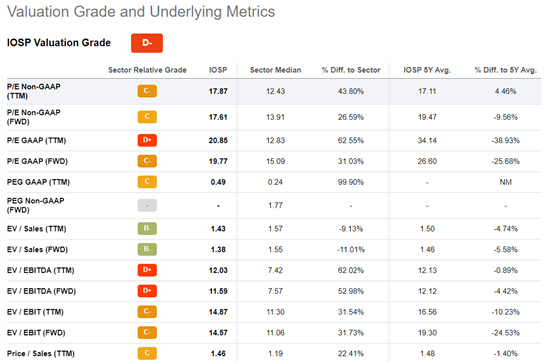

valuation (seeking alpha )

Currently, the company has been trading for about $2.7 billion, whereas it has produced over $107 million in the previous nine months. It seems that the company has been trading for about 27 times its previous nine months’ earnings. Such an earnings multiple for a slow-growing and cyclical stock seems high. Also, the current attractive performance is attributed to strong industry-wide pricing; therefore, any decline in industry demand might hurt the margins. I assign SELL ratings to the stock.

Be the first to comment