JamesBrey

Retiring on dividends from quality high-yielding stocks is a great way to meet financial needs during the golden years because:

- It provides a clearer picture of how well your portfolio is prepared to sustain your lifestyle during retirement

- It reduces the sequence of returns risk given that dividend payouts tend to be much less volatile than stock prices

- It can enable you to retire sooner than you would under the 4% Rule.

- It can give you peace of mind during market crashes since your retirement income stream is not dependent on where stocks trade at any given time

With these pros in mind, here are three conservative 9-10%-yielding investments that can facilitate a rich and happy retirement.

#1. Blackstone Secured Lending Fund Stock (BXSL)

BXSL has arguably the best dividend in the entire BDC sector (BIZD) given its very attractive 10.1% yield, strong dividend growth momentum, and the safety of its payout.

In fact, it has the highest yield among its large blue-chip peers, including Main Street Capital (MAIN) and Ares Capital Corp (ARCC), has the second-strongest projected dividend growth in 2024 among the six largest BDCs, and the largest dividend growth rate from 2021 through projected 2024 levels among the same group of BDCs.

Moreover, its dividend coverage ratio is quite conservative for a BDC at 1.25x on a Q4 net investment income basis and its balance sheet is investment-grade rated, further bolstering its status as a strong dividend stock. In fact, there is little cause for concern of financial distress at BXSL given that it has $1.8 billion in liquidity, a 1.0x leverage ratio (which is on the conservative end of the spectrum for BDCs), the backing of the world’s leading alternative asset manager in Blackstone (BX), very strong underwriting performance (less than 0.1% of its investment portfolio is currently on non-accrual), and 98.5% of its portfolio is invested in first lien, senior secured loans.

As a result, investors can sleep well at night knowing that their 10.1% dividend yield is likely to continue flowing into their brokerage accounts each quarter, going a long way toward meeting their living expenses.

#2.Virtus InfraCap U.S. Preferred Stock ETF (PFFA)

PFFA is a preferred stock ETF that pays out a hefty monthly dividend and currently yields nearly 10%. We are not particularly fond of preferred equities because oftentimes they give investors the worst of both worlds:

- They lack the growth potential that common equities provide

- They lack the seniority in the capital stack and contractual dividend payouts that debt investments provide.

As a result, it is very rare that we ever invest in preferred securities in our Core/International Portfolios due to their weak long-term total return prospects, and are highly selective in which ones we invest in within our Retirement Portfolio. Given that we do not think that preferreds offer much downside protection in the event of financial distress for a company, we think that only preferreds in high-quality businesses and/or a very broadly diversified portfolio are even worth investing in at all, and only then they are only worth investing in if consistently attractive income is the investment objective rather than total returns.

We therefore only invest in preferreds that combine very high and very well-covered yields with strong balance sheets and underlying business models in our Retirement Portfolio. However, PFFA is a potential exception for retirees for the following reasons:

- It offers an attractive near 10% dividend yield paid out monthly that is fully covered by internally generated cash flow.

- It is very well diversified, with 186 holdings, and is actively managed with a focus on valuation and quality.

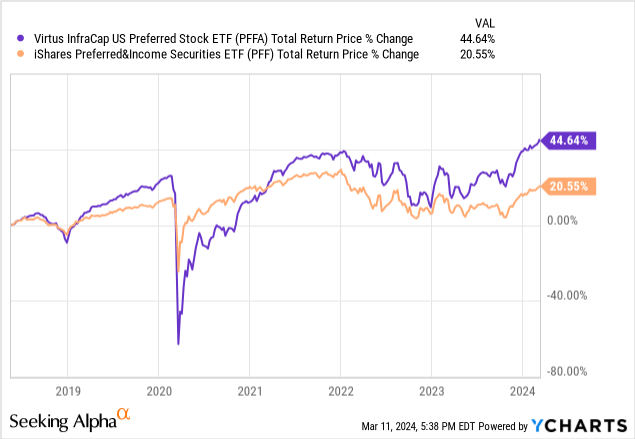

- It employs leverage fairly prudently to juice returns and its yield, combining with the active management approach to more than double the total returns generated by the broader preferred stock index (PFF) since its inception:

As a result, investors can enjoy a diversified preferred income yield of nearly 10% paid out monthly through PFFA while also resting easy knowing that it is backed by a skilled portfolio manager whose strategy has generated massive alpha over time. You can read our more in-depth thesis on it here and our recent interview with the portfolio manager here.

#3 Energy Transfer Stock (ET)

Last, but not least, ET pays out a 9% distribution yield that is arguably the safest 9%+ yielding common equity in the market today. The reason for this is that:

- It owns a large and well-diversified portfolio of strategic and mission-critical energy infrastructure assets that are mostly contracted with lengthy terms and strong counterparties.

- ~90% of its adjusted EBITDA is commodity-price resistant, making its cash flow profile very stable.

- Its balance sheet is in excellent shape, with a BBB credit rating, well-laddered debt maturities, substantial free cash flow generation, and plenty of liquidity.

- Its distributable cash flow is nearly twice its distribution payout obligation, giving it a very large cushion to support its payout even if its cash flow did take a substantial hit.

On top of the safety of its distribution, ET is investing aggressively in growth projects, enabling management to project that it will continue to grow its distribution at a 3-5% CAGR for years to come while also continuing to deleverage and buy back units opportunistically.

As a result, investors in ET can sleep well at night knowing that they are locking in a very attractive passive income stream that should not only be sustainable but actually grow faster than inflation over the long term.

Investor Takeaway

Between BXSL, PFFA, and ET investors can build a strong foundation for their income portfolios while also generating very high income yields. Moreover, BXSL – with its emphasis on investing in floating-rate loans – will likely benefit from rising interest rates, while PFFA – with its focus on primarily fixed-rate preferreds – will likely benefit from falling interest rates. ET – with its strong balance sheet, significant free cash flow, and inflation-resistant business model – is somewhat indifferent to the direction of interest rates. Best of all, all three business models are quite defensive in nature. As a result, investors who diversify across these three securities should be able to sleep well at night in just about any macroeconomic environment.

Be the first to comment