Anchiy

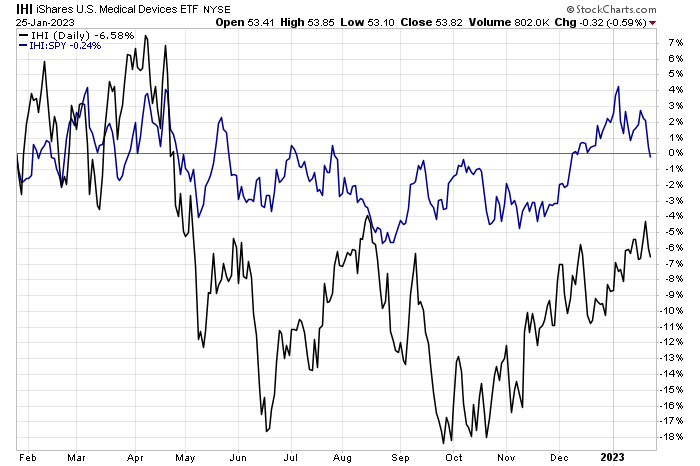

Medical device stocks are a more risk-on area of the defensive Health Care sector. Still, the group has underperformed the broad market so far in 2023 after rallying both on a nominal and relative basis during the first several weeks of last year.

Some momentum appears to be coming out of the group, but I see upside potential with one GARP name that sports a positive technical development. Let’s check out ResMed Inc. (NYSE:RMD).

Medical Device Stocks: Up YTD, But Negative Alpha

Stockcharts.com

According to Bank of America Global Research, ResMed is a leading developer and manufacturer of medical devices, masks, and cloud-based software applications that diagnose, treat, and manage respiratory disorders. Headquartered in San Diego, California, RMD is focused on connected health to deliver better outcomes for sleep apnea and chronic obstructive pulmonary disease sufferers.

The $34 billion market cap Health Care Equipment & Supplies industry company within the Health Care sector trades at a high 43.2 trailing 12-month GAAP price-to-earnings ratio and pays a small 0.8% dividend yield, according to The Wall Street Journal.

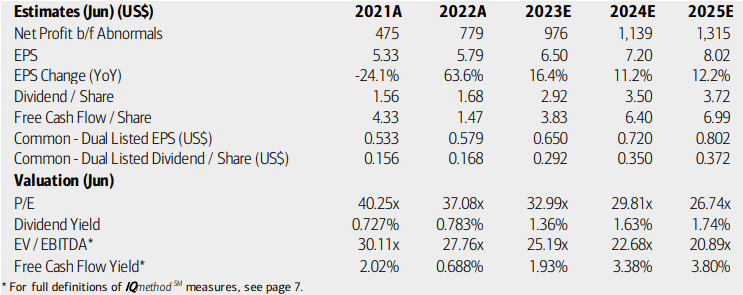

ResMed reports results this week, and analysts expect $1.62 of EPS on revenues of $996 million. Shares fell after its Q1 2023 report back in October, but then rallied to finish off the year. Fundamentally, higher production levels are expected which should help RMD increase sales this year. Margin expansion is also seen, which should boost the bottom line. Unfortunately, the firm does not issue guidance in most cases.

On valuation, analysts at BofA see earnings having risen by a strong 64% in 2022, but the firm is already operating in its FY 2023. This year’s per-share profits are expected to show more decent growth at more than 16% before earnings growth moderates to the low-teens rate. Dividends, meanwhile, are expected to rise commensurate with EPS while free cash flow also rises – helping to support shareholder accretive activities.

The sore spot for value investors is the stock’s elevated non-GAAP earnings multiple and low yield. The EV/EBITDA ratio is also high – about double that of the broad market. Here’s where I spot some value, though – the forward operating PEG ratio is just 1.43. That’s below the sector median of 2.06 and a more than 50% discount to the company’s 5-year average. So, I assert it’s a solid value for a GARP play.

ResMed: Earnings, Valuation, Dividend Forecasts

BofA Global Research

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q2 2023 earnings date of Thursday, January 26 after market close (today’s date as I write) with a conference call immediately after results are posted. You can listen live here.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

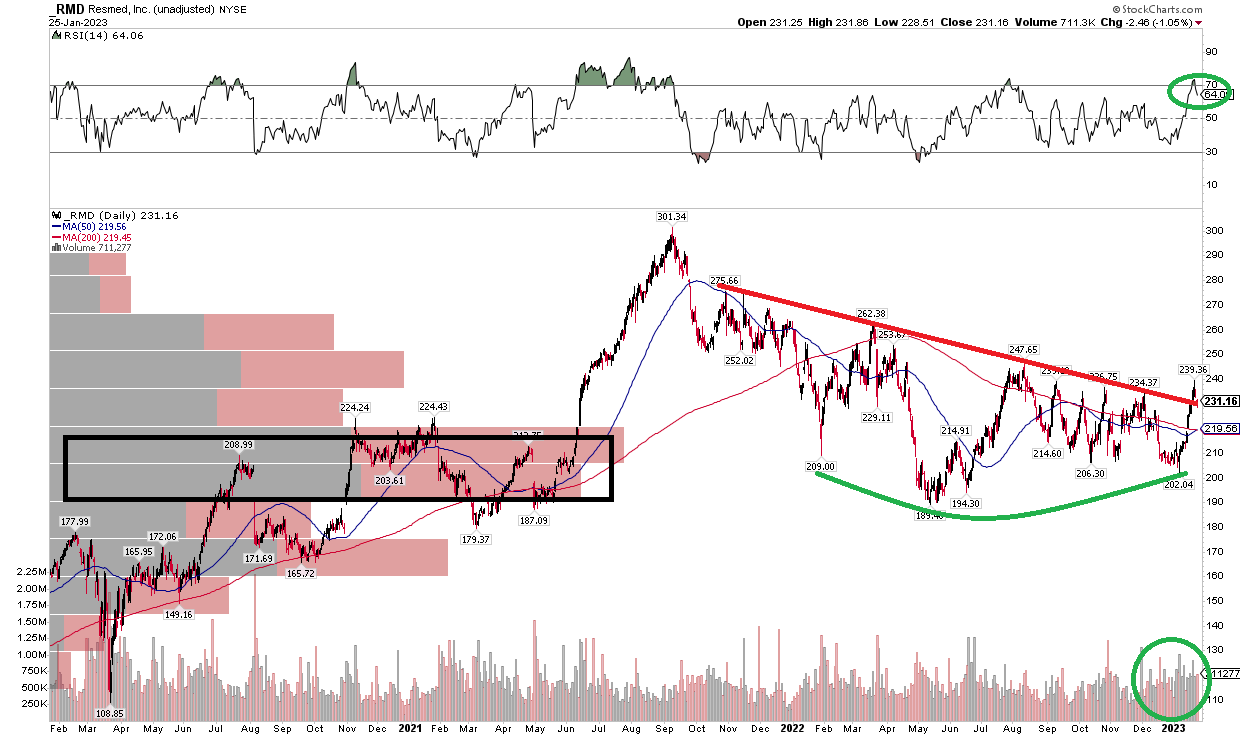

Back in November, I was a hold on RMD due to mixed technicals despite its strong earnings trends. Now, however, I see the very early stages of a bullish breakout in the works. Notice in the chart below that shares have rallied above a downtrend resistance line on high RSI momentum. This comes after RMD established a bullish rounded bottom reversal pattern with increasing volume lately. I would like to see a successful retest of the resistance line (which should now be support). But a long play with a stop under $190 is warranted.

What I also like about the chart is significant volume by price in the $190 to $220 range – that should be support on a bigger pullback. Based on the breakout thesis, a measured move price objective to near the previous high of $301 would be in play. Even without the breakout, the $240 to $260 could bring back some ‘dead bodies’ of supply from those who bought in that range and are now looking to get back to even. It’s not a 100% clear chart, but I see more bullish than bearish risks at this time.

RMD: Bearish to Bullish Reversal Signs

Stockcharts.com

The Bottom Line

ResMed is a solid GARP play with improving technicals. Better supply and production trends this year should help meet growing demand, leading to higher revenues and profitability.

Be the first to comment