Robert vt Hoenderdaal/iStock Editorial via Getty Images

Leading pest control and hygiene services specialist Rentokil Initial (NYSE:RTO) continues to offer investors a defensive option to outperform the broader macro uncertainties. In addition to its established global market position and pricing power, there remains ample room for more market outgrowth as the company expands into new regions. In the near term, consolidation is a key theme – the recently completed Terminix (TMX) deal will add strategic and financial benefits to the pro-forma entity, enhancing the through-cycle growth potential. Backed by a strong balance sheet, RTO is well-positioned for more accretive deals within pest control as well, supporting the case for the mid-to-long-term growth runway in North America and elsewhere.

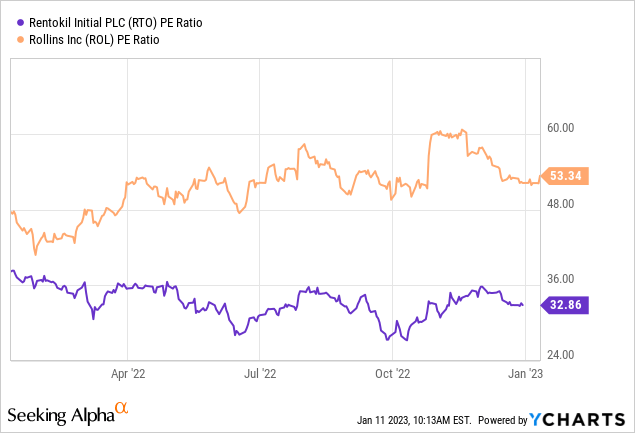

The stock has traded lower post-Q3 results, as RTO’s subpar organic growth in US pest control disappointed relative to key peer Rollins (ROL). Yet, this was largely down to one-off weather impacts and should normalize in Q4. Plus, it’s worth noting that ROL trades well above RTO on earnings, presenting a re-rating opportunity as the company delivers on its synergy targets post-TMX combination.

Q3 Disappointed, but Fundamental Strength Remains Intact

Near-term trends have been below par for RTO – pricing as of last quarter was running at 4-4.5% overall, with developing markets being the key drag. Management has guided to prices moving higher for the developing markets region in FY23, though, as it sees itself as a price setter. Things are different in North America, where RTO is a price taker. Here, the lower +3.5% organic pest control growth fell short of expectations and key peer Rollins’ Q3 growth of ~9%. Key detractors include the tougher YoY comparison and one-off weather events like the timing of hurricanes, which should fade over time.

Importantly, the overall business remains healthy, and with the TMX integration set to add significant scale, there is likely upside to the GDP plus growth runway. As for margins, RTO management seems confident in leveraging pricing power to offset cost input inflation (mainly wages), so the full-year North American margin target of 18% (~2%pts above H1) seems well within reach.

Rentokil Initial

Upside from the Synergy Run-Rate

Going forward, the execution of the TMX integration will be worth monitoring. RTO has earmarked a gross of ~$100m of operational synergies, although this is closer to a net of ~$75m after equalizing staff wages (note TMX staff wages are below RTO). In aggregate, the synergies come up to $150m. Note, however, that this headline figure excludes any benefits from productivity improvements at TMX post-wage hikes. In an ideal scenario, higher pay and employee retention should translate into higher organic growth and margins via improved customer retention; whether this pans out, however, depends on the execution.

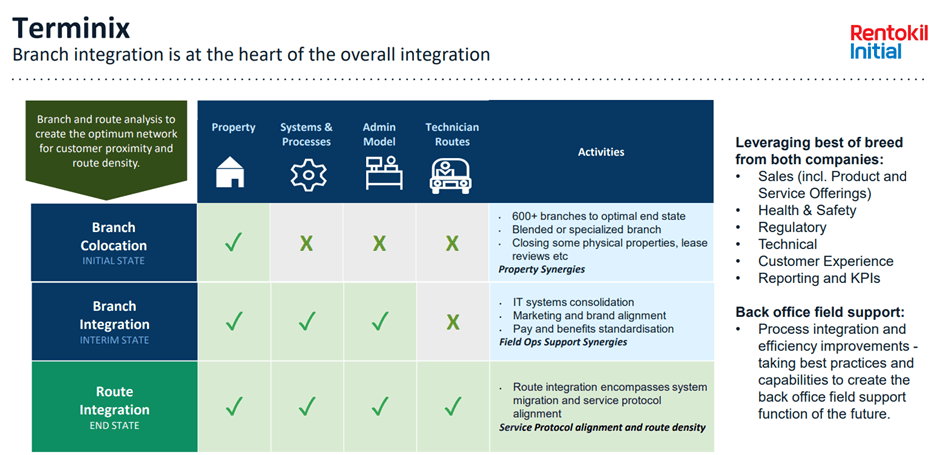

Rationalizing the branch networks will also be key – management cited a 400-branch network target by the end of the integration, implying a rationalization of ~250 branches across the RTO/TMX footprint. All in all, the path to unlocking these synergies will not be easy; while it remains early days, progress on the rebranding exercise and the IT rationalization should offer a good indicator of the merger accretion potential.

Rentokil Initial

Signs of an Upturn Heading into Q4/FY22 Results

With Q4 results coming up, I am expecting an improved set of numbers. All eyes will be on the shape of the RTO US organic growth trajectory on a standalone basis. Relative to the +3.5% print in Q3, expect Q4 to revert higher. Recent weather headwinds in the US (e.g., the Southeast hurricane impact toward end-September) could still impact the numbers, but given the strong August/September momentum, I remain bullish for Q4. Plus, staffing levels will be improved post-TMX – having previously hinted that a lack of staff might have contributed to below-par organic growth, the addition of TMX should allow for more outgrowth over time.

The FY23 guidance will also be worth keeping an eye on. Recall that management’s current guidance calls for $20-25m of annual run-rate synergies by year-end, which equates to an impressive 50% of the initial twelve-month target post-TMX combination. Thus, there’s ample room for synergies to exceed management guidance in the coming quarters. Expect updates on the low-hanging fruits like IT integration in the upcoming results to drive incremental upside (or downside) to earnings estimates. March may be too early for any material guidance changes, though, given the uncertain macro outlook in FY23, so management may well opt to keep most of their cards close to the chest.

A Defensive Pick with Re-Rating Potential

RTO remains a great defensive play ahead of a challenging 2023 outlook on the back of its through-cycle pricing power and overall market leadership. In addition to its GDP plus organic growth profile, the company has also successfully tapped into inorganic growth opportunities. The accretive TMX deal, for instance, accelerates the pro-forma earnings growth profile and allows RTO to further consolidate the pest control industry in North America.

While RTO stock has underperformed peer ROL in recent months following an underwhelming organic growth result in Q3, the extent of the valuation gap seems overblown. With ROL’s fwd P/E of >50x (trailing P/E) well above where RTO trades, there is room for a re-rating going forward. Potential upside catalysts to monitor include progress on the RTO/TMX synergies and further updates on the M&A front.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment