Renewable Energy Group (NASDAQ:REGI) is financially sound. Shareholder returns over the last six years have been excellent, one might even say fabulous. One of my concerns with Renewable Energy relates to analysts’ consensus EPS growth rates, which will likely lead to modest returns at best, over the next few years, as explained in detail below. My major concern is biofuels in general are not a clean energy source, and owe their present support to a lack of truly “green” alternatives. The emerging hydrogen economy does offer a truly “green” alternative, with likely far superior economics, at scale, than biofuels. Governments have already shown considerable reluctance to extend incentives and subsidies. President elect Biden notwithstanding, in the longer term, I can see biofuels losing their incentives and subsidies, their lifeblood, as a far superior alternative, in the form of hydrogen, comes into play. Renewable Energy is not attractive as an investment at current share price. Worse still, in the longer term, its products may go the way of horse whips and buggies. Avoid.

By close on February 22, 2022, the share price had fallen to $32.62, $15.81 (33%) below the price at time of my bearish September 2021 article.

Excerpts from a February 23, 2022, Seeking Alpha news item, “Renewable Energy Group shoots higher on takeover interest – Bloomberg”,

Renewable Energy Group +18.2% pre-market following a Bloomberg report that the biodiesel maker is exploring options including a potential sale after receiving takeover interest. Renewable Energy has held recent takeover talks with large oil and gas companies, and is working with financial advisors, according to the report.

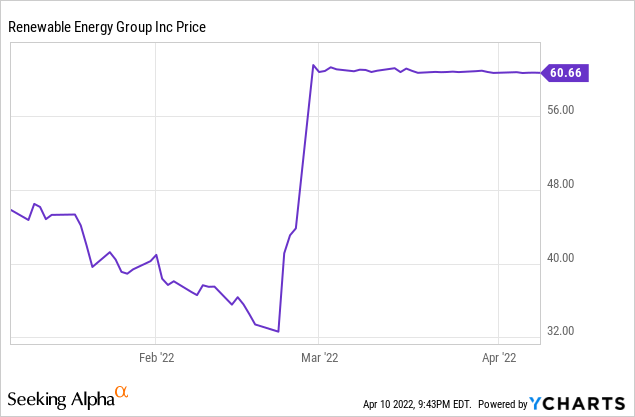

Figure 1 below shows the Renewable Energy Group price action leading up to and following a sale agreement entered into with Chevron Corporation (CVX).

Figure 1

Data by YCharts

Following news of a possible takeover, by Friday February 25, and before any takeover announcement, the market had priced in a fairly normal takeover premium ~34% above Tuesday February 22, with the share price closing at $43.81. This was still below the $48.43 share price at time of publication of my September 2021 article.

On Sunday February 27, over the President’s Day long weekend, the parties settled on a price of $61.50 per share, representing a premium of 40% to the Friday’s closing share price, and ~89% above the previous Tuesday’s closing price.

But for the ‘green’ nature of the business, the negotiated takeover price might well have been around the market’s assessment of $43.81, reflecting a more normal takeover premium.

Investment Thesis Outlook –

This Chevron bid for Renewal Energy Group is an interesting development. There is a lot of pressure on Chevron, and all the oil majors, to reduce emissions. Excerpts from an April 7, 2022 Seeking Alpha news item,

Filings also showed Exxon investors will vote during the annual meeting scheduled for May 25 on seven shareholder proposals that include a call for the company to reduce emissions.

Exxon’s board advises investors to reject all seven shareholder proposals, according to the proxy statement.

Chevron also faces a series of shareholder votes on climate and emissions at its annual meeting, also planned for May 25; the company advises investors to vote against the proposals.

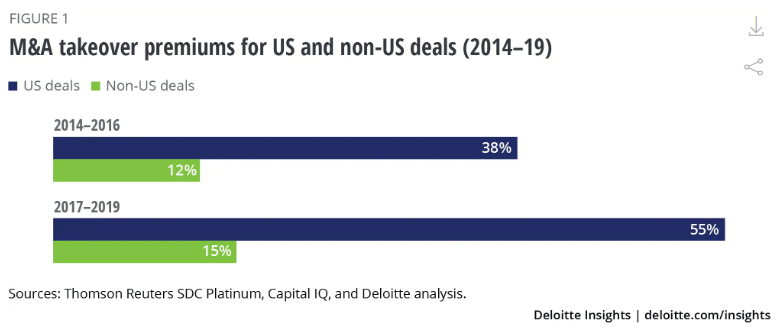

It is not too hard to read into the proposed Renewable Energy Group acquisition, a desire to appease shareholders. This augurs well for many other small, and possibly not so small, renewable energy focused companies. The apparent premium offered by Chevron is not dissimilar to what has been seen with telecommunications and media and entertainment sector acquisitions. Excerpted from this January 2020, Deloitte’s article, “With rising demand for proprietary content, media businesses are rethinking their approach to M&A“,

A wave of takeover activity in recent years has consolidated the telecommunications and media & entertainment sector, shrinking the supply of viable targets and enlarging asset premiums.

Deloitte

THE flurry of new streaming options introduced by major telecommunications and media & entertainment (TME) companies in the last year1 has ignited a run on iconic proprietary content-including acquisitions of entire companies and media businesses-to populate these stand-alone offerings. And with a limited number of established companies available, M&A deal premiums have risen-bringing into question how companies should approach M&A going forward.

Chevron is not alone among the oil majors to face shareholder demands for reductions in emissions. Do the oil and gas majors see acquisition of renewable energy companies as the quickest and least cost way to appease shareholders demanding emission reductions? Was the 89% takeover premium offered for Renewable Energy group a result of vigorous competitive bidding in the “…recent takeover talks with large oil and gas companies…”, referred to in the SA news item linked above? What are investors to make of this?

Obviously, buying before any hint of a takeover offer would be the best approach, and for Renewable Energy group that time has passed. Sometimes there will be further higher offers. The agreement with Chevron precludes the Board from actively seeking higher offers, but per SEC filing dated Feb. 27, 2022, includes a provision,

…In addition, the Board may, in response to a Superior Proposal not resulting from a breach of the Merger Agreement, (i) change its recommendation to the stockholders or (ii) cause the Company to terminate the Merger Agreement to enter into a definitive written agreement with respect to such Superior Proposal, subject to payment of the termination fee…

The possibility of a higher offer remains, and existing shareholders might wish to hold on to shares for that possibility. However, the share price at close on Friday April 8 was $60.66, slightly below the proposed acquisition price of $61.50, suggesting the market is not anticipating a higher offer. What investors might take away from this is the possibility of other renewable energy companies being bid for by the oil and gas majors at significant premiums to their current share price. The offer from Chevron is all cash. Perhaps now might be an opportune time to sell Renewable Energy Group shares with a view to gain cash now and reinvest proceeds into other renewable energy companies. This would maintain exposure to this sector and also open up opportunity to gain from a ‘green’ premium in any potential takeover.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment