Neme Jimenez

Here at the Lab, today, we are back to comment about the French automaker player Renault (OTCPK:RNSDF, OTCPK:RNLSY). Renault was not an easy story to tell. This year, the company was heavily affected by its Russian activity – we reported two follow-up articles about this development called ‘The Most Exposed Automotive Company In Russia‘ and ‘A Sad Day For The French Group‘ when the company announced an agreement to sell AvtoVAZ and its Renault Russia subsidiary for a symbolic amount equal to two rubles (€0.03). Despite that, we were not so pessimistic about the French player. Although we recognized that the Group’s EBIT targets were not ideal within the sector, considering that Russia was the company’s first market (excluding its home market – France), we were positively impressed with how the CEO raised the guidance (after an important turnaround), decided to heavily invest in the EV transition with key partnerships, managed the Nissan relationship and more importantly on how is currently implementing the Renaulution strategic plan.

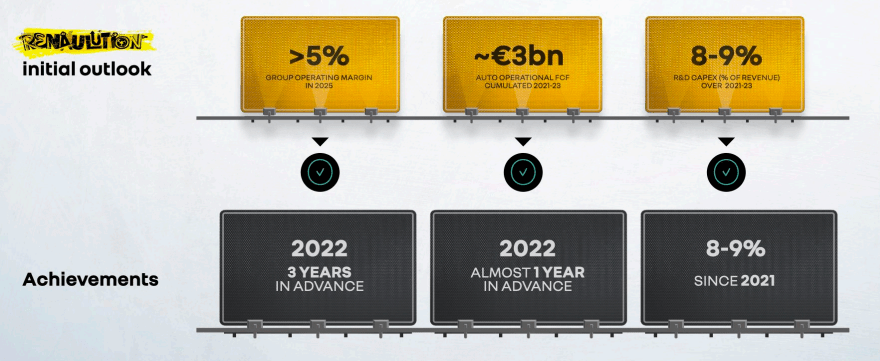

Results achieved (Renault Capital Market Day 2022)

Renaulution Plan in Action

The Renaulution, the strategic plan introduced at the time of the CEO settlement Luca de Meo, is in full swing. In fact, after having restructured the activities of the French giant, bringing them back to satisfactory levels of profitability, the company decided to start a further transformation of their business model to better face the great changes happening in the automotive sector. Renaulution aims to revolutionize Renault’s activities by concentrating them as a priority on electric models, software, new mobility services, and the circular economy, even if hybrid and internal combustion vehicles will still have their role at least in Europe.

Technically, Renault will become a holding company with the creation of five independent and autonomous companies. The two main ones will be Power and Ampère. The first, Power, will focus on the development and production of diesel and petrol engines and will become an equal joint venture with the Chinese group Geely. The second, Ampère, will focus on the electric and digital businesses and will be listed on the stock exchange in the second half of 2023, market conditions permitting. Financially speaking, the new strategy should allow Renault to return to the dividend as early as 2023, subject to regaining the investment grade rating on debt. The operating margin will exceed 8% in 2025 and 10% by 2030, while the average cash flow will be more than €2 billion per year in the period 2023-2025 and more than €3 billion per year in the period 2026-2030. The distribution of the coupon may reach up to 35% of the profits generated by the group.

Looking at the division, Ampère will be based in France and will be able to count on around 10k employees, of which 3,500 are engineers, half of whom specialize in information technology. Furthermore, by 2030, it will be able to count on a range of electric vehicles and capable of guaranteeing 80% of profits in the BEV car market. The Ampère division projections are set at a very high level, the company aims to grow over the next decade at a rate of 30% a year and reach a production of 1 million electric by 2031.

To achieve the ambitious goal, the French house decided to partner and collaborate with Qualcomm (QCOM), which will develop a dedicated platform based on System on Chip solutions, low-layer software, but also in-car services and applications. Another technological partner of Renault will be Google, with which the French will strengthen the current agreement to develop a platform based exclusively on Android. The two partnerships will allow for a reduction in costs and an improvement in efficiency. Moreover, the American chip giant Qualcomm will certainly take part in the listing process; however, the French house will retain a large majority in the capital of Ampère. Thanks to Ampère, Renault will aim to relaunch Alpine, the sports brand also present in force in F1.

Here at the Lab, we already talked about Nissan and Mitsubishi negotiations. At the moment, it is still not clear what role Nissan and Mitsubishi will play in Renault’s reorganization, and whether or not they will participate in the listing of Ampère. The Japanese ally did not like the involvement of the Chinese Geely. During the press conference, Luca de Meo preferred not to comment on the ongoing negotiations, anticipating future communications in this regard; however, we understood that Nissan would also like to re-discuss the shareholding weight in the alliance.

In detail, in Renault’s plans, there is also the creation of a Joint Venture called Horse. The goal is to create a new global car giant fully dedicated to the development and production of engines and transmissions for hybrid cars, both for the brands of the two respective groups and also for other brands. Once created, the new company resulting from the Geely-Renault agreement will include 17 industrial plants, 5 research and development centers spread over three continents, and a workforce of 19k employees, including 2k engineers from 130 different countries.

Conclusion and Valuation

It is important to report the CEO’s words: “this is a new sign of Renault Group’s determination to prepare the company for the future challenges and opportunities generated by the transformation of our industry“. And again, “after executing one of the fastest and most unexpected turnaround plans, preparing the company for growth by ensuring the development of the best product line decades we intend to allocate up to 10% of the capital to our employees who will help to promote a new common culture oriented towards value creation“.

Q3 results were pretty supportive of the company, that once again demonstrated an increasingly competitive product offering coupled with a disciplined approach to revenue that prioritizes value over volume. We increased Renaulution plans with upgraded midterm targets. Our new topline sales projections for 2022/2023/2024 are €45/48/50 billion, from €46/48.5/49.5 billion, respectively. And looking at the total EPS estimates move from €5.08/8.3/9.1 to €5.1/8.5/9.3. The next key catalyst is Renault’s FY 2022 Financial Results planned for February 16. We decide to reiterate our neutral rating case and raise our target price from €31 to €33. We value Renault by applying a 4.0x Price Earnings multiple to the core business, adding in our sum-of-the-part valuation a dividend growth model to value Nissan’s stake.

Be the first to comment