nikkimeel

I need to offer a very sincere thank you to one of my readers, RMUinFL. As 2022 closed, he commented this on my article, “5 Dividend Growth Stocks to Help You Sleep Like a Baby”:

“Happy New year, Brad. I think your transparency has been exemplary this year. Do you still consider Regarded Solutions one of your role models?”

To which I responded:

“Oh yes. That reminded me… I need to work on a remembering Regarding Solutions article… he’s greatly missed!”

Those of you who are new to Seeking Alpha – and many of you who aren’t – might not know who we’re talking about. In which case, here’s the eulogy I wrote in 2021:

“… Alan Saltzman – known here as Regarded Solutions… loved dividend-paying stocks (like me). Somewhere along the way, he ‘was introduced, luckily, to the power of dividend-growth investing and the magic of compounding.’ That’s how, over the years, he would cover names like AT&T (T), Coca-Cola (KO), Procter & Gamble (PG), Exxon Mobil (XOM) and Altria (MO) along with ‘nuggets of wisdom’ in every article.”

Those “nuggets,” along with a focus on family and having fun, were his trademarks. As such, they’re also his legacy above and beyond the insights into and analysis of stocks I and so many others gained so much from.

Alan was quite simply one to beat all around.

He still is today.

Words of Wisdom

Here are just some of the wise words Alan imparted to us from 2011 until he passed away:

- Save as much as you can for as long as you can as soon as you can.

- Spend less than you have coming in, forever.

- Invest in quality dividend-growth companies and reinvest the dividends until you finally need them.

- Eliminate debt, including your mortgage.

- Downsize into what you need to be comfortable.

- Understand your risk tolerance.

- If you use credit cards, pay them off at the end of the month.

- Keep in mind what is truly important in life. Money is just a piece of life’s priorities.

Family really did come first in Alan’s book. Riches and rewards meant nothing otherwise.

Naturally though, he knew that money was necessary to provide for his family. Just like he knew the same held true for so many of his readers.

All that, no doubt, factored into his final Seeking Alpha article on March 4, 2021: “Retirement Strategy: National Fuel Gas – A Smart, Safe, Simple Dividend King to Avoid the Market Turmoil.” In it, he wrote how:

“It’s been a crazy market of late and with so much uncertainty surrounding valuations, wouldn’t it be nice to find a reliable, boring dividend king that has been a great source of income for five decades continuously? On top of that, the energy market has finally come out of hiding and even could offer capital appreciation.

“I realize that the current payout ratio is high, and the free cash flow is weak right now. However, National Fuel Gas Co. (NFG) continues to be one of the most financially sound companies in the sector.”

He acknowledged that the share price back then might look “fully valued.” But he had an alternative view.

Keep in Mind What Is Truly Important in Life

It’s been nearly two years since Regarded Solutions published his opinion that the stock was undervalued. And here’s where NFG was as of January 5:

Yahoo Finance

It’s also continued its Dividend King streak, making it another solid winner in Alan’s collection.

For the record, I’m not recommending NFG today. Frankly, I haven’t looked into it recently and, therefore, have no guidance to give one way or the other.

I only want to say that:

- Regarded Solutions still stands out even after he’s gone

- Value what’s valuable.

Here’s another section of my eulogy to explain that second point:

“Alan was larger than life in so many ways and a true role model to me, as we both started writing on [Seeking Alpha] in 2011.

“For the longest while, he had far more followers. I know this for a fact considering how frequently I looked at his author page. It seemed to me at the time that I would never catch up to the ‘Tiger Woods of Investing.’

“Despite our friendship these past 9+ years, I have to confess that I never told him he was a role model or how much of my prolific writing was inspired by his ‘lead from example’ teaching style.”

I really should have, especially after he shared his cancer diagnosis in 2018.

Life is filled with such regrets; don’t make more of them today. Say what you need to say and do what you need to do.

That can – and possibly should – include stocking up on strong dividend stocks like the ones below. That can definitely be an expression of appreciation for those you care about, as mentioned earlier.

Just don’t let it be the only one.

AT&T Inc.

AT&T is a leading provider of telecommunications, media, and technology services. They provide nationwide wireless services, business and consumer wireline, and equipment and wireless service in Latin America. AT&T is the largest telecommunications company by revenue.

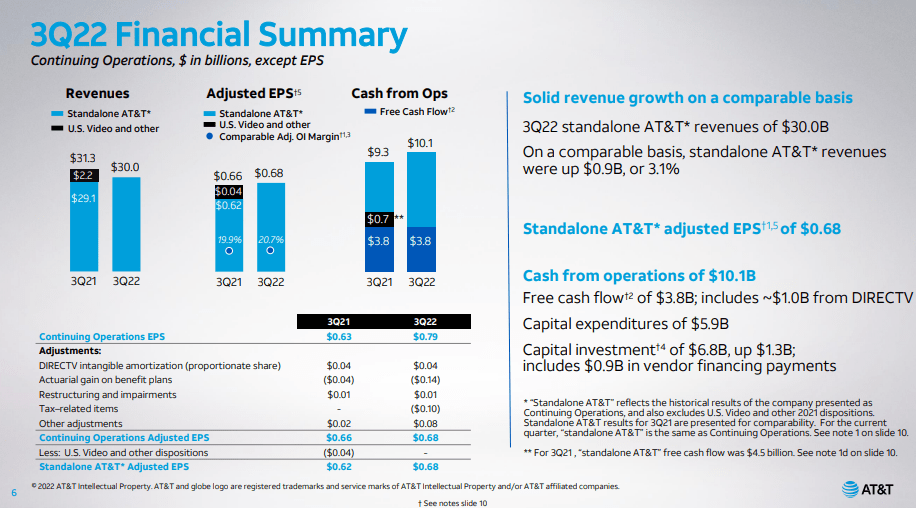

Year 2022 was a strong year for AT&T as reported so far. 3Q 2022 revenue grew by $0.9 B (3.1%) and cash from operations grew from $9.3 B to $10.1 B YoY. The free cash flow (“FCF”) generation was $3.8 B last quarter. Strong subscriber growth in postpaid phone services and AT&T Fiber is also a highlight of the results.

Investor Relations

As more and more appliances, cars, and phones are connected to the internet, the demand for telecommunication services will only increase. AT&T is in the perfect position to take advantage of this trend. They are already one of the biggest wireless and wireline providers in the world, and new opportunities like 5G will continue to come up.

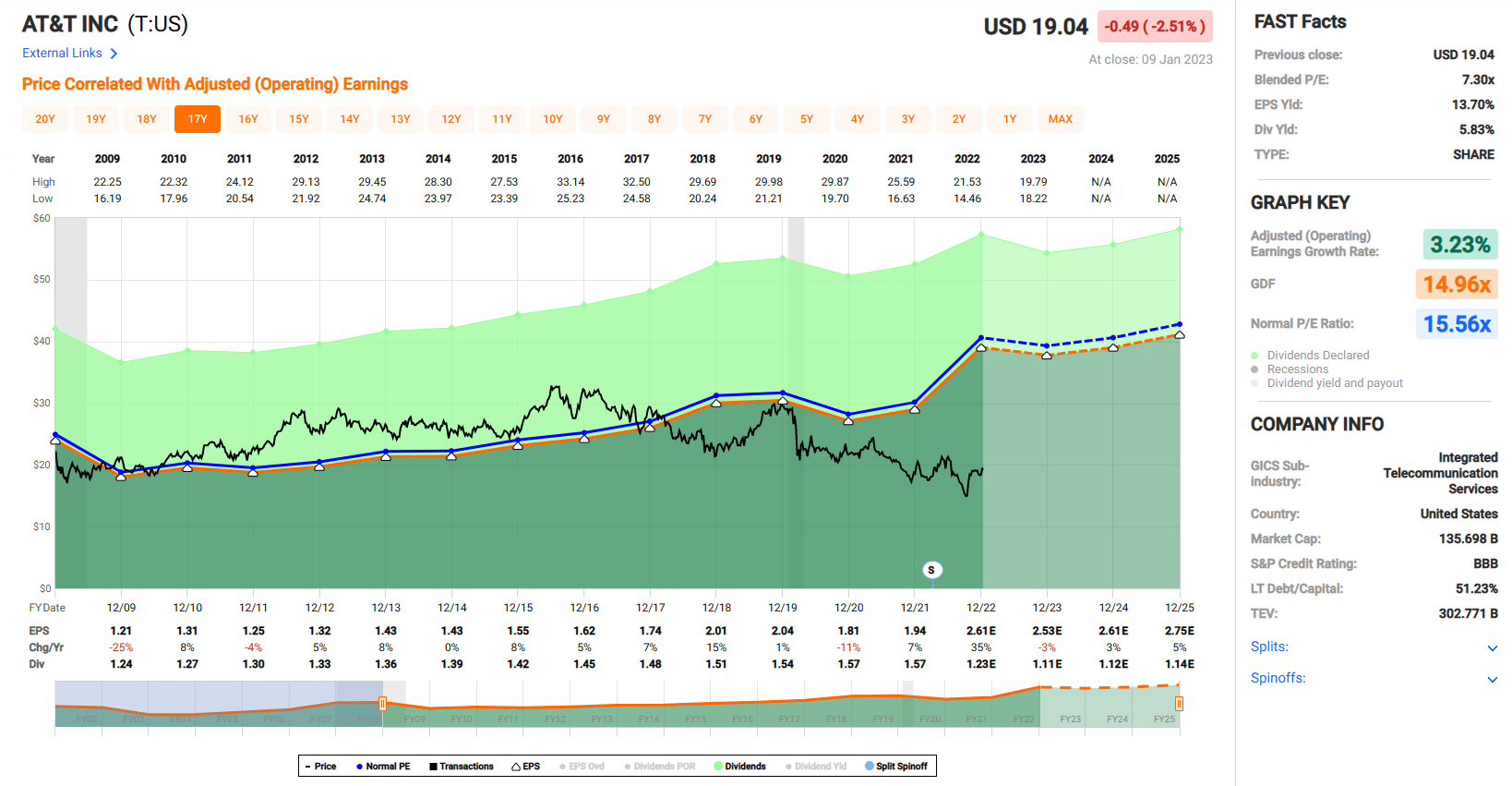

At the current valuation, AT&T is severely undervalued. P/E ratio of 8.12x and EV/EBITDA of 5.94x are substantially lower than their historical values. Also, the current valuation metrics of AT&T are lower than their peers.

Given their leadership position in the business and track record of success, I believe the market will soon realize the mistake in valuation, and the stock price of AT&T will rise in the future.

In the meantime, at their beaten down share price, AT&T offers a nice 5.7% dividend yield and has built up a 38-year streak of consecutive dividend payments.

FAST Graphs

The Coca-Cola Company

The Coca-Cola Company is a total beverage company. They own, license, and market numerous beverage brands around the world. Coca-Cola owns and markets five of the world’s top six nonalcoholic soft drink brands: Coca-Cola, Sprite, Fanta, Diet Coke, and Coca-Cola Zero Sugar.

Investor Relations

Even though Coca-Cola has been in the leadership position for a long time, they are never complacent with what they have but keep on pushing growth. Currently, they have been driving portfolio growth through organic means (e.g., 17% volume growth of Simply vs. 2019), category-expanding acquisitions (e.g., Body Armor, Costa, and Fairlife), and strategic relationships (Topo Chico, Fresca, and Monster).

Other factors that may help Coca-Cola’s bottom line include some decreasing costs for raw materials and distribution. For example, aluminum price went up to near $4,000 per ton last year, but now has come all the way back down to the $2,300 per ton range. The bulk shipping rate fell 21% in November, reaching its lowest level since December 2020.

These factors will help Coca-Cola generate more cash and record higher income.

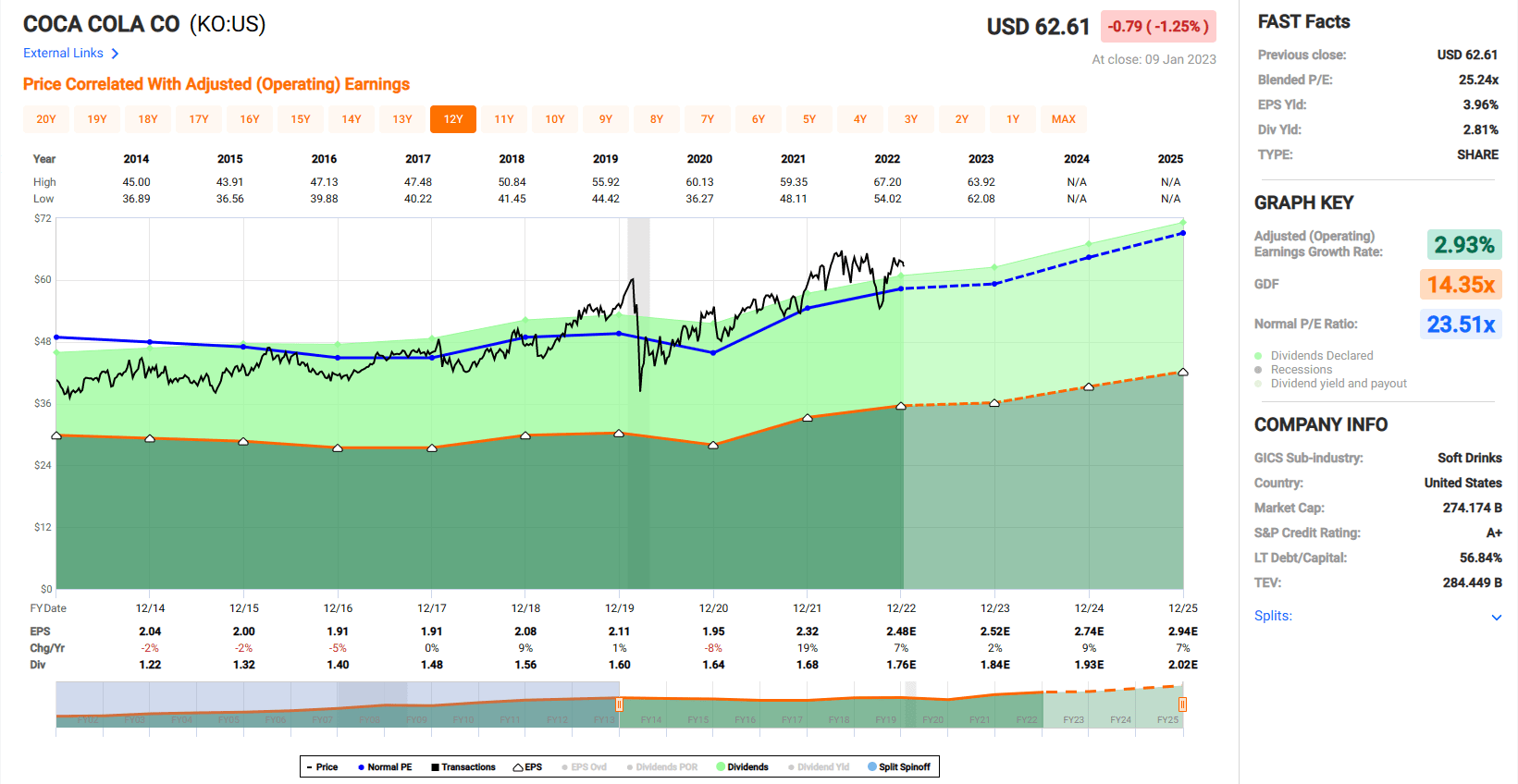

As a proud member of the Dividend Aristocrats, they have been paying and raising their dividend consistently over the past 60 years. Coca-Cola’s 2.8% dividend is very safe at this point. The cash dividend payout ratio is 56.98%, and interest coverage ratio is 16.47x.

Given the strength of their business and cash generating ability, I expect their dividend will be safe for a long period of time. Recession or not, people like to drink Coca-Cola products. As viewed below, KO appears soundly valued:

FAST Graphs

The Procter & Gamble Company

Procter & Gamble is a global leading consumer product company that provides branded products of superior quality and value to customers around the world. P&G has an impressive list of products and brands under their umbrella, and they have leading brands in health care, beauty, grooming, fabric and home care, baby care, and feminine care.

Company Website

Thanks to their strong brand names and operational strength, P&G was able to drive sales growth and generate strong cash flow even in high material cost and souring consumer sentiment environment. Their organic sales grew 7% in the latest quarter, and the growth was broad-based across multiple business lines.

The adjusted free cash flow productivity was 86%, and P&G returned $6.3 B of cash to shareholders ($2.3 B in dividends and $4 B in share repurchases).

As P&G has gone through multiple economic cycles successfully, I believe P&G will do just fine in the current high inflation and recessionary environment. P&G was formed in 1837 by William Procter (British candlemaker) and James Gamble (Irish soap maker). So, they have survived multiple world wars, great depressions, hyperinflation of the 1970s, and many other economic downturns. P&G remained the leading consumer products company through all those challenges.

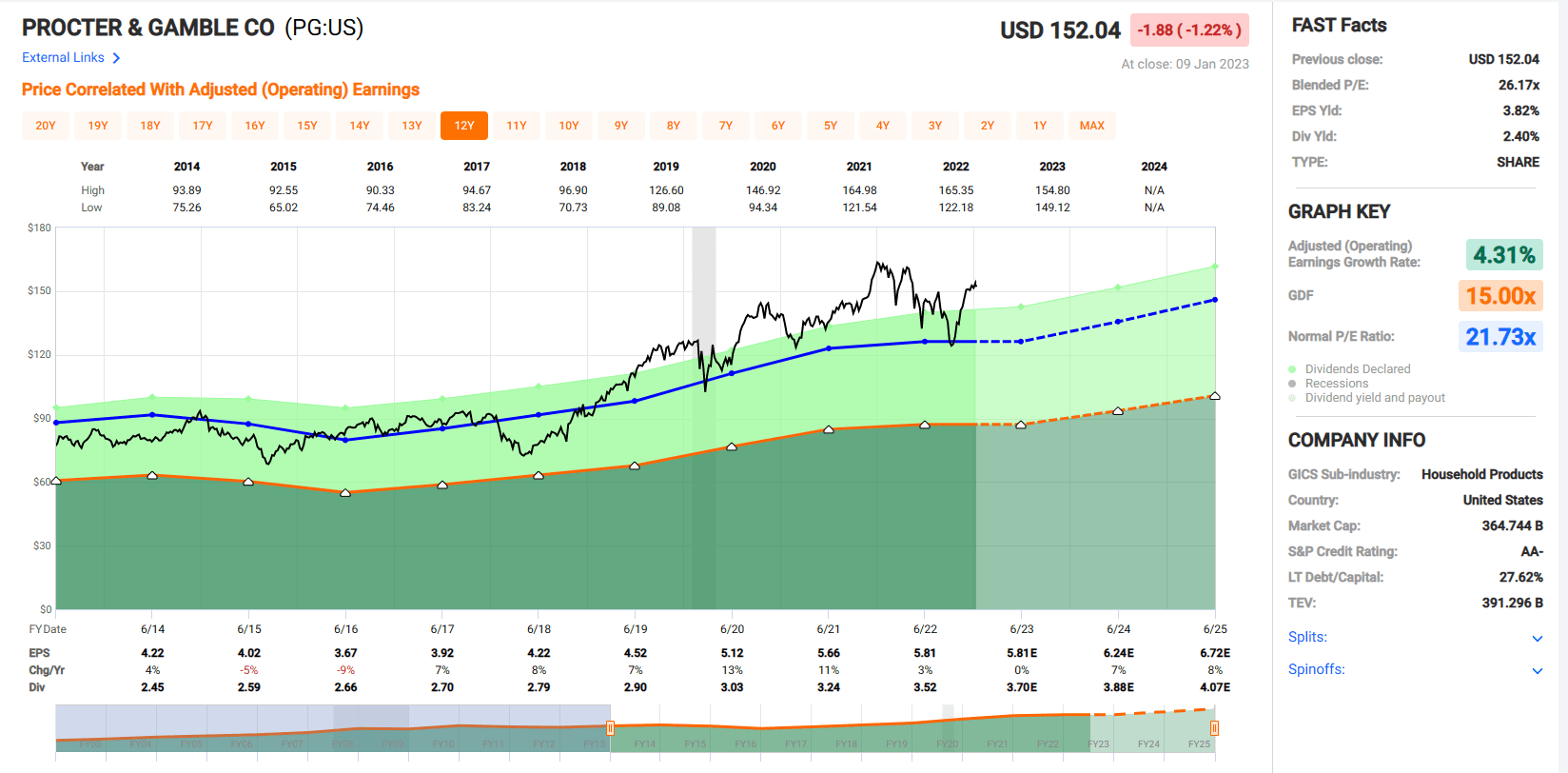

Their dividend payment is safe at this point, demonstrated by the cash dividend payout ratio of 67.02% and interest coverage ratio of 41.07x. P&G offers a reliable 2.4% dividend yield.

P&G has an impressive streak of 66 years of consecutive dividend payments and has grown that dividend every single one of those years, and I fully expect P&G to continue their impressive streak. As viewed below, PG is soundly valued:

FAST Graphs

Risks…

The job report came out strong last week, which is typically very good news for the economy and stock market. However, the current situation is a little tricky.

Since job growth is strong, and the inflation rate is staying high, the Federal Reserve will likely stay hawkish. The interest rate will stay high until the inflation rate goes drops back down close to the 2% range that the Federal Reserve (and we) want. Therefore, a bullish stock market won’t be returning any time soon.

There were several reports about Covid resurgence and related deaths in China. China has been a wild card in terms of Covid response. Their zero-tolerance policy has been causing a lot of confusion and disruptions around the world.

If the Chinese government decides to impose another set of strict Covid measures, it will negatively impact the supply chain, manufacturing capacity, and the general cost environment.

Conclusion

The three companies mentioned in this article share many common characteristics (Regarded Solutions wrote about them often). They are leaders in their industries, have a track record of success, and have strong record of returning value to shareholders.

Investing money in blue chip companies like these with strong fundamentals and a great future outlook will allow you to sleep well at night (“SWAN”).

The recession might be coming, and it may or may not be severe. Some companies may struggle more than others. These uncertainties and volatilities make investing scary in the current environment.

However, investing in companies like AT&T, Coca-Cola, and Procter & Gamble can take some of the stress off. After all, these companies have been through multiple ups and downs in the past, coming out stronger at the end of each cycle. These are some of the safest bets around.

In his very first Seeking Alpha article published on Oct. 10, 2011, Regarded Solutions – wrote:

“There are more ‘issues’ out there than I have ever seen in my 40 years of personal investing. And I am weary of them all. Don’t misunderstand; I am not giving up yet… I am still seeking Nirvana… so what should we do?”

As we enter another year, perhaps all of us should stay positive, and embrace our failures and most importantly, keep “seeking Nirvana”…

Happy SWAN Investing!

Be the first to comment