guvendemir

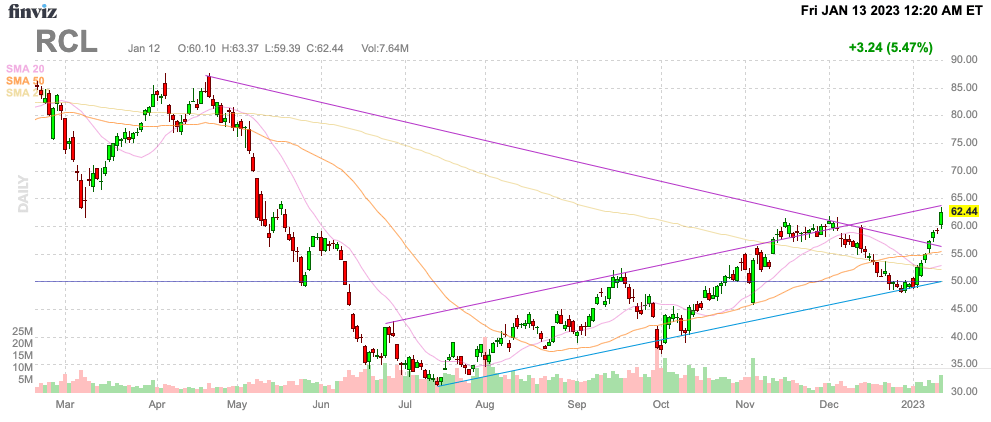

The market keeps doubting the cruise lines, yet Royal Caribbean (NYSE:RCL) is finally pushing recent highs. The travel sector news continues to shine in an indication of the earnings power ahead for the cruise line. My investment thesis remains ultra Bullish on the overlooked stock ready for a big rebound in 2023.

Source: FinViz

Strong Read Off Industry Earnings

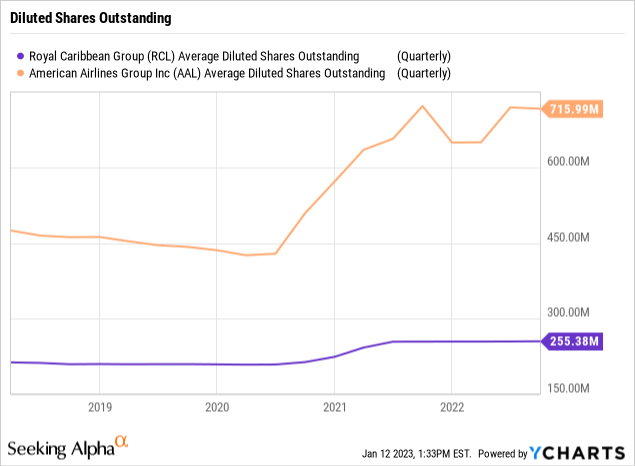

Investors don’t need to look any further than the numbers from American Airlines Group (AAL) to grasp the earnings rebound potential of Royal Caribbean. If any airline was impacted as much as the shutdown cruise lines, it was American Airlines piling on more debt and diluting shareholders via massive share dilution.

The airline just reported Q4’22 numbers would nearly double analyst targets. Not only did American Airlines smash targets the market didn’t even want to believe with the stock recently trading at $12, but also the company is set to match the $1.15 EPS produced back in Q4’19.

The airline with nearly 300 million additional shares outstanding and interest expenses topping 2019 levels by ~$170 million per quarter is set to smash the income levels of the prior years. The much higher income levels will help American Airlines further deleverge leading to additional reductions in debt and related interest expenses.

If one of the weakest airlines can jump all of the hurdles in late 2022 to produce massive income, than Royal Caribbean should be able to do the same. Back in 2019, the cruise line was producing massive income and the is oddly set up some 6 to 12 months behind the airlines with American Airlines reporting massive losses in Q4/Q1.

Remember, travel demand is so strong travelers are more than willing to pay up to offset higher costs. American Airlines saw Q4 costs up 10% while cruise line peer Carnival Corporation (CCL) reported similar metrics with their recent earnings showing FQ4’22 costs excluding fuel per ALBD up 7.2% (11% in constant currency).

Most importantly, the largest cruise line continues to see a huge boost in bookings and hence deposits that help cash flows:

- The company’s full year 2023 cumulative advanced booked position is higher than its historical average at higher prices in constant currency, normalized for FCCs, as compared to a strong 2019.

- Total customer deposits hit a fourth quarter record of $5.1 billion as of November 30, 2022, surpassing the previous record of $4.9 billion as of November 30, 2019.

Similar to how the airlines started recovering in early 2022, Carnival reported North America and even Australia booking volumes in November exceeding the comparable period in 2019. The company faces tough markets in Europe due to the war in Ukraine and China with the lack of a reopening when the cruise line reported back in December.

Recapturing 2019 Levels

Royal Caribbean had fallen back below $50 in the last few months despite the cruise line previously predicting a recapturing of the 2019 levels. The Trifecta Program launched with the Q3’22 earnings report forecasts the cruise line achieving the following metrics by the end of 2025:

- Triple Digit Adjusted EBITDA per APCD, to exceed prior record Adjusted EBITDA per APCD of $87 in 2019.

- Double Digit Adjusted Earnings per Share to exceed the prior record Adjusted Earnings per Share of $9.54 in 2019.

- Return on Invested Capital (“ROIC”) in the teens to exceed the prior record ROIC of 10.5% in 2019 through optimizing capital allocation and enhancing operating income.

The market clearly didn’t believe this plan, but the American Airlines numbers are far more supportive of such a scenario. Heck, the airline numbers should make investors think the timeline for Royal Caribbean can be pulled forward a year or so.

Analysts only have Royal Caribbean earning $8.87 in 2025 in a sign of ongoing market fears that appear irrational. Either way though, the stock was trading below $60 heading into the increased guidance from American Airlines when the debate was actually whether the cruise line would generate a 2025 EPS of $8 per analysts or $10 per the estimate from management.

Source: Seeking Alpha

The only question now appears the curve of the rebound to prior levels and the eventual profit levels in the future. The cruise line has a massive debt level entering 2023 with quarterly interest expenses in the $340 million range (down from $427 million last Q3). Royal Caribbean will need to deleverage over time and record bookings will help provide the cash flows to return the quarterly interest expense back to the $100 million range.

Takeaway

The key investor takeaway is that the metrics reported by travel industry peers should reduce the doubt of Royal Caribbean reaching the goals of the Trifecta Program. The ultimate goal of the program is for the cruise line to generate a $10+ EPS by 2025 due to boosted profits per APCD and higher returns on capital despite knowing the impacts of higher costs due to inflation.

The stock is cheap near $60 with few reasons to think Royal Caribbean shouldn’t approach the previous highs above $130 when the EPS is targeted to top prior records.

If you’d like to learn more about how to best position yourself in undervalued stocks mispriced by the market heading into a 2023 Fed pause, consider joining Out Fox The Street.

The service offers model portfolios, daily updates, trade alerts, and real-time chat. Sign up now for a risk-free, 2-week trial to start finding the next stock with the potential to generate excessive returns in the next few years without taking on the outsized risk of high-flying stocks.

Be the first to comment