Real Estate Special Report

In this Real Estate Special Report, we analyze the potential impacts from the ongoing coronavirus outbreak in the United States to determine which REIT sectors are better-prepared to withstand a potential near-term economic shock. While many pundits and commentators suggest that the current uncertain environment requires us to completely disregard the pre-coronavirus fundamentals, we believe that it is especially critical to understand where REITs were before the start of the outbreak to understand where REITs will be when the dust settles.

{kind=link}

(Hoya Capital, Co-Produced with Brad Thomas through iREIT on Alpha)

Lessons Learned The Hard Way

“This time is different?” Amid a historically violent market plunge resulting from the ongoing coronavirus outbreak, investors have been understandably drawing linkages to the financial crisis a decade ago. Real estate – both residential and commercial – are remembered as some of the hardest-hit victims of the downturn that saw the S&P 500 (SPY) lose more than half of its value before launching into the longest bull market in history. By comparison, the broad-based Commercial Real Estate ETF (VNQ) plunged roughly 75% from its peak in February 2007 to its trough in March 2009 as seizing credit conditions caught over-extended REITs flatfooted, forcing many real estate companies to issue equity at firesale valuations simply to stay afloat.

Owing to the harsh lessons learned during the financial crisis, most REITs have been exceedingly conservative with their balance sheet and strategic decisions in the post-recession period. With the scars still visible enough to be daily reminders of more dismal times, REITs have been “preparing for winter” for the last decade, perhaps to the frustration of yield-hungry investors that have turned to higher-leveraged and riskier alternatives in recent years. REITs entered 2020 with historically strong balance sheets across essentially every metric. Debt as a percent of the market value of assets accounts for less than 32% of the REITs’ capital stack, down from an average of roughly 45% in the pre-recession period. EBITDA coverage ratios ticked higher to over 5x entering 2020 compared to the sub-3x average in the pre-crisis period.

Conservatism has positioned these REITs exceedingly well relative to their riskier alternatives in the private or non-traded markets in the event of a sustained slowdown in fundamentals or near-term coronavirus dislocation. In sharp contrast to the trends observed in the run-up to the prior crisis, REITs have used lower interest rates to extend their debt maturities considerably and dramatically improve the durability of their capital stack. Interest expense as a percent of NOI ticked down to new record lows this year at 21.0%. As more REITs have obtained investment-grade bond ratings, they have been able to issue longer-term unsecured debt, pushing the average term to maturity to 84 months last quarter, smashing the record highs set during the quarter.

As we’ll analyze in far more detail below, with the exception of the troubled mall sector, property-level fundamental metrics entered 2020 as healthy as they’ve ever been. Occupancy rates ticked up to record-highs in the fourth quarter, up slightly from 3Q19 to end the year at 94.1%. Same-store occupancy metrics have been helped by the continued portfolio recycling strategies employed by many REITs, which have sold off underperforming properties and purchased higher-occupancy assets. All four major property sectors saw a year-over-year rise in occupancy, led by an 80 basis point gain from office REITs. By comparison, occupancy levels peaked out at roughly 92% before the recession and dipped as low as 88% by 2010.

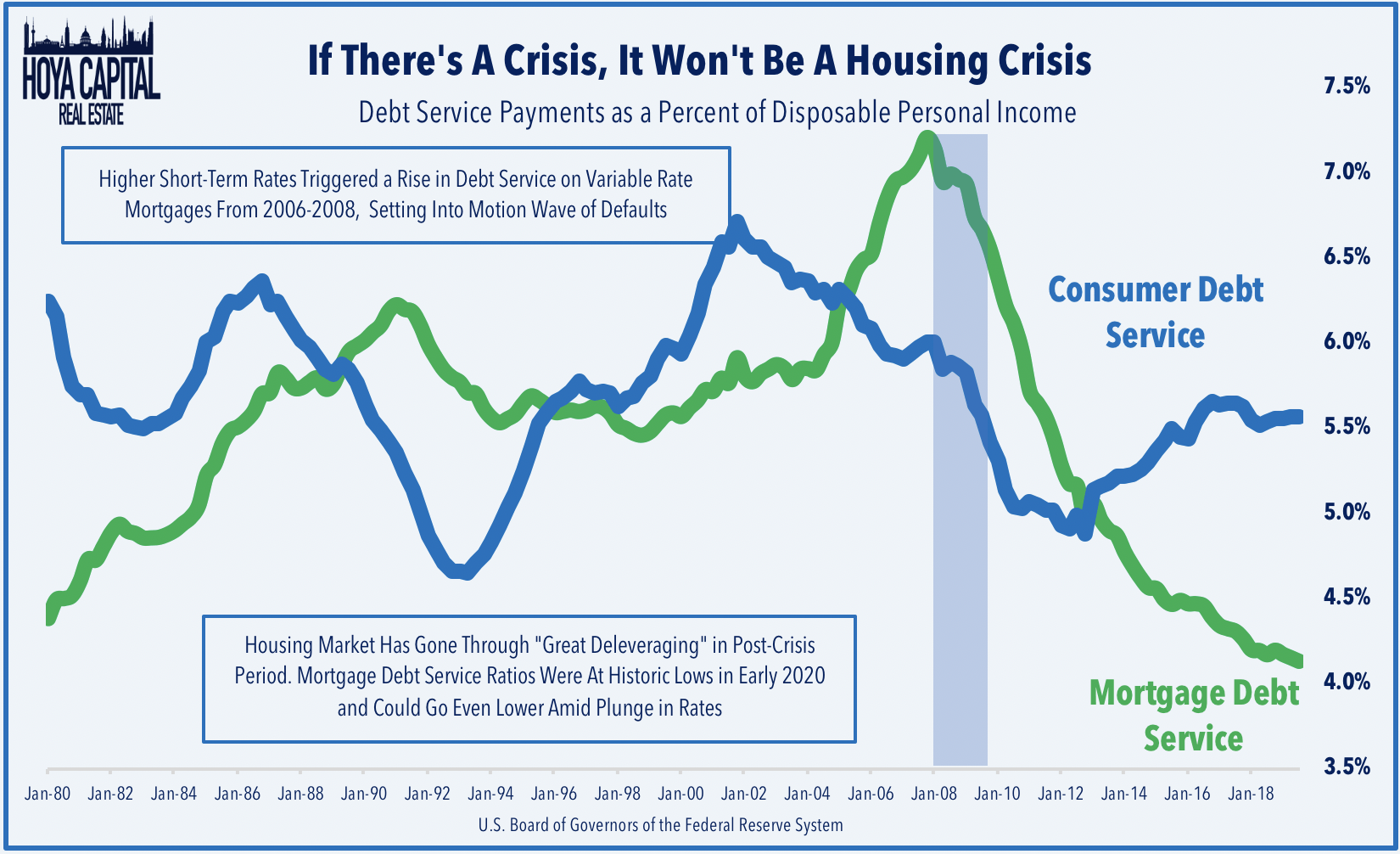

While no sectors would be entirely immune from the effects of a potential recession, we continue to believe that the U.S. residential real estate sector will prove to be a source of resilience amid this period of dramatic volatility. Owing to years of tight mortgage lending conditions and a generally slow post-recession recovery in homeownership, the housing market has undergone a period of significant deleveraging over the last decade. At the end of 2020, the mortgage debt service payment ratio as a percent of disposable income reached the lowest level on record at 4.12%. By comparison, this level was at 7.13% at the time that job growth turned negative in Q1 2008.

Not All REITs Are Created Equal

Domestic-focused and yield-sensitive equity sectors have been relative “safe-havens” so far in 2020 amid the market turmoil. The residential and commercial real estate sector should be expected to be among the biggest beneficiaries of lower interest rates if the U.S. economy can manage to hang on long enough to avoid an outright recession amid the coronavirus outbreak. Thankfully for REIT investors, the “rising interest rate environment” and “rates up, REITs down” paradigm that dogged the sector from 2016 to 2018 appears to have given way – at least temporarily – to a new economic reality of “lower for longer.” The near-lockstep correlation between REITs and the 10-Year Treasury Yield (IEF), however, has broken down over the last several weeks as investors price-in increased odds of a more substantial and lingering recession.

The broad-based averages, however, mask the sharp divergences between individual REIT sectors. While balance sheet metrics as a whole are as strong as they’ve ever been, more than two dozen of the roughly 175 publicly-traded equity REITs tracked by NAREIT reported debt ratios in excess of 60% in the most recent month, the vast majority of which are small-cap REITs under $2 billion in market capitalization. Pockets of stress will undoubtedly emerge if the Covid-19 outbreak intensifies and lingers for longer than expected, particularly for highly-levered retail and lodging REITs that could be in a fight for survival in the early stages of 2020. (Scroll down for a link to our sector reports.)

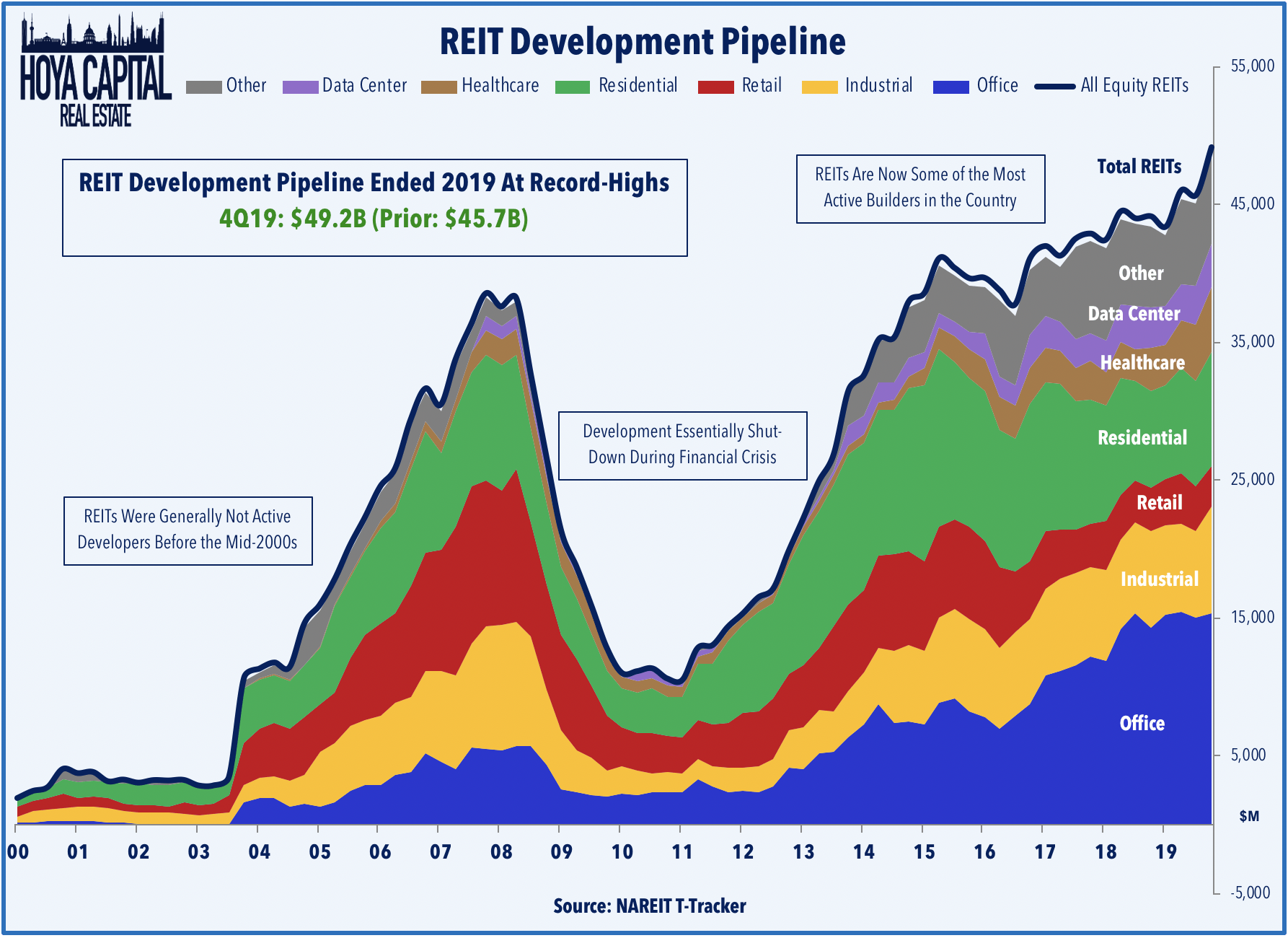

While balance sheet metrics are as strong as they’ve ever been, the historically large REIT development pipeline does represent a source of “shadow leverage” that could become a risk in the event of a sustained downturn. Before 2005, only a handful of REITs had in-house development teams, but that has changed significantly over the last decade, and many large REITs are now among the most active real estate developers in the country. Fueled by firm private market values, development yields remain attractive in many sectors, driving the development pipeline to new record highs of $49.2 billion at the end of 2019. We view office REITs as the sector with the most “shadow leverage” given the pro-cyclical nature of office demand and the nearly $15 billion office development pipeline.

Access To Capital Shouldn’t Be An Issue for REITs

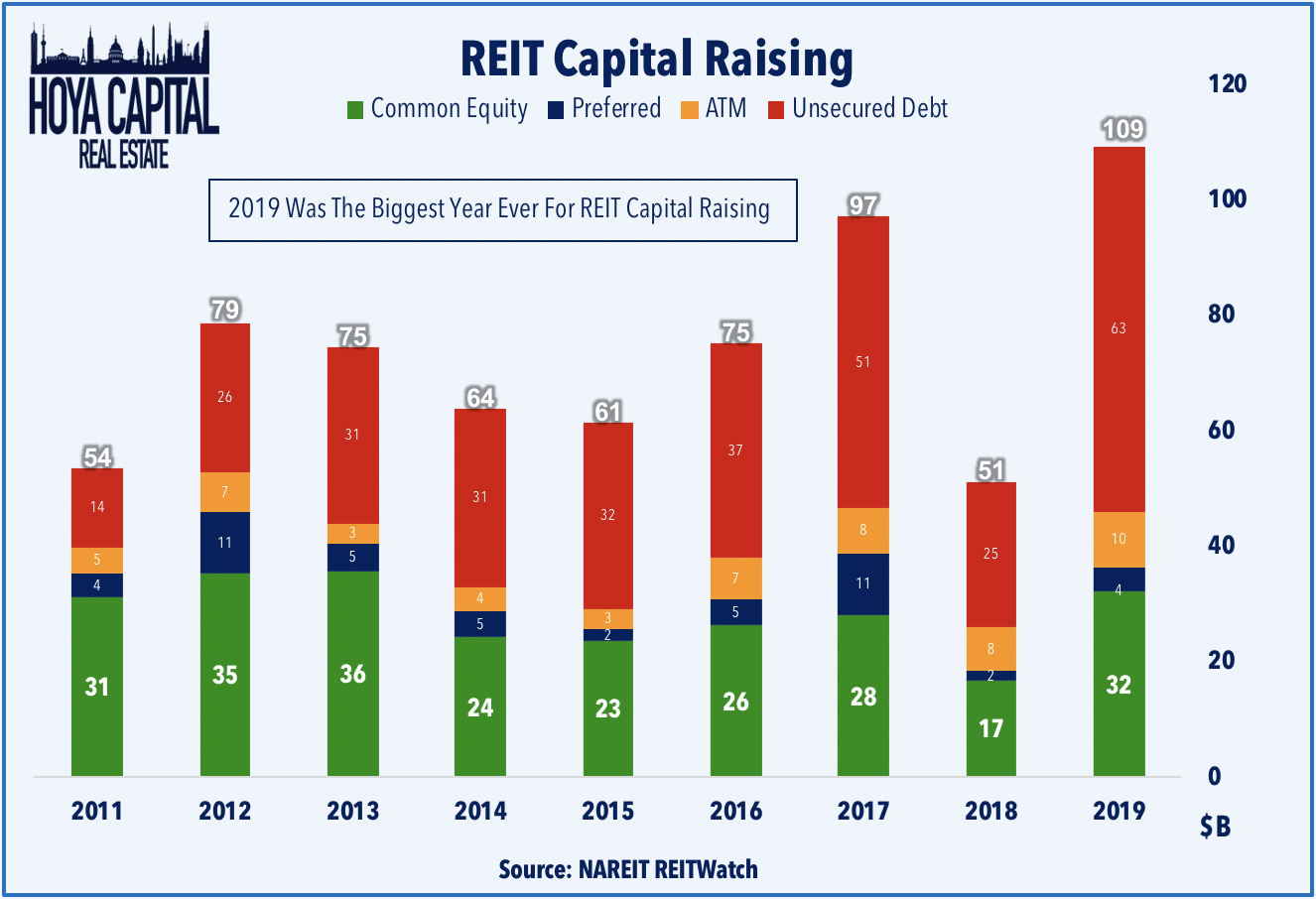

Access to capital – or lack thereof – was the accelerant that turned a bad situation into a dire one for REITs during the financial crisis. REITs enter this period of volatility with a “war chest” relative to their position in 2008 as REITs raised more capital in 2019 than in any prior year since the recession. REITs raised $109 billion last year with $61 billion of that raised through long-term unsecured debt and $32 billion raised through secondary offerings of common equity. At roughly 40% of the total, common equity issuance as a share of total capital raised is towards the lower end of the historical averages, as REITs took advantage of declining interest rates with long-term debt offerings, pushing their average maturity out to record-long terms as discussed above.

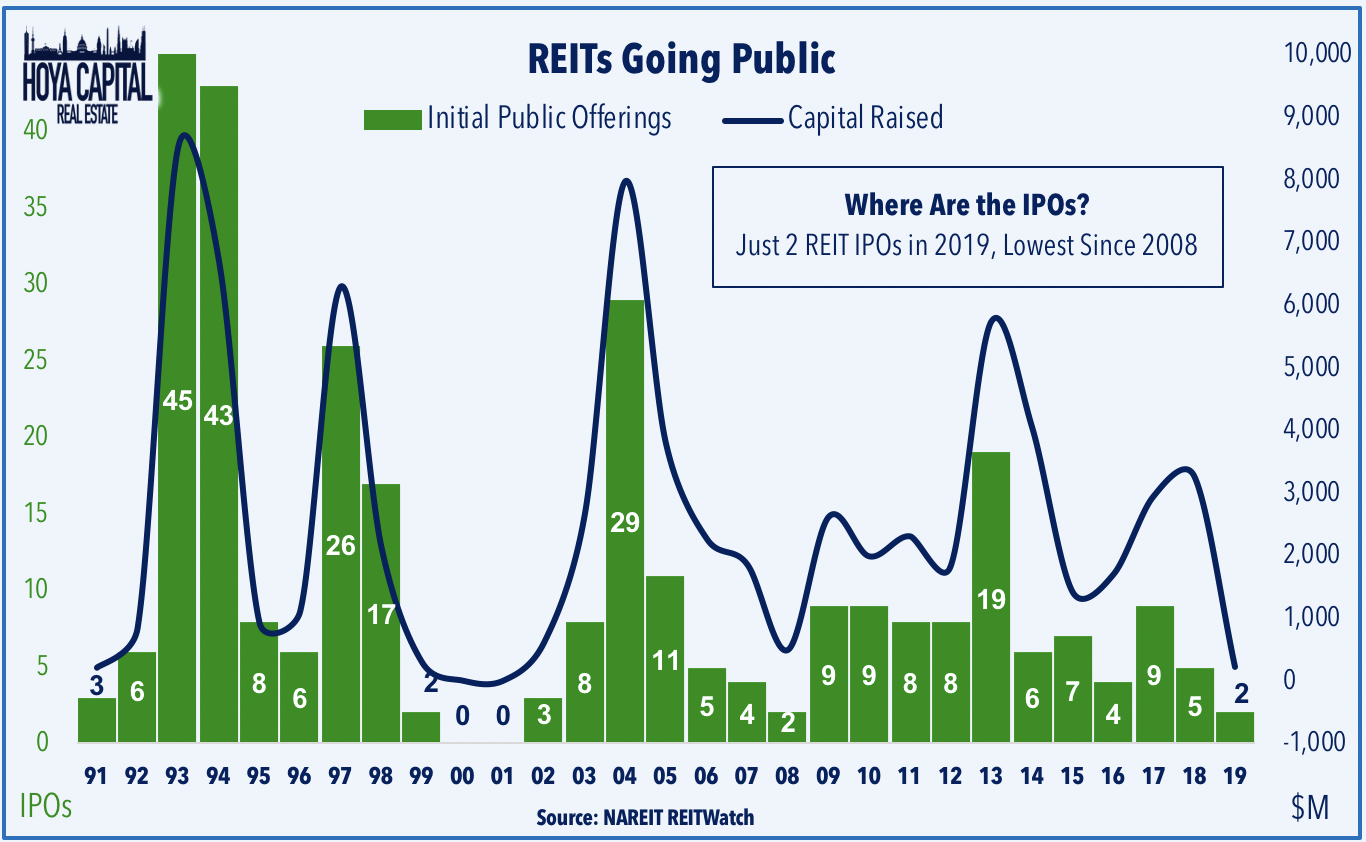

One area where we didn’t see the effects of 2019’s “REIT Rejuvenation” is the IPO market, and perhaps for the better considering the brutal market environment in early 2020. Just two REITs, Postal Realty Trust (PSTL) and Alpine Income Properties (PINE) went public last year, raising a combined $250 million in equity. This quiet year for REIT IPOs comes after five REITs went public last year, the largest two being casino REIT VICI Properties (VICI) and cold storage operator Americold Realty Trust (COLD). IPOs in the major property sectors have been few and far between over the past half-decade. The three largest IPOs since 2013 have been office REIT Paramount Group (PGRE), followed by single-family rental operator Invitation Homes (INVH) and net lease operator STORE Capital (STOR). Before the Covid-19 outbreak, we expected an uptick in IPOs in 2020.

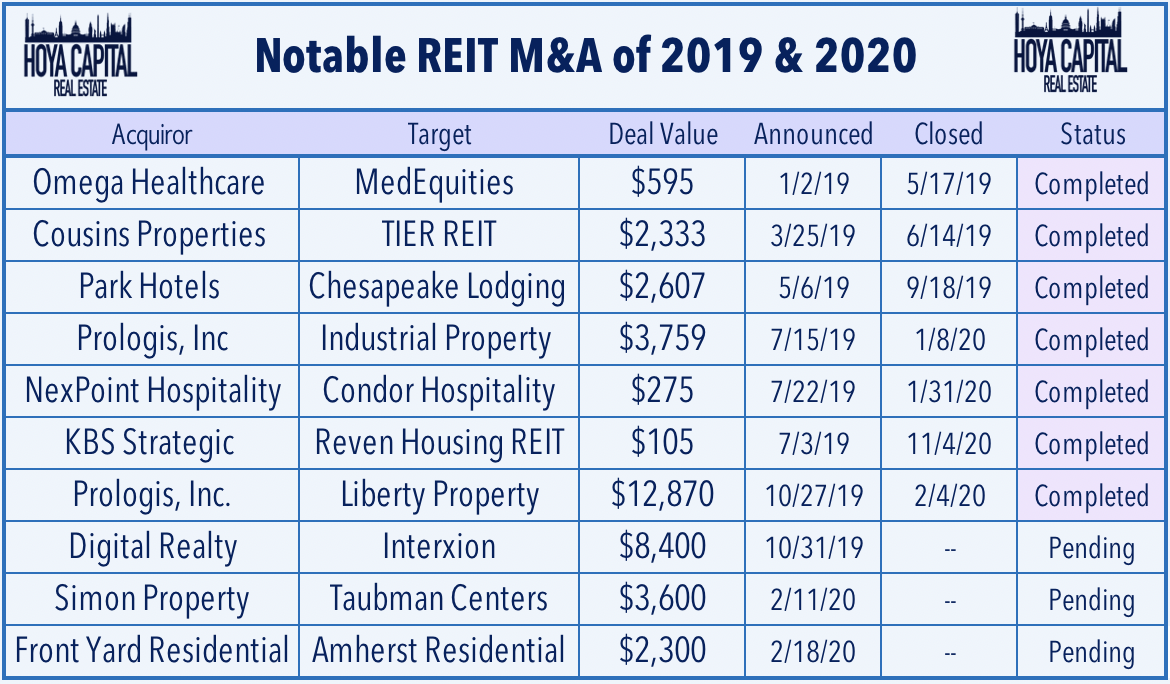

Merger Mania? It appears that we were headed that way before the Covid-19 outbreak. After a dearth of activity in 2018 and early 2019, the wheels had started to spin again in the REIT M&A machine. Seven deals in excess of $2 billion have been announced since late March, including two deals involving industrial giant Prologis (PLD), which closed on its acquisition of Liberty Property Trust (LPT) in February several months after closing on its acquisition of non-traded REIT Industrial Property Trust (IPT) in July. Last October, data center REIT Digital Realty Trust (DLR) announced plans to acquire European data center giant InterXion Holding (INXN) for $8.4 billion. This year, Simon Property (SPG) announced plans to acquire fellow mall REIT Taubman Centers (TCO) while Front Yard Residential (RESI) was purchased for $2.3 billion from private equity firm Amherst Residential.

REIT Fundamentals Were Solid Heading Into 2020

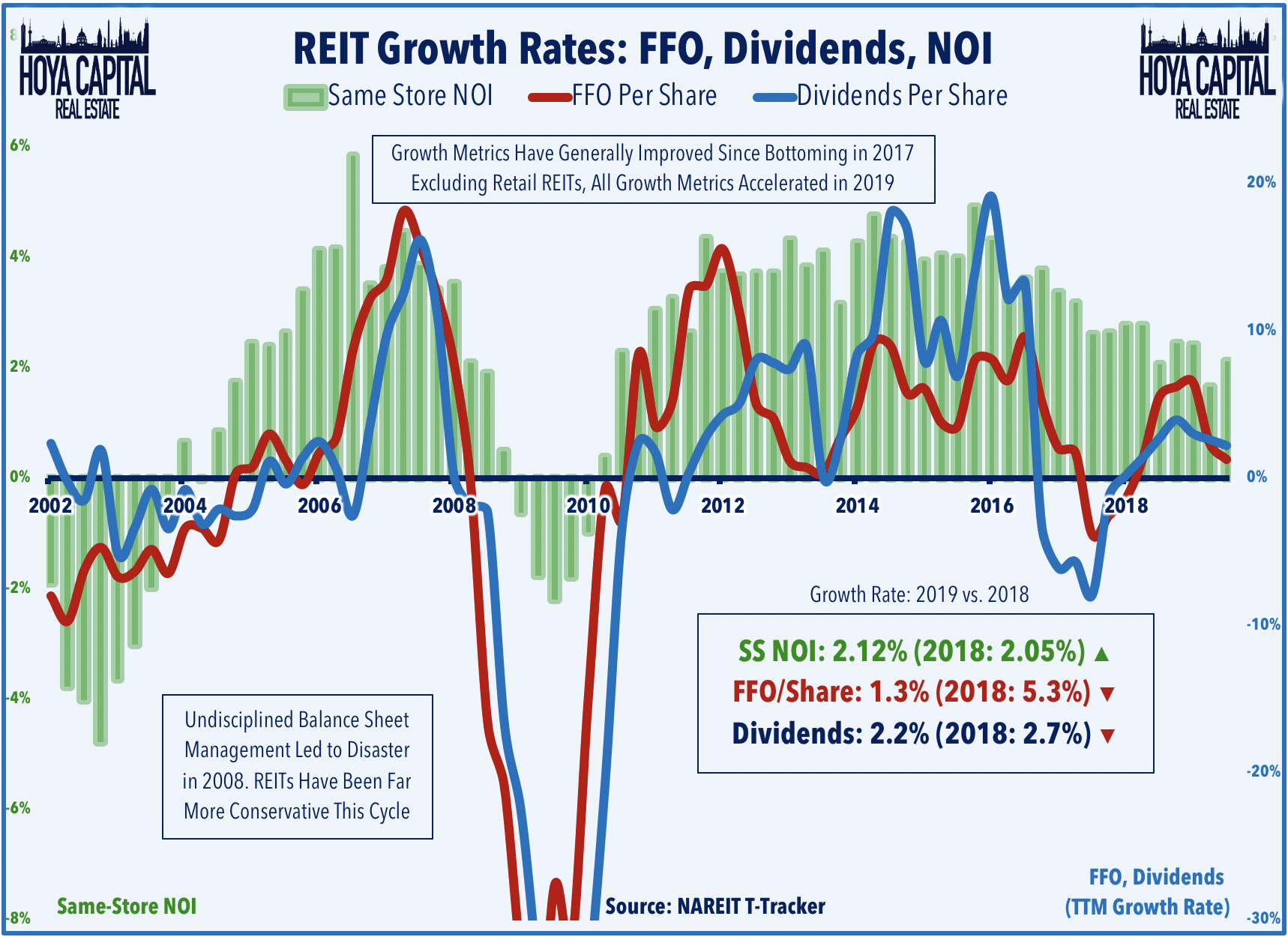

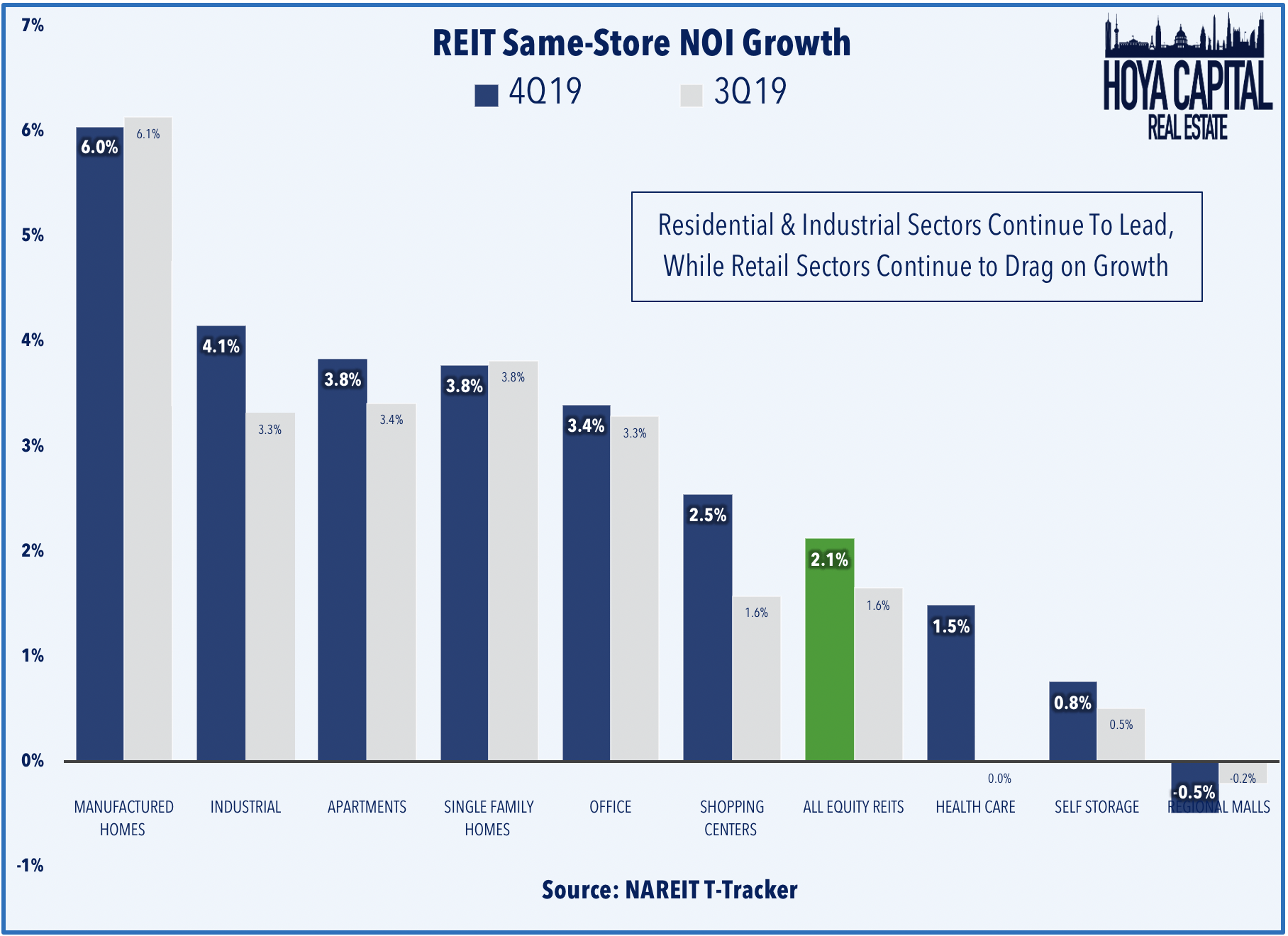

Apart from the retail sector, REITs entered 2020 on a path of accelerating growth led by the residential, industrial, and technology REIT sectors, which have been a source of shelter amid the continuing turmoil. After sliding from 2016 through 2018, REIT growth metrics have generally improved since bottoming in 2017 as same-store NOI growth ticked up to 2.12% in the fourth quarter from 2.05%. For the overall REIT averages according to NAREIT, after growing at the fastest rate since 2016 in 2Q19, FFO and dividends per share ended 2019 with 1.3% and 2.2% growth, respectively. Excluding retail REITs and including the technology REITs that are excluded from the official NAREIT calculations, however, FFO and dividends per share each grew roughly 4.0%.

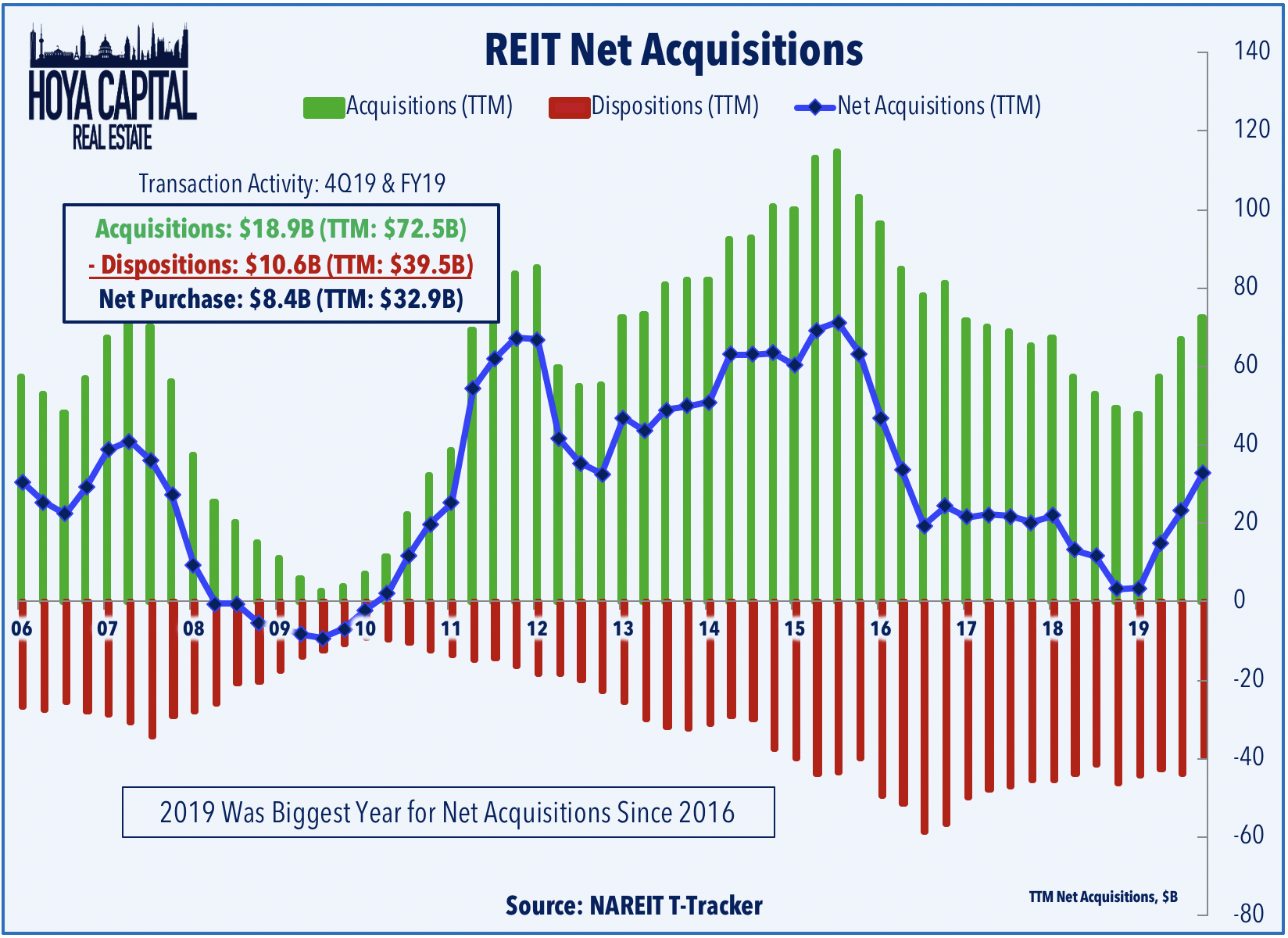

REITs were just beginning to get back to doing what they do best: utilizing their access to equity capital markets – one of their primary competitive advantages over private market peers – to accretively grow via external acquisitions. Importantly, the vast majority of REIT asset management teams have remained highly disciplined in their capital allocation. “Capital recycling” has been a primary theme of the past decade in which REITs have been proactive in selling lower-quality properties and redeploying the capital into higher-quality assets with more stable cash flows. REITs acquired $72.5 billion in assets in 2019 while disposing of $39.5. The $32.9 billion in net acquisitions was the largest annual net “buy” since 2016.

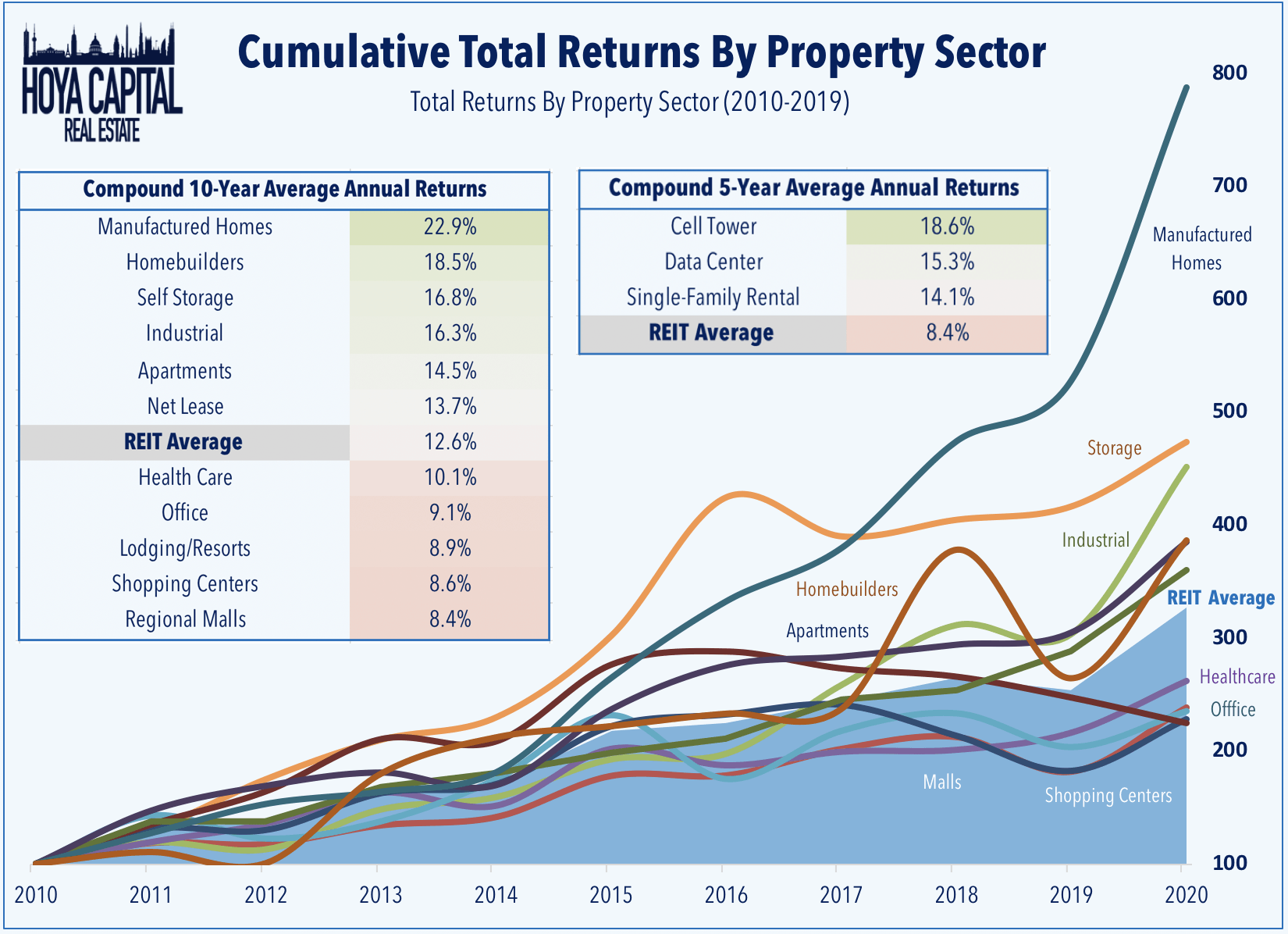

The trends that dominated 2019 continued in the fourth quarter with the residential, industrial, and technology REIT sectors continuing to record strong growth while the retail sector continues to struggle. Residential REITs, in particular, have led the way over the last three years as an intensifying housing shortage has reignited rent growth, a result of strong household formations and wage growth over the past two years. Same-store NOI growth remains strongest in the affordable housing segments which are experiencing the most significant demand imbalance: manufactured housing and single-family rentals, where same-store NOI jumped 6.0% and 3.8%, respectively, over the past year. Retail REITs remain a drag on the real estate sector, though shopping centers have been comparable stronger than the enclosed regional mall REIT sector.

Bottom Line: This Time Is Different, Really

It may be hard to believe now, but things will get better, but in the meantime, we believe that the residential and commercial real estate sectors are more than prepared to weather the storm. Owing to the harsh lessons learned during the financial crisis, most REITs have been exceedingly conservative with their balance sheet and strategic decisions in the post-recession period. Conservatism has positioned these REITs exceedingly well relative to more highly leveraged private equity competitors in the event of a sustained slowdown in fundamentals related to the coronavirus outbreak.

Small pockets of stress will undoubtedly emerge if the Covid-19 outbreak intensifies and lingers for longer than expected, especially in the highly-levered REITs and private firms that have lacked similar discipline during this cycle. Importantly, REITs entered 2020 on a path of accelerating growth led by the residential, industrial, and technology REIT sectors. Given the counter-cyclical properties of the residential sector, in particular, combined with the lingering affordable housing shortage, we expect the residential sector to be a source of continuing shelter amid the continuing turmoil.

If you enjoyed this report, be sure to “Follow” our page to stay up to date on the latest developments in the housing and commercial real estate sectors. For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Healthcare, Industrial, Data Center, Malls, Net Lease, Shopping Centers, Hotels, Billboards, Office, Storage, Timber, and Real Estate Crowdfunding.

Announcement: Hoya Capital Teams Up With iREIT

Hoya Capital is excited to announce that we’ve teamed up with iREIT to cultivate the premier institutional-quality real estate research service on Seeking Alpha! Sign-up for the 2-week free trial today!

Disclosure: I am/we are long STOR, INVH, PLD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. All commentary published by Hoya Capital Real Estate is available free of charge and is for informational purposes only and is not intended as investment advice. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.

Hoya Capital Real Estate advises an ETF. In addition to the long positions listed above, Hoya Capital is long all components in the Hoya Capital Housing 100 Index. Real Estate and Housing Index definitions and holdings are available at HoyaCapital.com.

Be the first to comment