Puttachat Kumkrong

Redwood Trust (NYSE:RWT) is a REIT that specializes in managing the credit risk of residential mortgage debt, by both investing in it and originating it for sale. I’ll go into detail on its businesses below.

Redwood’s current valuation is relatively and historically very cheap. On a relative basis, it currently pays a $0.92 annual dividend, for an 12.5% yield. That beats the heck out of the 10-year Treasury’s 3% yield, the 7% BB corporate bond yield (ICE Data Indices) and nearly matches the 15% yield on high risk CCC and lower corporate bond yields (ICE Data Indices). And Redwood’s price to its most recent book value of $10.78 is only 68%. That’s well below the 94% price-to-book of home mortgage REIT AGNC.

Redwood’s current 12.5% dividend yield is very near its post Financial Crisis high:

Yahoo Finance

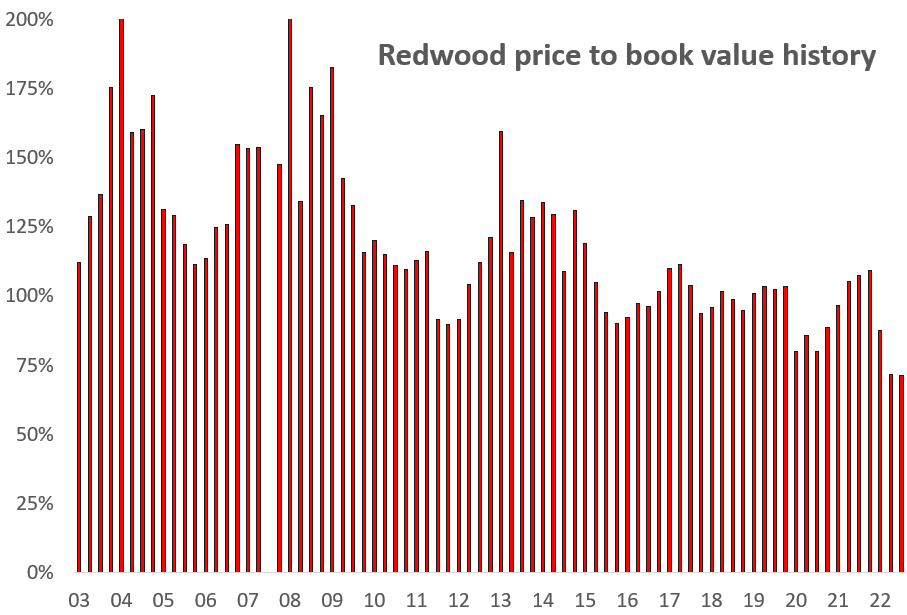

And its price-to-book is at its historic low:

Yahoo Finance and Redwood Review

But to even consider taking the time to learn Redwood’s business, you have to believe a surge in residential mortgage defaults is not on the horizon. So let’s get right to my contrarian housing argument.

Yes, housing has entered a recession…

I’m sure you’re quite aware of the current nasty housing trends. I few quick quotes to remind you:

“Sales of previously owned homes fell nearly 6% in July compared with June, according to a monthly report from the National Association of Realtors. Sales dropped about 20% from the same month a year ago.” (CNBC, August 18, 2022)

“Sales of new U.S. single-family homes plunged to a 6-1/2-year low in July as persistently high mortgage rates and house prices further eroded affordability.” (Reuters, August 23, 2022)

“Home prices declined 0.77% from June to July, the first monthly decline in nearly three years, according to Black Knight, a mortgage software, data and analytics firm.” (CNBC, August 24, 2022)

…but a surge in home mortgage defaults is very unlikely

Redwood doesn’t build homes. It doesn’t sell homes. It does take the risk that home mortgage debt defaults. At present, almost nobody is defaulting. For example, Fannie Mae’s annualized charge-off rate so far this year on its $4 trillion of home mortgages it guarantees is a mere 1 bp. In my view, the risk of a material rise in default rates over the next few years is small. I present four charts to support this view:

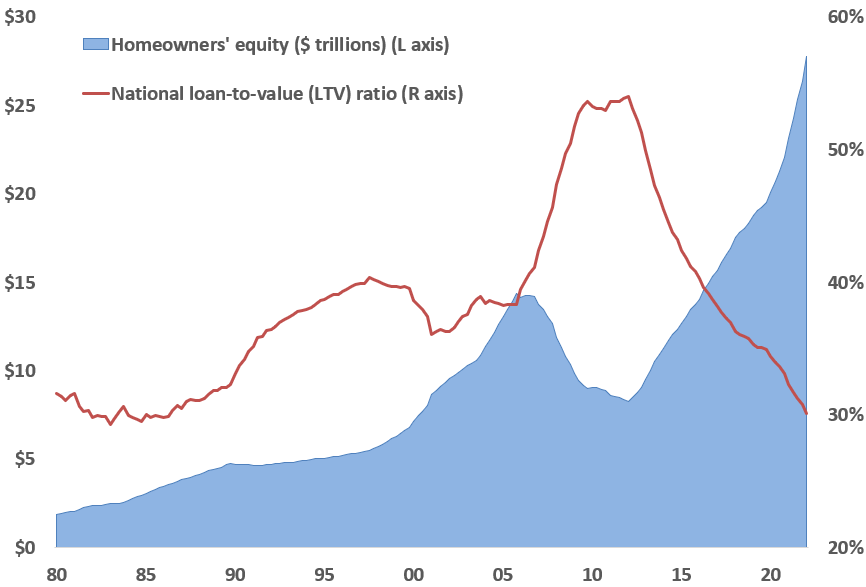

1. Home mortgage borrowers have huge amounts of equity to support their mortgages. And debt as a percent of home values is the lowest in at least two generations:

Federal Reserve

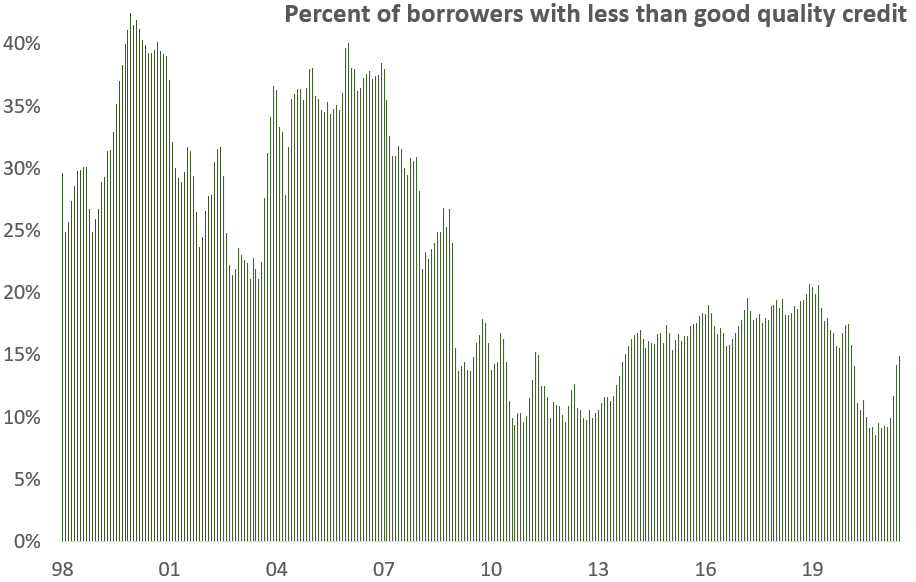

2. The quality of home mortgage borrowers is very high, and has been so for over a decade:

FHFA

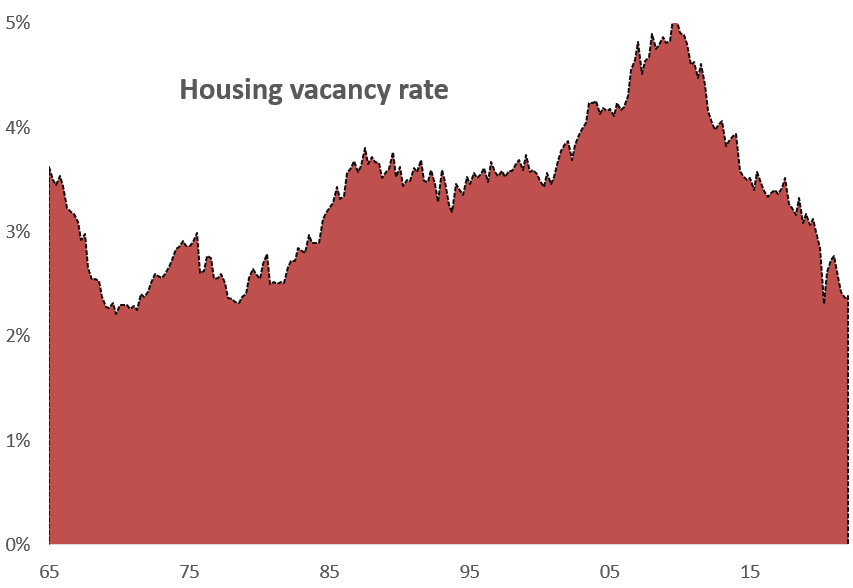

3. Housing is in seriously short supply, which supports home prices. Again, multi-generational lows, for both single and multi-family housing:

Census Bureau

4. Demand for hiring still far exceeds supply. This fact should materially limit the coming rise in the unemployment rate, which reduces the risk of home defaults:

Bureau of Labor Statistics

Hopefully, these charts persuade you that the key housing factors are the polar opposite of the ’07-’11 housing bust. If you do, keep reading. If not, check out another Seeking Alpha article. No hard feelings.

Redwood’s business units

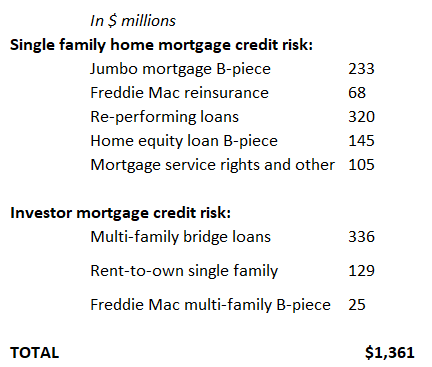

As I said, Redwood’s core business is managing residential mortgage credit risk. Most U.S. residential mortgage credit risk is managed by Fannie Mae and Freddie Mac – 63%, to be exact. And banks own another 20%. Redwood cannot profitably compete with them, so it looks for niches. A summary of its current net capital investments in each niche is:

Redwood Review

Jumbo mortgage B-piece. Jumbo mortgages are underwritten to (or close to) Fannie Mae and Fred Mac’s (the GSEs) underwriting guidelines, but are larger than the GSEs are allowed to insure. For example, the GSEs today can’t insure loans over $647,200. Redwood buys these jumbo loans from mortgage and commercial banks, then sells some as loans and securitizes the rest. The securitizations are broken into low credit risk A pieces and higher credit risk B-pieces. Redwood keeps the B-pieces, in keeping with its mission of managing residential credit risk.

Freddie Mac reinsurance are securities that Freddie Mac created for investors to share in its own home mortgage credit risk. Redwood is one of those investors.

Re-performing loans are home mortgages that many years ago were heading into default but were restructured, generally with more favorable terms for the borrower.

Home equity investments share in the home price appreciation of individual homes when they are sold in the future.

Mortgage servicing rights and other. Mortgage lenders earn 25-30 bp a year on mortgages for collecting mortgage payments for borrowers and passing along the payments to the owners of the mortgages. Redwood invests in the rights to a portion of these servicing fees.

Multi-family bridge loans finance the purchase and renovation of apartment buildings before selling them within a few years. The loans have 2-3 year maturities. Redwood sells most and keeps some.

Rent-to-own single family are to loans to owners of single-family rental properties, currently a booming business because of the housing shortage. Redwood provides mortgages for both individual homes and pools of homes. Like Redwood’s jumbo mortgage business, it sells some of the mortgages and securitizes some. Redwood invests in some of the securitizations.

Redwood’s risks

Redwood faces three risks:

- The macro risk of a sharp rise in home mortgage defaults

- The micro risk of poor loan underwriting

- A funding risk of having to use capital to meet margin calls on secured debt

I’ve already reviewed the first one above. Let’s address the other two.

Redwood’s loan underwriting risk

Redwood looks like it maintains pretty conservative lending standards. Here’s the data to support that view:

- The average loan-to-value (LTV) ratio of its jumbo mortgage investments, using current home values, was only 46% at the end of Q2, and the loans are fairly seasoned with 4-year average lives. The average FICO scores of the loans at origination were around 750.

- For its re-performing loan investments, the average LTV at present is only 44%, and the borrowers have been paying on average for 16 years.

- Redwood’s investor loans – the bridge loans, rent-to-own and multi-family B-pieces – all had original LTVs of 68-69% on average. The single family rental loans had debt service coverage (net income divided by debt payments) of 1.4 times.

Redwood’s margin call funding risk

Redwood uses debt financing to fund its long-term investments and to warehouse loans originated in its mortgage banking businesses prior to sale or securitization. For risk purposes, an important way to analyze its debt is to break it into “margined” and “non-margined”. The great bulk of Redwood’s debt uses its assets as collateral. For margined debt, if the market value of that collateral declines, Redwood is required by its lenders to come up with extra capital to support the debt. The risk is that a sharp decline in the market value of the assets used as collateral forces Redwood to sell assets to meet margin calls, assets that could have recovered their value over time.

That is exactly what happened when the COVID financial crisis hit in the spring of 2020, as this quote from the Q1 ’20 Redwood Review explains:

“During the last several weeks, we have made significant progress de-levering our balance sheet through asset sales and debt repayments…We have generated a substantial amount of cash and reduced our exposure to further volatility in asset prices by reducing both our marginable and absolute debt balances.”

Redwood has maintained this lower exposure to margin calls. Only 21% of its $3.1 billion of debt is currently subject to margin calls, compared to about 80% going into the COVID financial crisis. Redwood is therefore much more able to withstand another financial panic without having to sell assets into a weak market. That is especially important now because the company estimates that holding its current investments to maturity will add more than $3 per share to its current $11 book value.

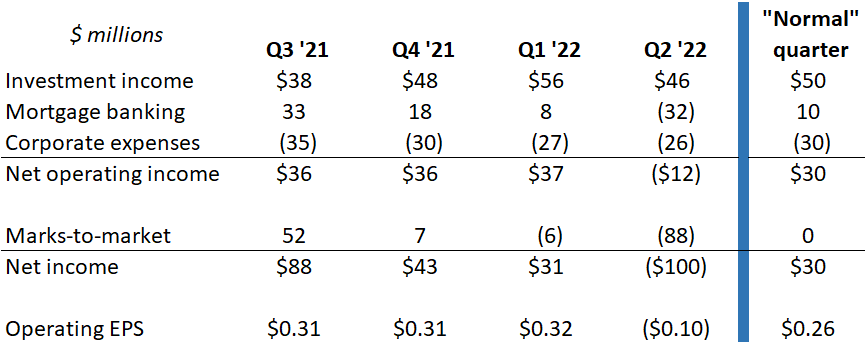

Can Redwood maintain its $0.92 dividend? My earnings forecast

Redwood’s last four earnings reports are excellent illustrations of the potential range of the company’s earnings. Here is a summary, plus my forecast of a normal quarter:

Redwood financial data

And here is a line-item review:

Investment income is the interest income Redwood earns from its investment portfolio, less the cost of managing it. It bounces around pretty materially quarter-to-quarter, in large part due to “amortization income”. Many of Redwood’s investments are valued on its books at discounts to par value. When the loans prepay more rapidly, the amortization of those discounts increases, and vice versa. My “normal” estimate assumes slow amortization and some investment portfolio growth.

Mortgage banking income is the net gains or losses Redwood earns on originating and re-selling its jumbo, bridge, and rent-to-own lending loans. Mortgage banking income does well when (A) home mortgage refinancing is active, and (B) mortgage rates are flat to down. Last Q3 was a great environment – national home mortgage originations were nearly $4 trillion annualized and the 30-year mortgage rate fell by about 20 bp during the quarter. This Q2 was the opposite – originations fell to $2.7 trillion annualized and the mortgage rate spiked from 4.5% to 5.7%. My forecast assumes more stable interest rates and relative weak home mortgage originations; essentially all of the mortgage banking income should come from Redwood’s bridge and rent-to-own originations.

Corporate expenses vary largely due to bonus pool accruals, which are tied to earnings.

Share repurchases could be a wild card. Redwood believes that its true book value per share, after collecting its loan discounts, is more like $13-14 than its current GAAP book value of $11. When the stock fell below $10 this past June, management started buying back its stock. It bought 3% of its shares during Q2. Its current $171 million repurchase authorization would allow it to buy back over 20 million shares, or a whopping 17% of its 116 million shares. If actually done, my normal EPS estimate would rise to $0.30 a share. I am confident Redwood will be a very active buyer this quarter.

The bottom line – I expect Redwood to keep paying its dividend

My quarterly EPS forecast of $0.26-$0.30 obviously exceeds Redwood’s current $0.23 quarterly dividend. There will likely be quarters where operating EPS is below $0.23, like Q2. But it took quite a bond market shock to do so. A nasty recession – not a mild one – could do the same. But short of that, I see Redwood maintaining the dividend.

I am therefore confident that buying the stock today should earn a 12.5% dividend yield for the foreseeable future. That seems worth doing.

Be the first to comment