gopixa

Redwood Trust (NYSE:RWT) is a real estate investment trust (‘REIT’) that specializes in the origination and investment of single-family real estate loans and investment property loans (known in the financial reporting as business loans). The company’s common shares pay a dividend yielding nearly 12%. Recently, the company issued preferred shares with a dividend of 10% (OTCPK:RWTRP) over the next five years, with a reset rate floor of 6.278% after that. Based on the company’s performance, I believe the preferred shares are a good holding for income investors.

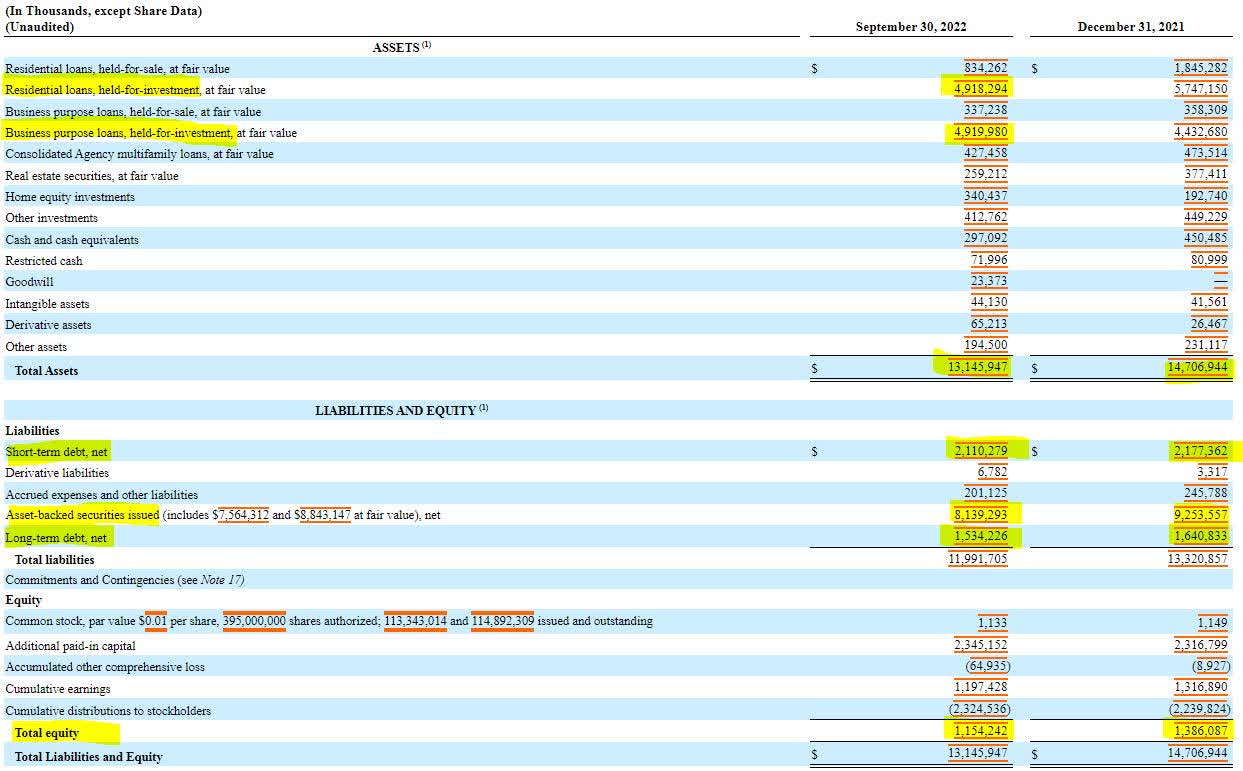

Redwood Trust’s balance sheet details the extent of its business operations. The company invests in a wide variety of loan products and real estate securities, but the bulk of its assets are comprised of residential loans (non-agency mortgages) and business purpose loans (mortgages against investment properties). Since the end of last year, the company has reduced the amount of loans it is offering for sale and the fair value of these loans has likely taken a hit due to higher interest rates. While short-term debt has remained unchanged, the company has reduced its asset-backed securities liability, but not commensurate with the reduction in the value of its assets. The result is a $230 million decline in shareholder equity.

SEC 10-Q

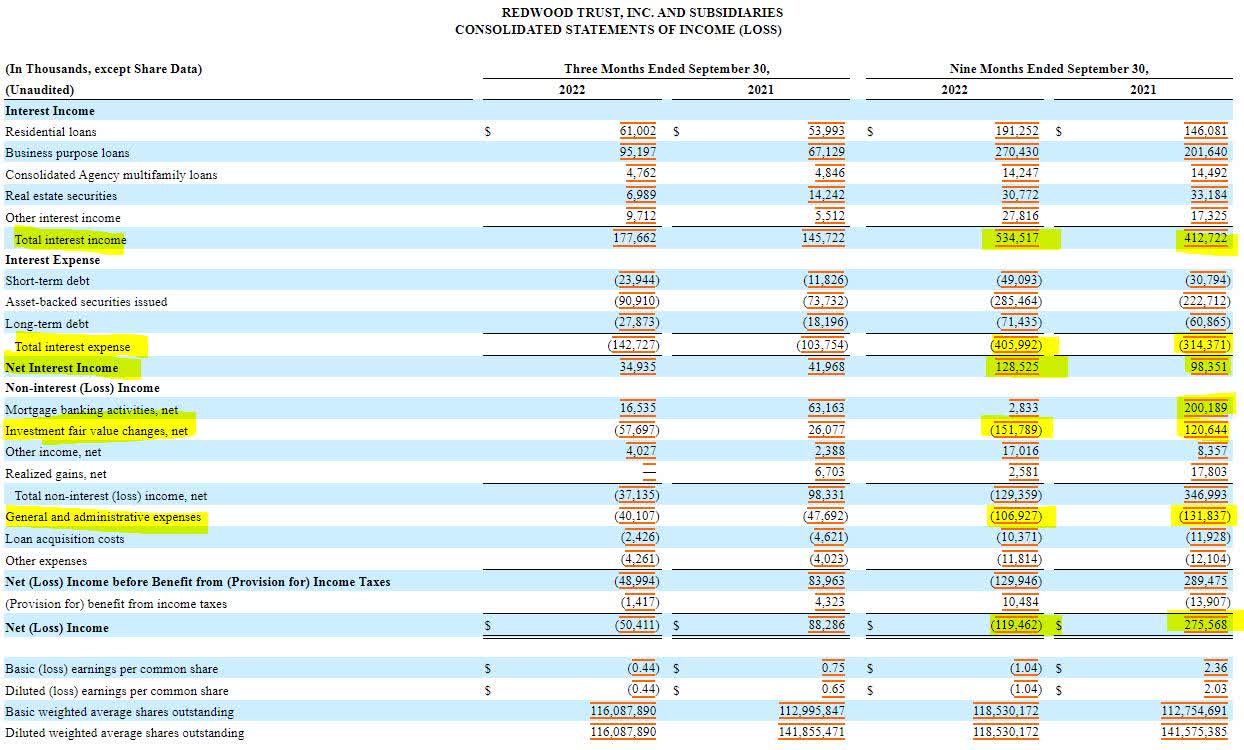

The company’s income statement sheds more light on the valuation of its assets along with Redwood Trust’s financial performance. Due to higher interest rates, interest income year to date is up $124 million, or more than 25% from the same period a year ago. Additionally, interest expenses have increased, but only by $92 million. The result is a $30 million increase in net interest income. Where Redwood Trust has hurt this year is the $151 million decline in the fair value of its investments, essentially a devaluation of the loans it holds. Fortunately, this is a non-cash expense. General and administrative expenses declined by $25 million, signaling that management is taking the challenging environment seriously.

SEC 10-Q

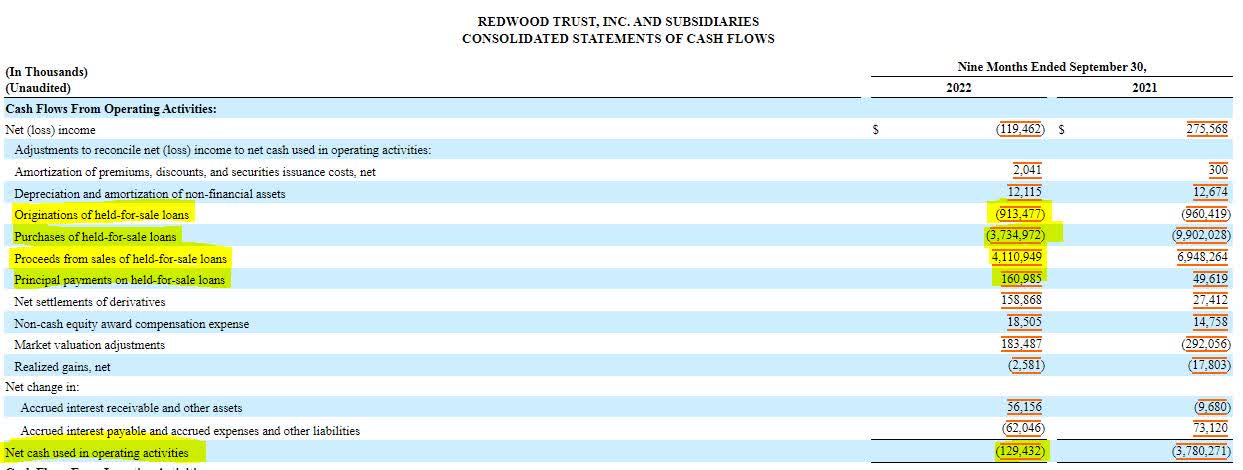

When it comes to Redwood Trust’s cash flow statement, it appears as if the company is heavily burning cash to operate. Redwood Trust reports loan originations, loan purchases, loan sales, and principal payments as operating activities. These activities are likely a day-to-day part of the operation, but I believe they are a little more discretionary than the remaining items. Therefore, I exclude them from my analysis to come up with $247 million in cash flow from operations, generated by the firm’s existing investments. By comparison, a year ago, the adjusted cash flow was $84 million.

SEC 10-Q

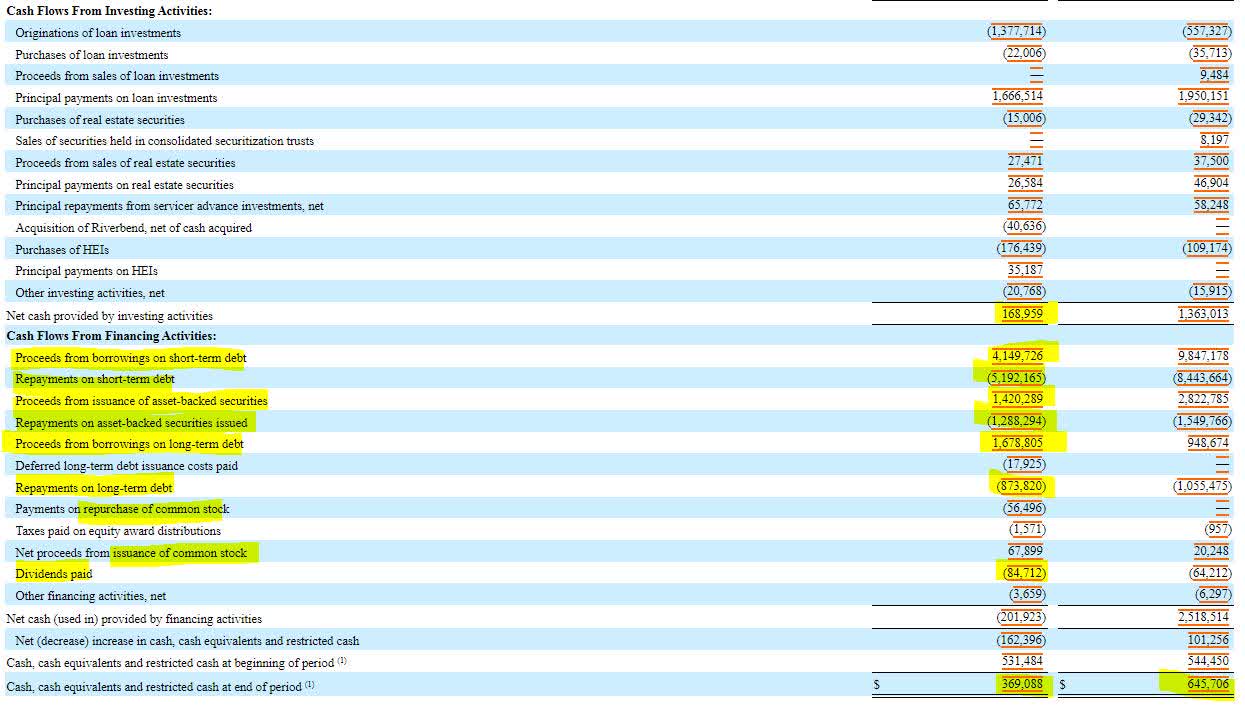

Redwood Trust used its cash to originate and purchase new loans, but also to reduce its debt. Of equal importance is the fact that Redwood Trust paid out $85 million in dividends, which is enough compared to the cash generated by the company’s investments. While the dividend obligation will grow with the issuance of preferred shares (by $6.5 million per year), preferred shares hold preference to common shares. The common share dividend would have to be eliminated to cut the preferred share dividend, which I believe would not be necessary given the current operating performance.

SEC 10-Q

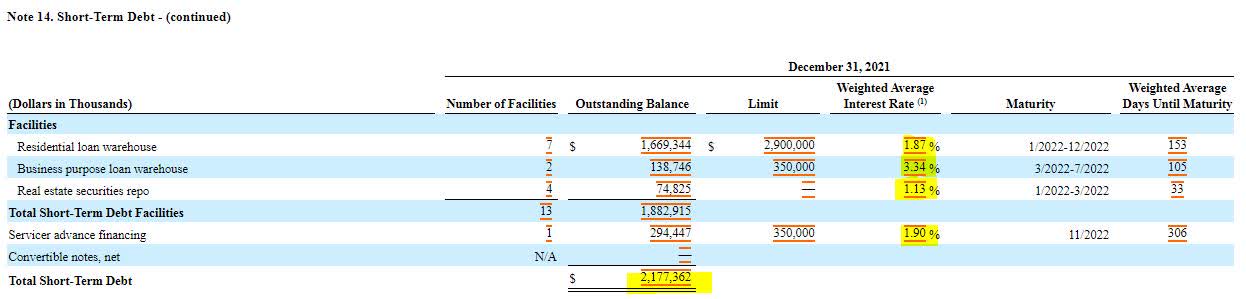

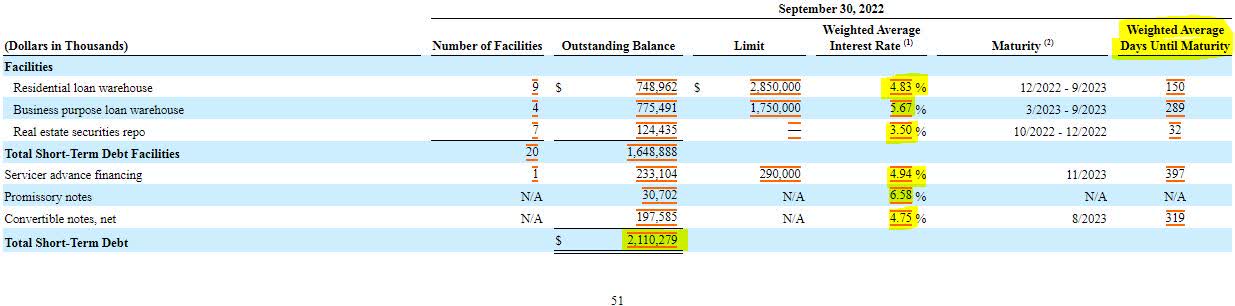

Redwood Trust is not naive to the fact that it faces risks related to the interest rate market. In its most recent 10-Q, the company noted that it expects interest rates to remain higher for several quarters, signaling that it is prepared for a prolonged decline in the mortgage market. When it comes to higher rates, Redwood Trust has seen $1.9 million of its $2.1 billion in short-term debt impacted by higher interest rates in the last nine months. These higher borrowing costs have the potential to erode cash flow and shareholder value.

SEC 10-Q SEC 10-Q SEC 10-Q

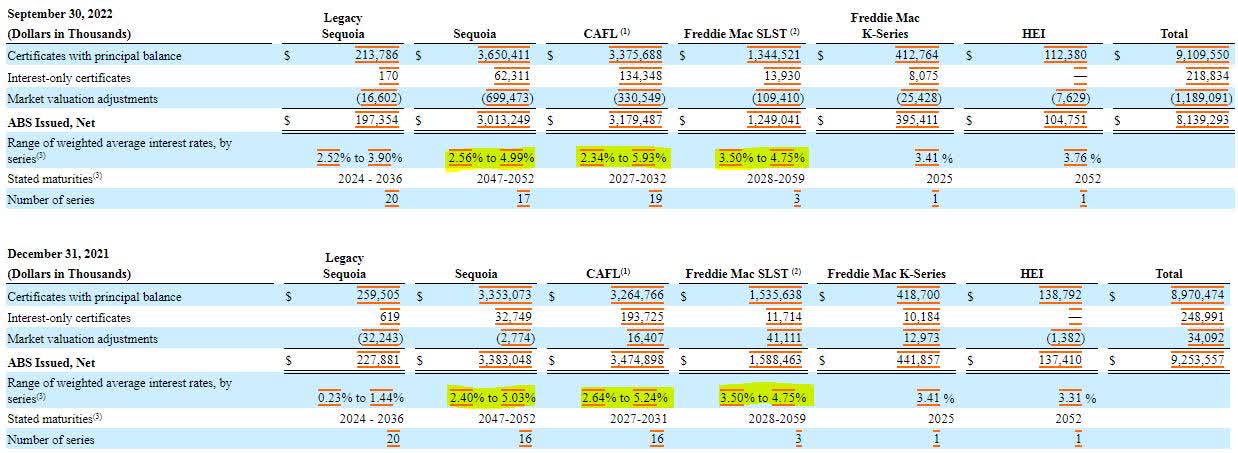

Fortunately, Redwood Trust seems to have taken steps to shelter itself. The interest on the company’s $8 billion in asset-backed securities liabilities, representing approximately two-thirds of its total debt, has remained relatively unchanged since the end of last year. While the legacy sequoia division saw interest rate increases, this division represents a group of loans underwritten prior to 2012 that is expected to phase out over time.

SEC 10-Q

The company has also reported a little over $450 million in liquidity between its cash and available capital. It is likely that the available capital disclosed in the company’s 10-Q was a part of the subsequent $65 million preferred share issuance. Additionally, the company has over $3.7 billion in available capacity from its warehouse credit facilities. These borrowings would be used to acquire new loans, which is the lifeblood of a company like this because continued principal payments by borrowers would reduce the portfolio’s income over time.

SEC 10-Q SEC 10-Q

I believe that Redwood Trust can pay both its common and preferred share dividends within the current environment. I have opted to purchase the preferred shares due to the additional seniority over the common shares. On a final note, readers may be interested in knowing that Redwood does have debt trading on the market, with yields as high as 11.5%. Unfortunately, these bonds are private placement and only available to institutional investors.

FINRA

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment