Severin Schweiger / Bernhard Haselbeck/Image Source via Getty Images

Investment Overview

Scilex (NASDAQ:SCLX) is a commercial stage biopharmaceutical company focused on developing and commercializing non-opioid therapies for patients with acute and chronic pain.

Back in May, Scilex announced that it would become publicly traded on the Nasdaq via a merger with Vickers Vantage Corp I, a Special Purpose Acquisition Company (“SPAC”) based in Singapore.

SPACs are often referred to as “blank check” companies since their objective is to raise money via an Initial Public Offering (“IPO”), and then either acquire or merge with an existing private company to help that company go public.

When listing, SPACs have no commercial operations of their own – their shares have a par value of $10, and they’re granted two years to complete an acquisition or merger, otherwise they must return funds to investors.

SPACs are seen as a faster way for companies to obtain a public listing – the process may take up to six months, while launching an IPO could take more than 12 months. They also provide a more “light touch” route to a listing, with less onerous reporting requirements, due diligence, and administrative processes.

Anyone can invest in a SPAC, from hedge funds to individual retail investors, but there is a caveat. The performance of SPACs post M&A over the past few years has been generally dismal.

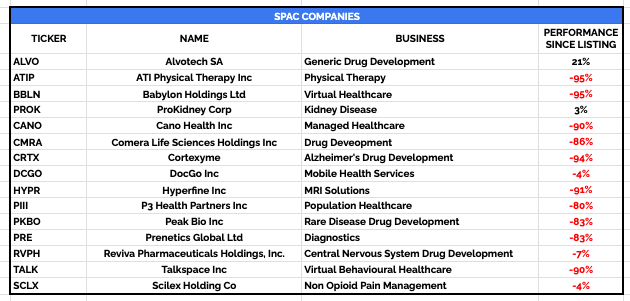

For example, I picked out 15 biotech or healthcare companies that have recently listed using a SPAC, and tracked their share price performance:

Performance of SPAC companies post acquisition / merger (TradingView)

As we can see, companies listing via SPACs have not just under-performed – nine of 15 companies have seen their share prices decline by >80%, and the average loss has been nearly 60%.

It’s not necessarily that the businesses are catastrophically bad. The poor performance can be attributable to other factors, for example, the desperation of a SPAC to find a company to acquire or merge with before its two-year window expires, or the unpreparedness of the acquiree company, that goes public much faster than management may have expected.

In the case of Scilex, based on the above, at its market cap valuation of ~$1.6bn at the end of last week, it seems as though the stock presented a fairly solid short sell opportunity (with the caveat that short-sellers’ losses can be almost unlimited, when the share price defies expectations and goes up instead of down).

This was arguably proven today, given Scilex stock has fallen in value by ~33% today (trading at $6.5 ), from >$11, to $6.5 at the time of writing

Arguably, companies that list via SPACs may simply need more time to establish themselves as public companies, and many of the above mentioned companies stock prices ought to grow in time once the businesses become better established.

Post M&A SPAC prices may simply be completely unrealistic, and investors need to wait for the stock price to reach a more natural valuation before making a decision on whether the underlying business is worth investing in or not.

In this post I will therefore take a look “under the hood” of Scilex and try to establish whether there is an underlying business here with genuine promise, capable of justifying of recouping the majority of today’s losses, or whether investors should expect the stock price to decline further during the course of 2023 until a more realistic valuation is met.

Scilex – Company Overview

Scilex and Vickers Vantage completed their business combination in November last year, with new CEO and Executive Chairman Henry Ji commenting:

Scilex is entering an exciting phase as the resources of the public capital markets will be available to enhance our business growth and enable us to continue to fulfill our mission to address patient pain management needs.

Another curious element of this deal is that Scilex is ~96% owned by Sorrento Therapeutics (SRNE), a San Diego-based biotech with a current market cap valuation of ~$500m, following a decline in the value of its shares of 86% across the past five years. With Scilex itself currently enjoying a market cap of $900m, it’s difficult to explain how Sorrento can be worth 2x less than the company it owns a 96% stake in.

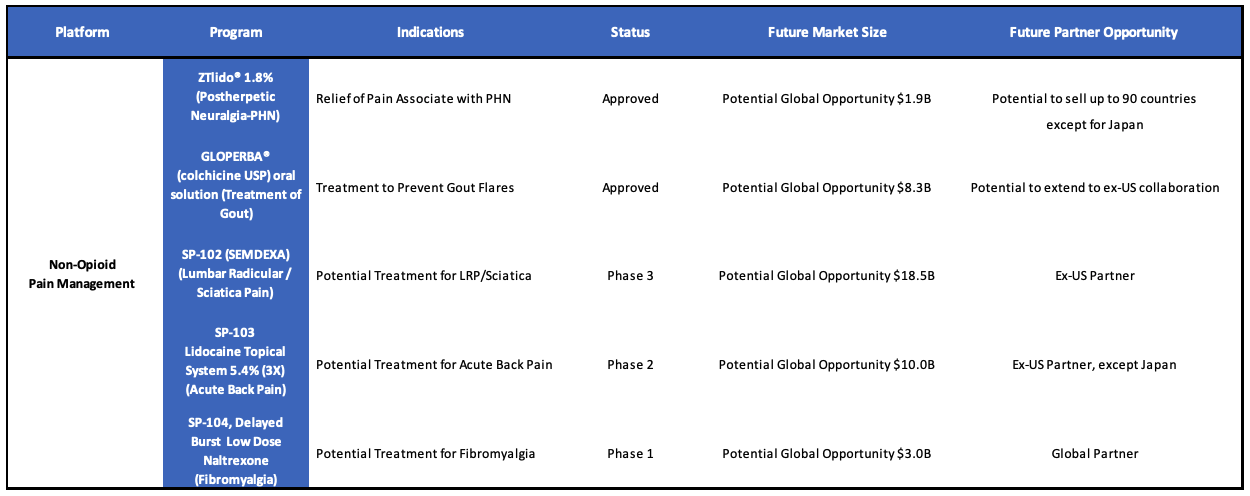

Moving on from this conundrum, Scilex does at least boast two FDA approved non-opioid pain therapeutics, as well as a pipeline of three further assets undergoing clinical studies.

Scilex product portfolio and pipeline (Scilex investor presentation)

ZTLido – Categorically Not A Blockbuster, But An Asset To Build Around

ZTLido is approved for relief of pain associated with Postherpetic Neuralgia (“PHN”) pain and was launched in 2018, while Gloperba was approved to treat adult gout flares in February 2019, although Scilex only in-licensed the US rights to market and sell the drug in June last year, and expects a full launch to take place this year.

ZTLido is a wearable painkilling patch with apparently superior adhesion to current standards of care, as proven in head-to-head studies.

ZTLido overview (Scilex investor presentation)

As we can see above, ZTLido has shown superiority to Endo International’s (OTCPK:ENDPQ) Lidoderm patches, and generic competitors, which gives it a good chance of taking a chunk of the 3.9m prescription, 147m patches-sold-per-annum addressable market.

The product was developed by Scilex Pharmaceuticals who had a New Drug Application rejected by the FDA in 2016, before Sorrento paid ~$48m to acquire Scilex, with 80% of that payment deferred until ZTLido was approved.

The drug was initially forecast by some analysts to achieve “blockbuster” (>$1bn per annum) sales, although in its merger approval documentation Vickers:

estimates that ZTLido has 5% share of the lidocaine patch market, which is estimated to have a current total addressable market size of US$1.8B based on publicly available annual prescription and prescription pricing data.

That equates to ~$90m sales per annum, which is roughly what Scilex management is guiding for in 2022: $93 – $98m – according to preliminary reported finances released by the company.

Interestingly, after reporting these results on Jan. 3, Scilex stock – which has fallen in value from $10 to <$3 after completing its business combination – leapt back up >$10 on the news.

That’s hard to explain when you consider current valuation implies a 2022 price to sales ratio of nearly 15x. A price to earnings ratio of ~15x would be impressive, but a P/S ratio of 15x would normally imply a company’s shares were at least a little undervalued.

Another concerning feature of the market outlook for ZTLido is that it already faces generic competition, with Scilex having filed a lawsuit against Apotex, which filed an abbreviated new drug application for a generic copy of ZTLido in May.

Gloperba – Larger Market, Added Competition

Gloperba has been in-licensed from ROMEG Therapeutics and addresses a much larger market than ZTLido of ~8.7m patients, which equates to a market opportunity of ~$8.3bn, management believes.

Gloperba is taken orally like cough syrup, making it patient friendly. Gloperba is a formulation of Colchicine, an anti-inflammatory drug that’s proven to lessen the buildup of uric acid crystals that cause gout – an extremely painful condition when it flares up.

The gout market may be a large one, and a nonsteroidal anti-inflammatory drug (“NSAID”) such as Gloperba preferable to e.g. corticosteroids, which are a popular treatment option, but there are several other therapies available.

One such treatment is Horizon Therapeutics’ (HZNP) Krystexxa, which is set to earn revenues of >$1.5bn in 2022, and with pharma giant Amgen (AMGN) set to acquire Horizon in a $28bn deal, Krystexxa will likely benefit from an increased marketing spend in 2023 and beyond.

Allopurinol is the most popular therapy for gout, and there are many versions of the generic drug available. Like Gloperba, allopurinol can be administered orally, albeit in pill form, so it remains to be seen if there’s a genuine market for Gloperba.

Scilex believes that its experienced sales force can establish Gloperba as a fixture in the gout treatment market, but as much as I like the cough syrup angle, blockbuster sales feel out of reach, given the Colchicine market is estimated at ~$800m in size by ROMEG.

My estimate is that Gloperba will likely drive similar revenues to ZTLido, and that $100m per annum in sales would be a decent achievement. If the opportunity were that much greater, why would ROMEG have agreed to out-license the US rights to the drug for apparently no fee?

Pipeline – Promising Sciatica Therapy, Triple Strength ZTLido, and Fibromyalgia

Scilex’ pipeline assets target markets in sciatica, acute back pain, and fibromyalgia that are worth ~$18.5bn, ~$10bn, and ~$3bn – over $30bn altogether.

SP-102 is likely the standout opportunity, being an injectable non-opioid novel viscous gel formulation that management believes is “on track to be the first and only FDA-approved epidural steroid product,” addressing a market of ~12m such injections per annum in the US.

With SP-102 apparently patent protected until 2036 (according to a Scilex corporate presentation) and Phase 3 studies completed, showing improvement against placebo over four weeks and continued effect over 12 weeks with reduced use of rescue therapy, with a clean safety profile, perhaps this is the asset that justifies Scilex’ near $1bn market cap valuation.

Or perhaps not, since steroidal injections are commonly prescribed off-label to treat lower back pain, implying the market opportunity may not be as large as management had hoped.

Scilex can admittedly show that its Phase 3 met its primary endpoint, and point to the fact that its treatment arm demonstrated significantly longer time to repeat injection (median 99 days) compared to placebo (median 57 days). Even so, for a company that wants to specialize in NSAIDs, SP-102 is an odd candidate to be pushing and there is no news yet on when – or even whether – a marketing application will be filed.

Moving to SP-103 – this is a triple-strength formulation of ZTLido to treat lower back pain, that was granted Fast Track Designation by the FDA last year. A Phase 2 study is underway, and given the study period is 28 days, results may be available this year.

My feeling here is that higher strength lidocaine may present some safety concerns (upping dosages was after all what started the opioid crisis) and again, is perhaps not exactly consistent with Scilex’s stated ambition to become an NSAID pioneer. In the case of SP-104, indicated for fibromyalgia, Naltrexone – marketed and sold under the brand name Revla among others – is already a well know alcohol and opioid use disorder therapy.

Scilex wants to use a low-dose formulation of the drug to treat Fibromyalgia, and I can see some merit in this – a low dose formulation is likely better than doctors prescribing Naltrexone off-label – although physicians often advise patients to make exercise and lifestyle changes as opposed to prescribing drugs.

I think Scilex may find it challenging to secure approval for SP-104, which is expected to begin a Phase 2 study this year – since it may be tough to prove that it works in Fibromyalgia patients, who are typically prescribed anti-depressants. I do think this is an intriguing opportunity that could spark a revival in Scilex’ fortunes, but objectively it can only be considered a speculative opportunity at present.

Conclusion – Scilex Mystery Gains Now Subject To A Major Correction – I’d Expect More Volatility and Would Only Buy <$3 per Share

Until today, Scilex was that rare thing – a SPAC merger holding onto its valuation post IPO. The upside generated by what can only be described as lukewarm sales figures for ZTLido was surprising based on most approaches to analyzing a company, and I am not surprised to see the valuation plummeting once again.

I would expect that there could be more volatility for short-term traders – short or long – to capitalize upon. I also believe that one or two elements of Scilex’ business model are intriguing, albeit unproven, including the “cough medicine” style gout therapy, and the sciatica and fibromyalgia opportunities.

The fact remains, however, that if a theoretical investor had heavily shorted every healthcare related SPAC without even bothering to check their pipeline and products, that investor would have done very well indeed, and although I’m not personally in the business of shorting companies it’s hard to see what is preventing Scilex escaping a similar fate.

Once Scilex stock finds its long-term trading range – and I would expect that to be ~$2 – ~$4, then it could be time to revisit the pipeline, monitor sales of ZTLido and Gloperba, and consider whether this is a SPAC that can buck a trend of underperformance – and also whether SPACs in general are being too heavily punished by a skeptical, risk-averse market.

Until then, however – and I suspect that time is at least six months away – I would steer clear of Scilex as an investment company – there are too many red flags and unanswered questions.

Be the first to comment