Galeanu Mihai

The strength of the US economy seems baffling to many, supporting the belief that a soft landing is possible. Much of what is currently being seen still appears to be related to the economy adjusting to the effects of COVID and the war in Ukraine. The impact of higher rates are still working their way through the economy, and the key threats to the economy continue to persist. Namely, consumers spending beyond their means and the housing market has frozen due to the combination of high rates and high prices. With inflation falling rapidly and a large backlog of housing under construction, it seems feasible that mortgage rates could fall and house prices adjust in an orderly manner without creating large problems. It is not clear that incomes can rise rapidly enough to support current spending before excess savings are consumed though. In any event, these situations likely won’t be resolved for 1-2 years, which could provide a near term tailwind for equity markets provided that inflation continues to decline.

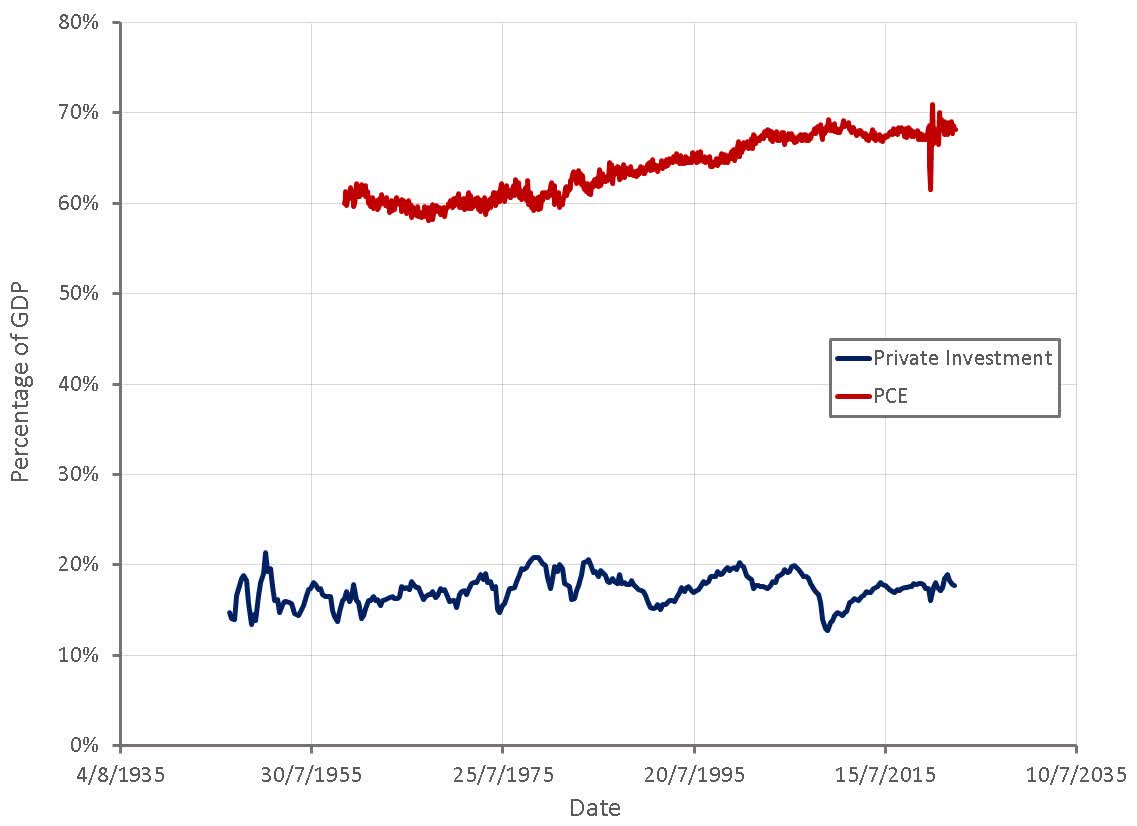

Investments are far more volatile and dependent on interest rates than consumer spending, although are far less important to a consumer led economy like the US. As expected, investments have responded more rapidly to the rise in interest rates over the last 12 months, but so far the broader impacted has been fairly limited. A large recession is unlikely without a substantial fall in consumer spending.

Figure 1: Private Investment and Personal Consumption Expenditures (source: Created by author using data from The Federal Reserve)

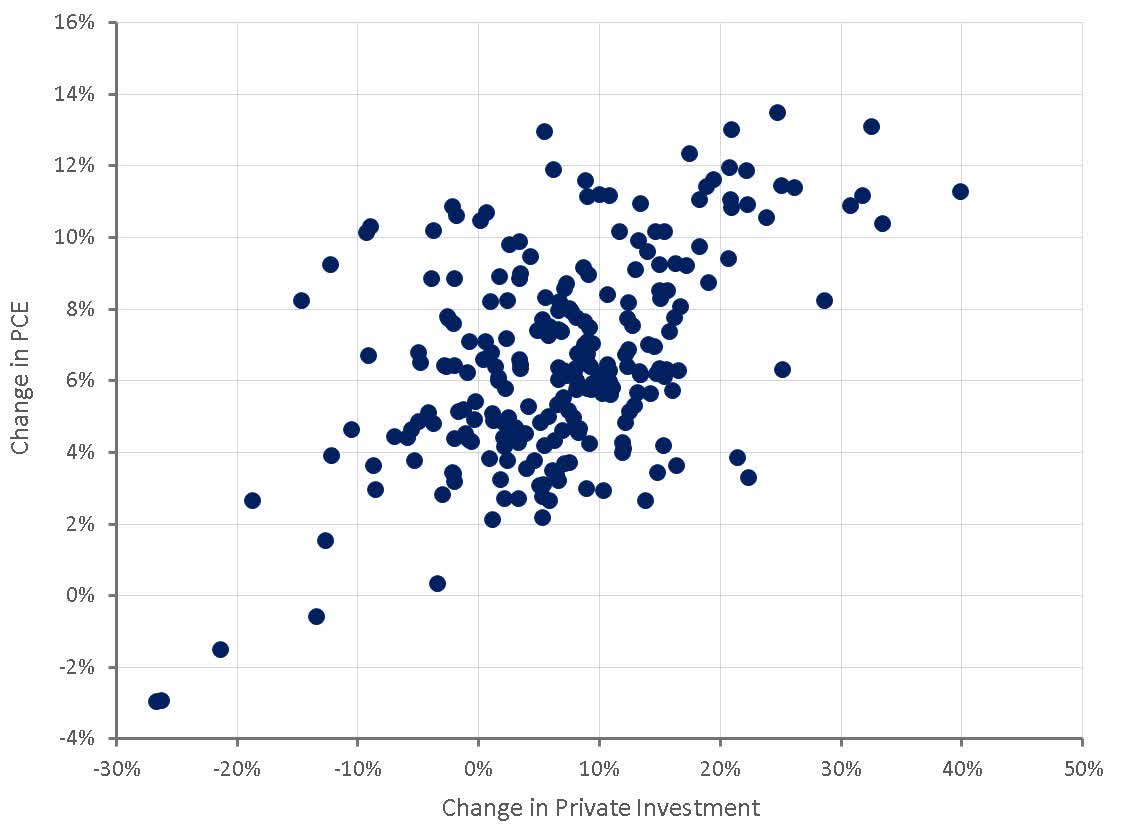

Investments and consumer spending tend to be correlated though, with investments generally leading spending. With the growth in investments falling rapidly in the second half of 2022, growth in consumer spending could be expected to follow in coming months.

Figure 2: Private Investment and Personal Consumption Expenditures (source: Created by author using data from The Federal Reserve)

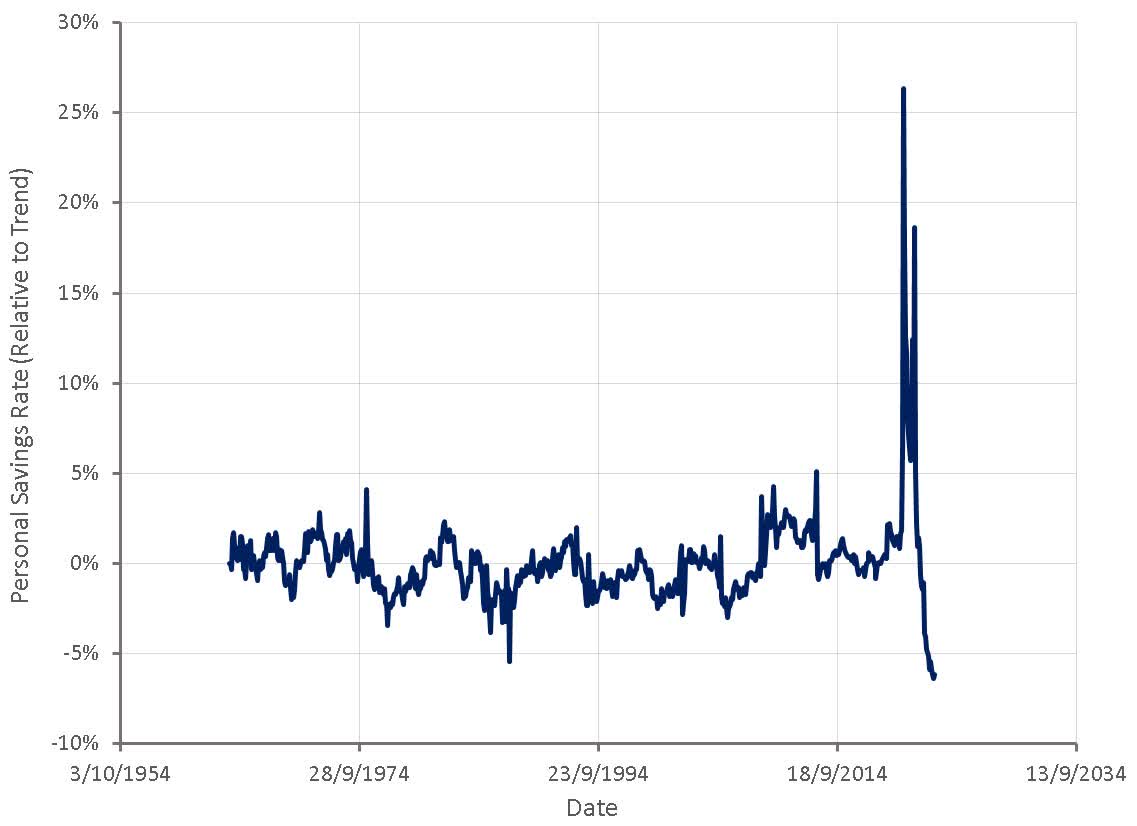

The sustainability of current spending levels could be key to whether there is a soft or hard landing. The personal savings rate is near record lows, as spending is extremely high relative to income. This is not really surprising given the excess savings accumulated during COVID, but investors need to look ahead to what could happen when excess savings are exhausted.

Figure 3: Personal Saving Rate Relative to 5 Year Median (source: Created by author using data from The Federal Reserve)

Excess savings have already dropped significantly, but remain fairly high. With current income and spending levels, excess savings are likely to be exhausted at an aggregate level sometime in the next 12 to 18 months. This is somewhat difficult to ascertain though as it depends on inflation, labor markets and consumer spending preferences. It should also be noted that savings are not evenly distributed across the population, and lower income individuals are likely already suffering due to inflation. This should result in a less rapid decline in excess savings going forward as higher income individuals will be less likely to need to draw down savings to support spending.

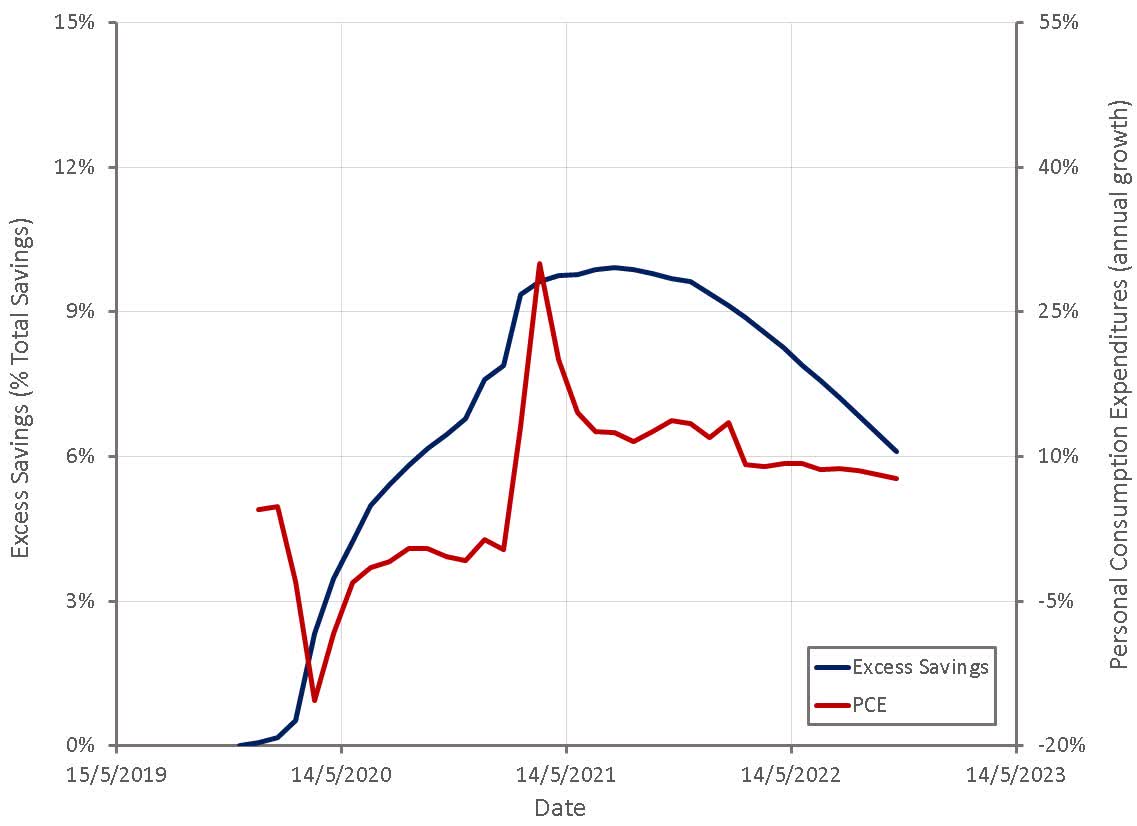

To avoid a recession, incomes will need to increase fairly significantly over the next 12 months so that the savings rate can normalize while spending remains robust. This appears like a low probability scenario though as labor markets are softening and the Fed seems intent on undermining them further.

Figure 4: Excess Savings and Personal Consumption Expenditures (source: Created by author using data from The Federal Reserve)

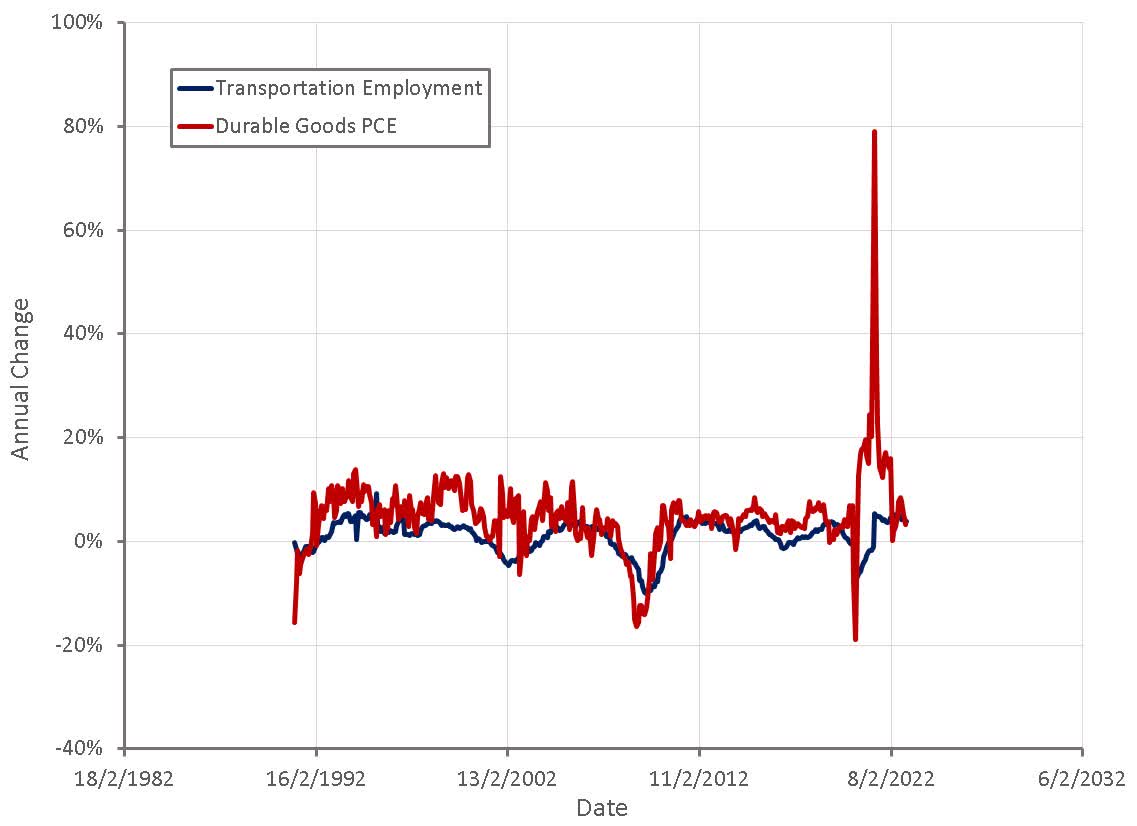

Excess savings continue to support high spending levels and as a result there are no early indicators of a recession led by a drop in spending. Growth in expenditures on durable goods has dropped from the COVID highs but remains robust. Employment in the transportation industry also continues to be strong. The fluctuations observed in freight and goods markets over the last year are most likely the result of demand normalization post-pandemic and a supply chain bullwhip effect, rather than anything more sinister.

Figure 5: Transportation Employment and Durable Goods Personal Consumption Expenditures (source: Created by author using data from The Federal Reserve)

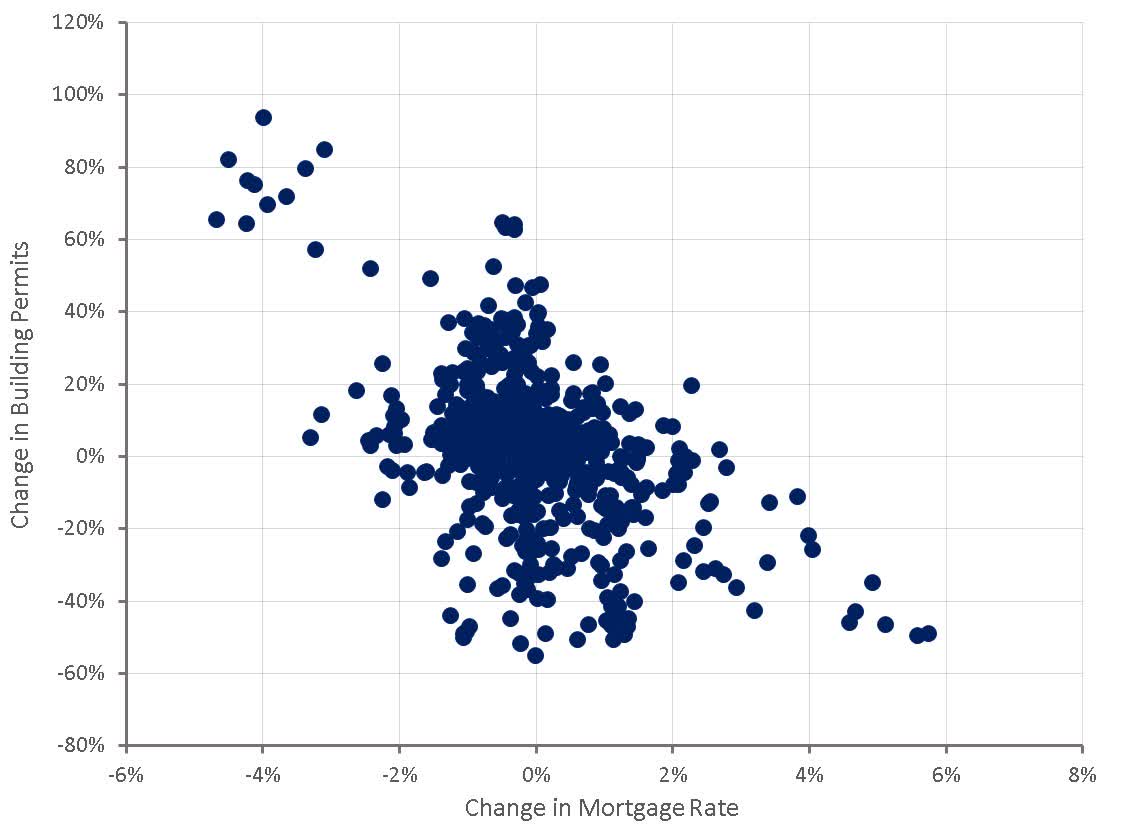

Housing is the other key risk to the economy and is also related to transportation employment and spending on durable goods. While the rapid rise in interest rates has crushed demand for the time being, construction activity has remained unscathed as there is still a large backlog of housing units under construction. If financial conditions ease sufficiently before this backlog is worked through, a housing recession could be avoided.

Figure 6: Impact of Mortgage Rates on Building Permits (source: Created by author using data from The Federal Reserve)

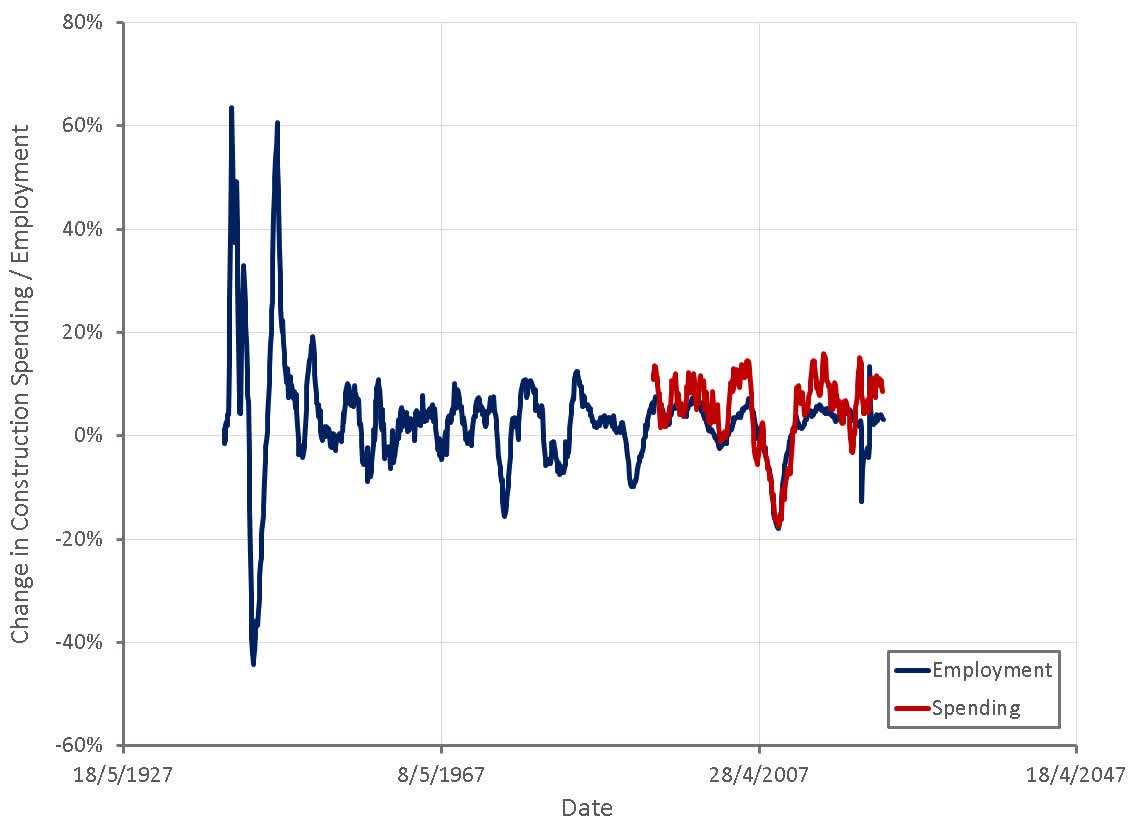

Construction spending and employment have so far shown little sign of weakness and hence housing has not presented a threat to the economy so far.

Figure 7: Change in Construction Spending and Employment (source: Created by author using data from The Federal Reserve)

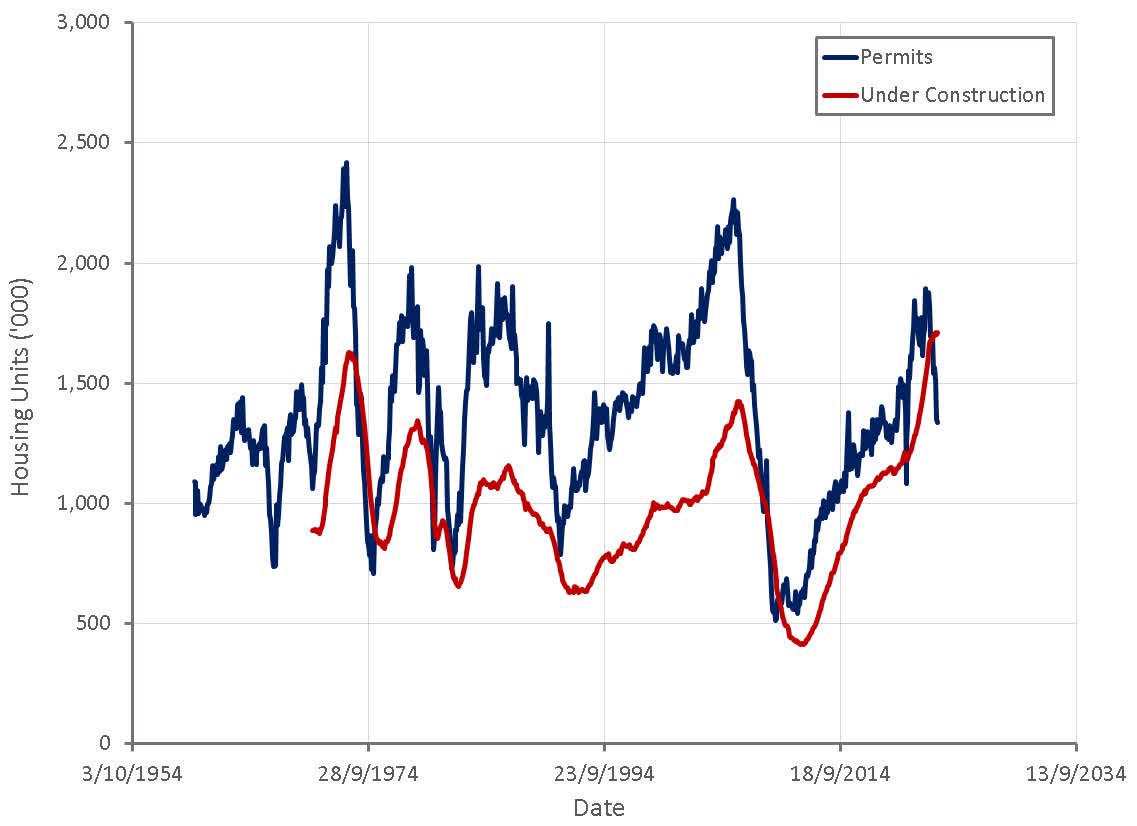

Permits tend to lead units under construction by around 6 months, and hence construction activity should be falling now. This has not occurred yet, but units under construction has levelled off over the past 4 months. Given the number of housing units under construction, it could take several years to work through the backlog, giving the economy ample time to adjust before a housing led recession occurs.

Figure 8: Building Permits and Housing Units Under Construction (source: Created by author using data from The Federal Reserve)

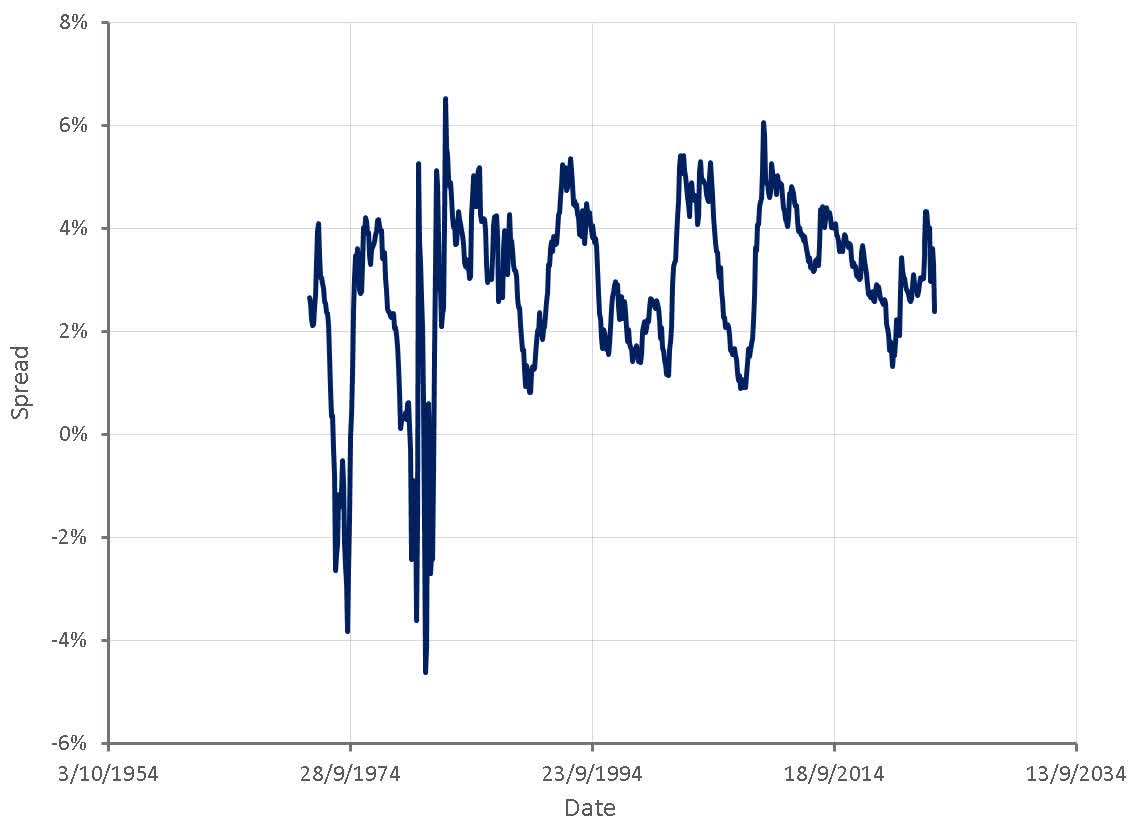

Mortgage rates will likely need to fall substantially to restart the housing market, but this will probably require a shift in monetary policy. The spread between mortgage rates and the Fed Funds rate has already compressed to near recessionary levels. It is difficult to see mortgage rates falling much further without the Fed cutting interest rates.

Figure 9: Spread Between Mortgage Rates and The Fed Funds Rate (source: Created by author using data from The Federal Reserve)

Even if mortgage rates drop significantly, allowing housing starts to reaccelerate, the balance of supply and demand in the housing market needs to be considered. Oft quoted studies point towards a housing shortage between 4 and 20 million housing units, but the methodology used in these studies needs to be understood. It has been suggested that this shortage exists due to a lack of construction after the global financial crisis and hence that there can be no housing recession. Rather, this shortage is more reflective of the fact that housing is not affordable for everyone. This shortage will always exist while house prices are high relative to income.

Over a period of decades housing has become an investment vehicle as much as a consumption good. In many developed countries prices have outpaced incomes for decades and now require two income households to take on a large mortgage that takes most of their working lives to repay. While there are obviously less houses than there are people who would like their own house, I believe calling this a shortage is something of a misnomer. If the suggested 4-20 million housing units were to suddenly materialize it would probably be the biggest economic disaster in recent memory. House prices in many places would crater leaving home owners with houses worth a fraction of their mortgage. Supply cannot be dramatically increased without crashing prices and large drops in house prices create enormous problems.

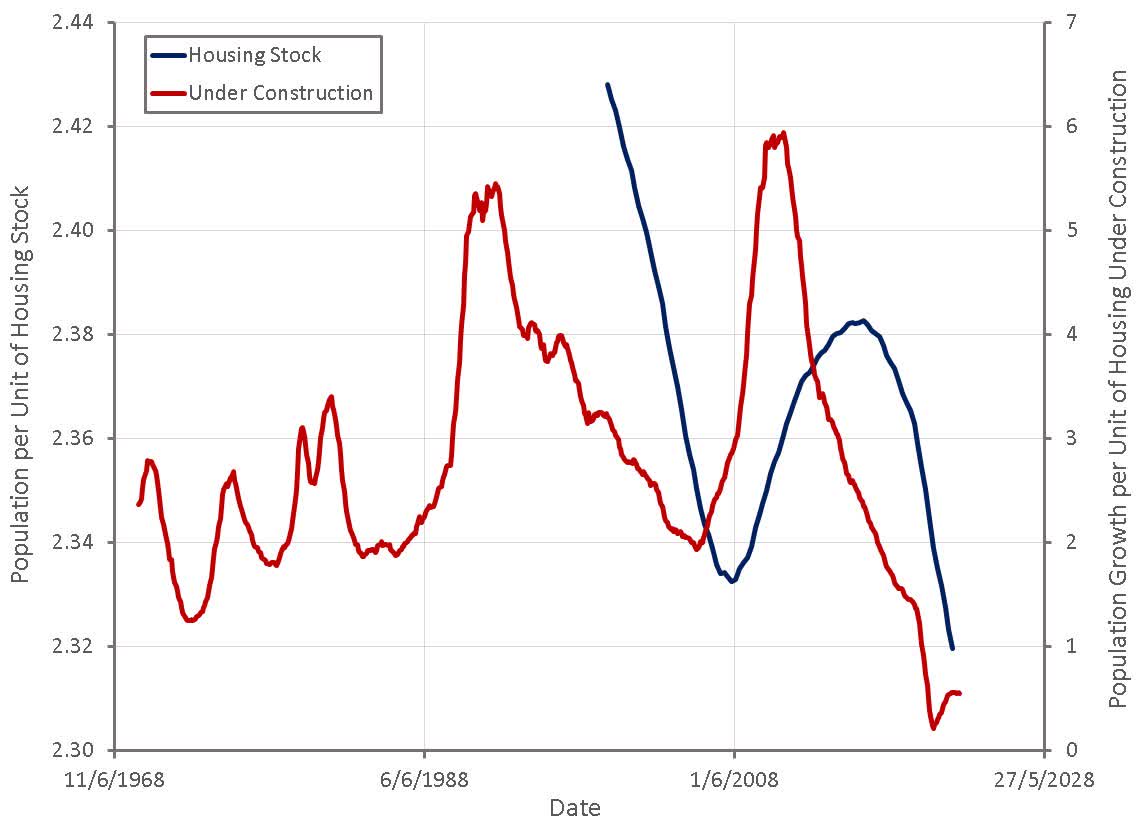

Historical data is likely a better indicator of how much supply the market can absorb before problems occur and this suggests at an aggregate level the market is becoming oversupplied. With population growth low and a historically large supply of new houses coming onto the market, supply is set to become even more abundant. Whether this can occur without prices falling substantially remains to be seen.

Figure 10: Housing Inventory and Units Under Construction Relative to the Population Size (source: Created by author using data from The Federal Reserve)

A soft landing will require mortgage rates to drop significantly before the housing backlog is consumed. It will also require incomes to increase significantly relative to inflation before excess savings are consumed so that current spending levels can be maintained. These situations will not come to a head in the short term though, providing space for equity markets to move higher as inflation fades.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment