By Anwiti Bahuguna

First, supply was the concern. Now demand is dropping – and recession risks are clearly elevated.

When the news of the novel coronavirus first began to emerge from China, economic analysis was generally focused on the disruption of supply chains and the effect on companies unable to easily relocate manufacturing. Now that companies and consumers are cutting back on spending, a drop in demand has heightened fears of a sharp slowdown in economic growth. A collapse in oil prices has added to concerns.

The growth outlook dims

Recession risks are now clearly elevated, and we expect that there will be a hit to U.S. growth. It’s also clear that the extent of the decline will depend on the severity and the duration of the coronavirus infections. If the outbreak disrupts demand for a prolonged period – beyond the next two months – the impact on growth will be that much more significant. Swift and draconian actions have led to containment in some East Asian countries (China, Singapore), but it’s evident from Chinese data (and likely from Italy’s data to follow) that these measures also take a severe toll on economic growth.

Further headwinds: Falling oil prices and capital expenditure

The experience of 2015-2016 has shown that a decline in oil prices is no longer a net positive for the U.S. economy. It may benefit consumer pocketbooks, but at times of uncertainty, people are likely to save the windfall and reduce their spending. Because of the sharp fall in oil prices, we cannot rule out the risk of credit downgrades and increased defaults among energy companies – which could spill over to other segments of the U.S. economy. Our expectation for capital expenditure (capex), specifically in energy production, is for deep cuts – perhaps to zero in 2020 – which will also be a drag on growth.

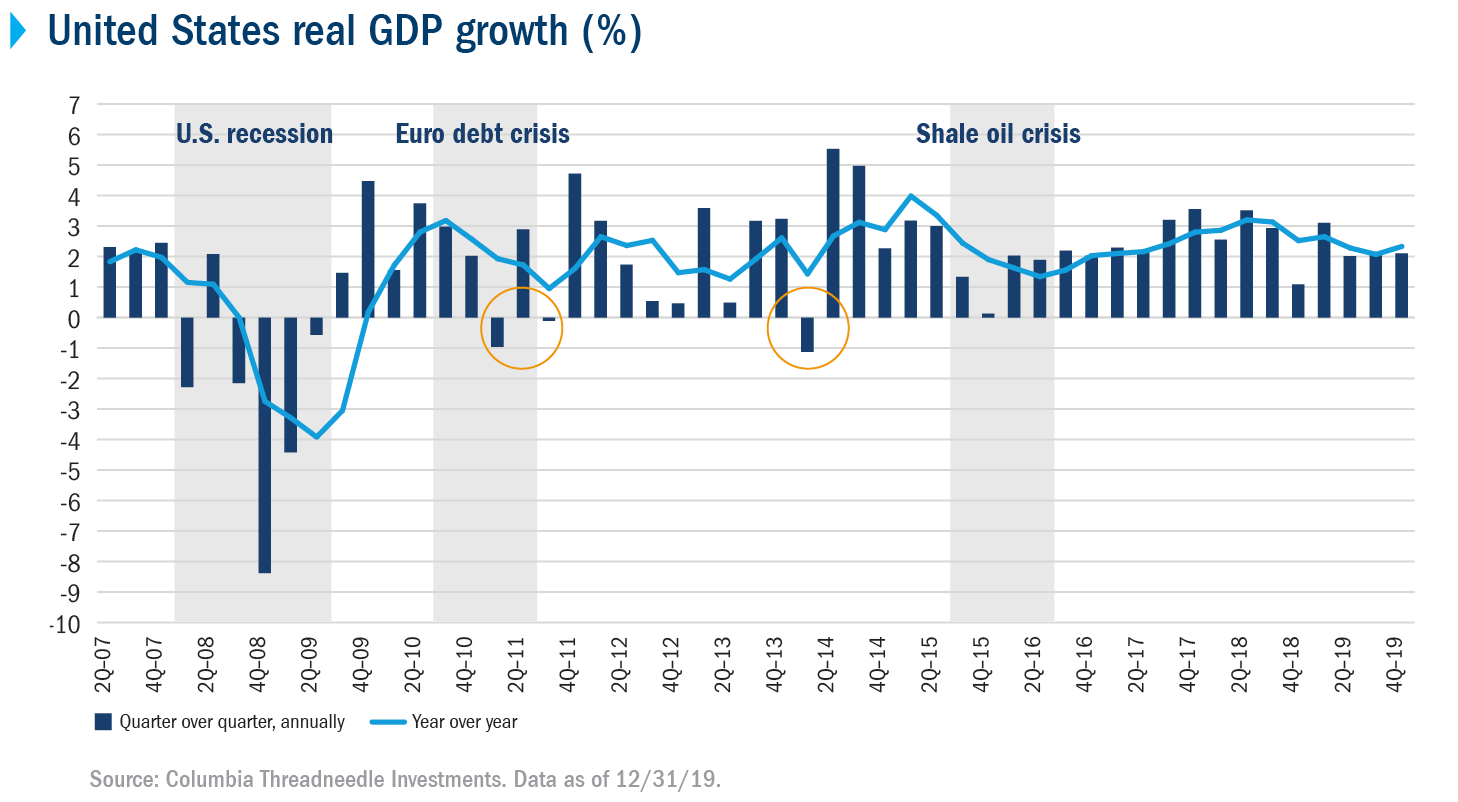

Watching for how consumers and businesses react

The current expansion is the longest on record, and there have been three instances of negative quarterly growth. And yet the economy has continued its long upward grind.

{kind=link}

If containment and mitigation efforts appear successful in the U.S., we expect the coronavirus hit to growth to be short-lived. In addition to public health efforts, a lot depends on how businesses and consumers react. U.S. companies will likely see an impact on earnings, but it’s not clear how they will respond. Consumers are also likely to be affected, and we need to understand if they retrench spending sharply or benefit from lower rates and lower oil prices. Leading indicators to help assess these responses include the Institute of Supply Management Purchasing Managers’ Index, a widely watched indicator of recent U.S. economic activity, consumer and business sentiment indicators, and monthly payroll data.

Catalysts for improvement

The most significant catalyst for improvement will be limiting the spread of coronavirus, but monetary and fiscal responses will also be important to ensure that companies can continue to borrow if they need to fund operations.

- Monetary policy: It’s evident that the Federal Reserve Board is prepared to act quickly and decisively, and the Fed’s activities and forward guidance can help stabilize market sentiment. Cutting rates is less important than keeping the credit channels open. Maintaining liquidity in the markets will be essential.

- Fiscal policy: We also need a well thought out and targeted fiscal response to support demand in the economy. The U.S. administration announced $8.3 billion in emergency funding, and more is likely to come. China is coordinating monetary, fiscal and credit programs.

Bottom line

If the coronavirus disrupts demand for a prolonged period – beyond the next two months – the impact on growth will be far more significant. Ongoing economic reports may continue to fuel volatility as investors digest the data, and it will be important for investors to distinguish between backward-looking reports (e.g., retail sales, payroll) and forward-looking indicators, like sentiment.

Disclosure:

© 2020 Columbia Management Investment Advisers, LLC. All rights reserved.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus. The prospectus should be read carefully before investing.

Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund’s most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here. These reports and other filings can also be found on the Securities and Exchange Commission’s EDGAR Database. You should read these reports and other filings carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA. Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

NOT FDIC INSURED · No Bank Guarantee · May Lose Value

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment