SDI Productions

By Breakingviews

When it comes to the possibility of a recession, some U.S. bank executives are saying the quiet part out loud. Not only would the largest lenders survive even a savage economic downturn, but they may emerge stronger from it.

Bank chiefs talk openly about a coming crunch, but don’t seem to fear it. Citigroup’s (C) Jane Fraser said in July that banks depend on capital, liquidity, credit quality and reserves in a recession, and that she feels “very good about all four.” JPMorgan (JPM) boss Jamie Dimon, has warned of an economic “hurricane”, and told clients two weeks ago that there might be a 40%-plus chance of a hard recession or even “something worse”. Yet he also boasted in July that even when Lehman Brothers collapsed in 2008, his firm remained profitable.

This isn’t hubris. Big lenders are better prepared for a rough ride than they were before the last big financial crisis. That’s not entirely through choice: The Federal Reserve forces banks to hold capital sufficient to absorb colossal amounts of red ink. JPMorgan, for example, must be ready for a $41 billion loss. As of 2020 lenders also have to pre-emptively take charges against today’s profit to cover future estimated bad debts. That’s something they hate but which leaves them even more thickly padded.

Dimon and his peers have also done some economic cherry-picking in recent years. Risky second-home mortgages and leveraged loans are out; so-called prime customers are in. Under boss Brian Moynihan, Bank of America (BAC) has cut its mortgage lending by roughly $130 billion since 2009, while lending an equivalent amount to clients of the bank’s wealth and investment management division. And lenders have shored up their liquidity, the lifeblood of a bank when markets seize up. Bank of America and Citi each had nearly $1 trillion of cash, and investments they could easily turn into cash, at the end of June.

It’s one thing to say big banks can survive a recession. What’s less loudly spoken about is the idea they can benefit from one. Some of their businesses are less exposed to the direction of the economy: Dealmaking may slow in hard times, but trading desks tend to do well when financial markets are volatile, on the way down as well as on the way up.

More importantly, a recession is likely to be more punishing for the young technology firms that are proving banks’ most troubling source of competition. Most digital-only banks and buy-now-pay-later services have yet to experience a downturn. Many need fresh capital, which becomes harder to raise as the economic picture deteriorates.

Besides, as Dimon points out, in a recession “certain things get cheaper”. This includes staff, whose pay is already falling sharply after taking account of inflation. An adjustment in the labor market could also help Wall Street firms looking to hire tech-savvy employees who can help build out their digital products and backstage technology. As big tech firms like Microsoft (MSFT) and Meta Platforms (META) lay off staff, banks become more attractive employers.

Potential takeover targets are getting cheaper too: Shares in online brokerage Robinhood Markets (HOOD), which competes with JPMorgan and Morgan Stanley (MS), have fallen nearly 50% this year. Privately held payment powerhouse Stripe has cut its internal valuation by 28%, the Wall Street Journal reported in July. Cashed-up banks may find a downturn gives them an opportunity to swoop.

Whether a recession is long, short, hard, soft or non-existent, banks are already priced for misery. Big lenders’ stocks are currently trading around 20% below share price targets set by research analysts, according to Morningstar. Though analysts tend to be overoptimistic, such that there is typically a small gap between their targets and where shares actually trade, the discount is now over half the 40% it reached during the recession of March 2020. At its widest in 2008, it was around 60%.

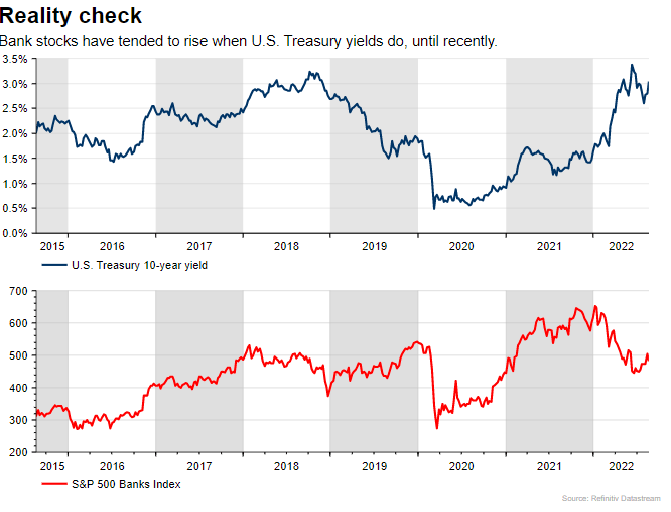

By another gauge too, investors are already being too harsh. Bank stocks tend to track the yield on U.S. 10-year Treasury bonds, in a broad reflection of the fact that when long-term interest rates go up, lenders make more money. That relationship has reversed for much of 2022. PNC Bank (PNC) Chief Executive Bill Demchak told analysts last month that the fall in valuations is “just wildly wrong” even in a worst-case scenario, adding that a downturn would help banks recapture some kinds of business that had gone elsewhere.

What’s clear is that a few years from now, big banks like JPMorgan will still be around, while some of their most aggressive new rivals will not. And more likely than not, the U.S. economy will eventually recover from any downturn. So while a recession may be brutal for customers, employees and Americans in general, for banks it could be a gift in disguise.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment