Lurin

Whitestone REIT (NYSE:WSR) recently announced that it had sold several of its assets, and we believe that these sales confirm that WSR is heavily discounted.

Before highlighting these asset sales, we first provide a quick overview of the company for those of you who aren’t familiar with it, and we then share an updated NAV analysis of the company.

Whitestone REIT: Growth at a Value Price

WSR is a retail REIT (VNQ) that specializes in service-oriented strip centers in strong sunbelt markets. Retail is today hated by most investors due to the threat of e-commerce and the risk of a near-term recession. But these retail properties are actually quite defensive because they focus on services that you cannot get online, or at least not with the same level of convenience, and these services are mainly recession-proof.

Think about a grocery store, a barbershop, a fast-casual restaurant, a gym, a dry cleaner, and a coffee shop. That’s the type of tenant that you will find at WSR’s strip centers. Just to give you a few examples, some of its tenants include Trader Joe’s, Whole Foods (AMZN), Chipotle (CMG), and Planet Fitness (PLNT):

Whitestone REIT Whitestone REIT

Besides, real estate is all about location, location, and location…

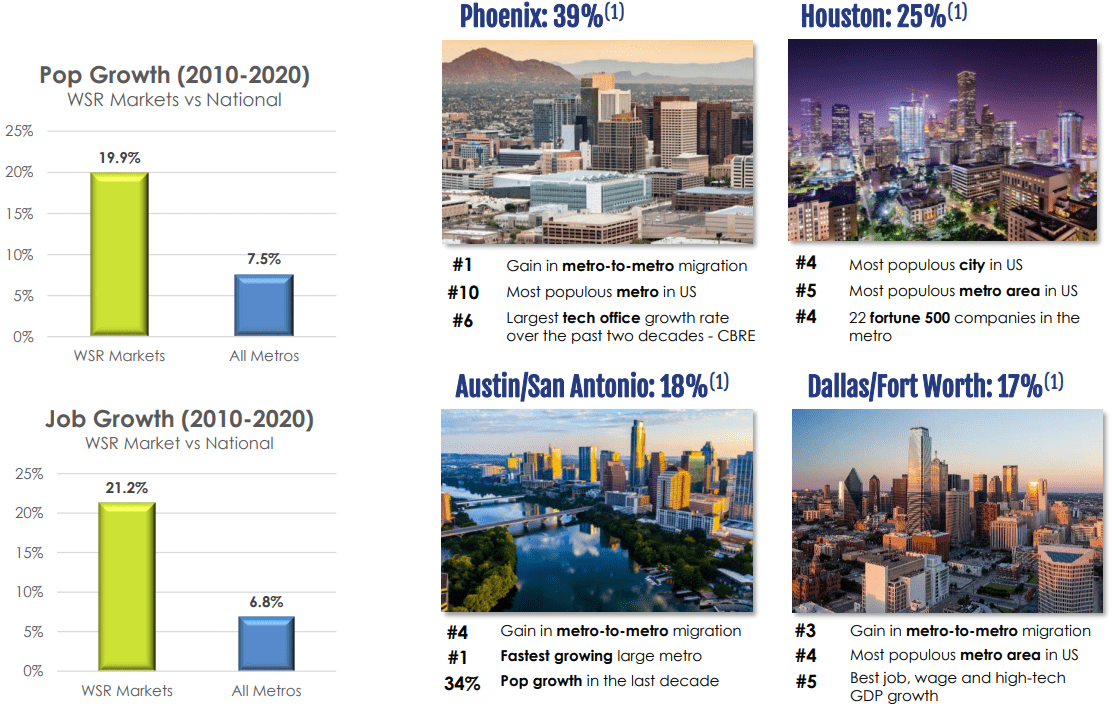

And WSR’s properties happen to be in some of the best neighborhoods of Phoenix (#1 market in terms of housing appreciation during the pandemic), Austin (#2 market in terms of housing appreciation during the pandemic), San Antonio, Dallas, and Houston (also among the top markets in the nation).

These markets are growing rapidly because a lot of companies are moving there to lower their taxes and other costs. They naturally bring a lot of jobs with them and people then follow jobs. The job growth of its markets has been nearly 3x the national average prior to the pandemic and this trend has only accelerated since then:

Whitestone REIT

So WSR owns very desirable properties that are e-commerce and recession-resistant, and they are set for long-term growth in rents and appreciation as a result of desirable demand/supply dynamics in its markets (growing population that’s becoming more affluent, but limited supply of good retail properties).

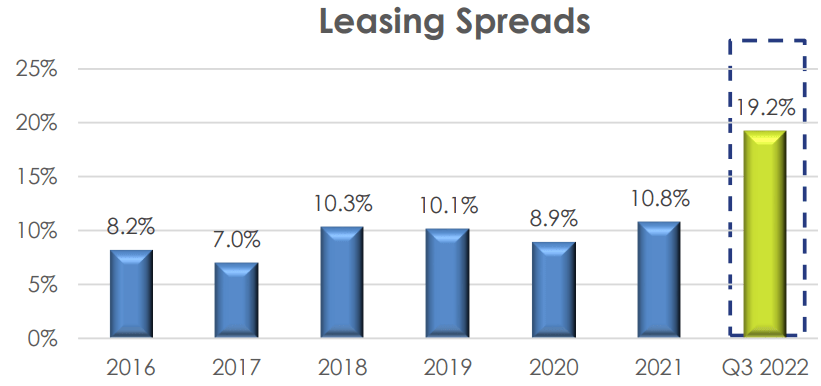

Its rents have been growing fast for years, with ~10% releasing spreads on top of 3% annual rent escalations, and this growth recently accelerated to nearly 20%:

Whitestone REIT

Despite that, WSR is today the cheapest REIT that specializes in service-oriented strip centers in the sunbelt markets.

For a long time, the market would price WSR at a low valuation because its management was overpaid and conflicted. Its strong fundamentals were overshadowed by ill-advised equity raises that diluted shareholders, and caused the FFO per share to stagnate. The market rightfully punished WSR with a low valuation multiple.

But earlier this year, the board finally fired its CEO, greatly improved the company’s corporate governance, and hired new executives that are set to unlock value for shareholders. I have held several phone calls with the new CEO and I am convinced that the company is now headed in the right direction and it is only a question of time before the market reprices WSR at the higher valuation that it deserves.

This is why WSR is one of our favorite opportunities in today’s market.

It is still priced at a “value multiple” as if it was a low-quality REIT that’s poorly managed. Right now, It is priced at just 9x FFO and a 30-50% discount to its net asset value, depending on the assumptions that you use.

But in reality, WSR has become a high-quality REIT, and it deserves a “growth multiple.” The market has been slow to react to the recent changes, but our access to the management for regular calls has given us a head-start to gain a better understanding of their future plans to maximize shareholder value.

We discuss this plan in a recent CEO interview article that you can read by clicking here, but in short, they plan to:

- Set a track record of rapid same-property NOI growth.

- Sell some assets to demonstrate the value of their portfolio.

- Reinvest the proceeds into higher-yielding projects.

- Deleverage the balance sheet.

- All while also exploring other strategic alternatives and buybacks.

The thought here is that this should remove all other “excuses” that the market might have for pricing WSR at a discount.

And here comes the good news!

Recently, WSR announced that it had sold two of its properties, which is very bullish for our investment thesis.

Below, we explain why:

Asset Sales Confirms Whitestone’s Discounted Valuation

In my previous discussions with the CEO, he explains that a ~6% cap rate would probably be fair for its portfolio. I think that this is fair given that its properties are located in highly desirable sunbelt markets, enjoy rapid growth prospects, their rents are below market, and occupancies have further potential.

The CEO has told me that they think that the near-term forward normalized NOI of their portfolio is around $100 million. They are not there yet, but as we noted earlier, releasing spreads are near 20% at the moment and leases are fairly short at just around 3.5 years on average. Their occupancy rate is also rising rapidly, but still at just 92%, and they have $150 million worth of development investment potential in their portfolio, which should generate an additional ~$15 million of NOI when completed.

Even if you use today’s lower NOI base of ~$85 million, you would get a $15 NAV per share using a 6% cap rate, which compares very favorably to the current share price of $9.5. This NAV should grow rapidly as rents are lifted closer to the market rate, occupancy makes further gains, and the development projects are completed.

So, clearly, the market appears to question the 6% cap rate assumption. Investors appear to think that it is too optimistic in today’s environment.

Well, WSR just announced that it had sold six of its properties at a 5.6% cap rate and these properties don’t seem to be above average in terms of quality.

On the contrary, their rents and occupancy rate would lead you to think that these assets are worse than the average of their portfolio.

| Sold properties | Rest of the portfolio | |

| Occupancy rate | 90.3% | 92.5% |

| Rent per square foot | $14.51 | $22 |

These metrics alone don’t necessarily mean that these properties are poor investments, but typically, more desirable properties will have higher rents and occupancy rates. The sold properties are materially lower in both cases, and if their growth potential was very significant, WSR would have kept them.

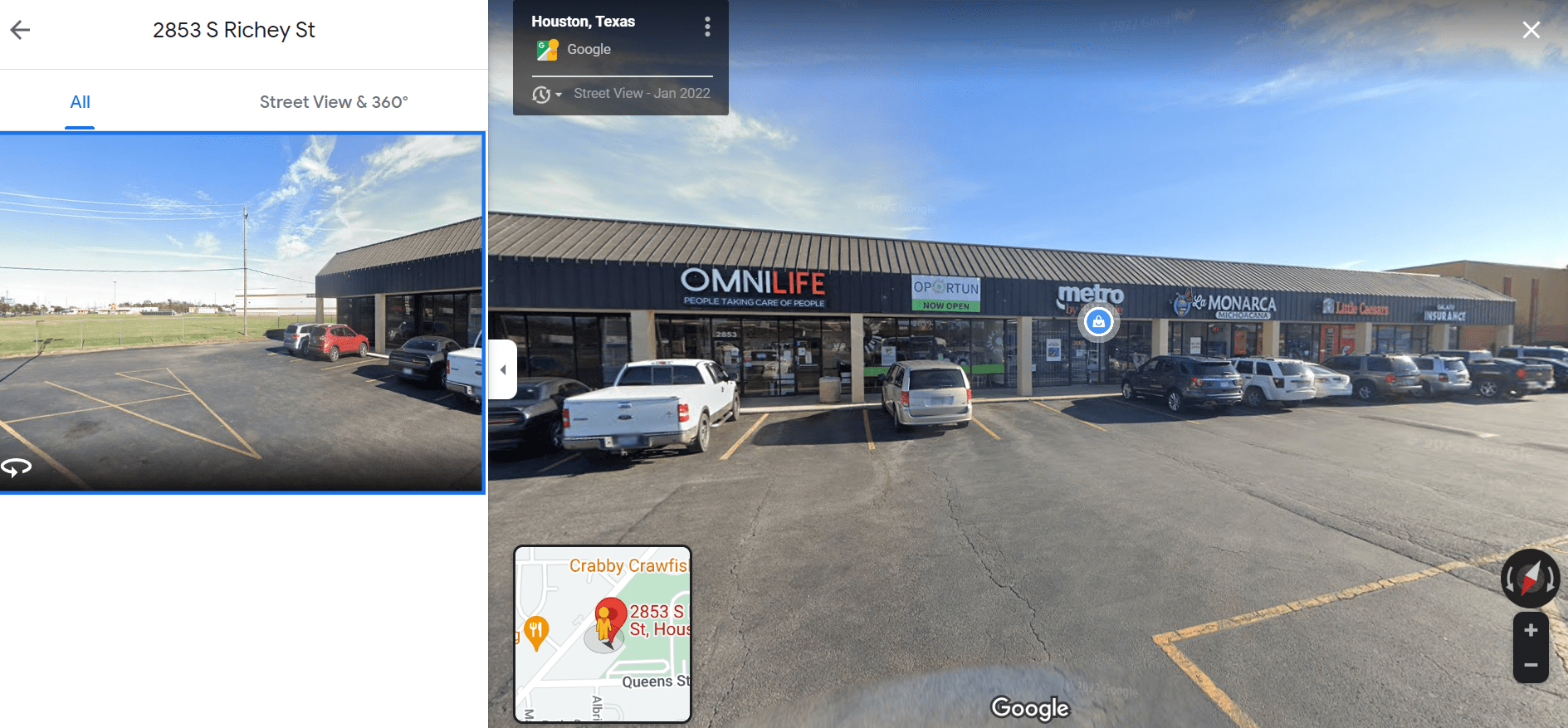

Digging a bit deeper, we found that one of these sold properties was actually an office building, one property was located in Chicago, and one is an old Houston strip center built in 1980:

Google maps

I think that it provides added evidence that the 6% cap rate is reasonable for WSR.

If you valued the whole portfolio at a 5.6% cap rate, WSR would be worth about ~$18 per share. It trades today at half of that.

Here is what the CEO commented on these asset sales:

“We believe the overall transaction cap rate on these property sales highlights the value of Whitestone’s portfolio of properties, which are located in some of the fastest growing and most desirable markets in the country. We anticipate using the proceeds for debt reduction and future accretive acquisitions with greater upside than the properties which were sold. We are pleased with the execution of these property sales which are consistent with our previously communicated 2022 property disposition goals and will allow us to advance our objectives to grow earnings and improve our debt metrics and equity market valuation,” said Whitestone REIT Chief Executive Officer Dave Holeman. [emphasis added]

He confirms that these assets have less upside potential than the reinvestment projects that they have in their portfolio, and so the theory that the cap rate is materially understated by below-market rents does not hold.

This will allow them to grow their funds from operations (“FFO”) per share by reinvesting the proceeds at a ~2x higher projected yields – all while deleveraging their balance sheet (via organic growth and debt paydown). They plan to be below 7x Debt/EBITDA within a year, and they are making great progress towards that.

Bottom Line

Even if you use a relatively conservative cap rate and NOI assumptions, Whitestone REIT’s portfolio is heavily discounted and the management is laser-focused on unlocking this value. Meanwhile, its rents keep growing at a rapid rate and the balance sheet keeps getting stronger.

Depending on the NAV estimate that you use, the company would have 50-100% upside potential to get there and this NAV keeps growing as well.

Perhaps the best part in all of this is that Whitestone REIT can create a lot of value internally without having to raise any additional equity. That makes it less dependent on the mood of the market, increasing its chances of outperforming other REITs in the future.

While you wait, you earn a 5% dividend yield that’s well-covered and set for rapid growth in the years ahead.

Be the first to comment