smshoot

Thesis

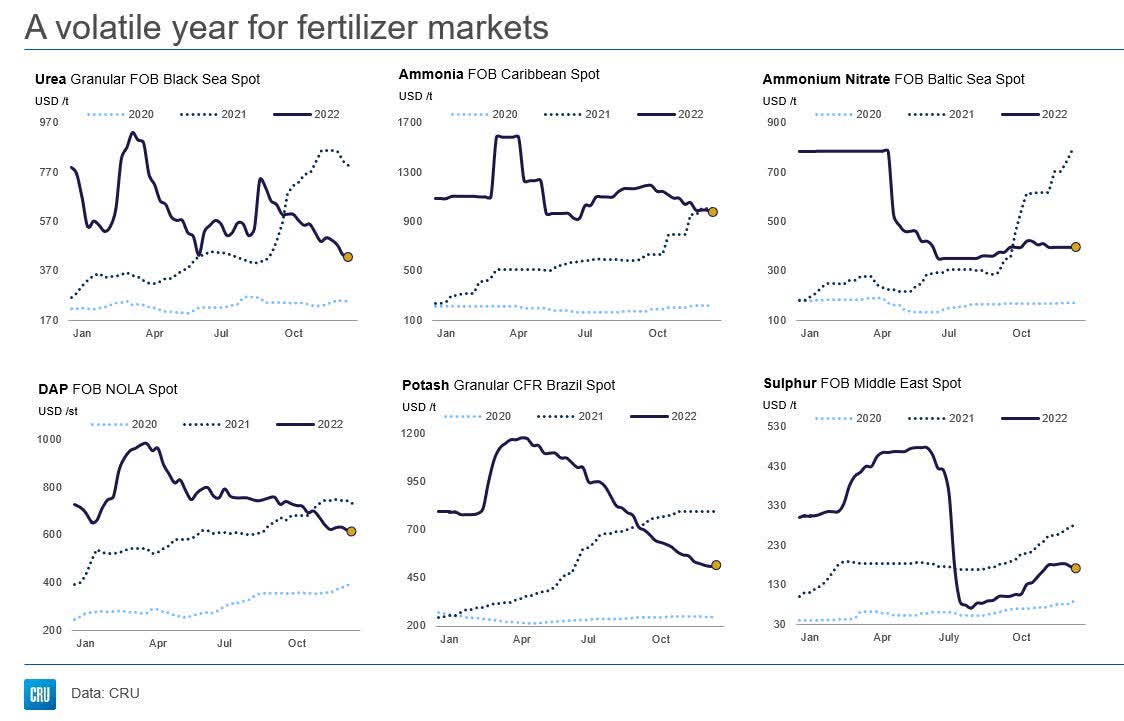

CF Industries (NYSE:CF) is one of the largest [> $16.2 billion market cap] U.S.-based fertilizer manufacturers [based in Deerfield, Illinois] that has rallied throughout 2022, but has recently come under heavy selling pressure due to cyclical fears and falling fertilizer prices:

Fertilizer Week, on Twitter: @FertilizerWeek1

Nevertheless, I have some reasons to believe that CF is oversold and that now is the best time to slowly buy back this dip.

Why Do I Think So?

If you have been following me for a while, you’ll remember my articles on CVR Partners (UAN). In the last of those articles – “CVR Partners Looks Like A Possible Double In 2023” – I went into more detail about why I believe the entire fertilizer manufacturing market has entered a new bull run due to years of underinvestment in the industry. The problems started long before the war in Ukraine – as shown in the charts above, where much more stable growth in fertilizers prices was seen in 2021. However, as soon as Russia ceased to be a reliable supplier of a) fertilizers and b) major crops, everyone started to worry about the first and second – the normalcy of life support is at stake, you know.

CF may be the only company of its size to take matters into its own hands quickly and supply fertilizer to Europe. The EU Council’s decision to temporarily suspend tariffs on urea and ammonia in Europe due to rising gas prices has led to the fact that there are so much of stocks in the Old World that local fertilizer producers are calling for the tariffs to be reinstated:

Between August and October of 2022 imports of urea rose by 247% compared to the same period in 2021. In August 2022 alone, imports rose by over 300 thousand tons. As Europe is already a net importer of fertilizers, policymakers must refrain from actions that will further strain the competitiveness of the domestic fertilizer industry.

Source: Fertilizers Europe

In fact, the problem cannot be said to be completely solved – CF will continue to supply a lot of fertilizer to Europe and benefit from the lack of capacity in the coming years [below an example with urea]:

Grain Farmers of Ontario [StoneX Financial Inc – FCM Division]![Grain Farmers of Ontario [StoneX Financial Inc – FCM Division]](https://static.seekingalpha.com/uploads/2023/1/5/49513514-16729141432658584_origin.png)

Given the cyclical nature of fertilizer demand, I have no doubt that fertilizer producers’ stock prices have managed to absorb all the negative effects of falling fertilizer prices in recent weeks and will rise again once seasonality changes.

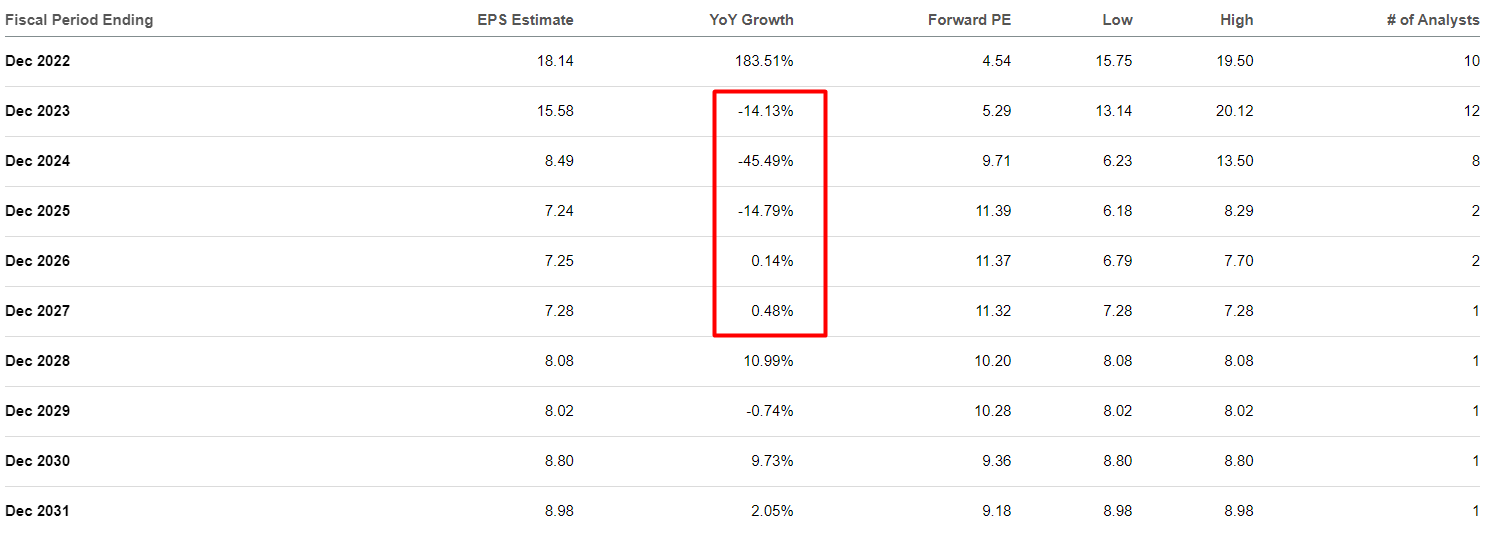

The second argument in favor of my thesis is the very low expectations for CF’s earnings over the coming years:

Seeking Alpha, CF’s Earnings Estimates, author’s notes

Let’s just do some basic DCF calculations.

I have roughly used Wall Street analysts’ revenue estimates [pulled from Seeking Alpha], assuming that EBITDA and EBIT margins will decline from 32.81% and 13.67% in 2023 to 29% and 11% in 2026, respectively.

A fairly low tax rate (I assume 15%) with borrowing costs of 6% and a market premium of 5% yields a WACC of 8.19% (beta close to 1).

Assuming a long-term, cycle-adjusted growth rate of 3% [Gordon’s g], we get a fair estimate of $91 per share, which is already 10.4% above yesterday’s closing price of $82.41.

The 14% decline in EPS in FY2023 leads us to a forwarding P/E of about 5.3x – but what happens if fertilizer prices eventually rise again and the estimates for the decline in sales and EPS no longer have any sense?

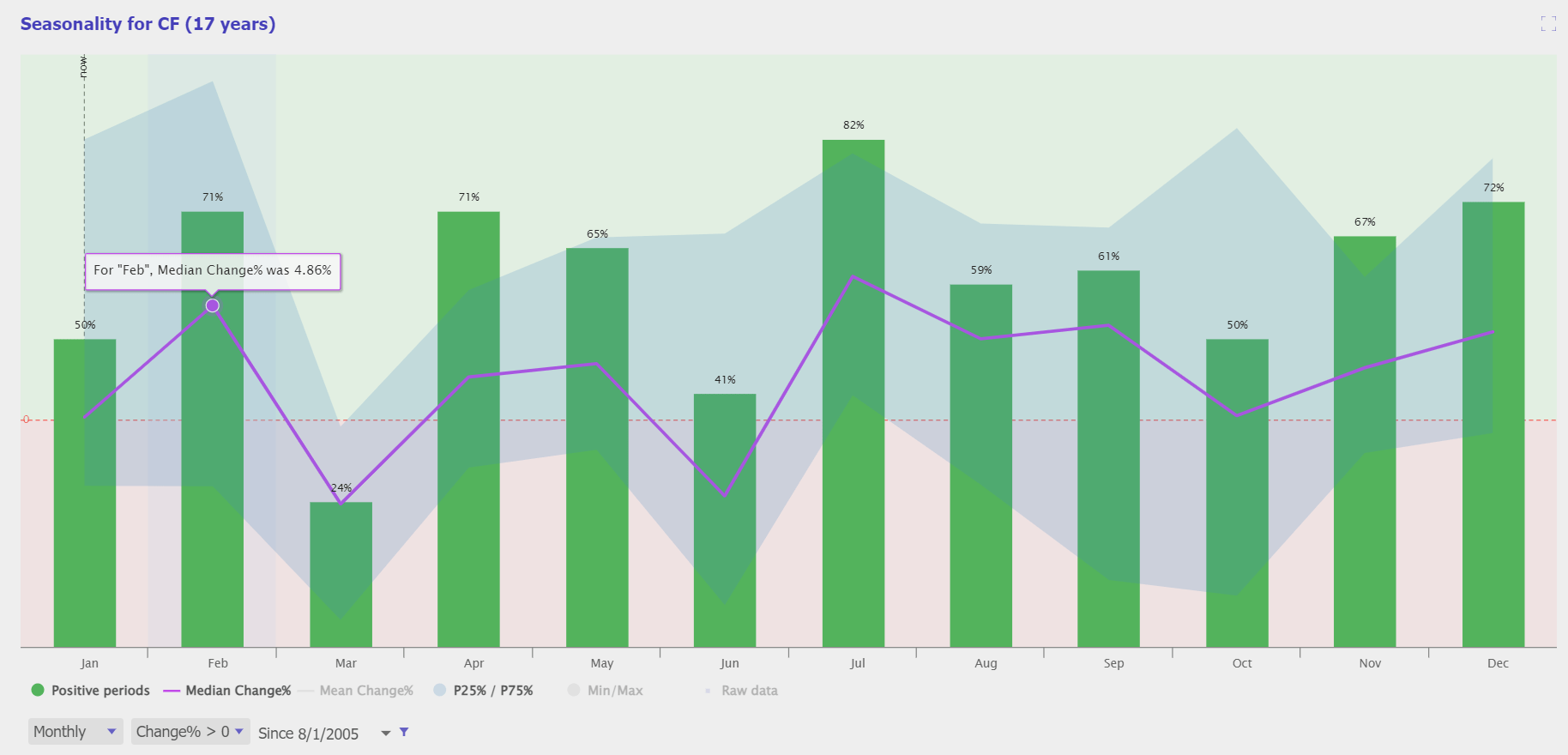

The third reason I expect CF prices to pick up in the short term is seasonality. Over the past 17 years, CF has risen 50% and 71% of the time in January and February, respectively. At the same time, median growth has been a modest 0.12% in January and 4.86% in February. If we experience a “regular year” in 2023, then CF should see a strong recovery in late January/early February.

TrendSpider, CF’s seasonality

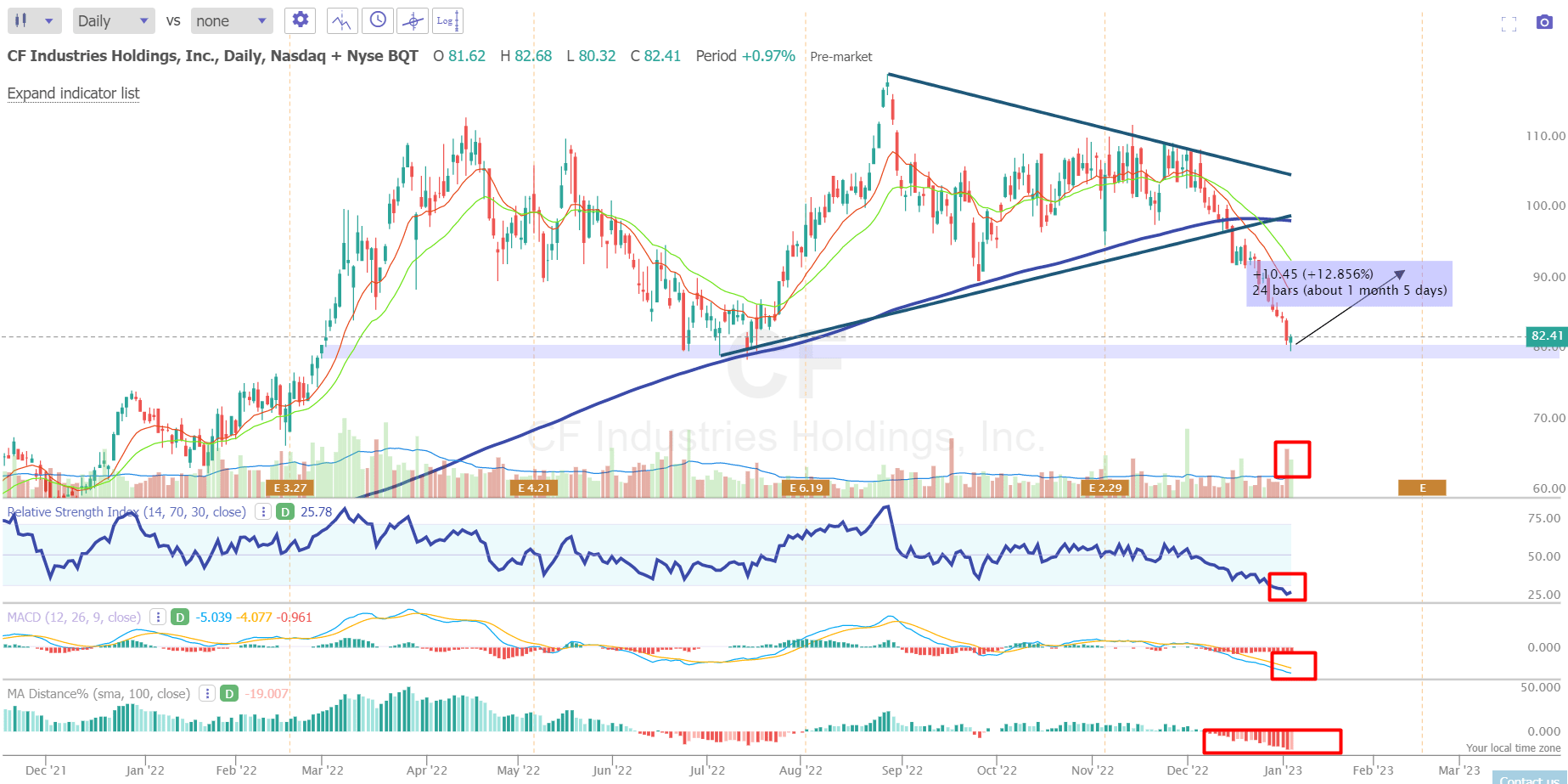

The fourth reason is the technical picture. We can clearly see how CF hit its local strong support line and started to recover slightly from it. In the last 2 months, the stock has managed to fall >20% below its 50-day moving average. On January 4, we saw anomalous buying volumes – the decline has stopped, and the MACD will apparently cross the signal line shortly if nothing bothers it.

TrendSpider, CF, author’s notes

In my opinion, the conditions are in place for a reversal move.

The Verdict

This article turned out to be quite succinct – I just described that I disagree with how the market prices CF stock. The whole picture now looks crazy when the stock is trading below its fair value under quite conservative assumptions.

Of course, I may be wrong in my conclusions. The obvious risk is that fertilizer prices in Europe and around the world will continue to fall as inventories rise. However, I do not dispute that the fall in prices will have a negative impact on CF and its peers. But in my opinion, this risk is fully reflected in the forecasts we now have.

I recommend considering CF as at least a speculative buy due to the current technical picture, which, combined with the fundamental analysis of the sector, represents an interesting opportunity for investors and speculators.

Thanks for reading!

Be the first to comment