Michael Vi/iStock Editorial via Getty Images

Investment Thesis

Rambus Inc. (NASDAQ:RMBS) is cheaper than its fair value, leading me to rate the stock as a Buy. Rambus continues to expand its DDR5 portfolio with decades of memory subsystem design experience; their experience will lead them to innovate better and faster server performance, eventually feeding their patent portfolio over its customers. I firmly believe that there will be increased demands for DDR5 memory, especially in the data center market and in the consumer market (sooner or later, it’s inevitable that everybody will upgrade and switch to DDR5 because of its bandwidth difference compared to its predecessor, DDR4 memory). The fair value of RMBS stock is $34.41, which is cheaper than today’s stock price of $28 (more or less).

Brief Overview Of The Business

Rambus provides semiconductor products in the United States, Taiwan, South Korea, and many international companies. They offer DDR memory interface chips, including DDR5, DDR4, and DDR3 interface chips to manufacturers and OEMs, silicon IP comprising interface and security IP solutions that makes data faster and safer by improving bandwidth, capacity, and security from cloud to the consumer.

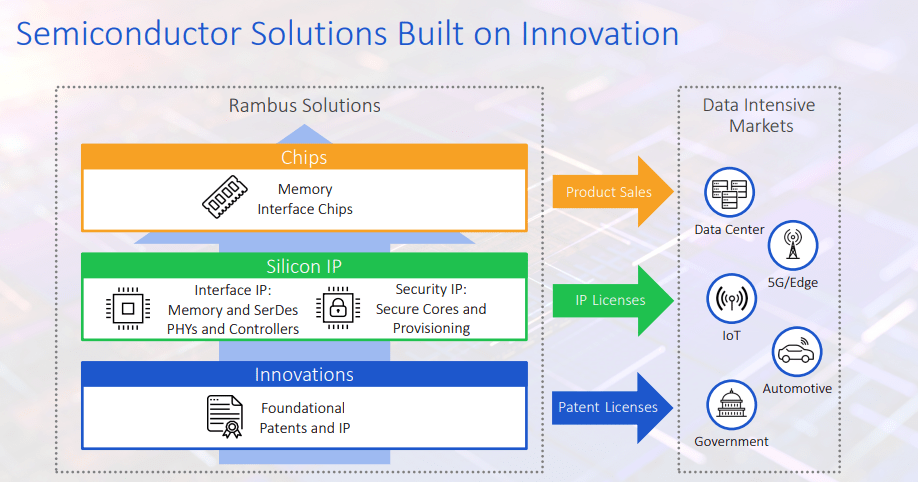

Source – Q32022 RMBS Investor Presentation

Rambus has two leading solutions: Memory Interface Chips and Silicon IP solutions. As the world is shifting to the cloud and with the widespread adaptation of artificial intelligence or AI across the data center and Internet of Things, or IoT, endpoints will significantly increase data usage and more need for data solutions. Here are the solutions that RMBS offers:

Memory Interface Chips

Rambus makes reliable high, speed and power-efficient DDR memory used in memory interface modules for server modules. Rambus’s portfolio includes DDR3, DDR4, and DDR5 memory interface chips, enabling increased bandwidth and expanded capacity in enterprise and cloud servers. They also sell memory interface chips directly and indirectly to memory module manufacturers and OEMs worldwide.

Silicon IP

Rambus provides security IP solutions that move and protect data in advanced applications. These solutions are critical to the high-performance data center, networking, machine learning, AI, and automotive applications since their solutions enable and optimize the transfer of data between chips and electronics. With a growing threat environment, hardware-based, embedded security solutions are mission-critical for protecting data centers and other advanced applications.

Completed Acquisition

It’s worth mentioning that in the company’s second quarter in FY2022, they completed the acquisition of Hardent, Inc., which can help the company improve the current electronic design of its hardware. In May 2022, the company acquired Hardent for a total consideration of approximately $16.1 million. I think adding Hardent will improve the current compute express link or CXL memory designs that Rambus currently has. Their engineers can help enhance bandwidth, transfer rate, and even more power-efficient memory modules, creating noticeable differences in memory speed in data centers.

The DDR5 Market

I wanted to dive more into the DDR5 market in today’s thesis. DDR5 is much faster compared to today’s DDR4 memory in many ways. Since RMBS plans to expand its memory portfolio in DDR5 even further, I wanted to dive deep into the performance and assumptions (my assumptions on demand, specifically in the data center and consumer markets). We will compare the DDR5 memory to DDR4, and I will tell you why I think the DDR5 is a significant growth opportunity for Rambus.

Source – Q32022 RMBS Investor Presentation

RMBS will play a significant role, especially in their different solutions that help the 5G/Edge innovation and further increase performance in Data Centers and IoTs. Still, I wanted to talk about DDR5 even more as data centers rely on memory for faster server performance and how DDR5 can affect the consumer industry through its partners in the PC market.

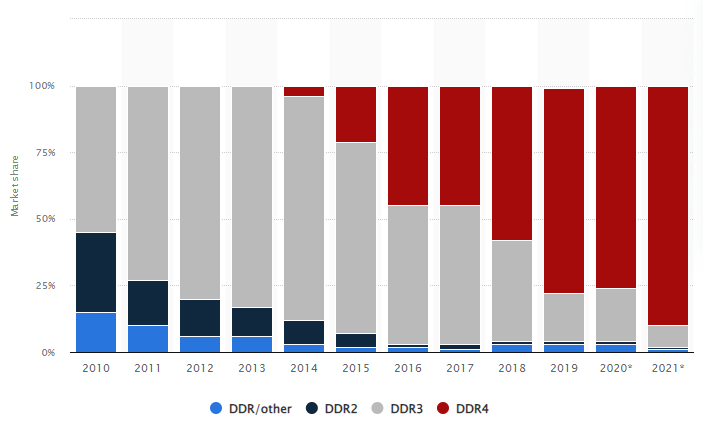

Source – DRAM Market Share Statista

Data Rate – MT/s

The data rate is how many bits a module can transfer in a given time. The larger the data transferred per second, the faster. DDR4 memory offers a 1.6 to 3.2 Gbps data rate, which is what most of the high-end PC market uses today and is expected to account for 90 percent of DRAM market revenues in 2021. Compare that to DDR5 memory, which offers a 4.8 to 8.4 Gbps data rate. Initial DDR5 delivers a 50% bandwidth increase and will scale up to 8.4 Gbps, significantly increasing data rate speeds.

Voltage – V

Since DDR5 memory has a faster data rate than DDR4 memory, this results in lesser power, from 1.2V in DDR4 to 1.1V in DDR5. According to Rambus, the reason for a lower data buffer voltage is because the Command/Address (CA) signaling is changed from SSTL to PODL, which has the advantage of burning no static power when the pins are parked in the high state. This makes the DDR5 memory power-efficient and provides more value, performance-to-voltage wise.

DDR5’s better power architecture is also what makes lower power consumption possible. DDR5 dual in-line memory modules or DIMMs will have a 12V power management IC or PMIC allowing better granularity of system power loading. The PMIC will then distribute 1.1V VDD (the supply voltage pin connected to the drain of the transistors), helping with signal integrity and noise with better on-DIMM control of the power supply.

Availability

Now that we know that DDR5 is faster and better than DDR4, we should talk about its availability. DDR5 was released in October 2020, so it has been available for two years for data centers and servers. Enterprises that want to improve cloud server performance can upgrade to DDR5 memory as this can improve the server performance, proven by the high MT/s rate that the DDR5 offers. However, I don’t think DDR5 is readily available compared to the PC market. First, we need to consider that most of the market is using DDR4, which means that most motherboards do not support DDR5 technology or capabilities for DDR5 random access memory or RAM. The latest CPU chips that support DDR5 memory are the latest 12th gen CPUs that Intel (INTC) offers. Not everybody has access to 1) a Motherboard that supports DDR5 or 2) A processor that supports DDR5. Although it is available, the PC industry is still limited to the latest releases, and we can’t make proper benchmarks unless there are a lot of DDR5-supporting MOBOs (motherboards).

My Assumptions For 2022 & Onwards

While it is true that DDR5 is available, I don’t expect growth in the PC market since there are still limited DDR5-supported products that can utilize DDR5 memory to its full potential. Limited supported products will also make it hard for consumers in the PC market to determine the price-to-performance ratios of this memory. However, I do think that Rambus is going to expect growth in the Data Center market. Think about it, the initial increase of the DDR5’s bandwidth increases by 50% and is scalable from 4.8 Gbps to an 8.4 Gbps data rate which will tremendously increase server performance and run at a lower voltage which makes DDR5 power efficient.

Financial Analysis

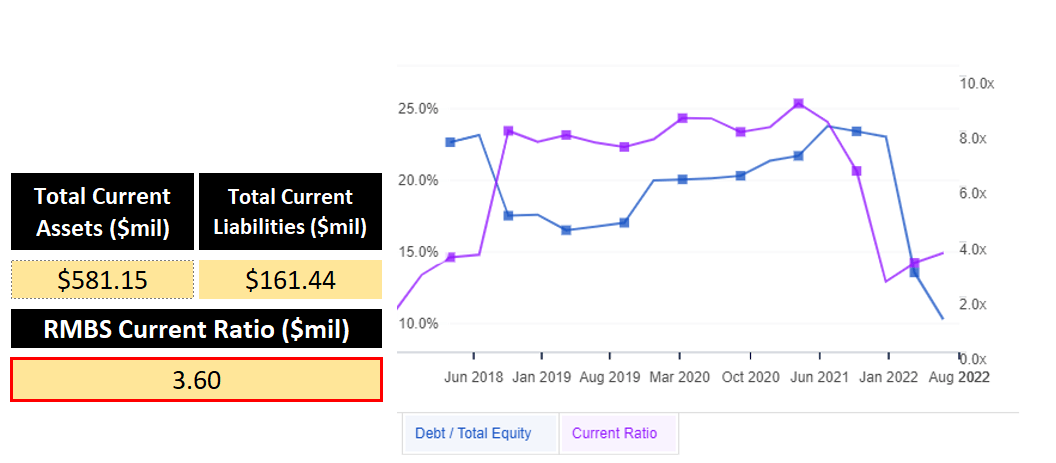

Author – Data From RMBS Financial Statements; Graph From Finbox

Rambus reported $171 million in cash in its second-quarter results, a -0.20% decline compared to its Q1’22 results but a 59% year-over-year increase. For short-term liquidity, the company has $581 million in current assets and $161 in current liabilities, which gives us a current ratio of 3.6. The company had $86.34 million in total debt, and if we divide that by the company’s total equity of $838 million, we get a 0.1 debt to equity ratio.

Valuation

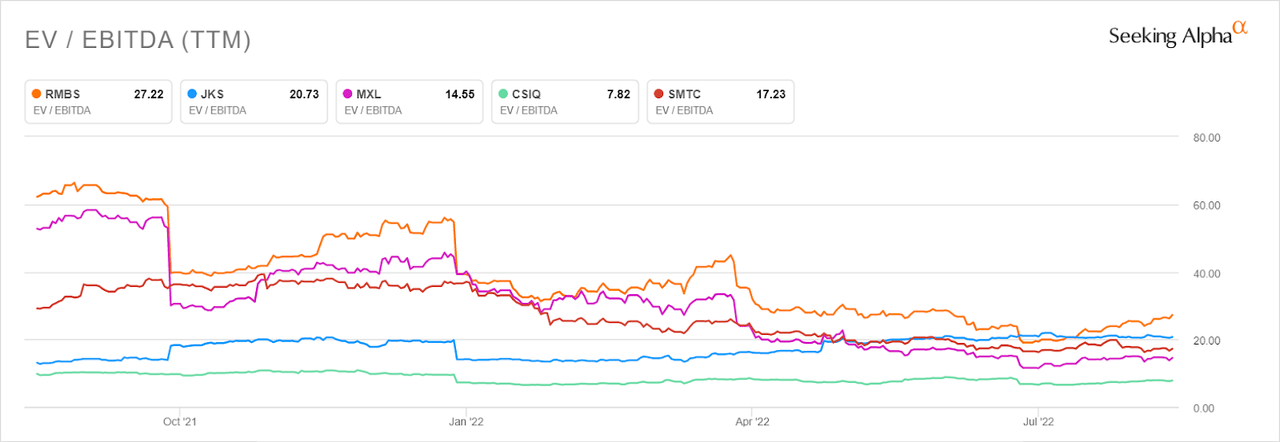

Source – Seeking Alpha EV/EBITDA

To start with my valuation, Rambus has been trading at a higher EV/EBITDA multiple compared to its peers. Although RMBS usually trades at a higher price than its peers, any significant increase would mean it’s potentially overvalued. The company should be trading around the average of its peers, more or less at an EV/EBITDA multiple of 17. However, the EV/EBITDA multiple is justified by how much cash the company generates. I just wanted to point this out because it’s usually not good that the company trades higher than its peers without justifiable reason. For example, if the multiple increases about, let’s say, 20x, then we should pay attention to what the company is undergoing or how the financial statement looks like.

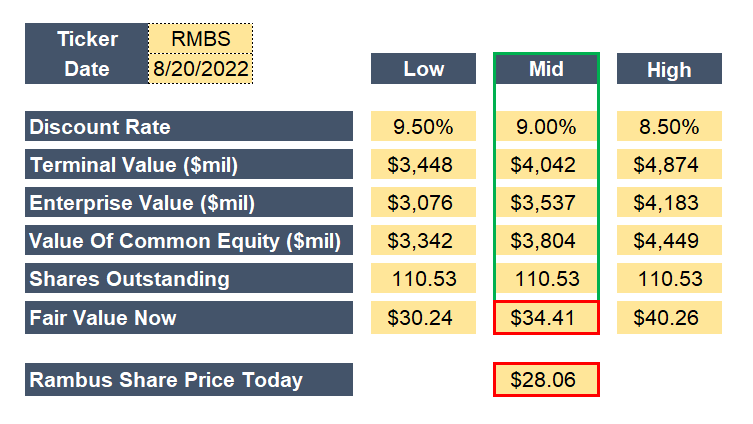

Source – Author With Data From RMBS Financial Statements

I created a 5Y DCF model mixed with the Street’s and my assumptions. I included the essentials of my valuation in the picture above. Starting with revenue, I projected that the company would have over 65-70% revenue growth because of data center demands. The company has been growing its revenue for the past fiscal quarter and going in on with 2022. The projection seems realistic and attainable.

The company’s EBITDA margin has recovered since 2019, and from there on, the projections are around 50% EBITDA margin. There are no significant changes with CapEx around 4.7% in the first three years and 3.9% onwards. The company also included in its Q2’22 results earnings call transcript that the tax rate would be 24% – higher than the statutory tax rate of 21% due to foreign jurisdictions. For the discount rate, I calculated the WACC of the company and ended up with a low discount rate of 8.5% and a high discount rate of 9.5%. I chose the median and ended up using a 9% discount rate. With the unlevered cash flow and a growth perpetuity range of 2.5% to 3.5% (I chose the median, which is 3%), we have a terminal value of $3.4 billion for the low estimate and $4.9 billion as a high estimate. I still chose the medians, so we’d have a $4 billion terminal value. By adding the current discrete cash flow with the discount rate and the PV of TV, we get an enterprise value of $3.5 billion for our mid-case.

After getting the EV, we would now add back cash, investments, and deduct debt from the Enterprise Value to get the value of common equity. We then divide the value of common equity with the shares outstanding to get our fair value of $34.41 today. Paired with my DDR5 growth analysis and the other growth opportunities that RMBS has, it’s fair to say that this is a reasonable implied share price. If we compare $34.41 with today’s share value, then I’d say that the stock is cheap, leading me to rate it as a Buy.

Risk

The only and most crucial risk I’m seeing right now is a decline in growth in their data center markets. The company relies heavily on its data center solutions and royalties from memory interface chips. If they want a future in DDR5 growth, they’d also want their customers to buy their products. A decline in demand will significantly affect the company and would have to rely solely on royalties and patents, which isn’t sustainable for the company.

Investor Takeaway

Rambus is currently in a strong market position, proven by its 30 years of experience in memory interface chips and several leading partners to innovate faster memory for servers and consumers. Although I am not sure how soon, people will eventually start adapting to DDR5 memory sooner or later since the performance difference between DDR4 and DDR5 memory is significant and would provide better enterprise servers and faster processing with PC product applications. I’ll be curious to follow the company’s next move and if the company will be exploring its other growth opportunities. Overall, the company doesn’t have short-term liquidity problems, and my valuation proves that it is trading cheaper than its fair value, and that’s why I rate the stock as a Buy.

Thank you so much for reading, I hope you have a great day.

Be the first to comment