PepsiCo, Inc. (PEP) remains a formidable figure in the food and beverage industry with its growth for the last 10 years. The consistency of sales and net income with some financial ratios is a testament to its long-lasting profitability and sustainability. Moreover, it remains an interesting company to the investors as dividends keep increasing while ensuring that its financial capacity remains adequate. Also, the stock price is still inexpensive amidst the volatility since the latter part of February 2020.

Dividends Per Share, Earnings Per Share, and Free Cash Flow

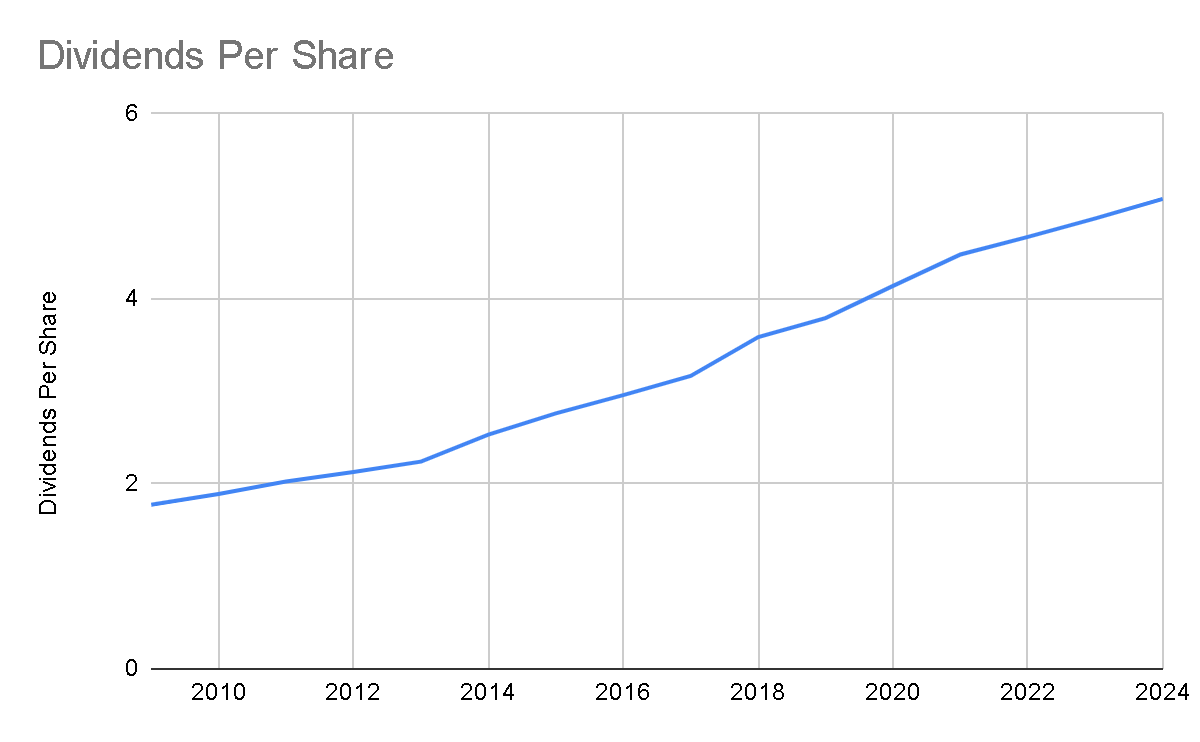

For the last 10 years, long-term investors have observed consistent growth in dividend payments. With an average annual growth of 7.92%, it is without question that PEP has been making substantial changes in dividends. There were years when the company made notable increases. From 2013 to 2014, the dividends per share grew by 13.1% as it moved from $2.24 to $2.76. It made another huge leap by 13.2% when it moved $3.17 in 2016 to $$3.59 in 2018. One can easily trace how the dividends per share doubled from 2009 to 2019. Higher amounts for the succeeding years may be anticipated given the solid financials of the company. The Dividend Growth Model supports the idea as the value is estimated to climb to $4.14 in 2020 to $5.08 in 2024.

{kind=link}

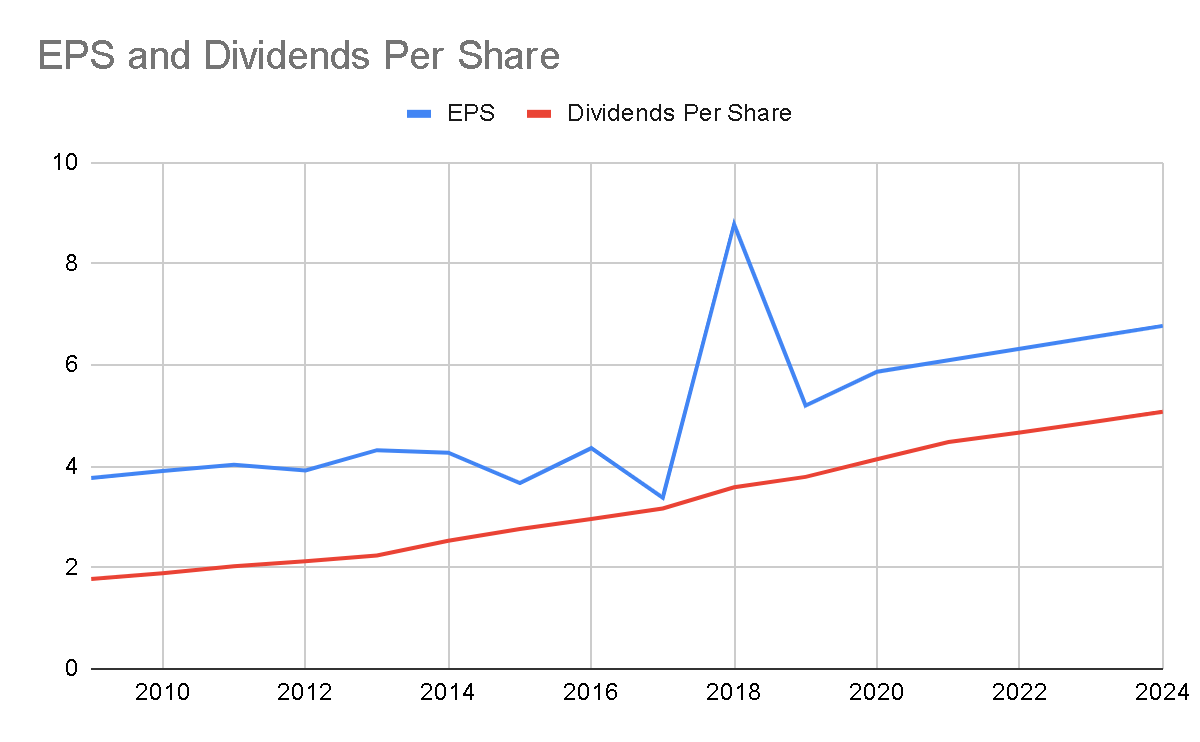

On the other hand, one must determine how, how much, and how long the company can suffice dividend payments. In PEP’s case, it can be seen that from sales down to net earnings, the values have been moving in a generally increasing trend. Throughout the years, the company has maintained adequate earnings to sustain dividend payments. Even if the earnings fell by 23% in 2017, it remained higher than dividends. In 2018, the company ended up with a higher capacity for dividend payments as EPS grew by 160%. This was primarily driven by a tax refund. Also, having an average annual Dividend Payout Ratio of 0.60, it can be seen that dividend payment comprises 60% of PEP’s earnings while the remaining 40% may be used to continue financing or even expanding the operations and/or be retained for investments and other financial obligations. Using the Linear Trend Analysis, it can be expected that the company’s earnings will remain solid from $5.86 in 2020 to $6.77 in 2024. Nasdaq affirms this estimation as the consensus EPS forecast for 2020, 2021, and 2022 are $5.89, $6.31, and $6.77, respectively.

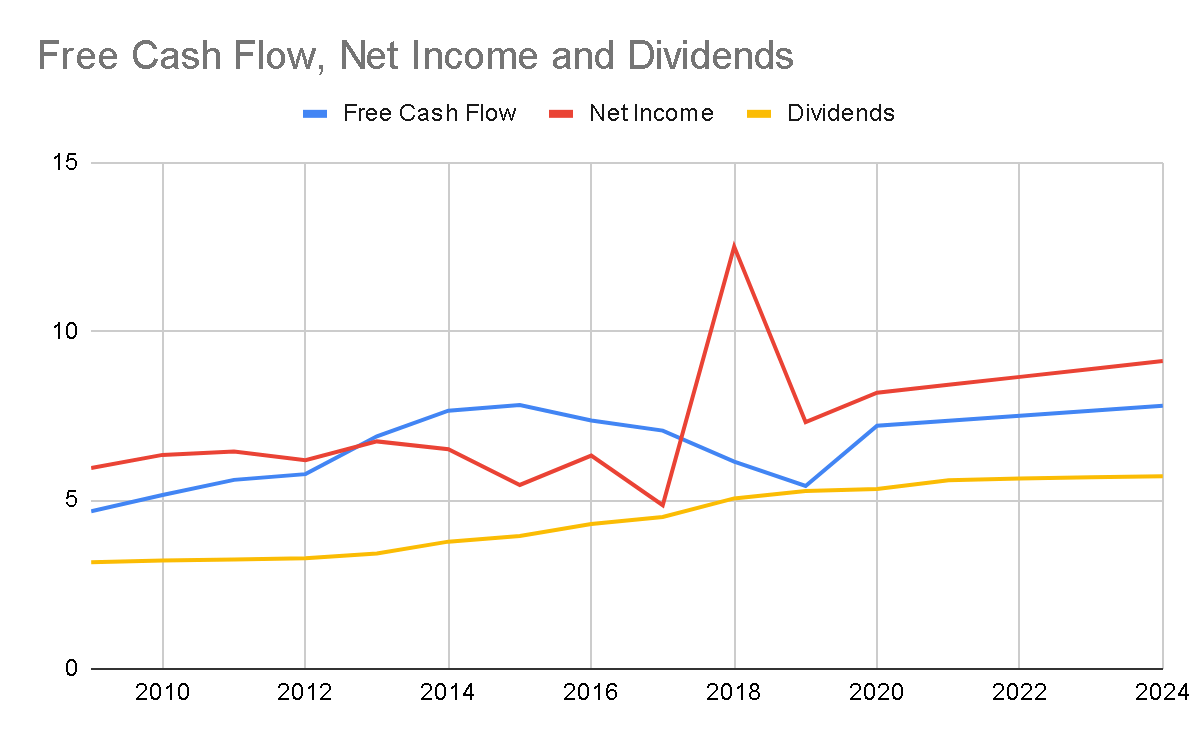

One may also refer to Free Cash Flow (FCF), which is always obtained by deducting capital expenditures (MUTF:CAPEX) or the amount spent on the acquisition of properties and equipment from the net cash gain or loss from all the company’s operating activities. From 2009 to 2019, PepsiCo’s FCF has always been large to cover consistent dividend growth. Relative to the average annual dividends of $3.92 billion, the average value of FCF remained high at $6.32 billion. Moreover, FCF has a similar trend with Net Income except in 2018 due to tax refund amounting to $3.37 billion. This shows the consistency with the company’s profitability and its cash flow from its acquisition, disposal and repayment of operating assets and liabilities which also implies the consistency of PEP’s profitability with its capacity to meet its financial obligations. This is also an assurance that even if the company decides to acquire more fixed assets to further strengthen its operations, it will still have enough for the creditors and investors. For the next five years, FCF may be even higher at $7.20 billion in 2020 and further increase to $7.79 billion in 2024.

Operating Revenue, Operating Costs, and Operating Expenses

PepsiCo remains one of the most formidable companies in the food and beverage industry. As posted on Food Engineering, PepsiCo comes after Nestle in terms of market value since 2015. Moreover, the fact it is one of Fortune 500, an investor can easily understand that PEP is a durable company that generates billions of sales through its large operating capacity over the past decade.

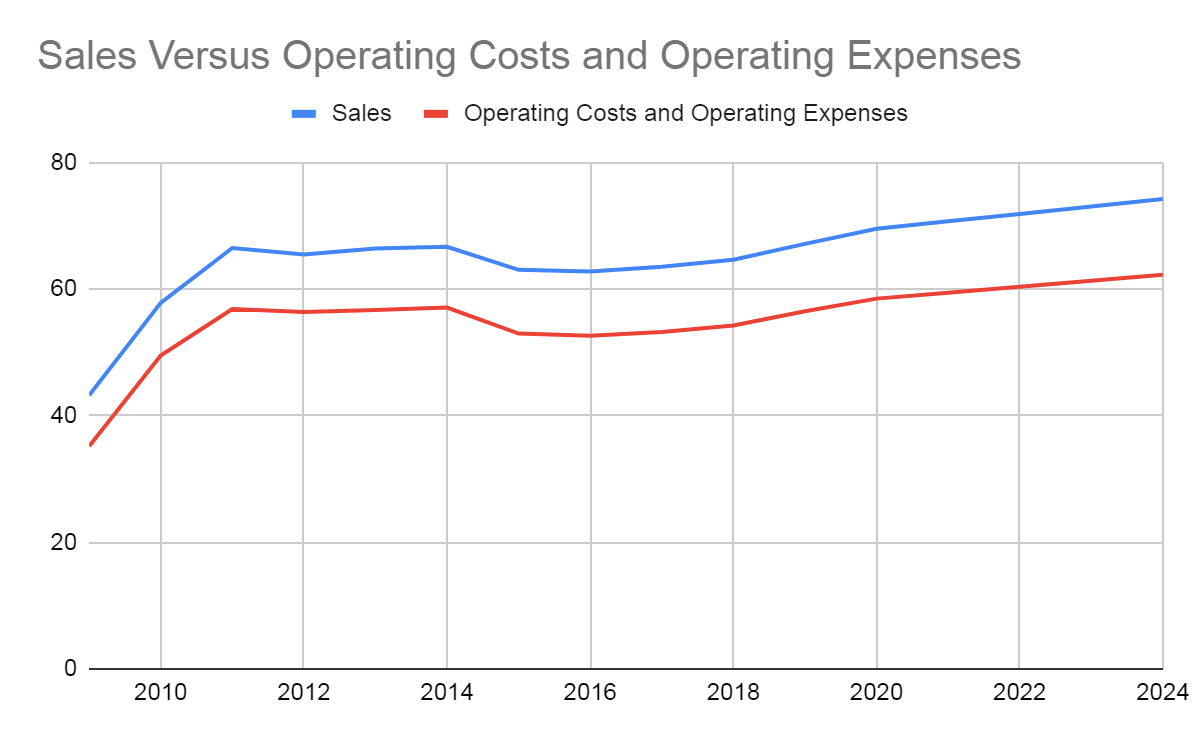

This also shows PEP’s strong market power. Since the company has been combining it with a good pricing strategy, revenue growth has been sustained for the last 10 years. There were years when revenue fell a bit, but the company maintained it above $60 billion since 2011. This also proves the durability of the company’s operations. Having an average annual revenue growth of 5%, one can easily observe how it changed by $24 billion in just 10 years as it sharply increased from $43 billion in 2009 to $67 billion in 2019. This may be maintained and raised as it is estimated to range from $69 billion to $74 billion for the next five years.

Likewise, COGS and SG&A have been moving along with sales. The company is at its best as it continues to exude productivity and efficiency to come up with a higher operating profit. It also has an average annual growth of 5% for the last 10 years although the change in revenue has been a bit larger. Moreover, it has always been kept below $60 billion, which also shows their substantial gap. This can be proven by Operating Profit. From 2009 to 2019, Operating profit slowly moved from $8 billion to $10 billion. This impressive trend may continue for the next five years as the Linear Trend projected operating profit to increase to $11 billion to $12 billion.

Net Income

Since there have been no significant changes in non-operating income and expenses, pretax income has been moving with a similarly increasing pattern with sales over the past decade. Taxes paid have not been changing significantly except in 2016-2018 when it increased from $2.17 billion to $4.69 billion and became a refund/income of $3.37 billion. This resulted in a sudden increase and decrease of net income from $4.86 billion to $12.52 billion to $7.31 billion. Nevertheless, what should matter here is the fact that net income has been generally increasing, and without the sudden changes in tax, it would be in a consistently upward pattern. Moreover, net income has been maintained at about $5 billion and above. This not only shows the profitability of the company but also the capacity to suffice the dividend payments and even expand its operations. This trend may continue for the next five years as it is estimated to increase to $8 billion to $9 billion.

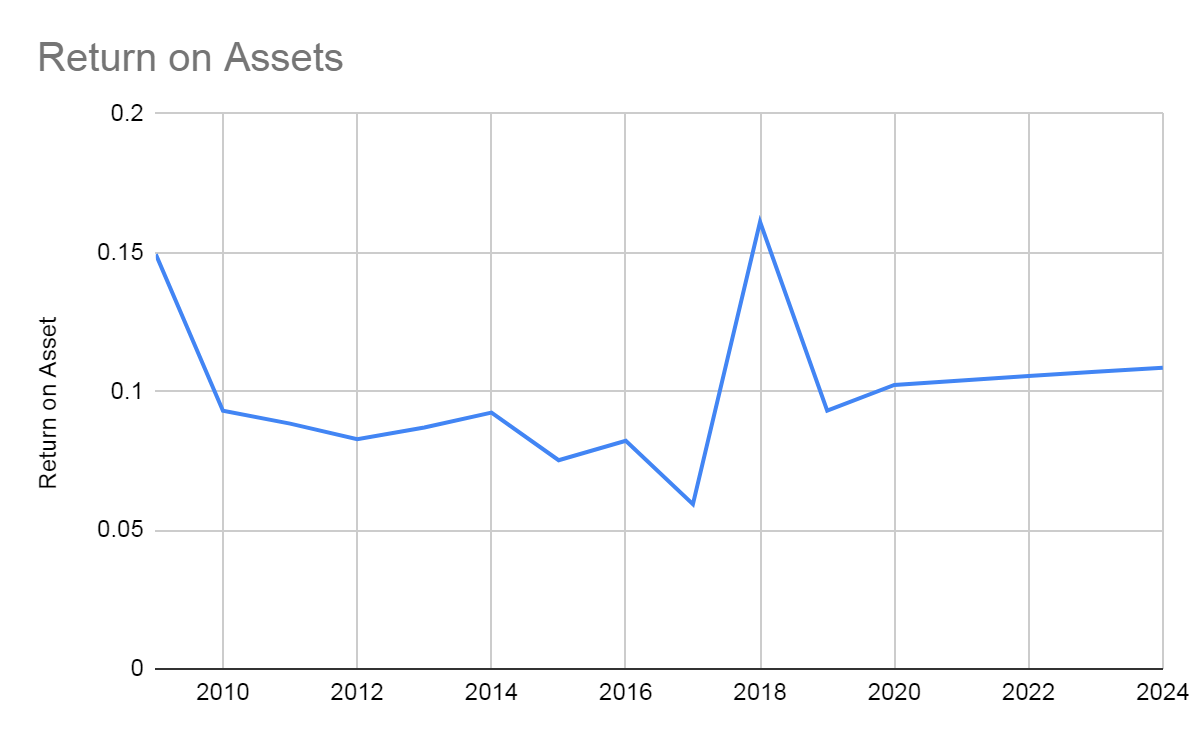

Return on Assets

For the last 10 years, PepsiCo has been showing the generated profit from every asset it has purchased. Although it may not be that massive relatively, the value is substantial. Having an average Return on Assets of 0.097, PEP has been realizing a value or profit of 9.7% for every asset it purchased. In dollars, the company generated about $7 billion from its $71 billion assets. This shows that it has enough capacity to turn its assets into earnings and even use and replenish them for a long time. For the next five years, it is estimated for PepsiCo’s ROA to rise to 11%.

Stock Price

The stock price of PEP has been noticeably volatile but generally decreasing since the latter part of February this year. Being a well-established company in the industry, it is not at all surprising that PEP has an expensive stock price at $137.26 recently closed last March 6. Also, the PE Ratio is quite high at 26.40 which will require every investor to spend $26.40 for every earnings they may get here. But as we compare it with the company’s financial status and dividend payments, the stock seems inexpensive. Using the Dividend Growth Model, we will assess if the stock price is still recommendable.

- Current Stock Price: $137.26

- Average Dividend Growth: 0.07924473656

- Proposed Dividend: $4.14

- Cost of Capital Equity: 0.1094064734

- Derived Price: $148.1371325

With the derived amount, as well as the decreasing trend for the last two to three weeks, we can infer that the stock is still inexpensive and worth the risk.

Growth Catalysts

Pepsi Zero Sugar (Betting PepsiCo’s Zero Sugar)

PepsiCo has high hopes for Pepsi Zero Sugar as it is named as one of the fastest-growing brands of soda in the US last year. PEP will launch a new logo and a more appealing bottle design this year. This is a Pepsi Hero as it is one of the top contributors to Pepsi’s growth these past few years. With its continuous growth and improvement, the company may expect higher sales and earnings this year. This may also partnerships and even investments which may help the company further improve its well-established products and even discover new ones which may result in higher returns in the long-run.

PepsiCo in China (PepsiCo Acquired Be&Cheery)

Although Pepsico has already established its formidable reputation in the industry and even in NYSE, it still seeks to further improve and expand or at least maintain its impressive status. With its entry in East Asia, it may face a lot of competitors there but it will certainly capture a significant portion of demand in the region given the combined market power of PepsiCo and Be&Cheery. Also, it may introduce Be&Cheery’s products to the US and even in Europe which may result in higher returns. This may also entice more investments so the company can expand its operations and even find more interesting and smaller companies that may fit its quality products. However, PepsiCo must also understand the risk it took. Since COVID-19 is still spreading which is most prolific in East Asia, this may discourage consumers from purchasing the products which may decrease future earnings. This does not intend to deliver a biased prejudice against the Asians but the panic caused by COVID-19 in the region may affect even the financial health of the company which usually starts from its products, services, and investments.

The Potential Earnings and Risks in PepsiCo

Short-term Investors: It is really interesting for many short-term investors, especially those who venture in buying and selling of stocks for a very short period, to see the volatility in PEP. While it may result in instant high earnings, the price may also suddenly drop. The stock price is usually difficult to predict. Also, the PE ratio is a bit high at 26.40 and one must spend $137.26 for every stock. Nevertheless, if a potential investor wants to take risks here, he must hold on to the possible impact of the company’s impressive financials and fast-growing dividends which may give a significant impact on the price of the stock. Lastly, it turns out to be inexpensive and undervalued as estimated using the Dividend Discount Model.

Long-term Investors: We can no longer question the durability as it has already built its strong reputation in the market. The consistency in its financials, as well as the sustained growth in the dividends, is enough to assure every long-term investor that long-term earnings here is certain.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment