Khosrork

Pure Cycle Corporation (NASDAQ:PCYO) recently announced significant capacity expansion from now to 2024-2025, expansion Of Sky Ranch, and incoming revenue from Ironton in 2023. In my opinion, future free cash flow would imply a valuation of close to $13 per share. I obviously see risks from steel price increases or labor costs increases, however PCYO appears undervalued at its current fair price.

Business Model

Incorporated In Colorado, Pure Cycle runs a diversified water resource and land development business model. In other words, management presents its business as a wholesale water and wastewater service provider along with business interests in the development of single-family homes.

Our newest business is the development of single-family homes held for rental purposes. Both the land development and single-family home rental lines of business generate customers and usage fees for our water and wastewater resource development business. 10-K

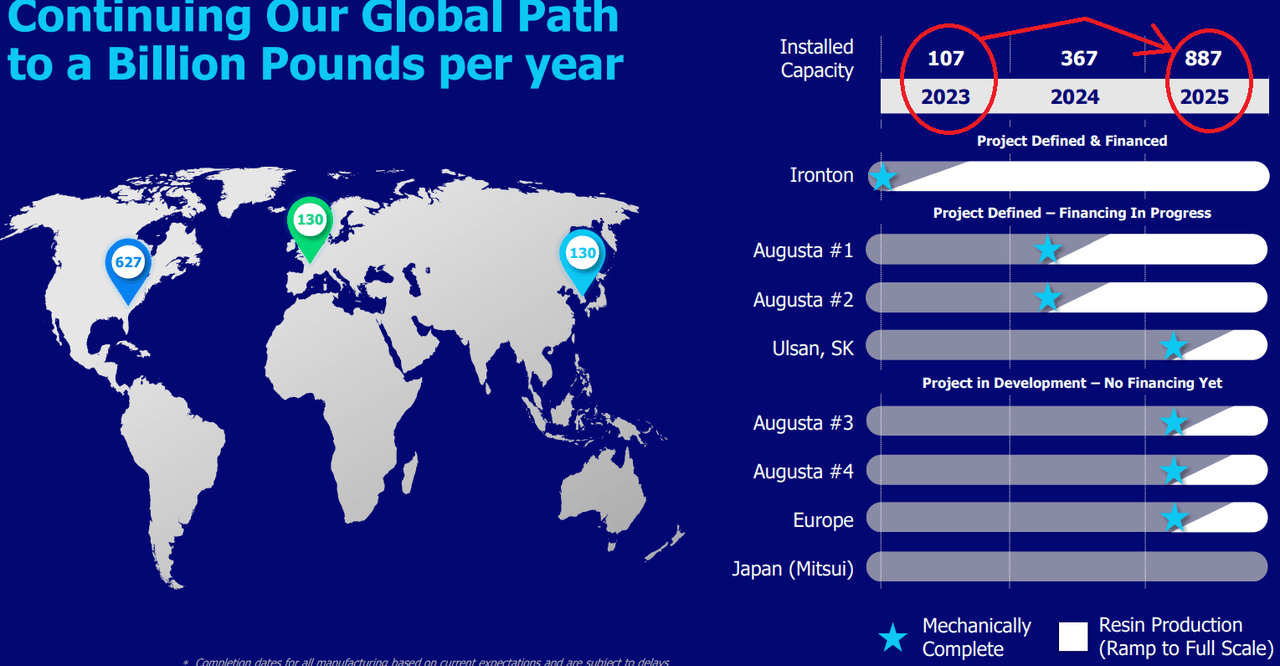

I usually don’t pay much attention to the real estate industry or home builders. With that, there are several aspects that drew my attention to recent Pure Cycle’s corporate documents. First, the company promised to multiply its installed capacity by more than 7 times. Let’s keep in mind that Pure Cycle reported that projects Augusta 1, Augusta 2, and Ulsan include financing in progress.

Investor Relations

Besides, management is quite optimistic about housing in the Denver market, which is expected to enhance the company’s business model and revenue from Sky Ranch, the company’s largest asset. Among the words from management in the last quarterly report, in my view, investors should have a look at the following lines.

Despite this, we believe several long-term land development and housing market fundamental factors remain positive. For example, available lots and housing supply-demand remain imbalanced due to a decade-plus of underproduction of new homes in relation to population growth, and low resale home inventory.

We believe our reasonably priced lots and the low inventory of entry level housing in the Denver market will help Sky Ranch. Source: 10-Q

Pure Cycle Sales & FCF

I could not find a lot of expectations from other financial analysts. With that, I believe that the company’s financial stats in the future will likely not be far from those in 2022.

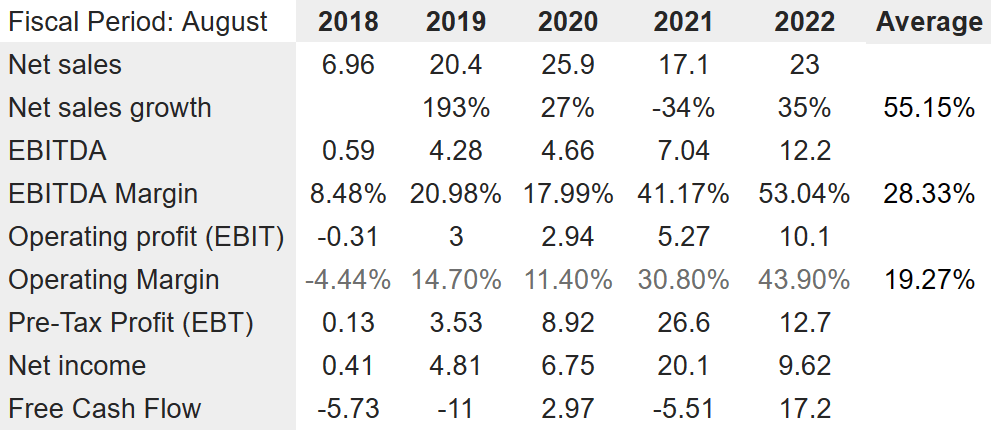

2022 net sales were equal to $23 million together with net sales growth of 35% and 2022 EBITDA of $12.2 million accompanied by 2022 EBITDA margin of 53.04%. In addition to 2022 operating profit of $10.1 million and operating margin of 43.90%, pre-tax profit was $12.7 million with net income of $9.62 million. Finally, free cash flow would stand at $17.2 million. Average figures included net sales growth close to 54%, an EBITDA margin of 28%, and operating margin of 19%. I used some of these financial figures in my DCF models.

MarketScreener

Balance Sheet

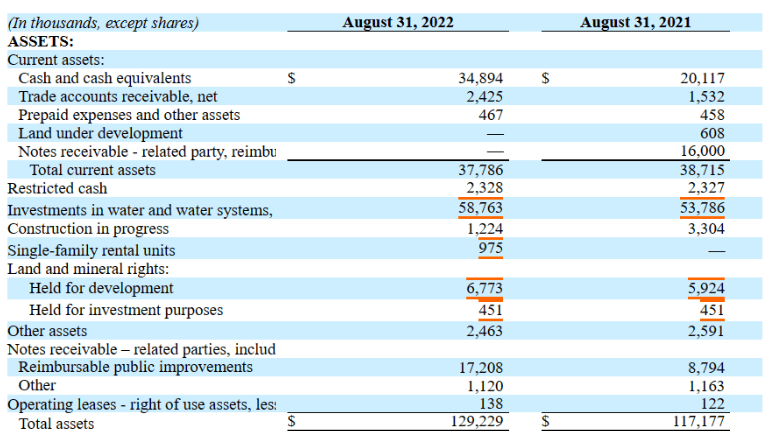

The balance sheet, in August 2022, included cash of $34.894 million together with a trade accounts receivable of $2.425 million. Total current assets stood at $37.786 million, more than three times the total amount of current liabilities. I don’t really see a liquidity risk here.

Investments in water systems stood at $58.763 million with land held for development worth $6.773 million. Other assets stood at $2.463 million. In addition, reimbursable public improvements were worth $17.208 million with total assets of $129.22 million.

10-K

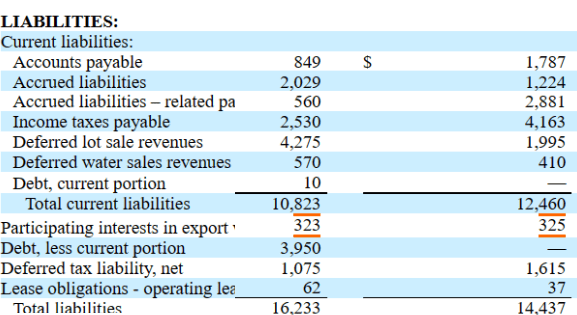

The liabilities include accrued liabilities worth $2.029 million, income tax payable of $2.5 million, deferred lot sales revenue of $4.275 million, and total current liabilities of $10.823 million. On the other hand, the debt, less the current portion, was close to $3.950 million together with a deferred tax liability of $1 million. Finally, total liabilities stood at $16.233 million, close to 8x the total amount of liabilities.

10-K

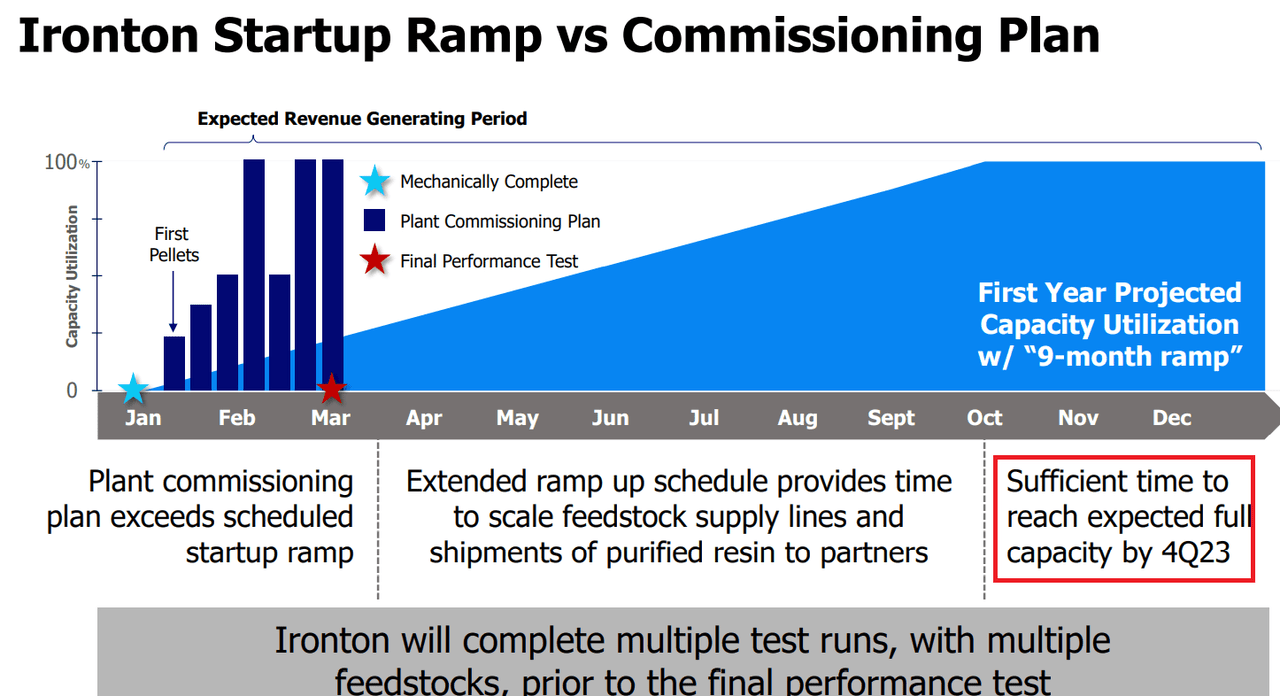

Base Case Scenario: Successful Implementation Of Ironton, Expansion Of Sky Ranch, And International Expansion Could Imply A Valuation Of $13 Per Share

Under my base case scenario, I mainly assumed that the company’s Ironton will successfully deliver revenue growth in 2023, and the expected full capacity will be reached by 4Q 2023. The following slide shows some of the expectations from management. Let’s keep in mind that my expectations are aligned with those of Pure Cycle.

Investor Relations

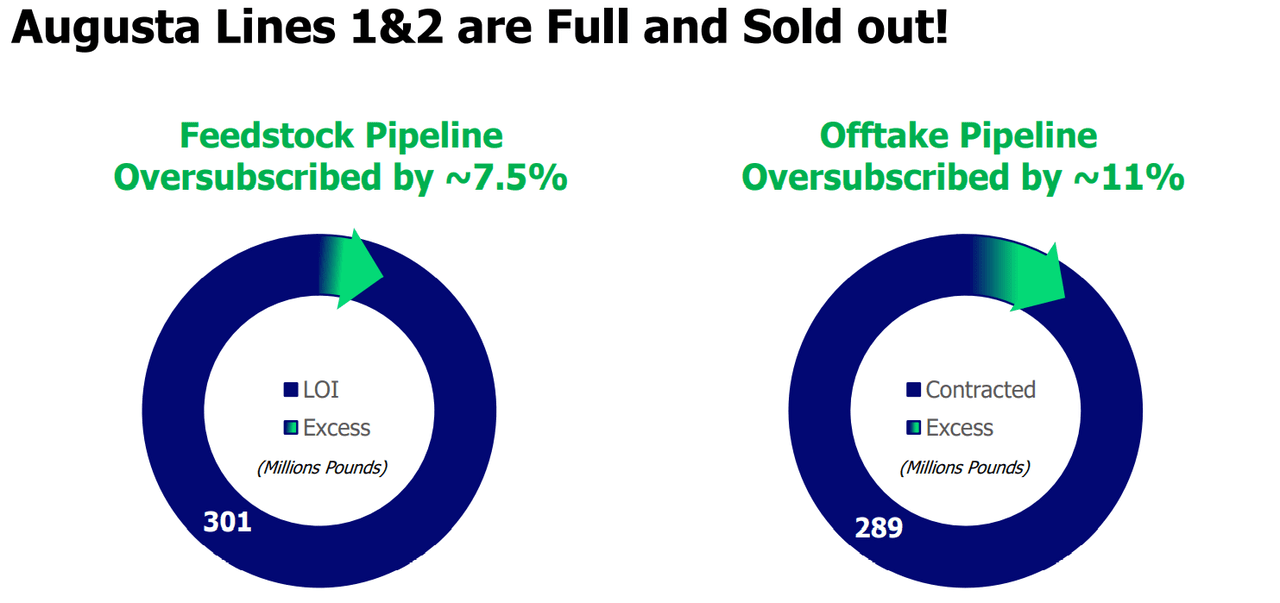

It is also worth noting that Augusta lines one and two will be successfully executed and financed. In my view, the company will likely find financing for more projects considering that these two were oversubscribed.

Investor Relations

I also assumed that management will successfully expand its capacity by around 200 rental units over the next several years. More capacity will likely mean more revenue and FCF growth.

Our newest line of business is our single-family rental business where we build single-family homes for rental purposes in Sky Ranch under annual lease agreements. We plan to expand this new line of business to more than 200 rental units over the next several years. 10-K

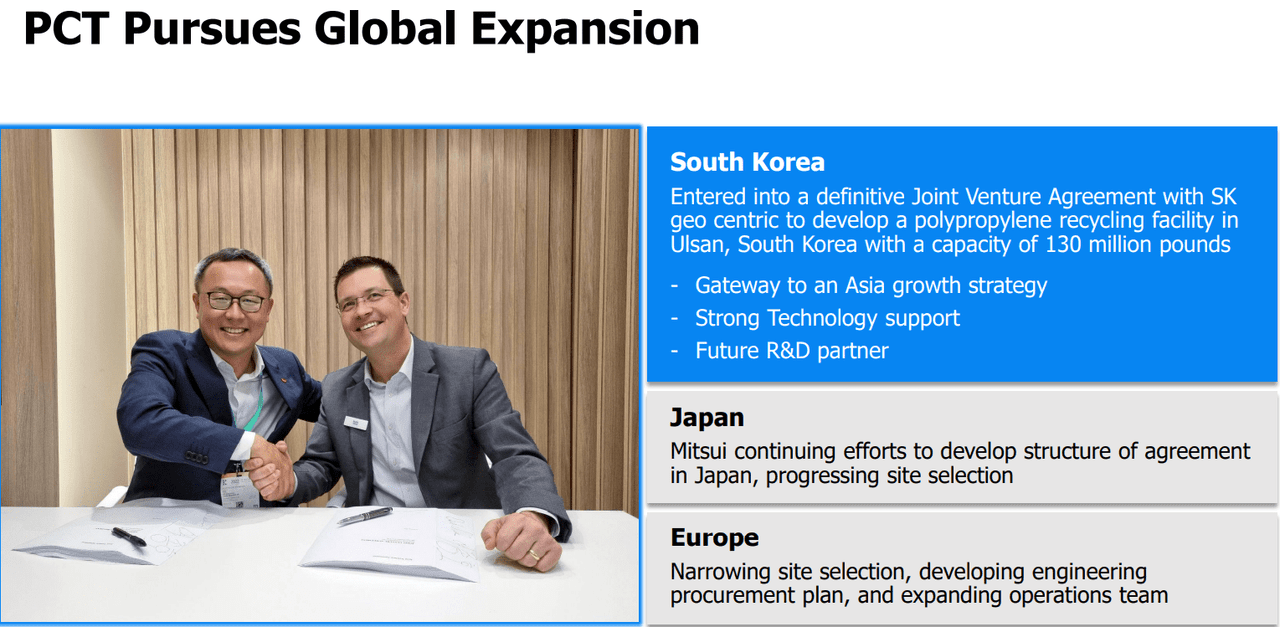

Finally, I am quite optimistic about the company’s international intentions in Japan, South Korea, and Europe. In my view, with know-how obtained in the United States and new international markets, the potential for revenue growth will likely grow.

Investor Relations

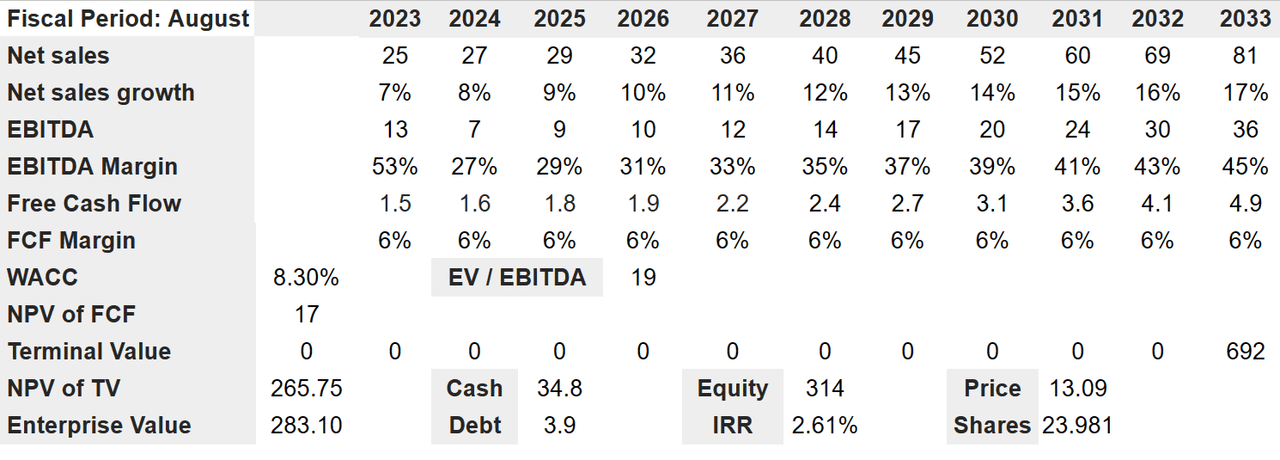

Under my base case scenario, I included 2033 net sales of $81 million together with a net sales growth of 17% and 2033 EBITDA of $36 million accompanied by 2033 EBITDA margin of 45%. 2033 FCF would be close to $4.9 million with a FCF margin of 6%.

Bersit’s DCF Model

By assuming a WACC of 8.30% together with an EV/EBITDA of 19x, I obtained a NPV of FCF of $17 million with a terminal value of $692 million and a NPV of $265.75 million. My results would also include an enterprise value of $283.10 million, cash of $34.8 million, debt of $3.9 million, and an equity valuation of $314 million. Finally, the IRR would stand at 2.61% with a fair price of $13.09 per share.

Bearish Case Scenario

Pure Cycle included in its balance sheet notes receivable from two related parties, Rangeview District and the Sky Ranch CAB. Doing business with related parties is always complicated because minority investors may not know whether the agreements signed were beneficial for Pure Cycle. Certain investors may stay away from the company due to these agreements, which may increase the cost of equity.

The Company has outstanding notes receivable of $18.3 million in the aggregate from the Rangeview District and the Sky Ranch CAB, which are related parties. The Rangeview District is a quasi-municipal corporation and political subdivision of Colorado formed in 1986 for the purpose of providing water and wastewater service to the Lowry Range and other approved areas.

The Company and the Sky Ranch CAB entered into a Facilities Funding and Acquisition Agreement effective November 2017, obligating the company to advance funding to the Sky Ranch CAB for specified public improvements constructed from 2018 to 2023. All amounts owed under the FFAA bear interest at a rate of six percent (6%) per annum. 10-K

It is also worth noting that the company is not at all diversified because most assets are located solely in the Front Range area of Colorado. If the economic activity in that area deteriorates, the decline in revenue may be significant. As a result, the stock price may decline. Management provided certain analysis about this risk in the annual report.

Our performance could be adversely affected by economic conditions in, and other factors relating to, Colorado, including supply and demand for housing and zoning and other regulatory conditions. To the extent that the general economic conditions in the Front Range area of Colorado deteriorate, the value of our assets, our results of operations and our financial condition could be materially adversely affected. 10-K

Besides, changes in the U.S. steel index, commercial transportation inflation, or even labor and supplier costs increases could diminish Pure Cycle’s FCF margins. As a result, I believe that the company’s fair valuation would decline significantly.

The market prices for certain materials and components we purchase, primarily steel and PVC piping, have been volatile. U.S. steel index prices alone increased 100 percent during calendar 2021. In addition, some supplies are subject to long lead times. Disruptions to the commercial transportation network, including limited container and trucking capacity and port congestion, have increased supplier delivery times for materials to our facilities. 10-K

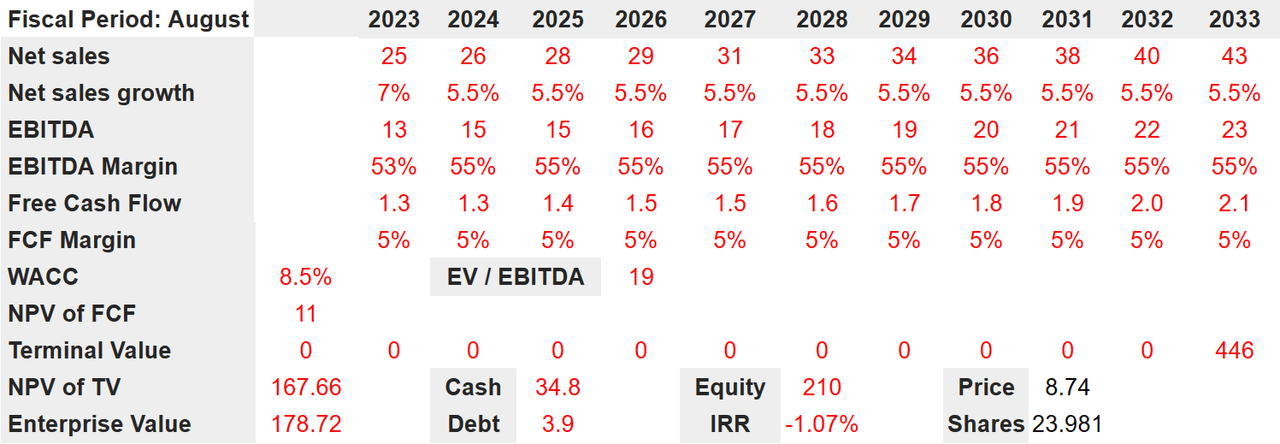

Considering the previous conditions, I included 2033 net sales of $43 million together with a net sales growth of 5.5% and EBITDA of around $23 million accompanied by an EBITDA margin of 55%. I also envision free cash flow of $2.1 million with a FCF margin of 5%.

Bersit’s DCF Model

With a WACC of 8.5% and an EV/EBITDA 19x, the NPV of FCF would be $11 million, together with a terminal value of around $446 million and net present value of $167.66 million. The implied enterprise value would be $178.72 million, which, with cash of $34.8 million and debt of $3.9 million, would imply an equity valuation of $210 million. Finally, the IRR would stand at -1.07% together with a fair price of $8.75 per share.

Takeaway

Considering the expectations with regard to total capacity growth, incoming revenue from Ironton, and the expansion Of Sky Ranch, I am expecting revenue acceleration from 2023. With conservative estimates, I obtained a valuation of close to $13 per share. I also envision certain risks from lack of diversification, steel price increases, and labor costs increases. With that, in my view, the company remains significantly undervalued.

Be the first to comment