small smiles

Investment Thesis

As fears of a recession grow, Prospect Capital (NASDAQ:PSEC), like many of its peers in the BDC sector, finds itself vulnerable to macroeconomic challenges inherent from its natural exposure to highly-leveraged SMEs. As a group, SMEs are highly sensitive to economic cycles, and those leveraged by BDCs through loans and debt instruments are particularly vulnerable.

Nonetheless, PSEC holds a tried-and-tested defensive tactic that will allow it to absorb at least some of the economic impact relatively better than most of its peers, giving it an edge in the market in a recession scenario. PSEC is where you want to be if you seek exposure to BDCs in my view.

However, for investors with a more flexible asset allocation strategy, I see that the 8.8% yield on the Series A preferred stock (PSEC.PA) is preferable to the 10.2% yield on the common stock.

Our hold rating mirrors PSEC’s attractive dividend yield, weighed against a limited capital gain potential. Below we discuss the company’s unique position in the BDC market, shareholders’ opportunities, and risks in light of economic headwinds facing the economy.

PSEC’s Strengths

PSEC is the top performer among the select group of BDCs surviving the 2007-2008 crisis (with fully-deployed capital) and remains so even when compared to newly-established BDCs that prospered in the subsequent economic recovery. To find out how this transpired, let’s follow two BDCs through the 2007-2008 crisis.

American Capital (ACAS) was already operating at full throttle when the financial crisis of 2007 and 2008 hit, stretching its balance sheet near asset coverage regulatory limitations, which stood at 200% at the time (currently 150%). As the economy weakened, management began to write off bad debts. It had to liquidate assets, ironically the ones that were doing the best in order to keep its coverage ratio stable. With investors’ confidence at an all-time low, the stock market was practically out of reach. The number of assets under management “AUM” dropped from $8.1 billion in 2007 to $5.5 billion in 2009.

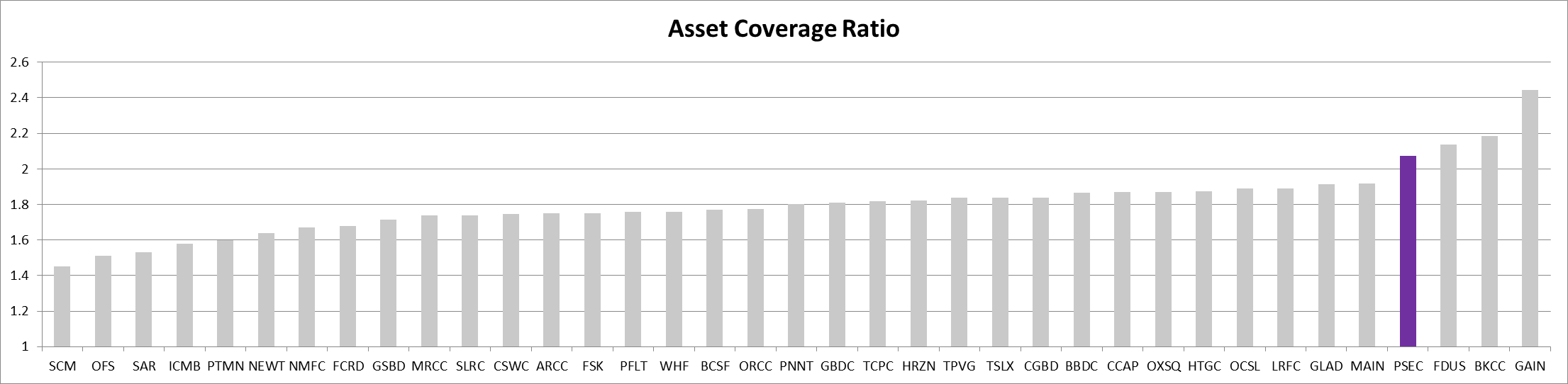

On the other hand, PSEC’s asset coverage ratio was 490% when the crisis began, well over ACAS and regulatory limits. This allowed PSEC to expand its assets when other BDCs were closed for business, leveraging its credit facility for interim finance and then gradually repaying it with equity as markets recovered. This allowed PSEC to scoop quality assets at attractive prices when everyone was selling.

The lesson learned is: low leverage is a critical aspect to consider when investing in BDCs in the current economic climate. Below is a chart showing PSEC’s asset coverage ratio compared to its peers.

Industry Comparison: Asset Coverage Ratio (Author’s estimates based on data from Ycharts)

A BDC’s access to liquidity is just as crucial as its low leverage. When times are hard and valuation multiples go down, equity financing becomes a bad idea because of the deep discount to NAVs experienced in the BDC sector as markets plummet. Debt becomes the only viable choice, but it may not be an option if money is scarce. Companies might find it hard to raise debt notes during economic disruptions when everyone is strapped for cash. Thus, having a leveraged margin above regulatory limits is sometimes not enough. A balance under a BDC’s revolving credit facility, along with regulatory access to this balance, is critical when assessing a BDC in the current market environment.

Weakness

PSEC leverage did increase in the past few quarters. In 2006, its asset coverage ratio was 450%, compared to 200% at the time of this writing. Thus, its dry powder did shrink.

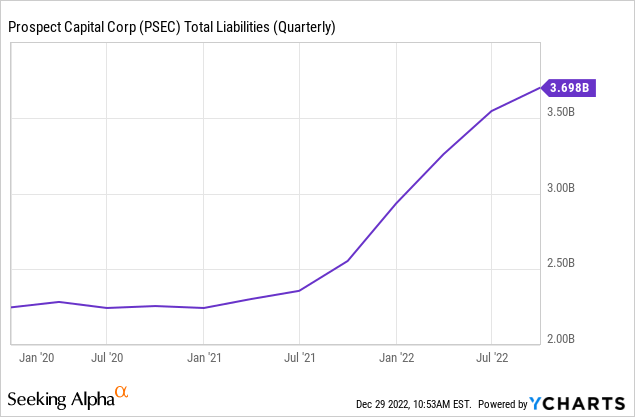

Below is a chart demonstrating PSEC’s leverage evolution in recent quarters, exhibiting growing leverage in the last fiscal year that ended in June 2022. Nonetheless, it remains below the industry average, as shown in the graph above.

Although PSEC has been increasing its leverage over the past few quarters, it is still one of the least leveraged of its competitors. Moreover, at this point, the company has about $700 million under its credit facility.

There is a fundamental problem in the company’s structure that almost guarantees future losses in NAV per share and, subsequently, price per share. Minimum distribution requirements limit PSEC’s ability to recover capital lost from bad loan write-offs. In the BDC sector, a dollar lost in bad loans will likely be lost forever and never be fully regained beyond negligible quarter-to-quarter NAV volatility and perhaps some realized gains from equity sales of the few companies that do well. This is why about 80% of BDCs lose NAV per share value after inception. It is up to the shareholder to make any necessary adjustments for capital losses in order to protect their wealth.

Despite its above-average historical performance, management doesn’t possess an exceptional talent beyond being cautious and prudent when others are greedy. PSEC’s rapid asset expansion through equity and debt allowed it to cover most of its losses, smoothing the decline in dividends and NAV.

The cost of management is the last thing we’ll talk about here. I don’t think PSEC shares will ever trade at NAV per share. Let’s say it does happen, and the ticker starts trading at $10 per share. At this point, PSEC’s dividend yield becomes equivalent to the yield of a similarly leveraged portfolio of 1-year Treasury bonds. The aberrant risk/reward stems from high management fees. About half of PSEC’s quarterly income goes to its large management fees and operational costs.

Summary

The nature of BDCs’ operations makes them a high-risk investment, and interest payments from financially vulnerable SMEs are a significant contributor to their bottom line. If you must invest in BDCs, PSEC is your best bet. Most of the other alternative BDCs run close to regulatory asset coverage limits, barely enough to cover the potential NAV write-offs during economic disruptions, not to mention enough to inject fresh capital to survive, whether from raising debt or tapping into a previously set credit facility. I think this gives PSEC an advantage over its peers.

PSEC is a great investment for long-term growth-oriented investors because of its history of strategically leveraging its revolving credit facility during economic turbulence, expanding while everyone is seeking cash. However, investors should be aware that the company, like all BDCs, faces structural challenges, making it almost certain that it will cause a loss of NAV per share in the long run. Buying PSEC is a gamble that your annual dividend will more than cover your investment losses in my opinion.

Be the first to comment