Torsten Asmus/iStock via Getty Images

Kudos to those investors who have correctly bet on rising interest rates in 2022 and bought the ProShares UltraPro Short 20+ Year Treasury ETF (NYSEARCA:TTT). However, I think it is now time to cash out your winnings, as long-term interest rates appear to be inflecting lower on recession fears. TTT is an inverse levered product and is not meant to be held over the long-term, as demonstrated by its 10Yr average annual total returns of -10.2%.

Fund Overview

The ProShares UltraPro Short 20+ Year Treasury ETF seeks daily returns that is -3x the return of the ICE U.S. Treasury 20+ Year Bond Index. The fund achieves its -3x daily exposure target through total return swaps with investment banks that are reset nightly.

Strategy

Readers are encouraged to take a look at some of the other articles I have written on levered ETFs to learn the mechanics of how levered ETFs work. The two key points to understand are that levered ETFs have “positive convexity” in the direction of their bet (position grows as it is going in your favour) and “negative decay” due to volatility and the daily reset of exposures.

The TTT’s goal is to provide 1-day returns equal to -3x the return of the ICE U.S. Treasury 20+ year Bond Index (“Index”). The index is designed to measure the performance of U.S. dollar-denominated, fixed rate treasury securities with minimum term to maturity greater than 20 years. In layman’s terms, the TTT is betting that long-term interest rates will rise, and long-term treasury bond prices will fall.

Portfolio Holdings

As discussed above, the TTT ETF’s holdings are total return swaps with major investment banks like UBS and Citibank on the underlying index. In total, the fund holds -300% of assets in swaps vs. 100% of assets in treasury bills (acting as cash) used to settle accounts daily with the investment banks (Figure 1).

Figure 1 – TTT ETF holdings (proshares.com)

Returns

So far in 2022, the TTT ETF has returned an incredible 181.6% to October 31, 2022, on the back of rising interest rates (Figure 2).

Figure 2 – TTT ETF returns (proshares.com)

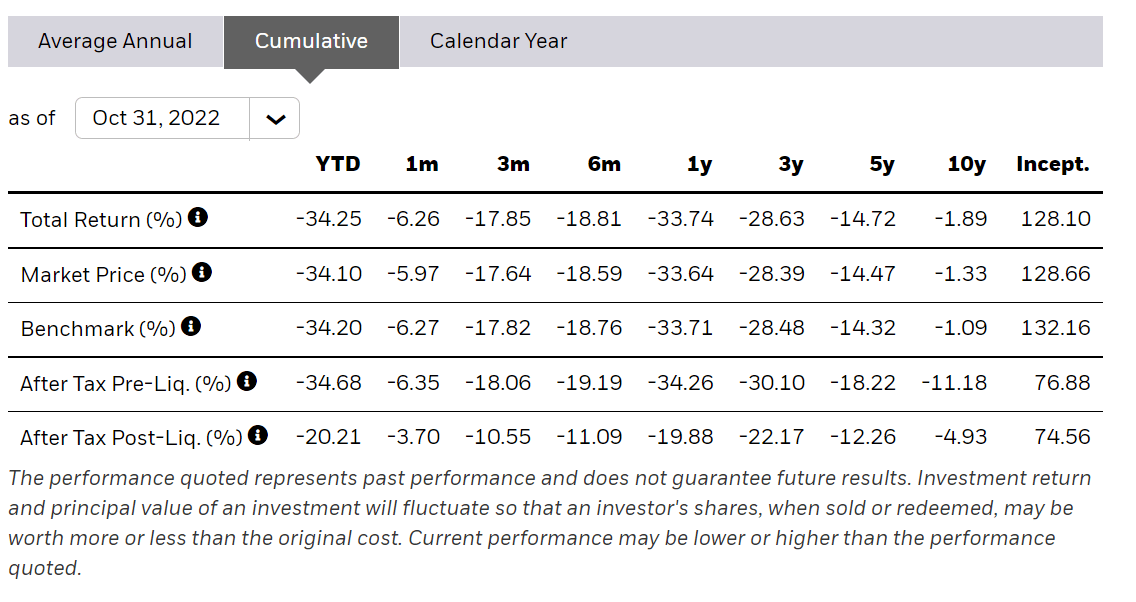

Note, TTT’s return has significantly outperformed -3x the return of the underlying index, as represented by the iShares 20+ Year Treasury Bond ETF (TLT), which lost 34.3% YTD. This shows the ‘positive convexity’ effect mentioned above (Figure 3).

Figure 3 – TLT ETF returns (ishares.com)

However, TTT’s long-term returns have been abysmal despite the short-term YTD boost, with 10Yr average annual total returns of -10.2%, which is reflective of the ‘negative decay’ factor.

Distribution & Yield

The TTT ETF does not pay a distribution.

Fees

The fund charges a 0.95% expense ratio.

Long-term Treasury Yields May Be Peaking

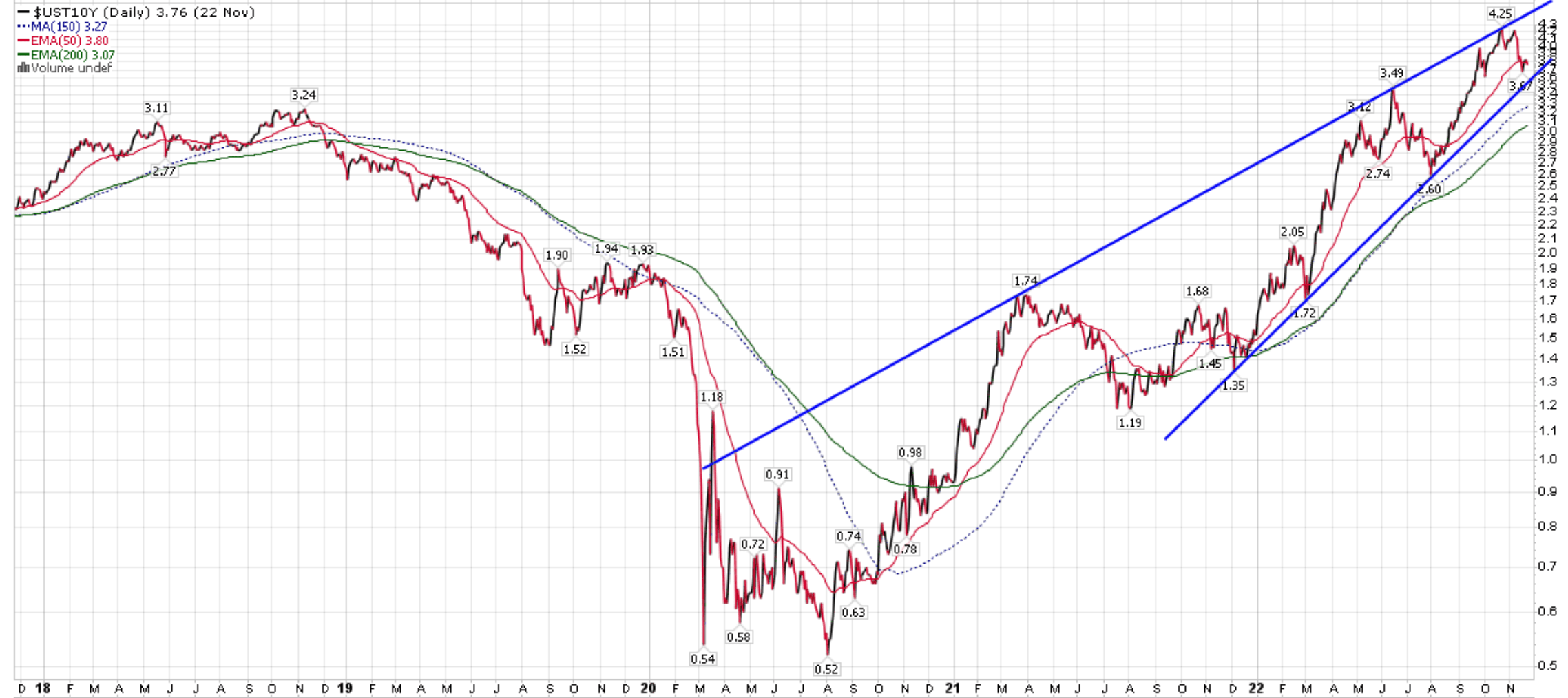

While TTT’s performance had been outstanding YTD to October 31, the fly in the ointment is that the fund has suffered a 30%+ drawdown in the last few weeks, as long-term interest rates have backed off their highs. Figure 4 shows the US 10 Year Treasury yield as an illustrative example.

Figure 4 – US 10 Year treasury yields is forming a bearish wedge (Author created with price charts from stockcharts.com)

Long-term yields have eased in recent days because economic conditions continue to deteriorate, with many signs pointing to a potential recession in 2023. For example, the recent S&P Global Flash U.S. Composite PMI readings of 46.3 was a big miss to consensus and is “consistent with the economy contracting at an annualised rate of 1%”, according to S&P Global Market Intelligence’s Chief Business Economist.

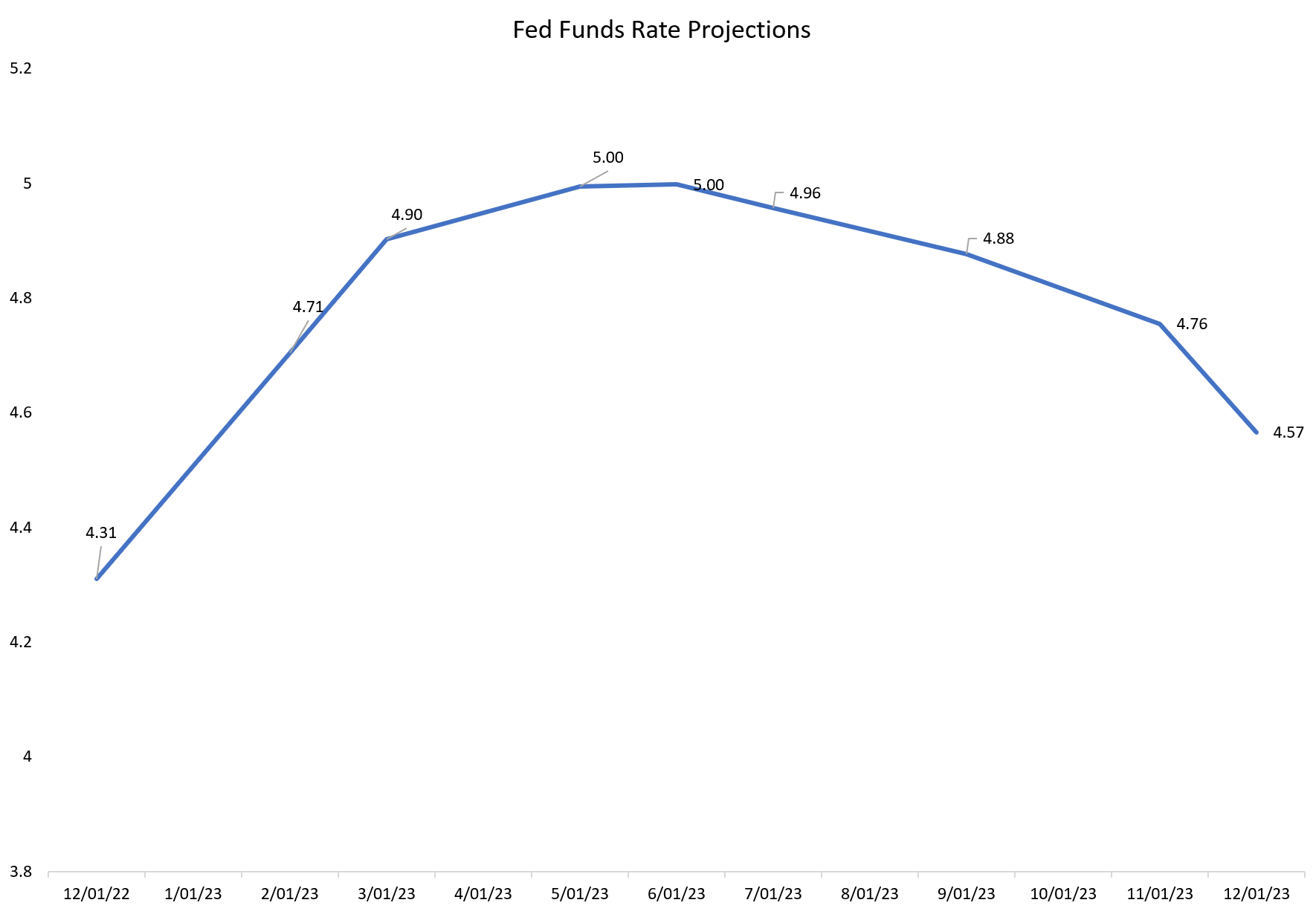

With an impending recession, the market is starting to price in the Federal Reserve ‘cutting’ interest rates in the back half of 2023 (Figure 5).

Figure 5 – Market implied Fed Funds rate (Author created with data from CME)

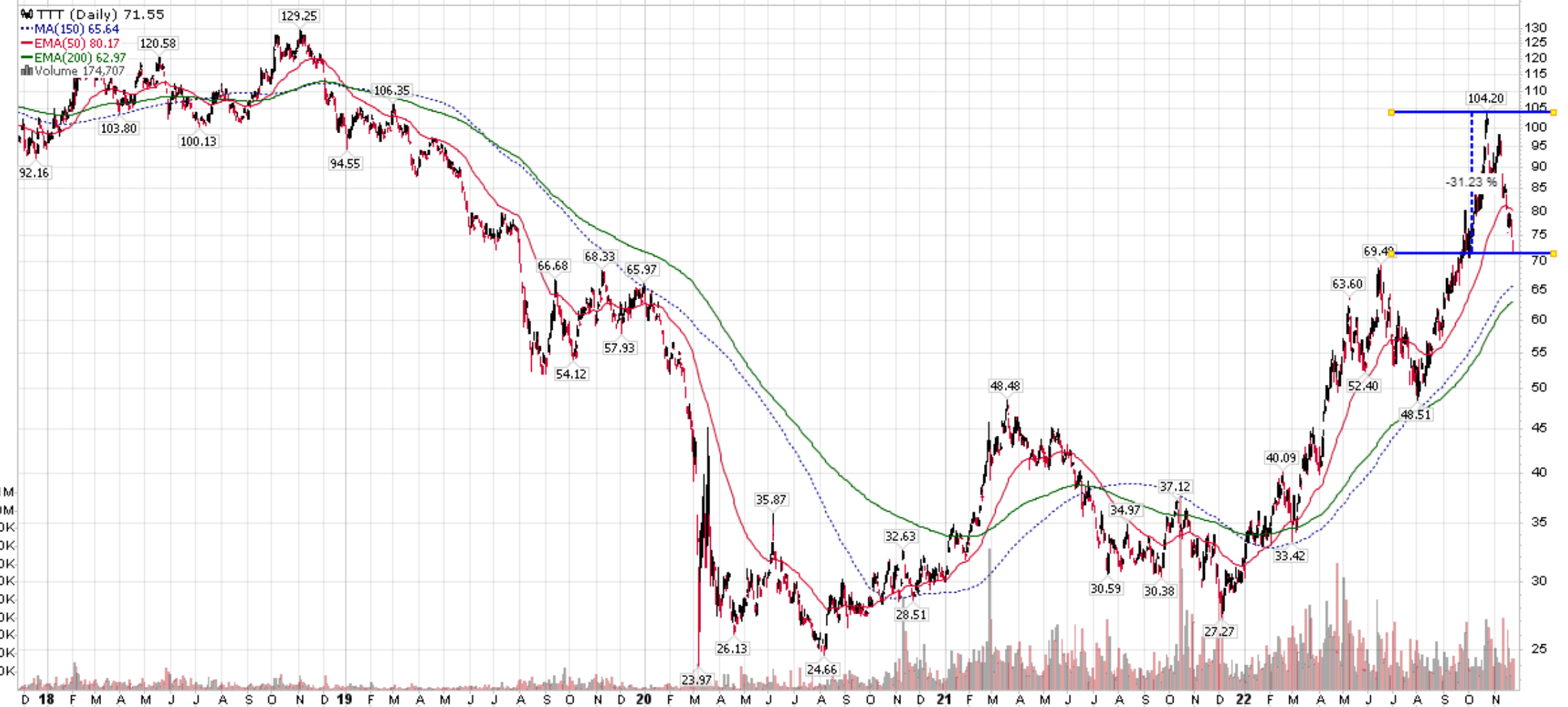

This has led to TTT’s dramatic 30%+ drawdown from October highs (Figure 6).

Figure 6 – TTT is suffering a massive 30% drawdown (stockcharts.com)

Conclusion

Kudos to those investors who have correctly bet on rising interest rates in 2022 and bought the TTT ETF. However, I think it is time to cash out your winnings, as long-term interest rates appear to be inflecting lower. TTT is an inverse levered product and is not meant to be held over the long term, as demonstrated by its abysmal long-term returns.

Be the first to comment