Editor’s note: Seeking Alpha is proud to welcome The Dragon of Wall Street as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Tony Studio

Progress Software (NASDAQ:PRGS) is one of those companies that has proven to be relatively stable with a low beta. However, as the title suggests, the current valuation and acquisition prospects raise questions as to whether the company is a good buy at this level or if it’s better to hold off. I believe it is currently better to wait for various reasons, including technical and fundamental ones, which is why I rate it a hold for now.

Company Description

Progress Software is a technology company based in Burlington, Mass., that provides a variety of business applications. Many of these applications were acquired by Progress, which has been performing mergers and acquisitions (M&A) almost consistently since 2002.

Among its suite of applications it has OpenEdge, which allows developers to create highly compatible programs that can be used on any device, platform, or cloud environment. Developer Tools provides the tools necessary for user interface (UI) development for applications in a variety of environments like web, mobile, augmented reality (AR), and virtual reality (VR) – to name just a few.

The company’s more recently acquired applications include Chef, which is a platform as a service (PaaS) meant to enable infrastructure automation. The company also has Kemp and its apps Loadmaster and Flowmon Network Visibility. Loadmaster allows users to load in software deployment templates to enhance performance for their applications, while Flowmon Network Visibility enables faster monitoring and diagnosis of problems by collecting and transmitting network data from the sources it can access.

According Progress’s corporate information page, their mission is “to be the trusted provider of the best products to develop, deploy and manage high-impact applications,” while their vision is to be a company that “propels business forward in a technology driven world.”

How is the company doing this? Their primary strategy seems to be to grow inorganically by purchasing other companies that they believe will have great synergies with their product offerings. They oftentimes reject a lot of offers even if the acquisition target were to lower their asking price dramatically, which would imply that they are a picky corporation when it comes to M&A:

And number three: deploy capital to produce the highest shareholder returns, preferably through accretive acquisitions that fit out disciplined criteria.

As a result of our stringent standards, we have passed a number of deals that did not meet recurring revenue or retention rate criteria. Some sellers have tried to reengage at significantly lower asking price, but we’ll remain disciplined because any business we buy must deliver strong returns that are sustainable over the long haul.

They sell their software on a perpetual license more often than their term licenses, although their cloud offerings are offered through a subscription service model. That provides some variation in revenue sources despite their concentric growth strategy.

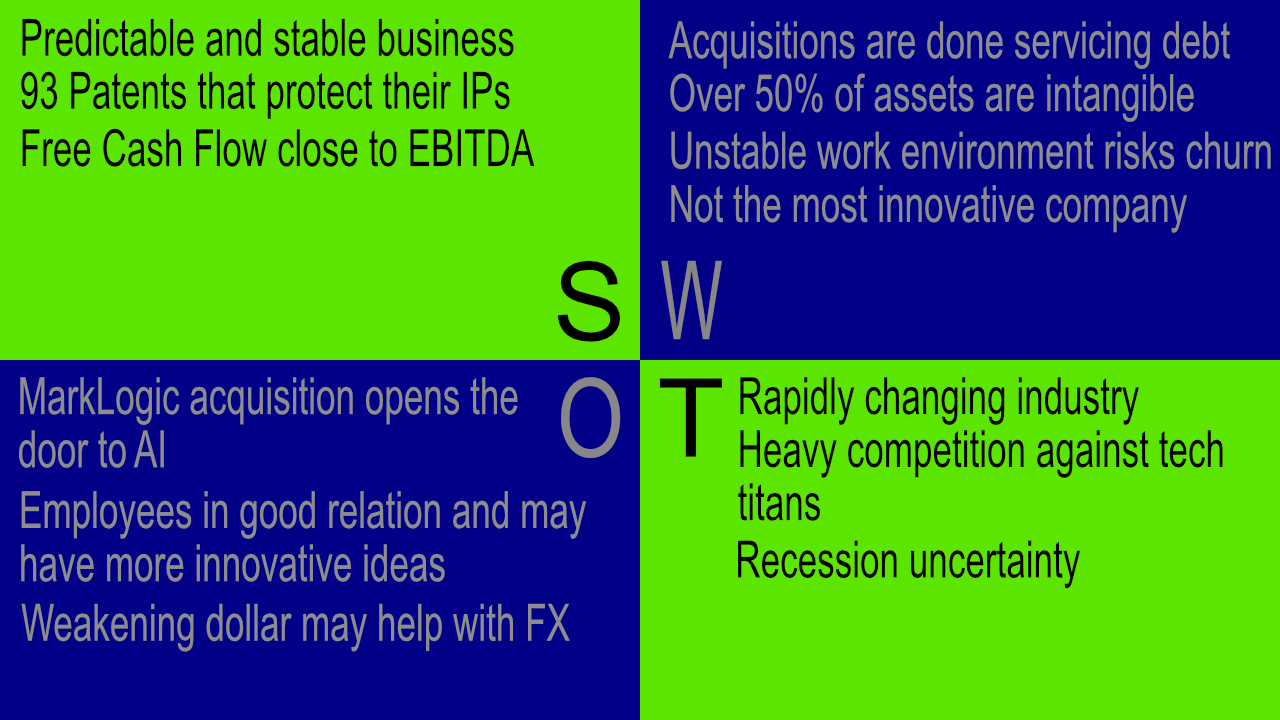

SWOT Analysis

Looking into their filings, environment, and employee reviews, I was able to prepare a SWOT analysis that can be summarized as follows:

Created through Affinity Designer

For more strengths, I read in their latest 10-K filing that they don’t have a single customer that contributes more than 10% of their revenues. That said, they also derive a lot of their revenues from OpenEdge and their licensing model. However, I haven’t seen any indicator as to the proportion of their revenues derived from each application.

They do, however, derive most of their revenues from North America and EMEA (Europe, Middle East, and Africa). This composition of revenues could explain the FX impact of last quarter if contributions from North America are less than half of the revenue derived from that geographic sector, which is why I see an opportunity if the dollar keeps weakening.

However, we must consider what a recession could do to the company. Because they are a business to business (B2B) corporation, they are a lot less likely to suffer majorly from a recession unless corporations decide that their offerings are not worth keeping during this kind of environment. Alternatively, a new or existing competitor could come up with a better and/or more comprehensive suite of offerings. Since they compete with some larger companies – such as Salesforce (NYSE:CRM) and Microsoft (NASDAQ: MSFT), for example – they are a relatively small fish compared to the sharks that can simply buy the company if they wanted.

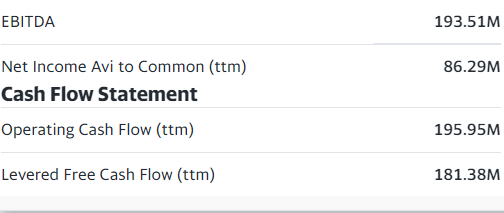

EBITDA vs Cash Flows vs Net Income (Yahoo! Finance)

Another thing that can help them is their strong cash flow, which is almost as large as their non-GAAP EBITDA. That said, while this would allow them to better execute acquisitions, I am concerned about the pace of acquisitions and the implications of such a rapid pace of change. It is certainly showing in their labor force, where their employees occasionally cite a rapidly changing environment – constantly onboarding new acquisitions or even having to handle a constantly changing market strategy, to the point that the company restructured their sales division and laid off employees.

I also find the way one employee’s review on Glassdoor described their M&A strategy rather impactful: “The acquisition strategy seems to boil down to ‘buy companies kinda sorta like us and add to the bottom line through their sales.'” I feel as if this describes to some extent what Progress might be doing, which is starting to raise some concerns regarding the execution. Granted, I also need to point out that Progress’s relationship with their employees seems to be in good hands, and they also seem to remain true to allowing flexible work for their employees as well as providing benefits. Only one employee that I searched on Glassdoor said that the company would rather switch back to a fully on-premises model.

Some employees also seemed to want to implement their own ideas, but weren’t listened to. It appears that the management structure within Progress might be more vertical and slower, which can inhibit innovation. That said, I do believe there could be new opportunity if employees are able to have a more impactful voice in the company, provided that those opinions are managed responsibly. I should note, however, that these employee reviews are anonymous and could certainly be proven false. However, I like to check this as part of my research as companies can overstate their treatment of employees, which I believe is a fundamental factor in effectively driving their mission forward.

To wrap up the SWOT section, I believe that that the strengths and weaknesses are there, but they seem to be evenly matched. This should give Progress the opportunity to hone in on the weaknesses and try to fix problems. Additionally, should a recession materialize, it would be rather intriguing to see how Progress, a low-profile B2B corporation, would fare compared to their larger competitors.

Recent Earnings

There are two sets of earnings results that I’d like to touch on, one being their latest Q3 results and the other being their Q4 preliminary results.

Q3 2022

Their Q3 results overall show the promise that the company presents. I can see why other investors would be modestly bullish seeing the large gross profit margins that they have. This would leave a lot of room to do research and development (R&D), sales and marketing, and even pay their employees a decent wage and good benefits, as well as hold small events for their employees (which can be a morale booster for some). However, their Q3 growth raises some concerns as revenue was rather modest compared to Q2, their gross profit margins remained flat, and their operating margins have shrunk.

Q3 Operating Expenses (Progress Software Filings)

If we look more closely, it seems as if the company is spending more overall for their sales, research, and administrative expenses as all three categories show an increased expense collectively hurting their margins. Some of this could be due to wage inflation, or it’s possible they hired more staff to better handle the expanded company. The former is more likely in this inflationary environment.

The company’s GAAP EPS for the quarter was $0.50, while the year currently boasts a diluted EPS of $1.61 according to their filings, which for me shows an interesting dichotomy in their GAAP and non-GAAP metrics. Because of this, most investors could reasonably believe that the company is trading at a fair valuation of around 12x their non-GAAP EPS. But if we take their average GAAP EPS throughout the year (~$0.54) and add that as an estimate, we’d have a total diluted EPS of $2.15 for the year, which converts the current valuation of $51.41 as of the close on Jan. 4, 2023, into a valuation of almost 24x GAAP EPS.

It’s worth looking more closely at the differences between their GAAP and non-GAAP financial measures, but this is a strong case of “the devil is in the details.”

Meanwhile, on their balance sheet things look normal, don’t they? Well, here’s the thing: Their total current assets amount to $364 million in value, while they have almost $1 billion in longer-term assets. The majority of these are intangible assets.

Let’s do the math:

- Net intangible assets = $233.436 million

- Goodwill = $672.901 million

- Total long-term asset value = $981.858 million

- 981.858 – 233.436 – 672.901 = 75.521

This means they have long-term tangible assets of $75.521 million.

There’s a lot I’m already thinking about with this information. It’s possible that they’re overpaying for some of their acquisitions, especially as goodwill increased more with their M&A activity. It’s also possible that the patents, trademarks, and product portfolio might have a high level of perceived value according to the people auditing and deciding on the fair value of each intangible asset. Whatever it is, this would be a slight risk if Progress fails to obtain a good price for any assets containing intangible assets as, in reality, intangible assets can have their value psychologically derived.

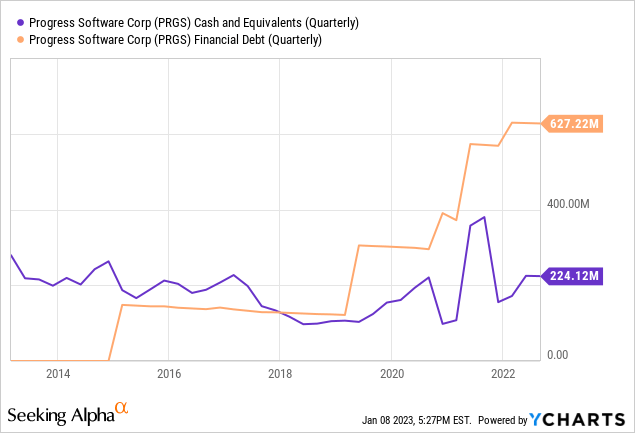

Their debt levels of over $600 million and cash levels of $224 million would raise some concerns, but even more concerning would be the fact that Progress Software gained more debt than it is paying off. One should reasonably expect some level of growth to justify the added debt – and to some extent, it has. However, with rising interest rates and a looming recession, it raised some eyebrows for me – especially with the current context.

Their combined operating and investing cash flows are consistent with the free cash flows calculated online, being slightly over $175 million, which is higher than their net income. Is this sustainable? So far, the bigger influences on cash flow outside net income are the amortization of acquired intangibles and stock-based compensation. It’s reasonable to say that such cash flow might be sustainable considering they are acquiring yet another company soon, so more likely than not we’ll see added amortization this year again once the acquisition succeeds.

Stock-based compensation could also be sustainable; however, I do not fully understand yet why it’s being added instead of subtracted. I could offer some interpretations such as executive stock-based compensation being available or added but not yet paid to executives, but outside of that I would figure stock-based compensation would be a drain on operating cash flows.

Q4 2022 (Preliminary)

As stated by the company:

Based on currently available information, Progress anticipates ARR to end the fourth quarter 2022 at approximately $497 million, or growth of 3.5% year over year. In addition, Progress anticipates non-GAAP revenue and non-GAAP earnings per share to be within or above the high-end of previously issued guidance provided on Sept. 27, 2022. The company will discuss full financial results on its fourth quarter earnings conference call on Jan. 17, 2023.

So far it seems as if things are going well for Progress for the remainder of 2022, as their ARR increased about 3.5% and they say that their non-GAAP revenue and their non-GAAP EPS would end close to or higher than what their guidance stated back in late September. In numbers, this means that their revenue would have to be closer to $166 million and their non-GAAP EPS closer to $1.10, slightly above average analyst estimates.

This could also mean that for the year their revenue would reach $600 million, which is a feat in my opinion, and some progress toward reaching $1 billion. I should also recognize that a non-GAAP EPS of $4.10 would be impressive for a company this size; however, remember what I noted before about the difference between the GAAP and non-GAAP metrics and how this impacts valuations.

MarkLogic Acquisition

To recap the transaction and to better allow you to understand the situation, the acquisition means that Progress would purchase MarkLogic, which is one of the leading modular NoSQL database platform providers that allows users to create insights from the data they allow into the platform. In some way, I feel this would compete with the likes of Snowflake (SNOW) as they too are meant to generate insights and store copious amounts of data. However, I am not fully educated on the more specific differences of both platforms.

MarkLogic has managed to leverage AI technology, however, so their platform can generate insights for the user utilizing already existing data, which is intriguing. It appears as if the acquisition is being made not just for the trending “AI” buzzword, but because the technology would be able to help customers more quickly get information and a better understanding of what they need, as such artificial intelligence would be able to give them the information in a more easy-to-digest manner.

They apparently generate revenue of $100 million, while they have over 300 customers. Progress Software claims that MarkLogic has high customer loyalty, but a quick look on Comparably gave me a rating of 68% when it comes to loyalty to the brand – not fantastic.

The transaction would use a mix of cash and debt to complete it, as was said early on during the update call. The company mentioned that they would use around $200 million from their line of credit, which would increase their net debt to over $800 million. Considering their currently minuscule equity ratio, this would push debt/equity above 200%, granting that equity remained the same. The transaction is valued at $355 million, which is $645 million cheaper than their valuation of $1 billion achieved in 2015 during one of their funding rounds. This would mean that Progress would have to use about $155 million cash to complete the transaction and bring cash levels below $100 million, not counting any cash added from Q4.

To be blunt, I’m skeptical about this. A pattern of increasing debt consistently could be a double-edged sword. While using debt can allow a company or individual to spread out the life of their current cash reserves and make an aggressive expansion, it’s concerning when a company is consistently spending more than they make in cash and adding more debt than they are managing to pay down. With a debt-to-equity ratio above 100%, this could be bad, especially as this acquisition could allow that same ratio to break above 200%.

It could be that Vector Capital is looking to divest one of their “dogs,” but there is no detail about the transaction value of MarkLogic when it was acquired by the private equity firm in late 2020. If the company does not manage to achieve their goals or MarkLogic or Progress starts to underperform after the transaction, this could end up trapping the parent company in a much more dire situation. It’s also possible that some of the claims could be exaggerated. However, the most I’ve seen so far is Comparably giving it a 68% in customer loyalty, which could also be skewed if the rating depends on people going there to rate their loyalty.

Overall, I think the best I can do is watch how the acquisition unfolds. Time tells the ultimate story, and I could be wrong. The added revenue is enticing, but at the rate we’re going there’s only so much inorganic growth a company can have before it needs to stand on its own two feet – given that the company even has feet.

Bull Case

A few factors come into play that help the bullish case. Investors have a potentially positive Q4 earnings to look forward to, which could help the fundamentals of the company and inspire people to buy the stock, potentially at higher valuations.

The company is also relatively safe in terms of momentum and dividends, which means that anyone could have this company’s stock as a dividend play or as a store of cash with a small potential for upside. The acquisition of MarkLogic can be very accretive as it is not a dilutive acquisition and isn’t fully financed by debt, which can help the stock in the long term.

They also have a very consistent stream of revenue and profits that endured the pandemic closures, and their stock price has shown some resilience and relatively fast recovery during the current bear market.

Bear Case

There is some reason to be bearish, even if temporarily. There could be a better time to buy the stock in the future, as the current sentiment might turn more bearish and more time is given for investors to digest the information from the last update call.

The current debt levels and lack of tangible assets might put into question the viability of Progress Software’s balance sheet in a difficult time. Much of their balance sheet depends on psychological valuations, intangible assets that could fizzle out should management or a potential buyer believe those assets are worth less than they were audited to be. However, it’s difficult to understand the nature of intangible assets; I’m using my best knowledge at the time to examine some of these questionable points.

Debt levels, and subsequently interest payments, might increase should rising interest rates prevent Progress from getting better terms that won’t put a dent in their margins from having to pay interest. Net cash used might also be affected if such debt spending ends up increasing more vs. what MarkLogic accrues.

The company also has a lackluster growth rate independent from acquisitions, as well as GAAP valuations that diverge from the non-GAAP valuations by a significant amount. The company also might not be immune from recessions and a complete crash in the stock market.

Conclusion

Progress is a very reliable company with a strong track record. However, with questionable execution of their M&A strategy and increasing risks in the global economy, it’s worth wondering if there are better days ahead to buy the company’s stock.

The business is not that unique in some ways, but I do like the concept and what the company has been able to achieve so far. I would rate it a buy if the stock price were below $43, which is at least 20x their GAAP earnings and over 14% below my price target for now. But its current state and the uncertainties ahead rationalize my caution. I rate Progress Software a hold with a price target of $50 until further clarity is seen from their earnings and price action.

Be the first to comment