jetcityimage/iStock Editorial via Getty Images

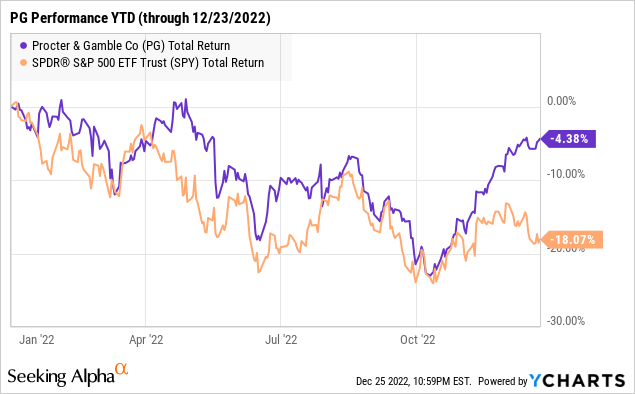

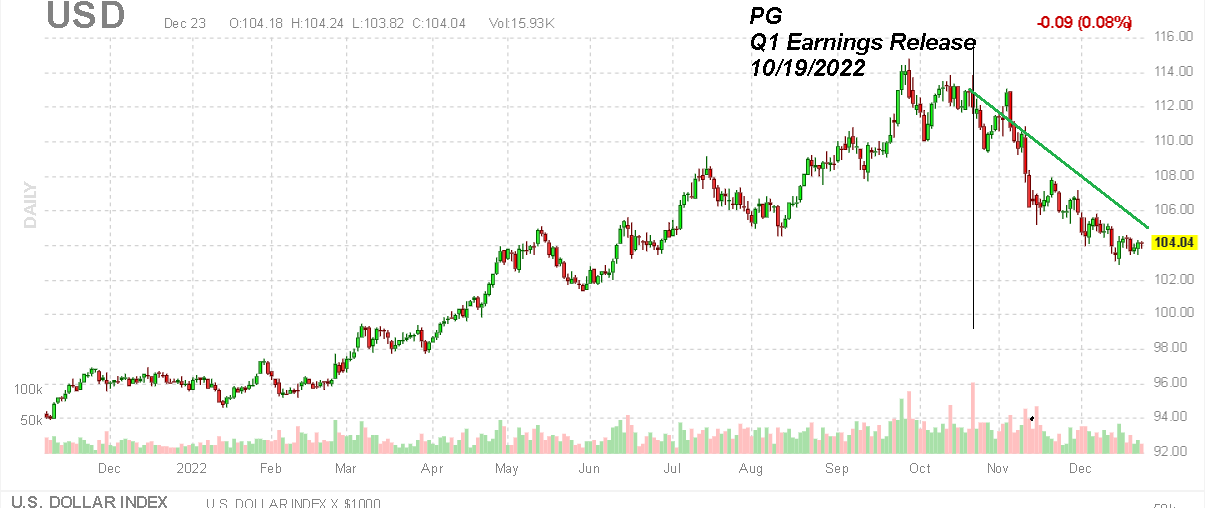

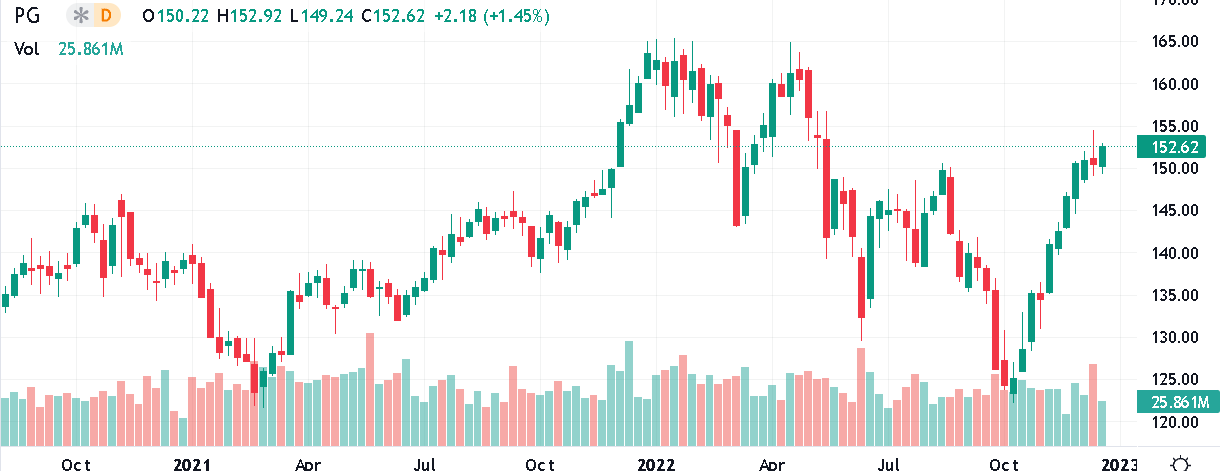

Procter & Gamble Co (NYSE:PG) has managed to salvage an otherwise challenging year with an impressive rally, up more than 25% since October with positive momentum. Even as shares are still down over the past year, PG is trading at a near seven-month high, with the strength coming on the heels of better-than-expected earnings last quarter.

On the other hand, PG is a stock that seemingly appears perpetually “expensive” with that criticism back in play considering several ongoing macro headwinds. Still, there is also an excellent case to be made that its premium valuation is justified considering the combination of leadership in consumer staples, excellent financial execution, and overall solid fundamentals. While we don’t expect shares to runaway significantly higher, we are bullish on PG which likely has more upside in 2023.

PG Key Metrics

PG is set to report its fiscal 2023 Q2 earnings on January 19th. The current consensus is for headline sales to decline by -1.6% from last year in the context of particularly strong comparables while EPS is expected to be -4.6% lower largely impacted by FX volatility. That being said, the key here is to focus on organic sales and currency-neutral EPS which paint a more favorable picture of underlying conditions.

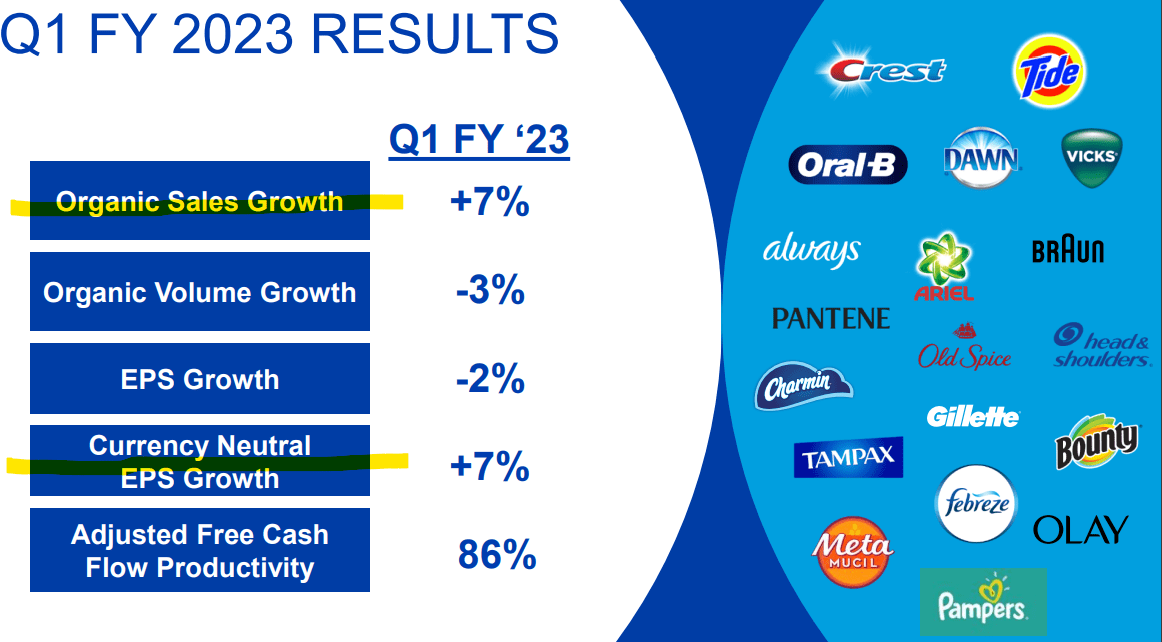

The setup into 2023 should be a continuation of positive growth despite what management has called a difficult operating environment. Facing cost pressures under the theme of persistent global inflation, an effort to increase pricing has paid off which led to 7% higher organic sales in the last quarter balancing some volume softness.

source: company IR

An important theme is an ongoing portfolio transformation where PG has consolidated its offerings from more than 170 brands back in 2017 to a current 65, focusing more on top performers in key categories. The result is that a shifting sales mix has supported climbing underlying margins. On this point, excluding FX, currency-neutral EPS growth up 7% last quarterly highlights the resiliency of PG financials.

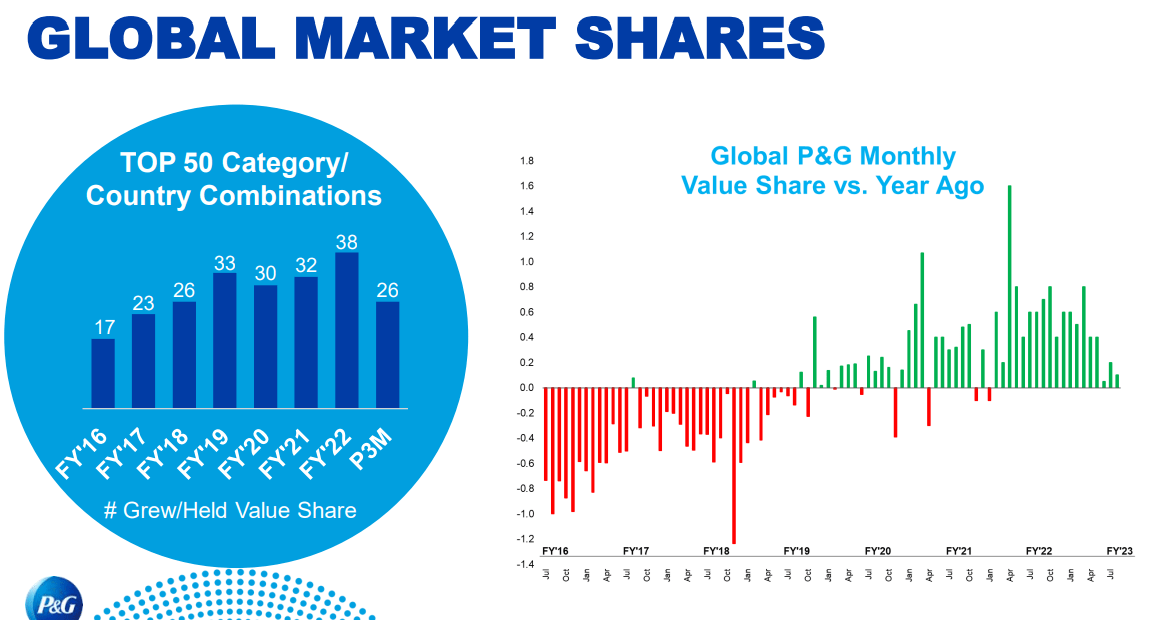

The chart that stands out to us is its ongoing global market share gains by PG where it was able to outperform rival brands in 26 out of the top 50 category-by-country combinations. The big insight is that consumers value PG’s premium positioning in segments from Beauty, Grooming, Personal Health, Home Care, and even Baby products.

source: company IR

What’s Next For PG in 2023?

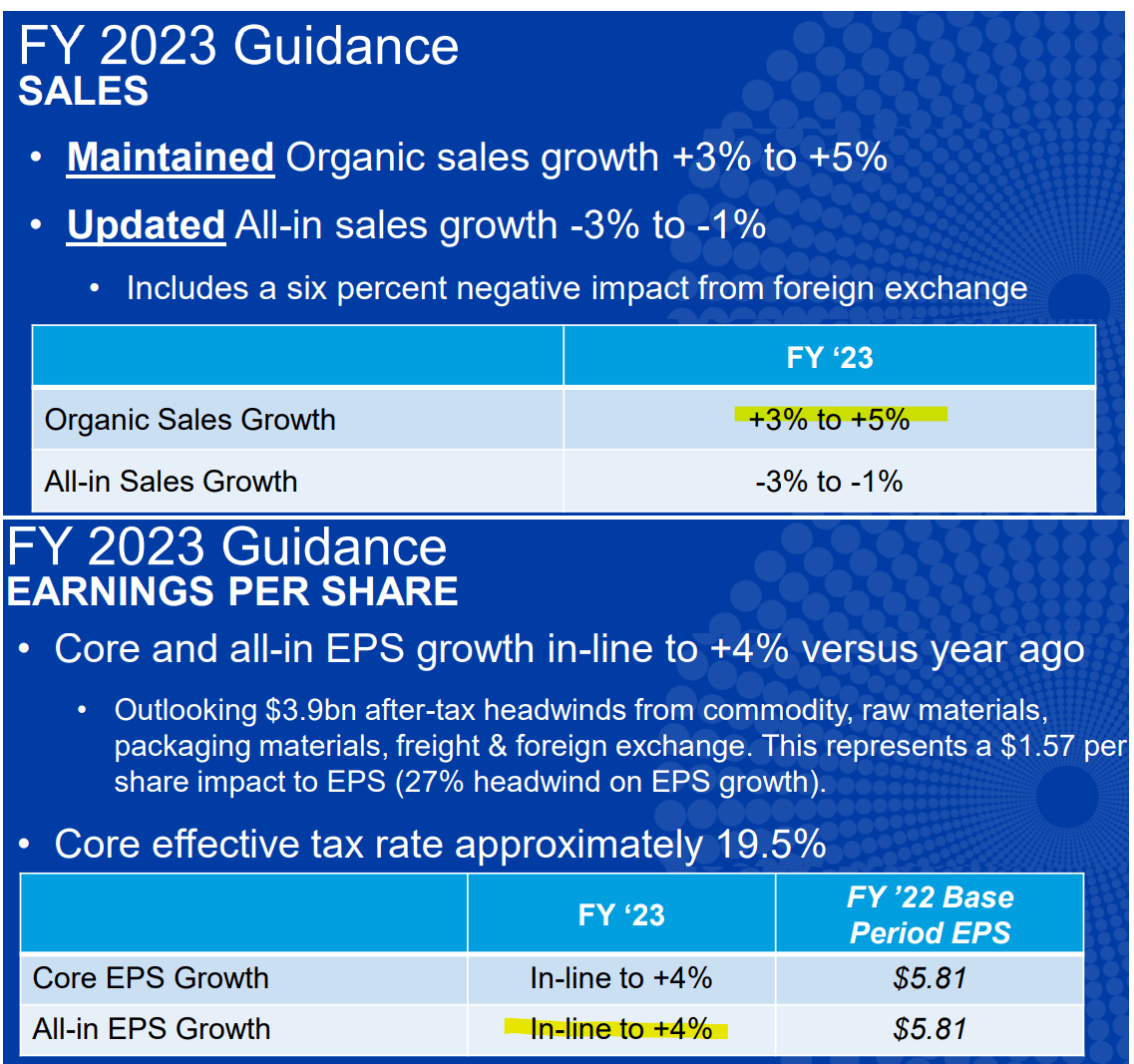

In terms of guidance, the update from last quarter was an adjusted to the full-year 2023 all-in sales target, now expecting a decline between -3% to -1% based on a six percent negative impact from FX citing the strong Dollar and its impact to sales in foreign currencies.

Again, the more important point in our opinion is that the “organic sales” estimate was maintained, forecasting growth between +3% and +5%. Similarly, the company also sees EPS climbing 4% from fiscal 2022 from normalizing margins.

source: company IR

We bring this up because a developing theme in the market in the period since the Q1 report has been a sharp correction in the Dollar, pulling back from multi-decade highs against a basket of currencies. The trend has been driven by signs of slowing inflation both in the U.S. and globally, opening the door for stabilizing interest rates which had driven Dollar strength previously. The result here suggests that PG may be better positioned to either hit the top range of those estimates or even outperform expectations.

There are ancillary benefits here as the inflation cools and the Dollar falls considering a view that consumer spending internationally gets a lift with improving sentiment. In other words, while the macro picture is still complicated, conditions for PG may have progressed compared to what was a weaker baseline just a few months ago.

source: finviz

Is PG Stock Expensive?

Considering the strong rally in shares of PG which curiously started from the lows around the last quarterly report, the sense here is that the market is picking up on what is now operating and financial tailwinds. Easing supply chain disruptions that were a theme at the start of 2022, lower commodity prices and logistical costs, along with the relief as the Dollar drops has represented a new growth and earnings runway.

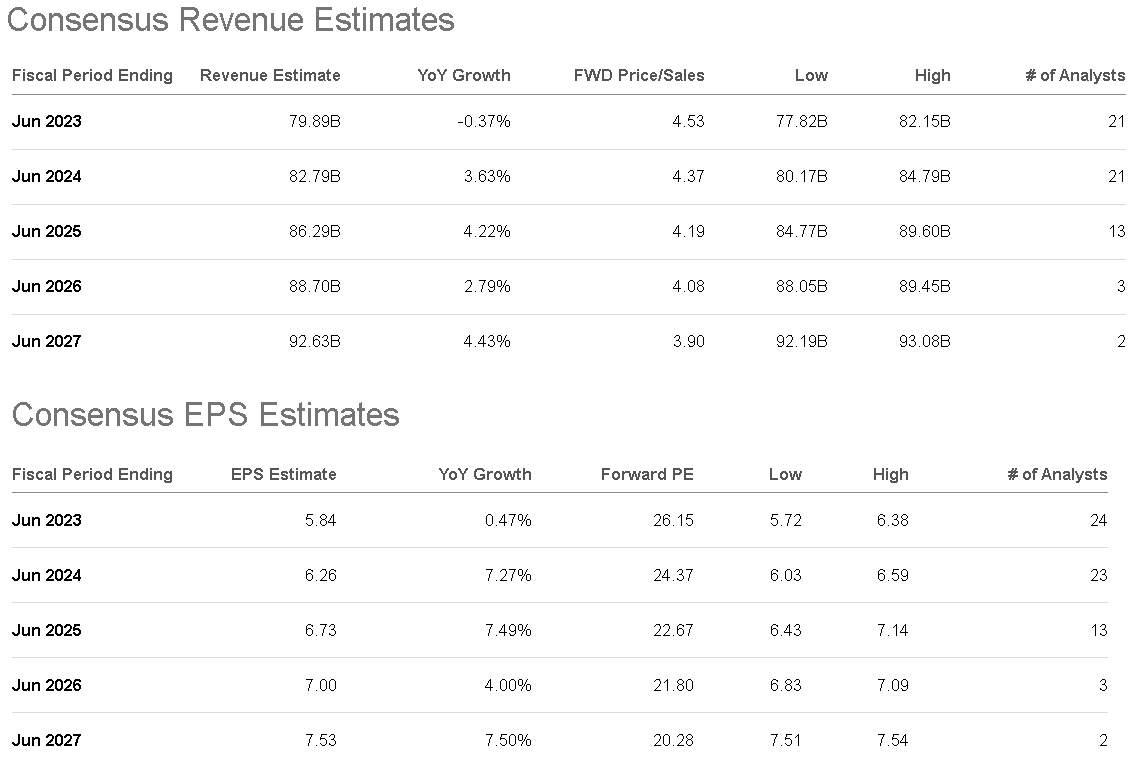

According to consensus estimates, the market is forecasting PG revenue to trend higher at a modest but steady 3% average annual rate over the next five years. For the reasons we touched on above, the outlook for EPS is stronger near 5% over the same period. These levels are also consistent with the company’s long-term guidance. The bullish case for the stock is that there is an upside to these estimates, particularly in a scenario where global economic conditions gain strength.

Seeking Alpha

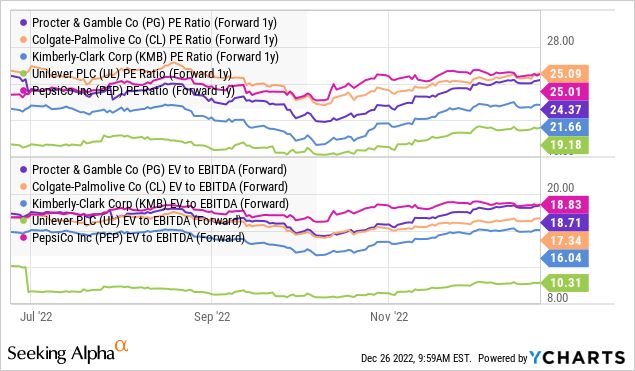

As it relates to valuation, we mentioned PG is typically seen as a “pricey” stock trading at a forward P/E multiple of 26x. Again, this type of premium reflects the company’s sector-leading profitability and history of consistency which makes for a high-quality investment.

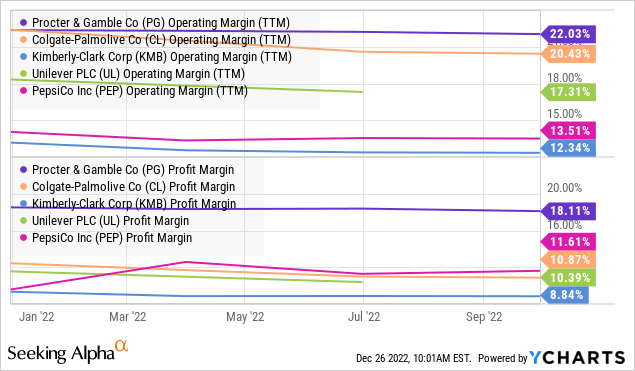

The trend is evident when we look at PG’s operating margin at 22% which is well above the group average for mega-peer household staples peers from companies like Colgate-Palmolive Co (CL), Kimberly-Clark Corp (KMB), Unilever PLC (UL), and even PepsiCo Inc (PEP) as a consumer food staples reference.

PG’s 18% net profit margin is also significantly higher than the 11% for CL, 10% with UL, and 9% for KMB over the past year. A lot of this is based on its operational efficiency and the fact that its customers have shown a willingness to pay up for the quality and brand recognition of PG products. This line draws parallels to how we believe investors should view the stock.

In this regard, it’s fair to say that PG screens favorably next to peers where an argument can be made it deserves an even higher premium. Getting into fiscal 2024, the 1-year forward P/E of 24x remains attractive in our opinion. While PG’s dividend yield at 2.4% is not the highest in the sector, the value here comes down to the combination of long-term growth potential and quality.

PG Stock Price Forecast

We rate PG as a buy with a price target for the year ahead at $170 representing a solid 11% upside from the current level and a 27x multiple on the current consensus fiscal 2024 EPS of $6.26. The takeaway here is that PG remains a reference “blue-chip” with a relatively defensive profile able to navigate across different market conditions.

In a scenario where global macro conditions evolve more positively compared to what is a low base of expectation, PG could find a resurgence of growth making shares appear cheap. In our view, as long as the stock remains above $135, the momentum remains positive with bulls in control.

On the other hand, the risk would be for a more concerning deterioration to the global economy defined by sharply higher unemployment, or a significant rebound of inflation pressures that would undermine the bullish case. Monitoring points over the next few quarters include the trend in operating margins and organic sales growth.

Seeking Alpha

Be the first to comment