Christmas Is Almost Here, So What Is It, Santa or Grinch?

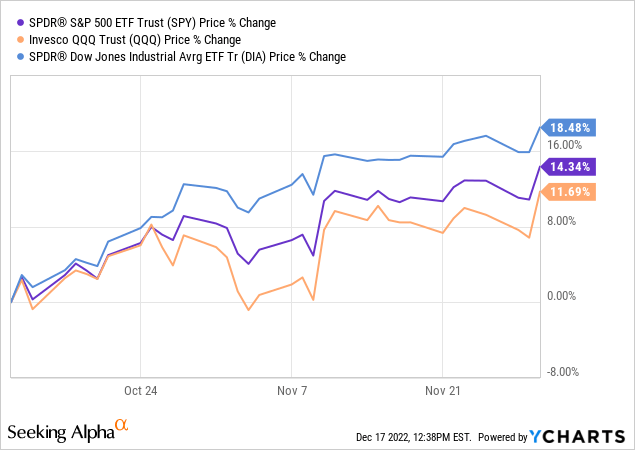

After hitting new lows in mid-October, equity markets were rallying higher (like there’s no tomorrow) up until late-November. On November 30, Mr. Market got extremely excited and rallied ~4-5%+ based on Jerome Powell’s speech at Brookings Institutional due to the tone being less hawkish than before. With the S&P 500 breaking above its bear market trendline resistance, the calls for a Santa Rally started flowing in from everywhere.

YCharts

Honestly, I don’t know where the market is going next, nobody does. We may or may not see a Santa rally this year, but whatever the market does, we are prepared, and our portfolios are positioned to win in 2023. At TQI, we pursue bold, active investing with proactive risk management.

While we don’t try to predict the markets, we do study it. Based on fundamental and technical analysis, I wrote the following excerpt in a TQI marketplace-only article on 26th November 2022:

Since the Fed’s November meeting, the equity markets have been rallying higher, with the S&P500 index (SPX) up ~15.33% off of its recent lows. Another bear market rally or a new bull market? Only time will answer this question; however, I think it is just another bear market rally because the bond market is screaming that a recession is coming (the longer-duration yield is falling rapidly, and the inverted yield curve is getting more and more inverted!). Yes, inflation is showing signs of cooling off; however, I have always believed that the Fed will win sooner or later, and inflation will collapse along with consumer demand. The problem is that the Fed is making a massive policy mistake by tightening into an inverted yield curve. And history shows that every time the Fed makes such a major policy mistake, the economy ends up in a recession (or depression), and honestly, the Fed has been pretty straightforward about the need to cause pain among households and businesses to get inflation under control.

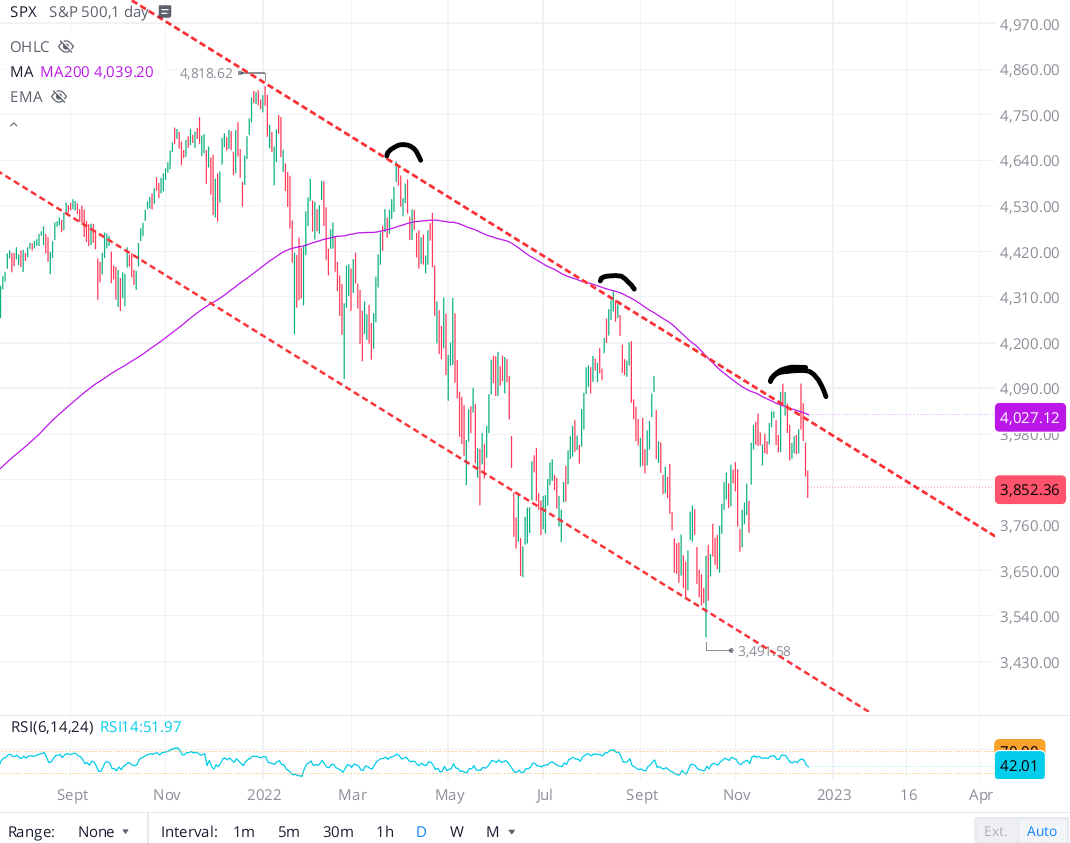

That said, let’s see where the market is right now and what we should be looking at in the coming sessions. As of the close on Friday, SPX is back above the 4,000 level and heading into a resistance zone – 200DMA at ~4050 and falling trendline at ~4100.

WeBull Desktop

As I see it, the ongoing bear market rally in equities (SPX) could have an upside of another 2-3% from here, but then we should see a reversal.

As of the market close on 16th December 2022, the S&P 500 has fallen back into its falling channel pattern (after a false breakout) and re-entered the bear market territory. Clearly, the latest rally in equity markets has been rejected. In the chart below, you can see a clear rejection just below the 4,100 level for SPX.

WeBull Desktop

Now, this is not a victory lap. As an investor/analyst/market strategist, I try to internalize as much data (economic, industry-related, and company-specific data) as possible to generate valuable investing insights for my community members and readers. And I think it is a responsible practice for all investors and analysts to evaluate the outcomes of their calls and stack them up against the logic behind those calls. In my view, this practice is key to investing success.

So, let’s see if my thought process or logic behind the “S&P 500 will form a local top in the 4,100 to 4,150 range” call was sound. While my technical and valuation arguments are purely factual, the economic outlook of inflation collapsing along with consumer demand resulting in a recession is debatable. However, the economic data received so far in December is supporting my thesis.

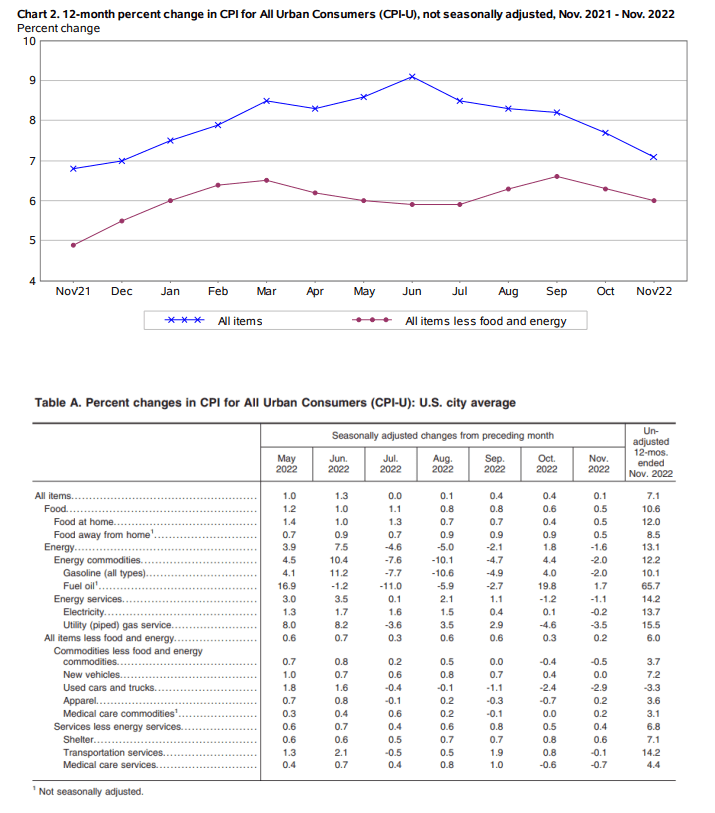

November’s CPI Report Shows Inflation Is Collapsing

bls.gov

bls.gov

In the latest report, US Consumer Price Index [CPI] came in at +7.1% y/y vs. consensus estimates of +7.3% y/y. On a m/m basis, inflation was up just 0.1% (est. 0.3%). Clearly, inflation is falling faster than expected. Furthermore, we know that energy and shelter prices have collapsed already, and the data in this report is not representative of this reality.

In November, the US economy added 263,000 jobs, well ahead of consensus expectations of 200,000. Additionally, unemployment rates remained steady at 3.7%, labor participation declined slightly to 62.1%, and average hourly earnings went up +0.6% m/m (+7.2% annualized). Despite tighter monetary policy from the Fed, the labor market remains tight for now. And a price-wage spiral cannot be ruled out just yet.

Inflation Will Collapse Along With Consumer Demand

In recent weeks, we have been talking about a recession hitting the US in the first half of 2023. Many market participants argue that there will be no recession in the near term because we have record low unemployment and American households still have excess savings of more than $1.5T. However, the Personal Savings rate has dropped below 3%, credit card debts are at record levels, and credit card delinquencies are on the rise (as stated in this SA article).

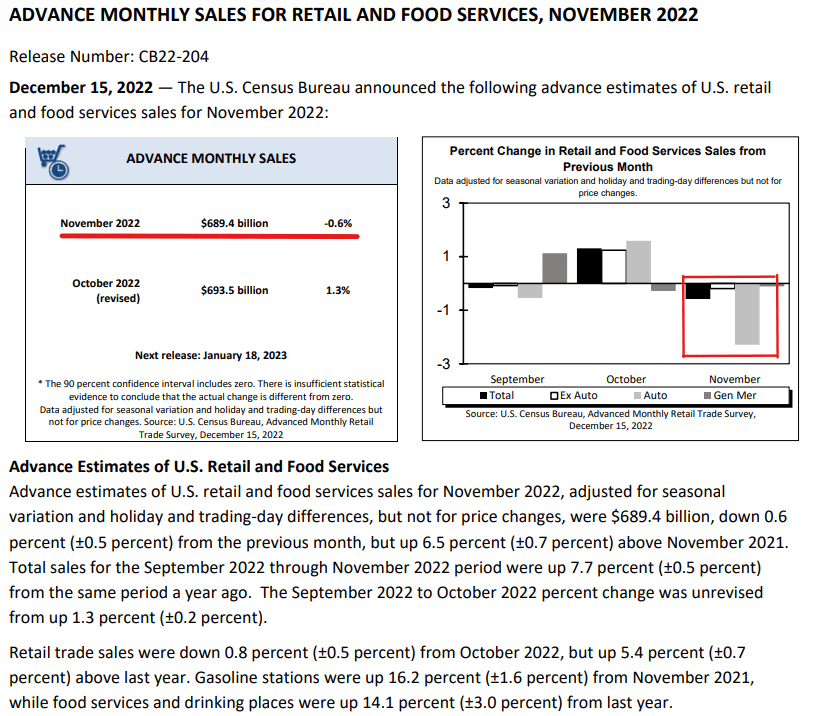

In my view, the low-to-middle income consumer is tapped out because wages have failed to keep up with inflation. And the latest report on U.S. retail sales backs up my view that consumer demand is falling off a cliff along with inflation.

census.gov

In November, US retail sales fell 0.6% m/m vs. estimated decline of 0.1%. This was a shocker, and an indication that consumer demand is breaking.

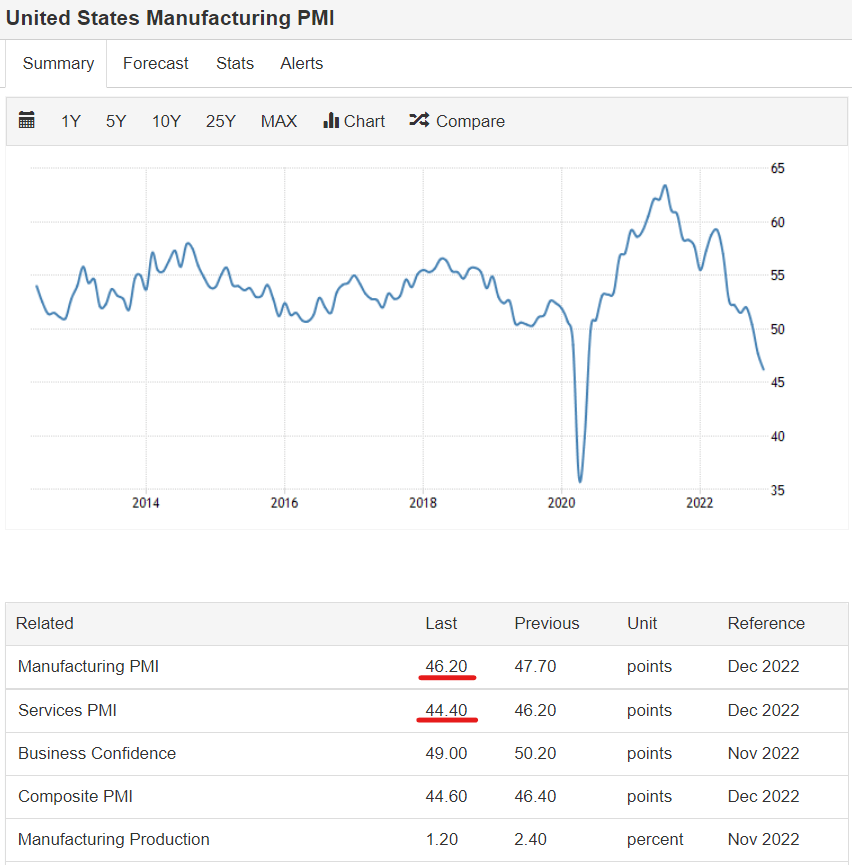

Further, US manufacturing PMI data is also indicative of an impending recession. Based on leading economic indicators, the Conference Board is also forecasting for a recession in 2023.

Trading Economics

Recent US retail sales and manufacturing data are proof of weakening consumer demand. And things are about to get worse, a lot worse. Why? Because the Fed is sleepwalking the American public into a severe recession by tightening into an inverted yield curve.

Here’s an excerpt on this subject from one of TQI’s bi-weekly updates:

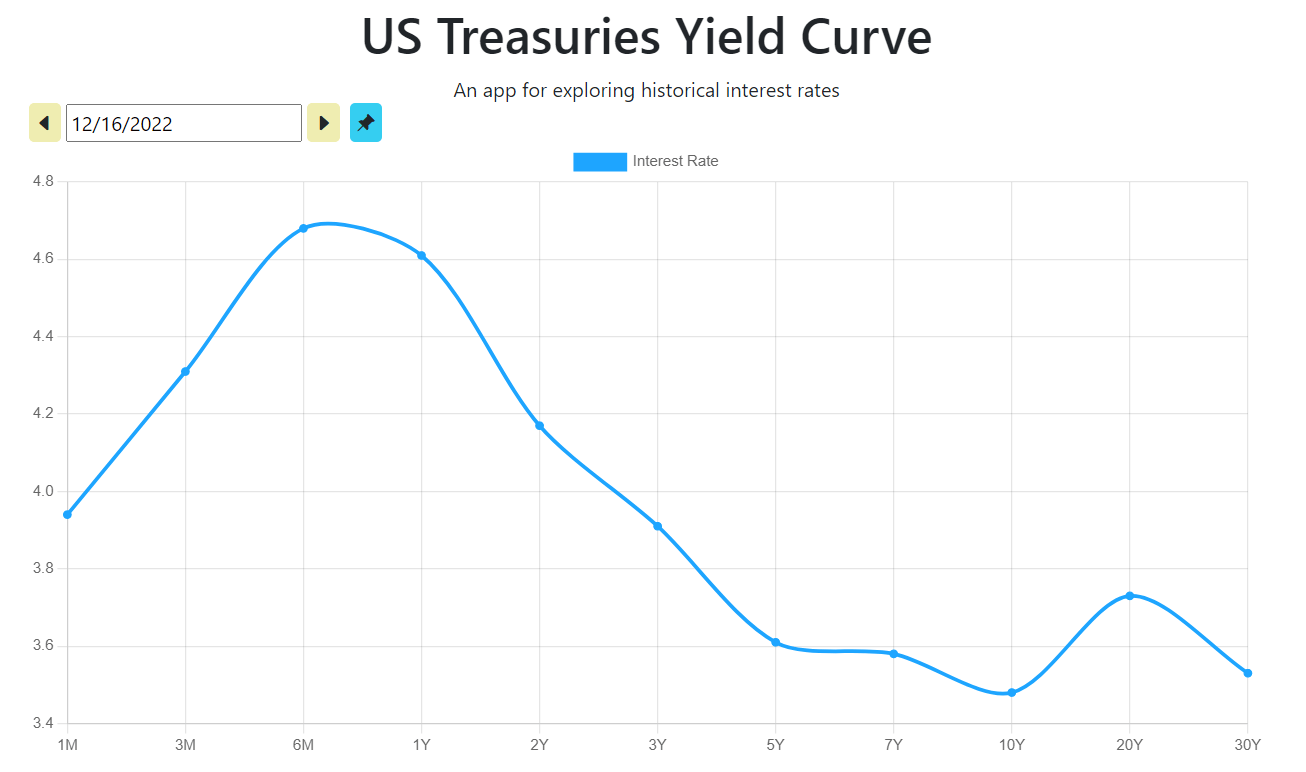

A deeply inverted yield curve has served as a reliable indicator of economic recessions in the past, and a FED-inflicted bust may hit us anytime now. The bond and stock markets are out of sync, and I continue to think that an earnings recession is coming in H1 2023.

US Treasury Yield Curve

In my view, the equity market is getting it all wrong. Investors are currently betting on a goldilocks economy where inflation is falling, wages are rising, and the labor market is robust. While all of this is true, inflation is falling due to recessionary conditions and a declining M2 money supply. Real wage growth is still highly negative, and rising wages could result in a highly-inflationary price-wage spiral. And yes, the labor market is tight; however, the labor participation rate is still in decline, which means the Fed has ways to go.

As I see it, we will likely experience stagflation next year.

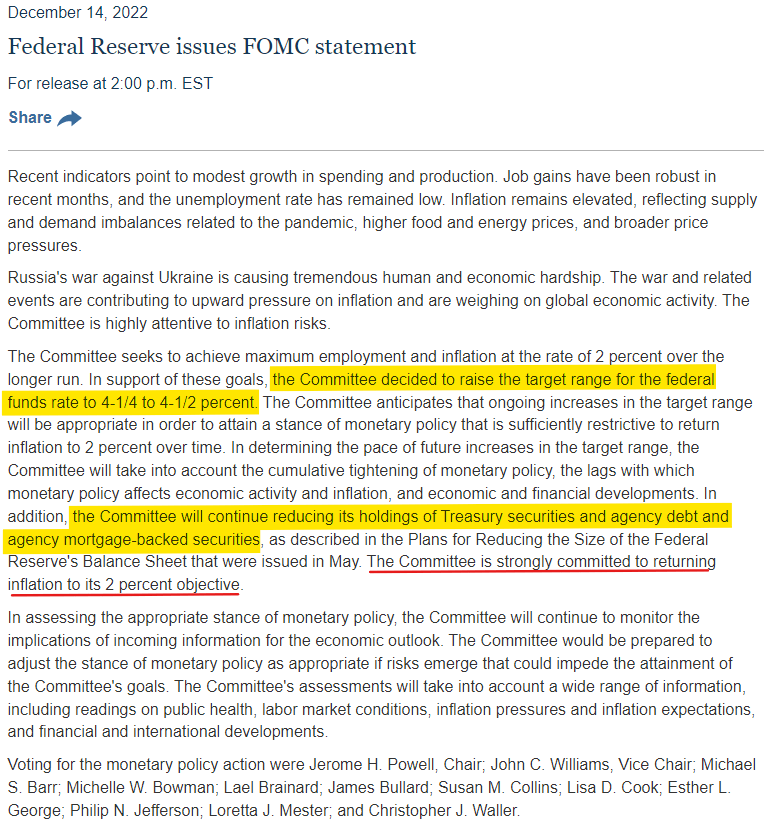

The bond market is screaming “Recession Ahead”, but the Fed is tightening its monetary policy to fight against inflation. In December’s FOMC meeting, the Fed raised federal funds rate by another 50 bps to 4.25-4.5%, and kept its $95B (treasury and mortgage) per month bond run-off (balance sheet reduction program) in place.

FOMC statement 13-14th December

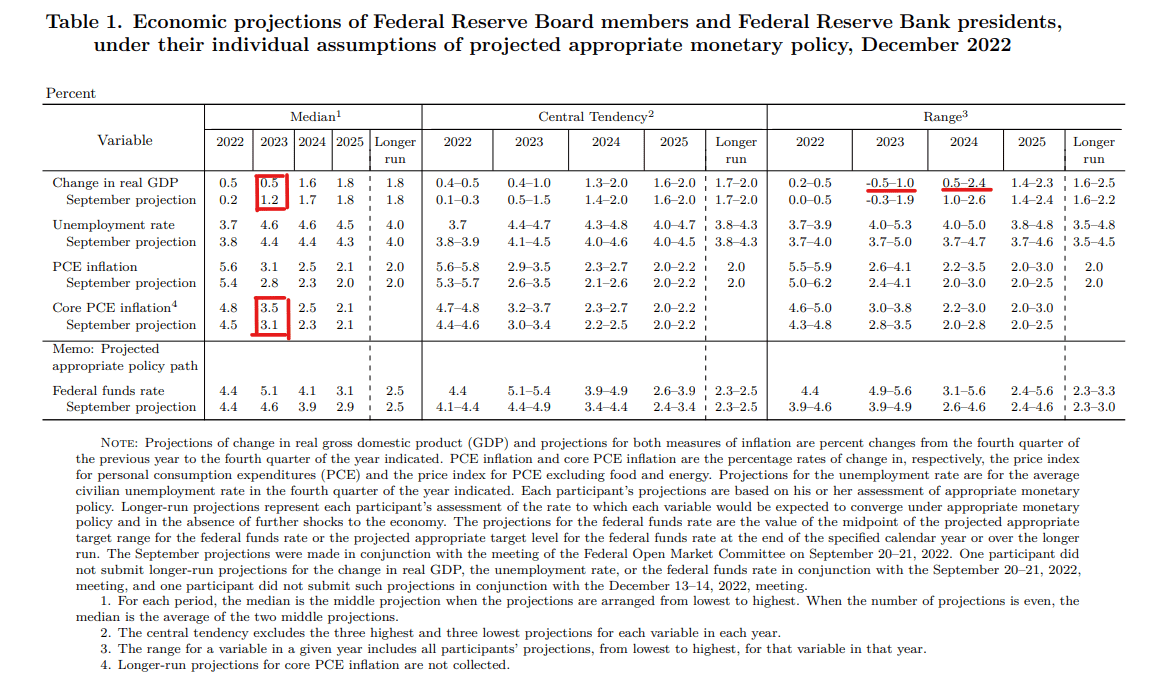

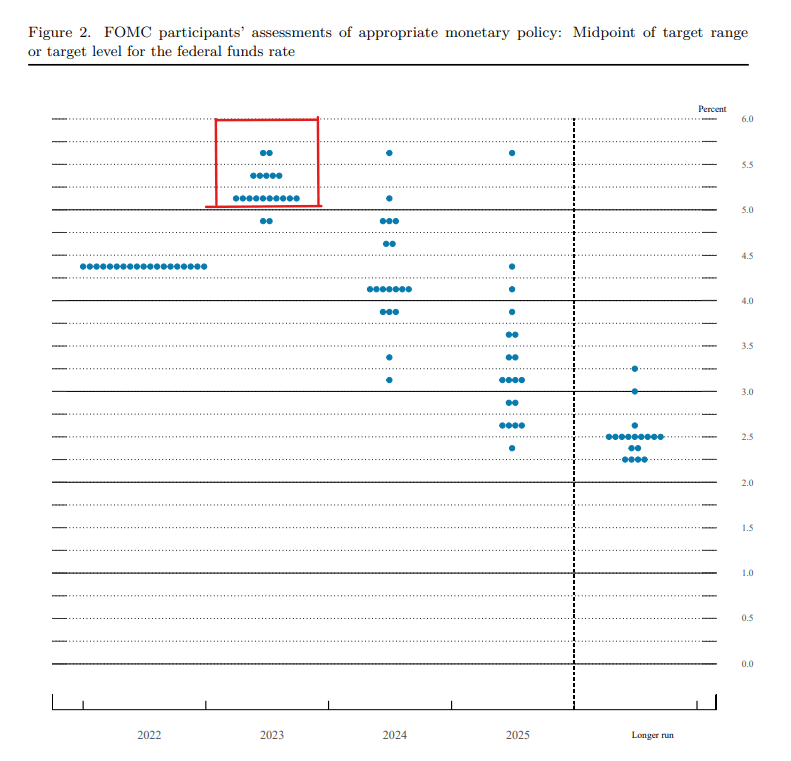

While this monetary policy action was in line with expectations, the details of the Fed’s Summary of Economic projections were shocking. As you can see below, the Fed raised its 2023 core PCE inflation estimate from 3.1% in September to 3.5% in December, and reduced its GDP growth estimate for 2023 from 1.2% to 0.5%. In my view, the Fed just predicted a recession without admitting to doing so.

Summary of Economic Projections Dec 14th 2022

This data suggests the Fed sees an economic slowdown ahead. And yet, the Fed’s terminal fed funds rate outlook has been raised to 5.1% with 17 out of 19 members supporting a terminal rate above 5%. Moreover, the Fed now expects to hold rates higher for longer!

Summary of Economic Projections Dec 14th 2022

The inverted yield curve suggests that the bond market expects the Fed to pivot by first half of 2023, and cut rates in the second half of next year. And a pivot happens only if something breaks in the economy. This is why I keep saying that the bond market is seeing a recession, and in today’s note we have seen a lot of evidence that supports this view. Now, I don’t know if (or when) the Fed will cave or the bond yields will move back up to meet the Fed, but history suggests that the bond market tends to lead the Fed.

On 14th December 2022, I shared the following commentary in a Seeking Alpha news report:

The Federal Reserve’s decision to reduce the pace of rate hikes to 50bps marks the beginning of the end of this rate hike cycle. However, a reduction in pace of rate hikes is not a pivot, and the Fed’s quantitative tightening program is likely to continue for the foreseeable future. With the Fed tightening into a deeply inverted treasury yield curve, the near-term environment should be risk-off. Hence, equity markets could see increased volatility in upcoming weeks.

The Fed is pulling liquidity out of an overvalued stock market (S&P 500 is trading at ~18.5x forward P/E), and it is fair to say that a financial accident may happen in these conditions. A ~25-50% decline in the S&P 500 from current levels cannot be ruled out, and risk management should take precedence in this environment for all investors.

How Are Markets Reacting?

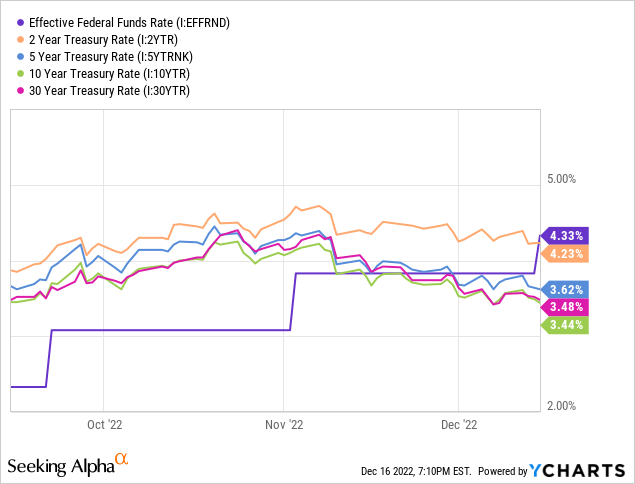

Despite the Fed hiking rates by another 50 bps, treasury bonds yields have continued to decline. In a nutshell, the bond market is fighting the Fed!

But, why? Because, we are likely on the precipice of a recession.

YCharts

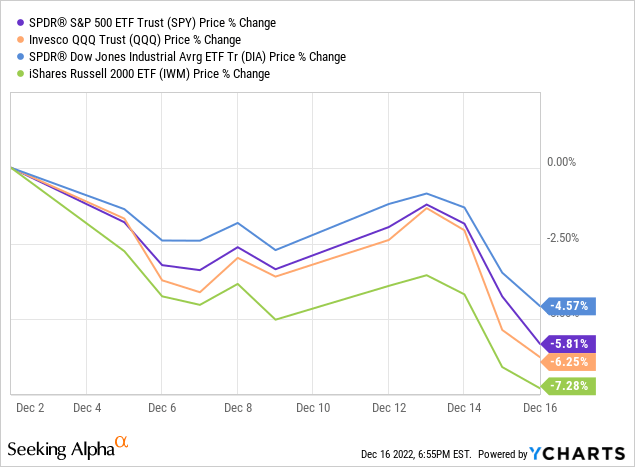

Until recently, equity markets had been rallying higher in hopes of a Fed pivot. A decline in bond yields supported the idea of higher equity valuations, but a pivot from the Fed would happen only if something breaks in the economy. And that is not bullish for equities at all.

YCharts

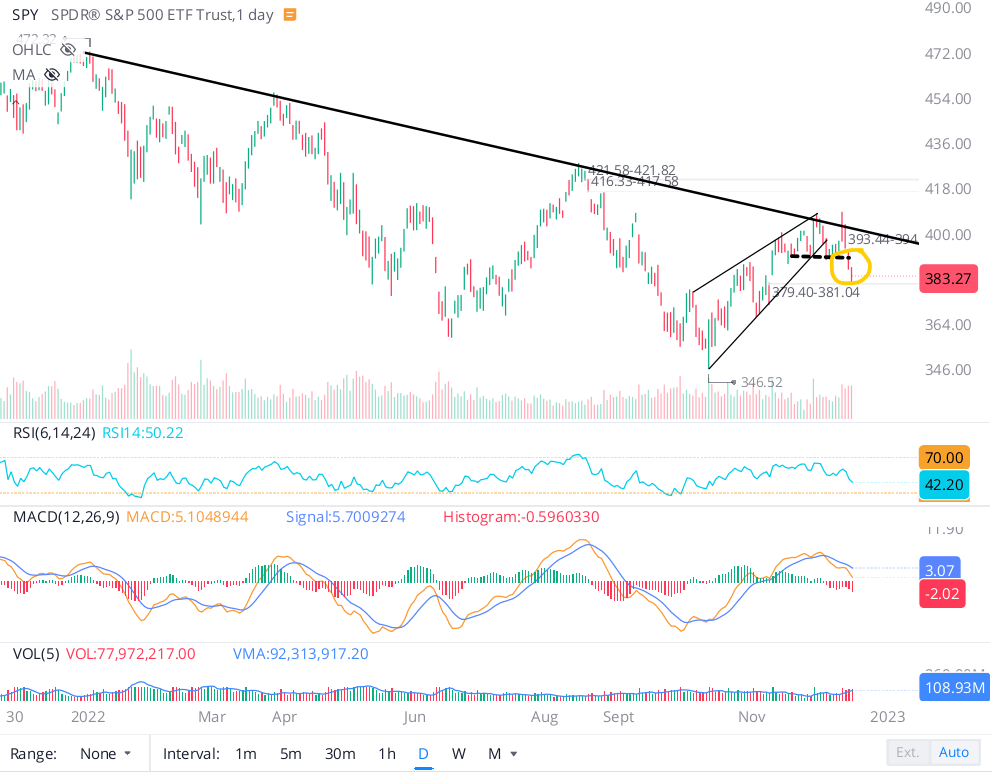

From the latest FOMC and subsequent interview of Jerome Powell, we know that the Fed will continue to tighten monetary policy for the foreseeable future. And the equity market seems to have finally gotten the memo.

Since the FOMC meeting, major equity indices have tumbled lower. Technically, S&P 500 (SPY) has broken a key level at 390, and it could be headed to ~370-375 range in the coming days.

WeBull Desktop

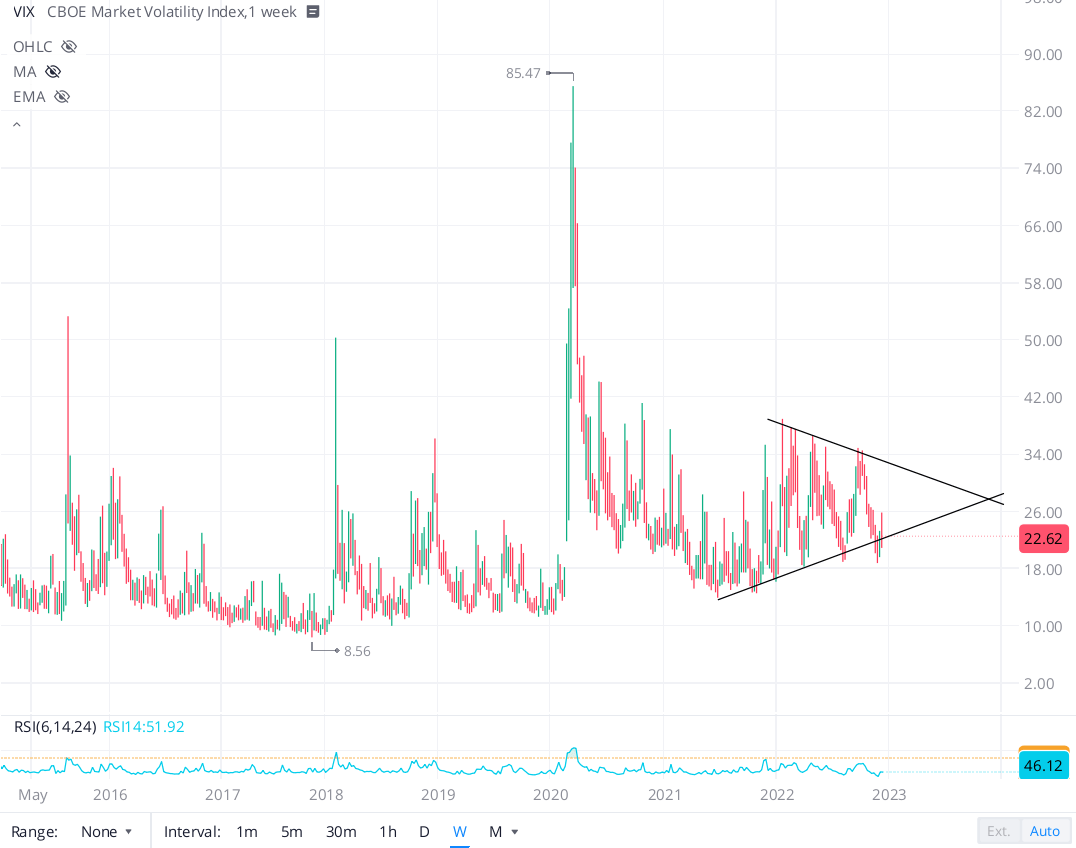

The CBOE market volatility index (VIX) is a gauge of fear for the S&P 500, and this reading is currently sitting in the low 20s, which is not high at all. So far in this bear market, we have seen measured selling, and I think we will continue to see more selling pressure until the VIX climbs back up to the 30s. This level would only be the upper trendline of the symmetric triangle pattern you can see on the VIX’s chart below.

WeBull Desktop

A true capitulatory bottom in equities is often marked with a 45+ reading on the VIX, and I don’t think this bear market will end without such a capitulation. However, if we do get the VIX back above 30, I would look to selectively add to our equity exposure at TQI.

At my marketplace service, we were on a buying hiatus over the last couple of months, and I believe we sat out a classic bear market rally. Last week, we resumed buying under our DCA plans; however, we are still accumulating tactical hedges to guard our portfolios against a potential ~25-50% market crash from current levels, and the net positioning for last week’s trading activity within our core portfolios was “net short”.

Final Thoughts

Looking at last week’s market action, I opine that we were in just another bear market rally during mid-October to late-November period. And now that the S&P 500 has broken back into bear territory, I think the market is ready for another leg lower. The Fed is slowing its pace of rate hikes, but it is just a different angle of attack, and not a pivot! Mr. Market is waking up to this reality, and this could mean more volatility for equity markets in 2023.

Key Takeaway: I rate S&P 500 a “Sell” at current levels.

Thank you for reading. Please share your questions, thoughts, and/or concerns in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment