JHVEPhoto/iStock Editorial via Getty Images

I previously noted that Potbelly (NASDAQ:PBPB) had been delivering strong sales growth and expected it to hit the high end ($119 million) of its guidance for revenues in Q4 2022. Potbelly slightly exceeded my expectations and indicated that its Q4 2022 revenues would end up in the $119 million to $120 million range. It also generated an excellent 3% sequential improvement in shop-level margins from Q3 2022 to Q4 2022.

Potbelly appears to be tracking well to reach its 2024 sales targets now, and appears to need a further 4% same-store sales increase from Q4 2022 levels to get there. This appears quite achievable for it to reach. Potbelly is further away from reaching its shop-level margin target, but has progressed faster with that metric than I expected.

Due to its Q4 2022 performance, I am increasing my estimate of Potbelly’s value by $1 to a new range of $7.50 to $8.50 per share. With the nearly 40% share price increase since I looked at Potbelly in early December, I now believe Potbelly is roughly fairly valued.

Q4 2022 Results

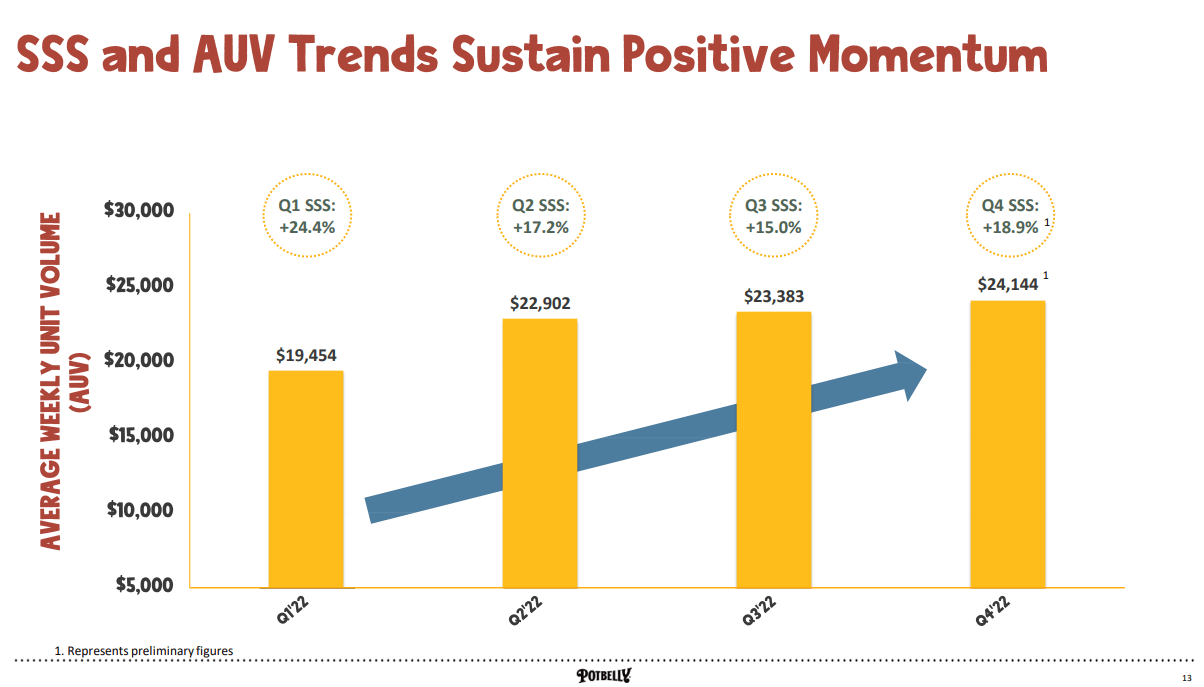

Potbelly reported preliminary Q4 2022 results that were quite strong. It indicated that Q4 revenue was expected to be around $119 million to $120 million, above its guidance range of $114 million to $119 million. It also noted that this translates into same-store sales growth of approximately +18.9%, which is better than its already strong +15% same-store sales growth in Q3 2022. The steady growth in average AUV in 2022 (including +5% AUV growth from Q2 2022 to Q4 2022) shows that Potbelly’s same-store sales growth involves an continuing improvement in sales levels rather than something just driven by an easy year-over-year comparison.

Potbelly’s 2022 Sales By Quarter (potbelly.com)

The strong sales combined with continued cost control efforts also helped boost Potbelly’s shop-level margins to a range of 13.4% to 13.9% in Q4 2022. This was above its guidance range of 10% to 13% for shop-level margins during the quarter.

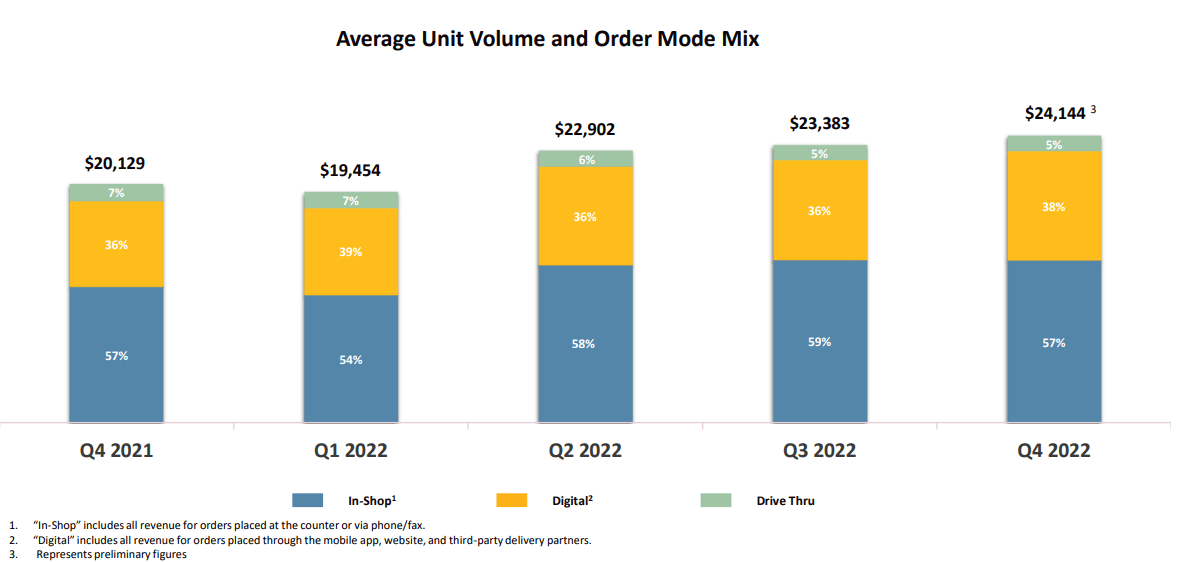

In terms of what is driving growth, Potbelly’s digital sales have been particularly strong. Potbelly launched its new app and website in mid-2021 and digital revenues now account for 38% of total revenues. The estimated mid-20s percent year-over-year digital growth is outpacing its +18.9% same-store sales growth. Potbelly’s apps also have a high 4.8 star rating on the Apple and Google Play stores.

Potbelly’s Order Mix (potbelly.com)

Progress Towards 2024 Targets

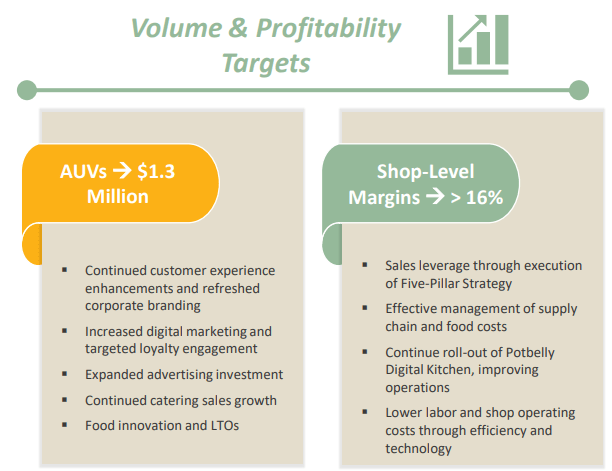

Potbelly appears to be making significant progress towards some of its 2024 targets. It is aiming for AUVs of $1.3 million during 2024. This translates into a weekly AUV of approximately $25,000. Potbelly’s Q4 2022 results involved a weekly AUV of $24,100 to $24,200, so another 4% growth in same-store sales from current levels would get it to its 2024 target for sales.

Potbelly’s 2024 Targets (potbelly.com)

Potbelly is also aiming for 16% shop-level margins for 2024. It is further away from reaching that goal currently (at 13.4% to 13.9% in Q4 2022). However, Potbelly has also made significant progress, with its shop-level margins jumping by around 3% from the 10.6% it reported in Q3 2022.

Valuation Notes

Potbelly looks to be tracking well in terms of revenue and I believe that it can reach its 2024 target of $1.3 million in full-year sales per store. I’ve been more skeptical about Potbelly’s ability to reach 16% shop-level margins before, but it is now much closer to reaching that target. Another 2% to 2.5% increase from Q4 2022 levels would get it there, although the last bit of improvement is often the hardest to achieve.

I am increasing my estimate of Potbelly’s value by $1 to reflect its sales growth slightly exceeding my expectations and its margin improvement performing even better. This gives Potbelly an updated estimated value of around $7.50 to $8.50 per share. This is based on a roughly 4.5x EV/EBITDAX multiple, with Potbelly getting to $1.3 million in annual sales per store, along with approximately 14.5% to 15.5% shop-level margins.

Conclusion

Potbelly has continued its strong run of sales performance, delivering +18.9% same-store sales growth in Q4 2022, while improving its shop-level margins by 3% compared to Q3 2022. It has been successful with its digital initiatives, which have been positively reviewed. Digital revenues now account for around 38% of total sales.

With Potbelly’s excellent Q4 2022 performance, I am increasing its estimated value to a range of $7.50 to $8.50 per share. I believe it is now roughly fairly valued, although continued momentum with sales growth and margins could further increase its value.

Be the first to comment