DjordjeDjurdjevic

Overview

Post Holdings (NYSE:POST) posted better-than-expected earnings and raised its EBITDA forecast for FY23. Although they have both benefited from the temporary uptick in demand for eggs caused by the recent Avian Influenza disruption, underlying performance remains strong. From here on out, I anticipate solid EBITDA and FCF conversion. Both would translate to positive capital returns via de-levering the balance sheet, stock buybacks, and M&As. All in, I believe POST remains a long after this strong set of results.

Earnings update

The $270 million in EBITDA reported by POST for the quarter was higher than the $249 million expected by consensus. The Foodservice division (grew 36.9%) was solely responsible for the quarterly outperformance, as this division continues to reap benefits from the avian flu. In particular, the Foodservice segment EBITDA increased to $109 million on the back of a 4.4% increase in volume, driven largely by rising out-of-home demand trends for eggs and potatoes. Notably, on the call, management not only highlighted the advantages of AI but also stated that the core business had emerged from any covid impacts and was on track to generate $350 million in normalized EBITDA in FY23. In addition, with the company’s new ready-to-drink shake production facility up and running and the growth of its underlying segments, I could easily foresee an EBITDA of more than $350 million in FY24.

When it comes to the Consumer Brands division, I was rather let down because I had anticipated growth in the low teens. The segment grew only high single digits, with the disparity (against my estimates) being largely attributable to falling unit volumes. In spite of the slower growth, it translated to an increase of 4.8% in EBITDA, which was alright in the overall scheme of things.

Sales for Weetabix were down 0.4% as price increases. More importantly, management acknowledged the red flag of supply constraints as a negative influence on the company’s branded business during the quarter.

Finally, sales at refrigerated retailers increased by 7.2% as increased activity in the Side dishes segment and improved promotional activities more than made up for falling sales of eggs. The EBITDA of the segment grew by 12.4%.

Margins

From what I can tell, the rising price of eggs is the primary factor supporting the Foodservice division’s profitability at POST in the near term. Even though POST won’t see similar Avian-focused benefits in the future, there is still a chance for it to recover its pre-covid margins over the near term. I can’t promise they’ll make it next year, but I can say that there is a realistic way for POST to increase margins. For instance: increased productivity, higher prices, and lower raw material costs, can push margins in the positive direction. It’s a similar tale for POST Consumer Brands, whose EBITDA margin is almost 4 percentage points lower than it was before the pandemic.

As a result, despite the increased guidance, I still anticipate healthy EBITDA growth potential thanks to the Foodservice segment’s strong revenue and margin upside potential.

Capital allocation

In addition to the growth of EBITDA, I believe investors can anticipate healthy capital returns. Considering the significant de-levering of the balance sheet over the past few years, I see room for several initiatives: share buybacks, further deleveraging, and inorganic growth via M&A.

Guidance

For FY23, management is now anticipating adjusted EBITDA of $1.025 to $1.065 billion, up from the previous forecast range of $990 million to $1.04 billion. Moreover, the range of expected CAPEX has been reduced to between $275 million and $300 million. Importantly, on the conference call, management stated that they anticipate achieving or exceeding this year’s EBITDA level in FY24, despite the fact that EBITDA this year is inflated by the temporary benefits of AI.

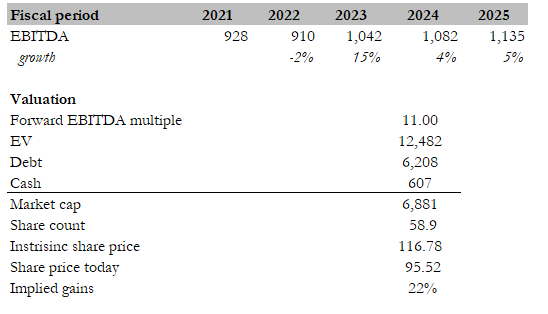

Valuation

POST should continue to post mid-single-digit EBITDA growth, fueled by margin expansion to pre-covid levels. As previously stated, there are several factors at work here that can increase margins: organic price increases, lower raw material prices, improved supply chain (efficiency), and so on. My model also did not account for the potential value addition from M&As, as such EBITDA growth may be greater than I anticipated.

POST is currently trading at 11x forward EBITDA, which is close to its 10-year average, which I believe is reasonable given the expected healthy EBITDA growth and healthier balance sheet compared to the past.

Author’s estimates

Conclusion

POST had a very successful first quarter and increased their forecast thanks to the positive effects of their Foodservice division. I expect the current trend of high egg prices and limited availability to ease, but I still like the longer-term margin recovery story.

Be the first to comment