FrankRamspott/iStock via Getty Images

Introduction

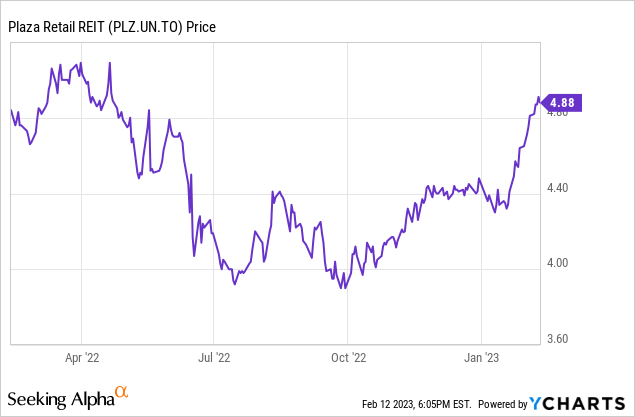

The last time I covered Plaza Retail REIT (TSX:PLZ.UN:CA) (OTC:PAZRF) was in November 2020 when the stock was trading at just C$3.59. This means the current share price represents a 33% increase compared to the Q4 2020 share price and in the past two years and three months, investors continued to receive the monthly dividend of C$0.0233 per month. This means the total return (on a pre-tax basis) is approximately 55% in about 27 months. Not bad at all. Additionally, I was able to buy the convertible debentures at a double-digit discount during the initial phase of the COVID pandemic, and I expect those debentures to be fully repaid at the end of Q1.

The FFO and AFFO are pretty strong, but the LTV ratio remains relatively high

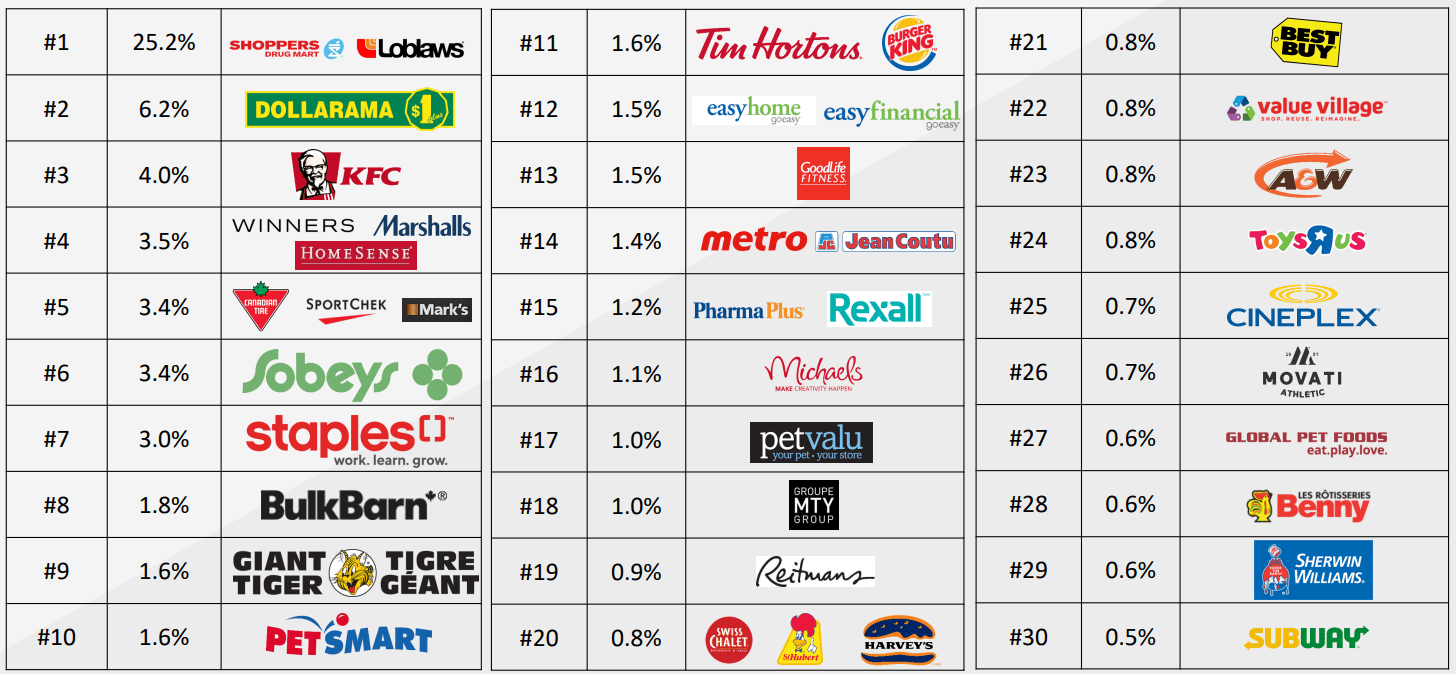

One of the reasons I liked Plaza was its focus on essential services. About a quarter of its rental income is generated from companies under the Loblaws banner. Additionally, 3.4% of the rental income comes from Sobeys with about 1.4% coming from Metro. This means grocery tenants made up 30% of the rent, with pharmacy-focused groups adding to that number.

Plaza Investor Relations

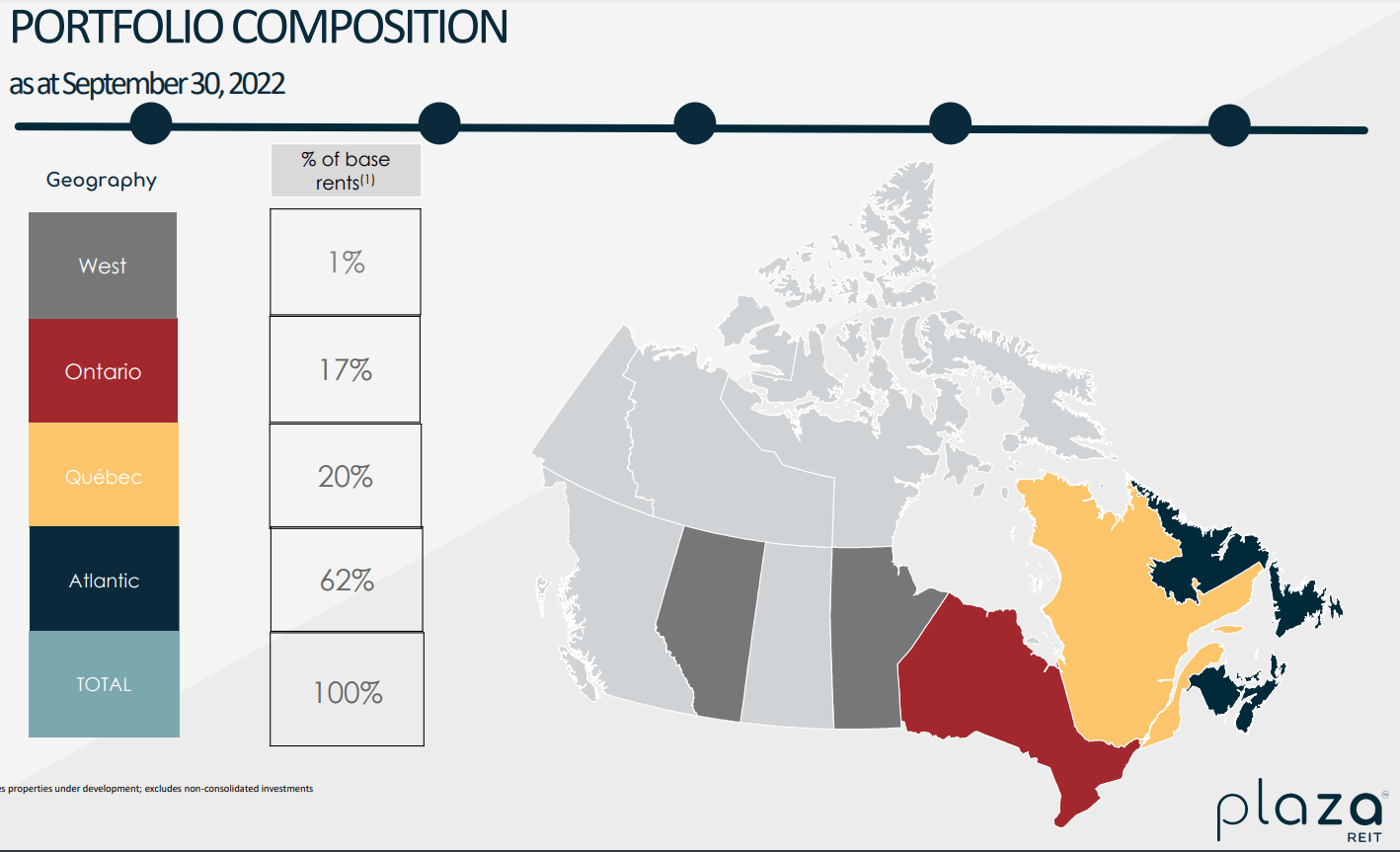

A relatively conservative and reliable tenant basis with a focus on essential services was what attracted me to the name in 2020. From a geographical point of view, Plaza is focused on Canada’s Atlantic provinces.

Plaza Investor Relations

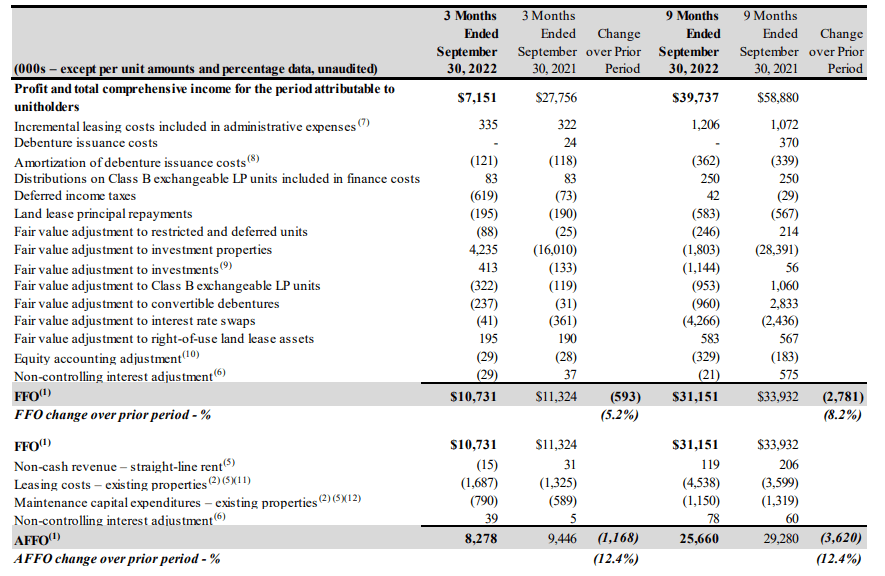

As the FFO and AFFO are the most important metrics for a REIT, I will focus on those elements. Plaza still has to report its full-year financial results, but the Q3 and 9M 2022 results provide a pretty good look under the hood.

During the third quarter of the financial year, Plaza saw its FFO decrease to C$10.7M, which represents approximately C$0.104 per share. That’s nothing to be too worried about, as the FFO in 2021 was boosted by early termination fees. According to Plaza REIT, the FFO per unit would have increased by approximately 2% compared to the results in 2021.

Plaza Investor Relations

The AFFO decreased as well, and as you can see above this was mainly related to the lower FFO on the one hand, and higher leasing costs and maintenance capex (in Q3) on the other hand. This again is nothing to be too alarmed about as the 9M 2021 AFFO was also boosted by the impact from a C$3.1M early termination fee. So you could argue 2021 was exceptionally strong, and we are now falling back on the more ‘normalized’ performance. The AFFO per unit in the third quarter was approximately C$0.08 while the AFFO per unit in the first nine months of 2022 was roughly C$0.249 per share. Unless a major issue pops up, I anticipate the full-year AFFO to come in at around C$0.34 per share.

This also means the current monthly distribution of C$0.0233 is well-covered. Based on my expectation to see an AFFO of C$0.34 per share, the payout ratio is approximately 82%. This means Plaza Retail retains about C$6M per year, which it uses to fund a portion of its development pipeline.

Plaza Investor Relations

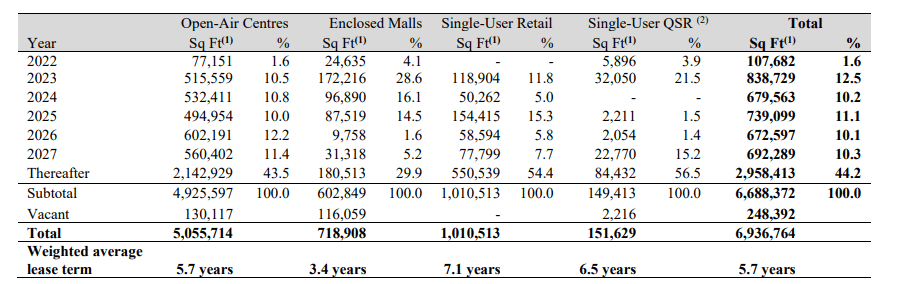

The weighted average lease term of the portfolio is 5.7 years and as most of the debt is fixed term, the increase in interest expenses should be pretty gradual.

Plaza Investor Relations

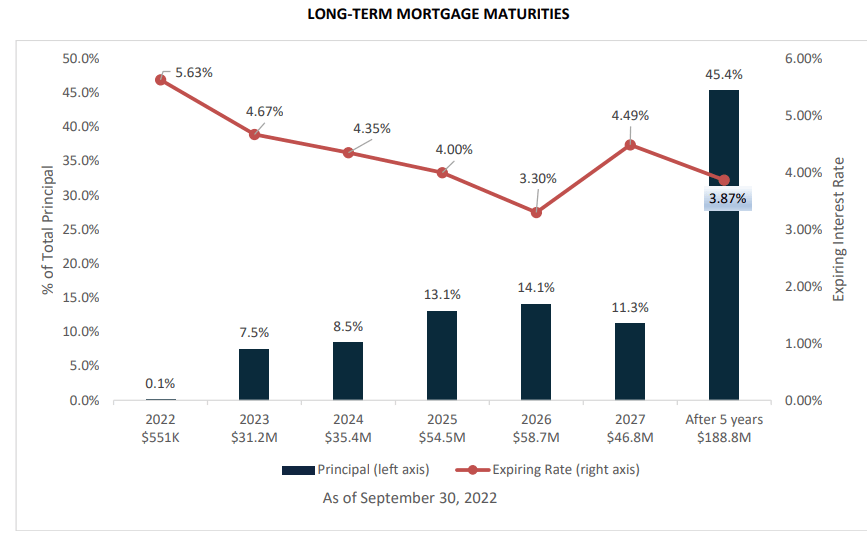

And as the average cost of debt is already in excess of 4%, I don’t anticipate a massive surprise there either.

I expect my convertible debentures to be fully repaid in 6 weeks from now

In this April 2020 article (paywalled), published when the COVID pandemic was still the talk of the town, I already discussed how Plaza Retail’s share price had fallen to approximately 70% of its book value. But more importantly, I zoomed in on the convertible debentures, which were trading at just 87 cents on the Dollar after having fallen as deep as just 70 cents on the dollar.

I argued the risk/reward ratio was pretty attractive. As those debentures are maturing at the end of March of this year, the YTM was approximately 10.6%, which I thought was pretty good for a debt security.

We are now almost three years later, and the debentures will indeed mature soon. No announcements have been made yet (but I expect Plaza will discuss the matter when it publishes its full-year financial results) but considering it is a pretty small issue of just C$47.25M, I do not anticipate any issues. I am hoping the REIT will issue a new debenture available to the general public, but I’m not holding my breath as bank financing might be cheaper.

Investment thesis

As I knew the maturity date of the debentures was coming close, I was contemplating just buying the stock outright. But for some reason, the share price recently moved up by about 15% in just the past month, and I’m not sure I’m willing to pay almost 15 times AFFO for Plaza at this point. Should the share price come back again to the C$4.25-4.30 level, I’d be more inclined to add to my long position in the common shares, but I may have missed my window of opportunity. The debentures are currently – surprisingly – still available just below par, but once I factor in transaction expenses, it’s not exactly worth adding to my debenture position at this point either.

The dividend yield of 5.65% is still attractive for income-focused investors, but I am hoping to add to my position at a slightly lower price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment