Larry French/Getty Images Entertainment

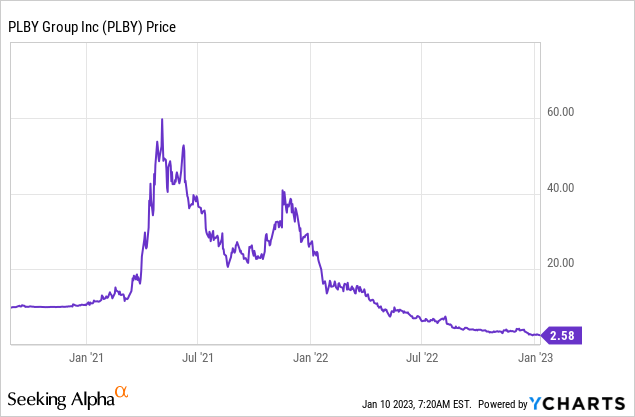

PLBY Group, Inc. (NASDAQ:PLBY) trades at a market cap that implies a market valuation of $120 million. It is a former SPAC that’s down substantially from a much higher valuation. At one point, it ran up to $60/share. Right now, PLBY trades at $2.58 per share and short interest is 31.08%.

Famous value investor David Einhorn has exited the building, and understandably so.

I really liked the vision CEO Ben Kohn laid out at the outlet of repositioning and reinvigorating the brand. A few years ago, it was clear that Playboy was a global brand. A very tired global brand.

Kohn had a lot of interesting ideas to reinvigorate PLBY Group, Inc. that built on the forward-thinking ideas of Playboy in the ’60s and 70’s and brought these value to the 2020’s.

But as an investor, it has been difficult to understand how all the moves Playboy has been making could work to achieve this:

- The company did a string of acquisitions Like Honey Birdette. Which is a lingerie company that’s probably pretty cool.

- It paid $235 million in cash and $2 million Playboy shares there worth at least ~$40 million at that point.

- October 18 2021, it acquired the social content platform Dream. Rebranded it to Centerfold. I think it is positioned as a more chic version of OnlyFans. Fortunately, the acquisition was financed through shares which were then in the $30-$40 range and the purchase price was “only” $30 million.

- It also acquired Yandi.com, a lingerie retailer, for an undisclosed amount.

- And the retail chain “Lovers” for $25 million.

- It did something with NFT’s when that was all the rage.

- It partnered with an Indian gaming company.

Playboy also made a few financial moves that individually seem fine but together are headscratchers.

After raising cash through the SPAC on June 10 2021, it sold another 4.7 million shares in the market for ~$46 for roughly $217 million in gross proceeds. This looks like a good move, as the current share price suggests the move was a bit overextended.

Then, May 17, 2022, the company announced a $50 million buyback financed by issuing private preferred stock. This also seems understandable given the stock had been decimated by then.

However, on December 19 2022, the company did a rights offering (at a discount to its stock price) to raise $50 million to repay senior debt and other general corporate purposes…

That gets me to the crux of this article. Shareholders of PLBY Group, Inc. have recently received rights that give them the right to participate in the scheduled rights offering. A rights offering is when shares are issued at a price and you can subscribe and get a portion of the shares on offer. Usually, this is done when companies need to raise money, and it is usually done at a discount to the prevailing market price.

When I looked at the summarized info I received through my broker, it said I could subscribe for $3.50 per share. Luckily, I had the experience that usually rights offerings aren’t done at a premium to the current share price. If I could only subscribe for shares at $3.50 each, I’d be happy to pass up the opportunity.

But the rights, in actuality, let you buy shares at $3.50 OR – as the company explains it – at:

eighty-five (85%) percent of the VWAP (as defined below) of a share of our Common Stock for the ten trading day period through and including January 20, 2023. “VWAP” means, for any trading day, the volume-weighted average price of our Common Stock on the Nasdaq Global Market (“Nasdaq”), as reported by Bloomberg L.P. between 9:30 a.m. and 4:00 p.m., Eastern Time, on such date.

With the offer closing on January 20, 2023, that means you can basically use the rights to buy the stock at 85% of the price over the next 10 days. There’s also an over-subscription privilege that lets you buy more shares IF others do not exercise their rights. This is often the case, especially if there are a lot of retail shareholders. If you have a small shareholding, it is barely worth most people’s time to look into the details.

However, if you own PLBY Group, Inc. shares and received rights, I think it is interesting to utilize the rights and subscribe for new shares. You may not want to own additional shares of Playboy and fear it continues to sell off (certainly a possibility). A possible solution could be to sell short an offsetting amount of shares. That way, you more or less lock in the 15% discount over the next 10 days. That results in around 17% upside on the capital exposure (although gross exposure is net zero) over 10 days. The annualized return is obviously ridiculous. I’d also argue it is relatively low risk, as the net exposure is effectively neutral.

It becomes very hard to hedge the position if you use oversubscription rights. This can be very interesting, as even a small PLBY Group, Inc. position may allow you to acquire a lot of discounted shares. The problem is that you will not be sure how many people will subscribe. Given the offer was amended and extended, I lean towards not as many as PLBY Group, Inc. had hoped.

Be the first to comment