stockcam

Thesis

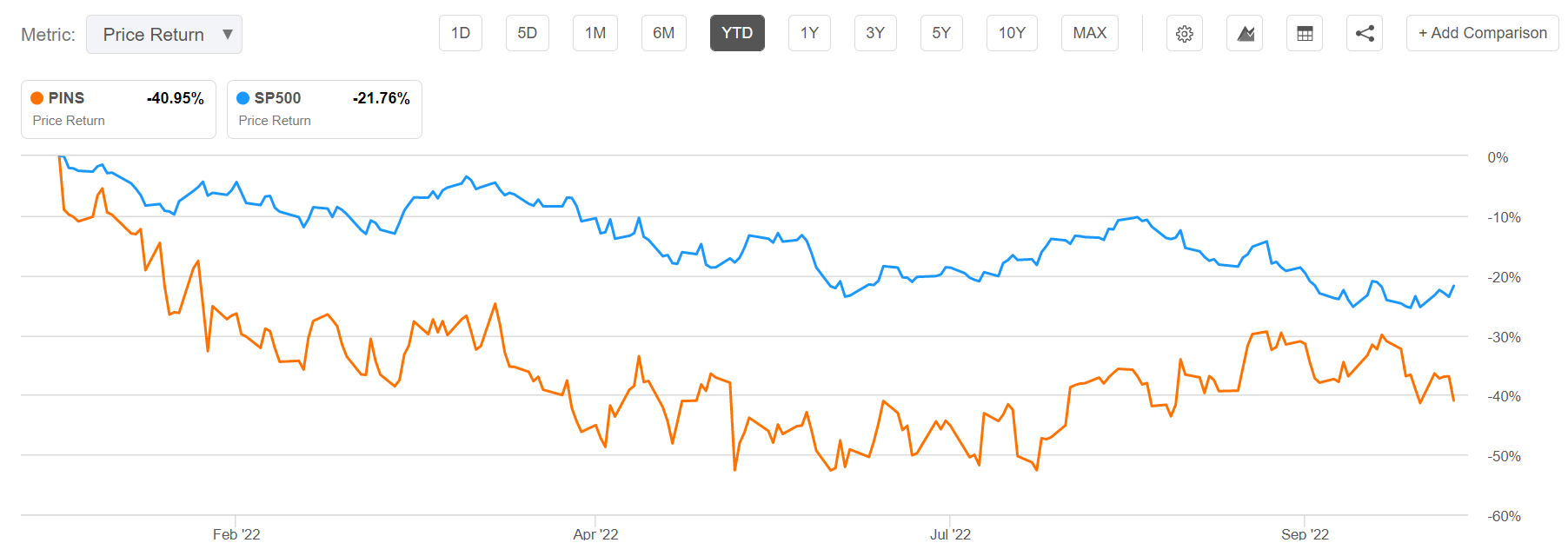

After losing about 65% from all-time highs, Pinterest (NYSE:PINS) stock has traded approximately flat since April. But following a sharp sell-off for Snap Inc. (SNAP) on October 21st, I argue Pinterest stock could soon reprice a leg lower – in line with peers, or lower.

Seeking Alpha

Investors should consider that Pinterest faces multiple challenges: a slowing demand for digital advertising, increasing competition from new social media and entertainment platforms such as TikTok, and lagging technological advantage to compete with the leading digital advertisers, Google (GOOG) and Meta Platforms (META).

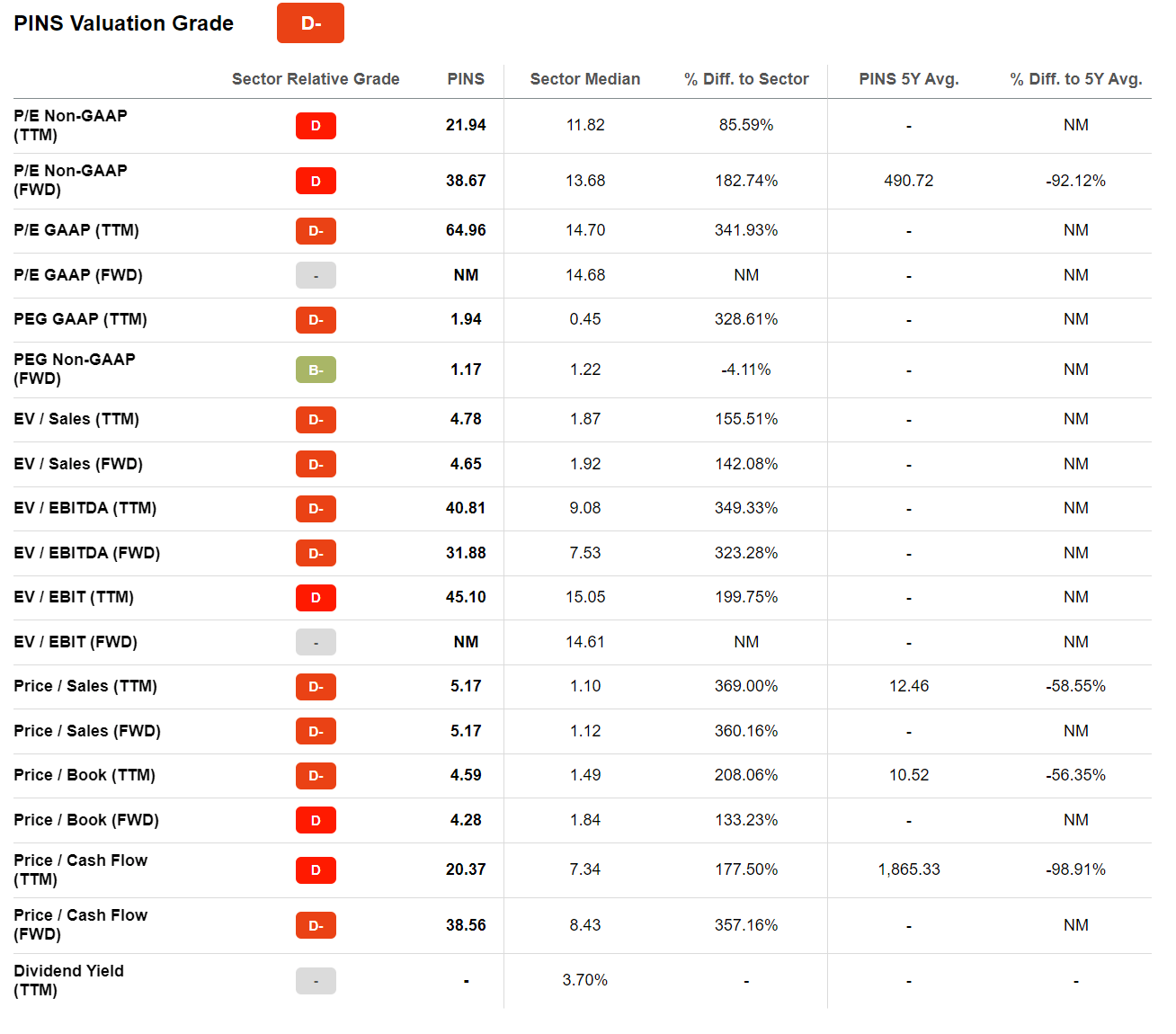

Moreover, Pinterest is also expensive – valued at a one-year forward EV/Sales of x4.65 and an EV/EBIT of x45.

About Pinterest

Pinterest operates a popular global platform, that enables people to discover imagery/content on specific topics using a visual machine learning recommendation algorithm. The Pinterest algorithm also incorporates bits of users’ individual tastes and interests.

Slowing Interest For Pinterest

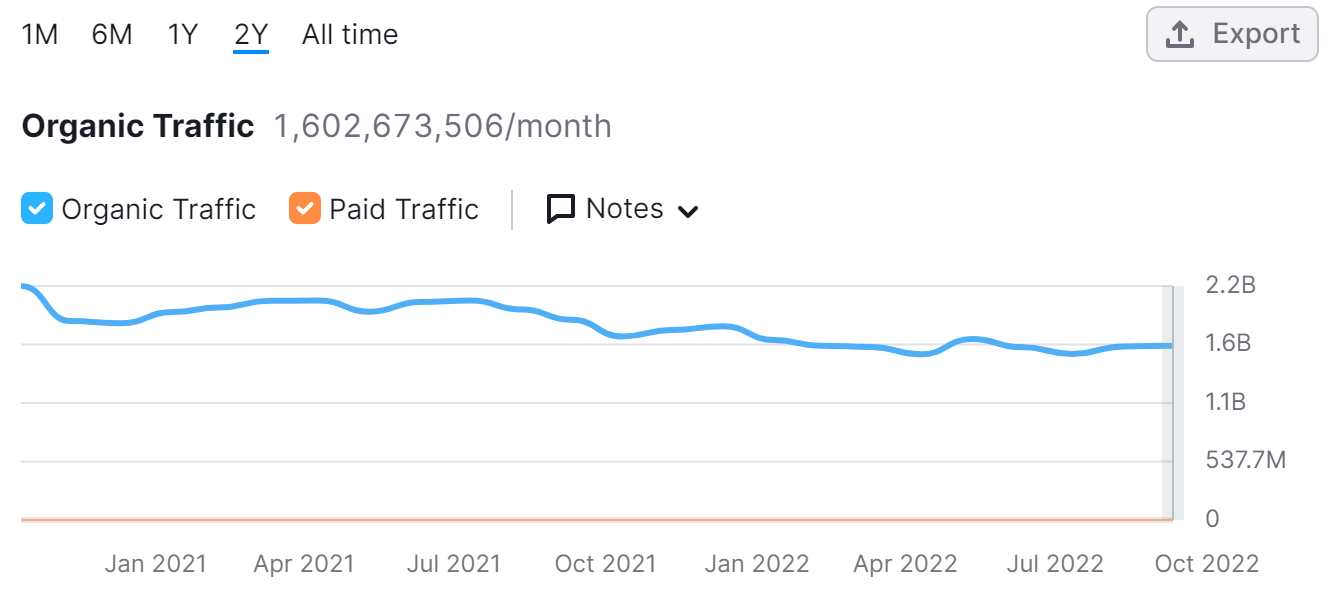

Pinterest’s traffic has steadily declined over the past two years, according to data provided by Semrush. In fact, as compared to late 2020, monthly Pinterest traffic is now almost 30% lower.

Semrush data is somewhat in line with data provided by Pinterest. In Q2 2022, Pinterest said that the platform’s monthly active user base has decreased by about 5% year over year, with a user base contraction of 8% in the U.S. and Canada.

Semrush

Competition Is Fierce

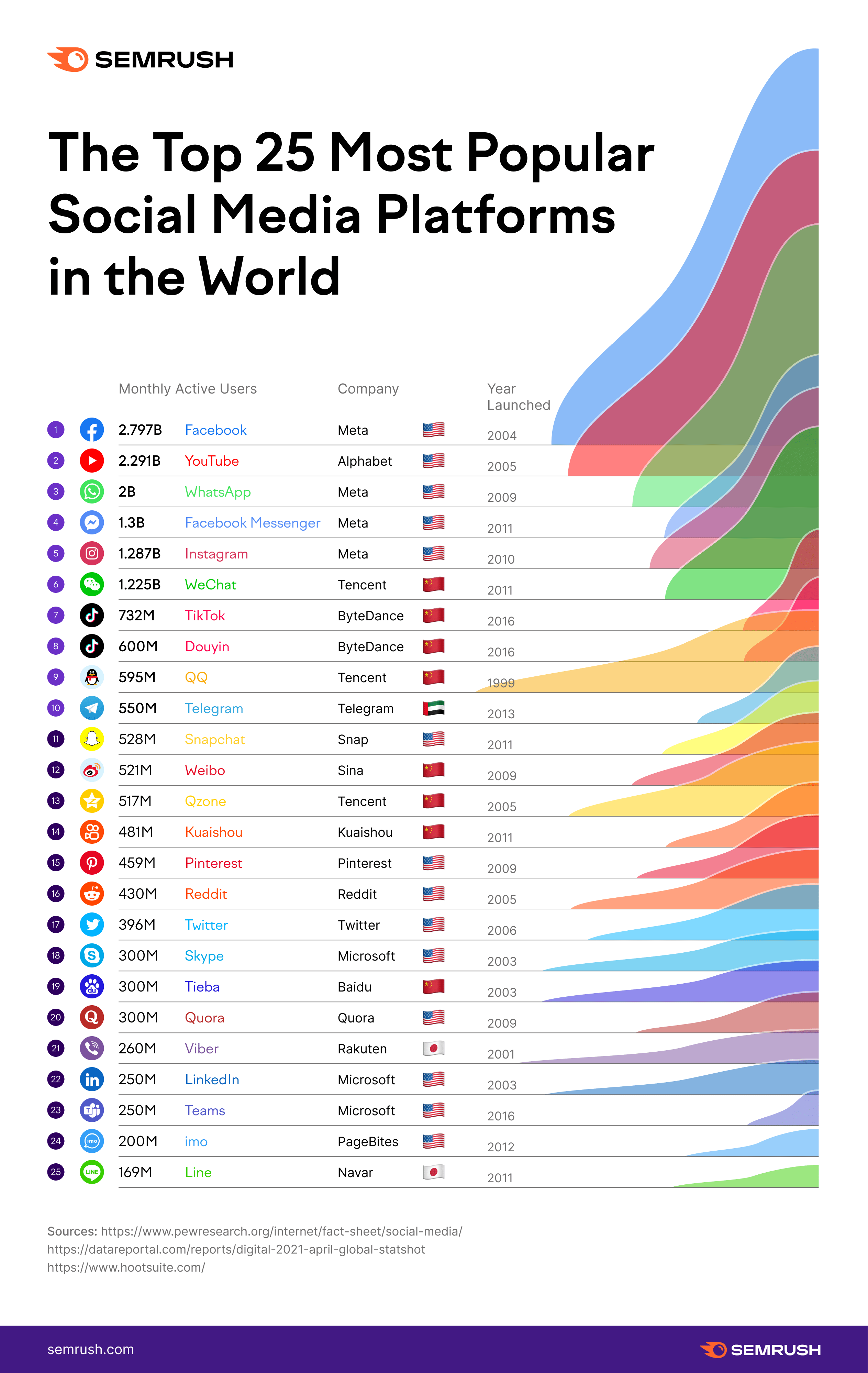

The problem for Pinterest’s declining traffic appears to be company-specific, unfortunately, as other social media platforms such as YouTube, Reddit, Instagram and TikTok accumulate more and more traffic. In an interesting industry report about the social media landscape dated October 2021, Semrush highlights that Pinterest is not among the top 10 most popular social media apps. Competition is simply too fierce.

Semrush

Monetization Fails To Project Confidence

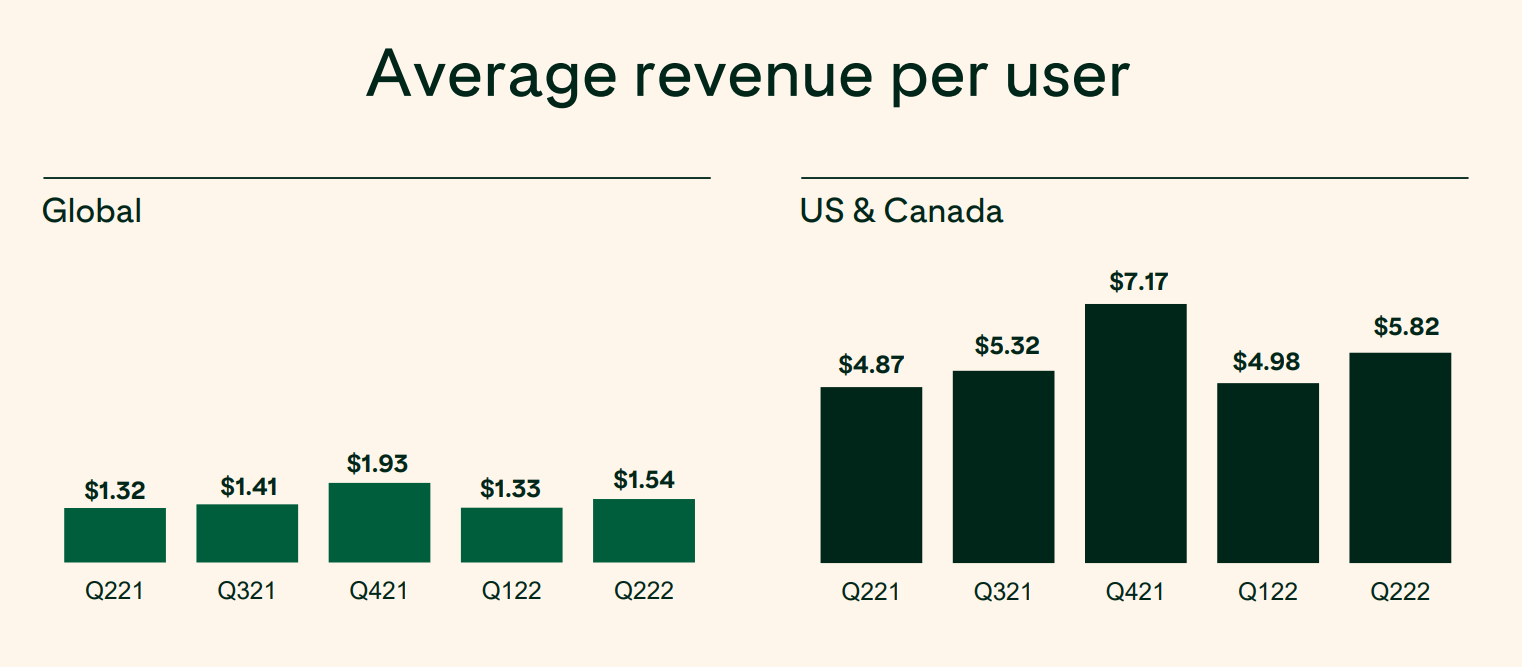

Besides a contracting user base, one of Pinterest’s key struggles, as I see it, is the company’s failure to capture adequate revenue from users. For the June quarter, Pinterest’s monthly average revenue per user (global) was as low as $1.54. This compares to $9.82 for Meta platforms, respectively.

Pinterest Q2 results

Relative Valuation Is Too Stretched

Personally, I don’t believe that Pinterest stock is attractively valued. Investors should consider that PINS currently trades at a one-year forward x4.6 EV/Sales and around x31 EV/EBITDA. This compares to x2.8 and x6.5 for Meta Platforms, respectively.

In my opinion, it is hard to argue that Pinterest should be valued at an x4.6 EV/Sales – especially as the demand for digital advertising is not only slowing, but also increasingly competitive (TikTok, Netflix (NFLX), Snapchat (SNAP), Twitter (TWTR), etc.).

Personally, I also find it hard to justify that PINS stock should trade at a premium valuation to the big FAANG advertising players such as Meta Platforms, Netflix and Google. These players have not only a much more diversified value proposition but also provide a more competitive ROI for advertising dollars (note that most advertising professionals prefer to spend ad dollars spend on Instagram Feed and Google Search as compared to Pinterest – here, here, here, here). And given the HR, financial and technological advantage of the FAANGs, it is hard to see how Pinterest’s algorithms can catch up.

As I have argued for SNAP stock, I believe PINS stock should trade down to about x2 EV/Sales, before the risk/reward becomes attractive for investors. This would imply a downside risk of about 50%, with $10/share as my target price.

Seeking Alpha

Upside Risks

In my opinion, there are three major developments that could justify Pinterest’s current valuation – and perhaps even a higher one.

First, Pinterest might develop new platform features that support new user growth and/or higher user engagement.

Second, Pinterest might succeed in closing the ARPU gap against peers such as Meta Platforms.

Third, as Pinterest’s valuation is falling, the platform might attract interest from a strategic buyer, which might offer a premium to fair value. Reportedly, Pinterest has already attracted interest from PayPal and Google – but so far, speculations regarding a takeover have been denied.

Conclusion

Pinterest stock is expensive – valued at a one-year forward EV/Sales of x4.65 and an EV/EBIT of x45. And following Snap’s a slightly worse-than-expected Q3, it should be clear that such high multiples in the digital advertising space/social media industry are vulnerable to a repricing.

If an investor would like exposure to social media, and/or digital advertising, I argue Meta Platforms is a much better opportunity – given that Meta’s valuation is competitive (in fact, better) and Zuckerberg’s media empire offers a much better growth outlook and monetization potential.

Be the first to comment