naphtalina/iStock via Getty Images

1/17/23 Update:

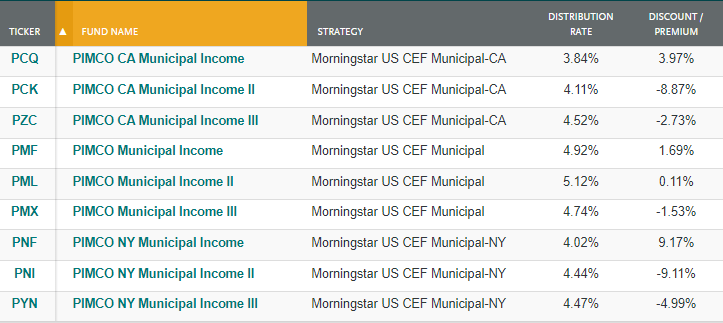

Since our update to members, the muni CEFs have fallen further in price as investors swap out of lower-yielding, leverage CEFs to move into unleveraged vehicles for their exposure.

This is the problem right now with muni CEFs. You are taking on leverage and discount risk – not to mention in many cases, illiquidity – for only a marginal increase in yield.

For example, the yields across the PIMCO muni CEF suite average 4.47%, not far off from the average across all muni CEFs today. The difference is that the valuation or discount/premium is not in the same ballpark as the Nuveen’s and BlackRock’s which are trading around -10% to -12% discounts with similar yields.

cefconnect

I have been buying individual munis with yield-to-worst’s of 3.93% to 4.75% with at least 5 years of call protection and 10-20 years until maturity. Credit quality is investment grade and many of the issues I’ve bought are BBB+ or better and some are even insured. This is what I look for when purchasing the individual bonds.

But I realize that many do not like buying individual bonds – especially individual munis so funds are the only option.

For now, we would avoid the PIMCO muni CEFs as the yields are just too low for the risks.

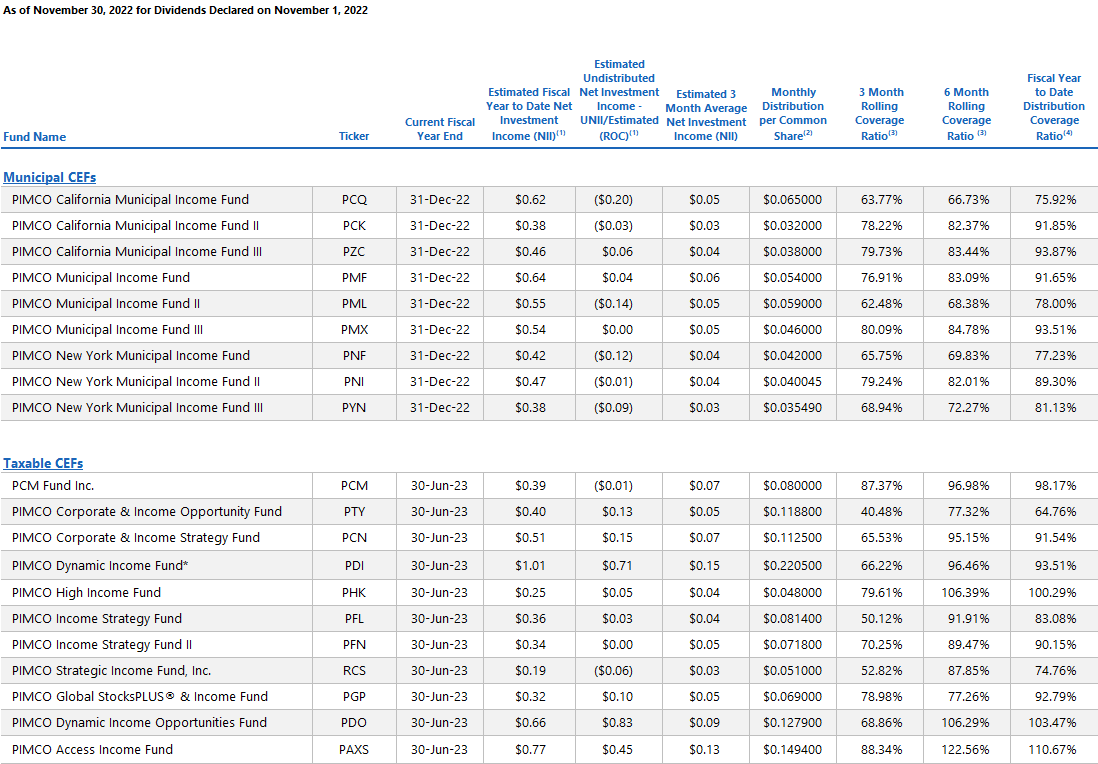

PIMCO UNII Report – December

PIMCO coverage fell precipitously in the last monthly update for November 2022. The drop can be largely attributed to the US dollar falling causing hedges to be marked-to-market lower and reducing net investment income substantially.

pimco

On the muni side, I think Jan 3 will bring significant cuts across the board. You may see PZC and PCK get spares but even that is unlikely. And I’m afraid the cuts could be massive – on the order of 20%-25% or more. That is especially true of PML and PNF, where coverage is in the 60s and UNII is negative double-digits. Those funds will have to slaughter their distributions by as much as 35%.

We would advocate selling any PIMCO muni CEF that you own right now. You can always rebuy after they announce their distributions.

On the taxable side. coverage for PDI and PDO fell from 113% and 136%, respectively, to 66% and 68%, respectively. One would say how in the world could net investment income be cut in half?

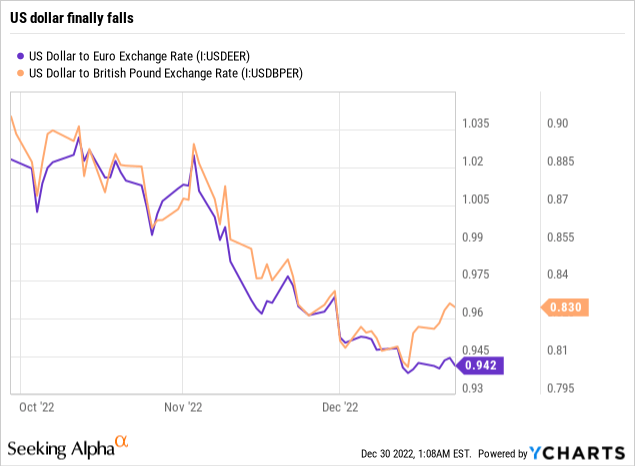

More than 20% of the fund are investments in bonds from outside of the US (14.3% non-USD developed and 6.3% emerging markets [though some of these are denominated in dollars]). PIMCO makes it a point to hedge these back to US dollars so as to not take currency risk on top of the credit risk they are already taking.

Most of their non-USD currency risk comes from the euro and British pound. The dollar for most of the last couple of years has been on a relentless path higher but began falling in October but accelerated in November.

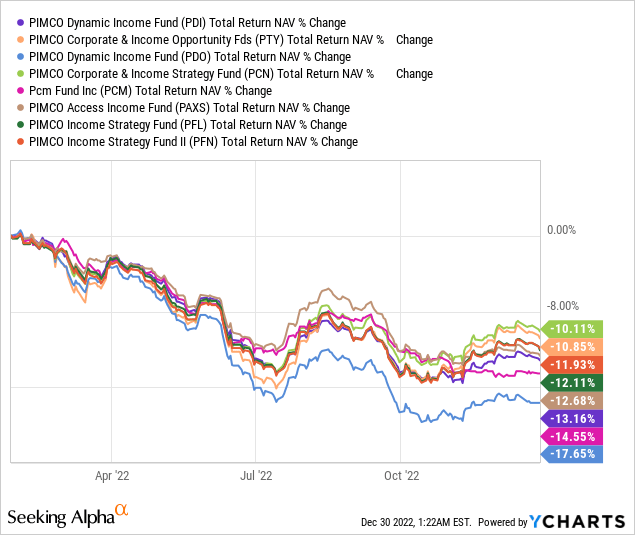

ycharts

Taxable NAVs are down double-digits across the board with PCN doing the best (-10.1%) and PDO doing the worst (-17.6%). PDO fared about 3 points worse than the second worst largely because it is the most different from the others given the start date. It came into being in early 2021 and given valuations of risk assets at the time – having largely recovered from the pandemic – it was forced to have slightly more high yield credits and less in the way of the non-agency mortgages.

Still, most of these funds are very similar with only slight variations.

ychart

The best strategy remains one of rotation from overvalued to undervalued. We made the call to sell PDO at a double-digit premium having bought it at a high single digit discount, on average. The share price ran because of the special distribution amounting to 95c. But the price ran from $14.85 to $15.33 in just 5 trading days offsetting more than half of the special distribution payment.

Since then, the share price has returned to Earth and trades close to fair value around -3% to -4%.

The better deal today is PIMCO Access Income (PAXS) which is trading at a -5% discount and a 12% yield. While that is NOT enough of a difference to swap from PDI or PDO into PAXS, those needing to establish a position in PIMCO taxable should focus on PAXS at the moment.

PIMCO Corp & Inc Opp (PTY) is also closing in on buy territory and should be watched for more weakness for a better entry.

Just remember that distribution announcement day is Tuesday afternoon (around 5pm EST) so we would be cautious about purchasing additional shares ahead of that announcement.

We will continue to highlight rotational and swap trades within the PIMCO suite as they materialize for those that are more tactical and looking to produce alpha through trading strategies.

Summing It All Up

We think there is a lot of risk in the PIMCO funds today – first on the taxable side from much wider credit spreads in 2023 and second on the muni side as valuations reset. That said, once the valuations bottom out on the munis, we think they become a solid buy for taxable accounts. That is especially the case for CA and NY residents who want to buy a single-state muni solution.

On the taxable side, PDO and PAXS remain our funds of choice but they are currently on the more expensive end of their range. We are much closer to sellers rather than buyers of these funds. Valuations remain rich and we think NAVs are at risk from a fall if/when credit spreads blow out.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment