cemagraphics

Thesis

Pioneer High Income Fund (NYSE:PHT) is a fixed income closed end fund. The CEF has current income as its stated goal, and contains a mix of U.S. high yield, International high yield, emerging markets bonds and catastrophe bonds (the fund calls them event-linked bonds). The vehicle is almost fully covering its 9.7% dividend yield now and has performed fairly robustly in the past year. Longer term the fund does not fall in the tier 1 high yield CEF category, but can be a nice play during a market bottom due to its high beta from a discount perspective to risk-off moves.

The vehicle is U.S. high yield centric, but has a multi-asset build, which provides diversification. From that angle we specifically like the catastrophe bonds sleeve, which is a nice diversifying asset class for a high yield vehicle. We continue to rate PHT as a Hold, but it is a fund to keep on one’s radar, given its portfolio diversification characteristics.

Analytics

AUM: $0.2 billion.

Sharpe Ratio: 0.13 (5Y).

Std. Deviation: 15 (5Y).

Yield: 9.7%.

Premium/Discount to NAV: -10.2%.

Z-Stat: -0.8.

Leverage Ratio: 31%

Performance

The fund has a robust performance in the past year, but it is a 2nd tier type of fund:

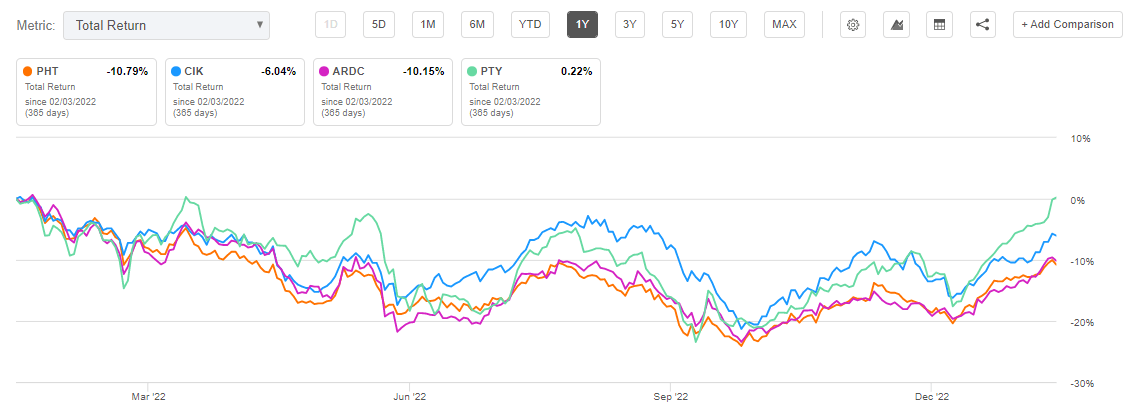

Total Return (Seeking Alpha)

From the above total return performance graph we can observe a clear tiering: on one hand we have premier funds like Credit Suisse Asset Management Income Fund (CIK) and PIMCO Corporate & Income Opportunity Fund (PTY), while in the second tier cohort we find the likes of Pioneer High Income Fund Inc (PHT) and Ares Dynamic Credit Allocation Fund Inc (ARDC).

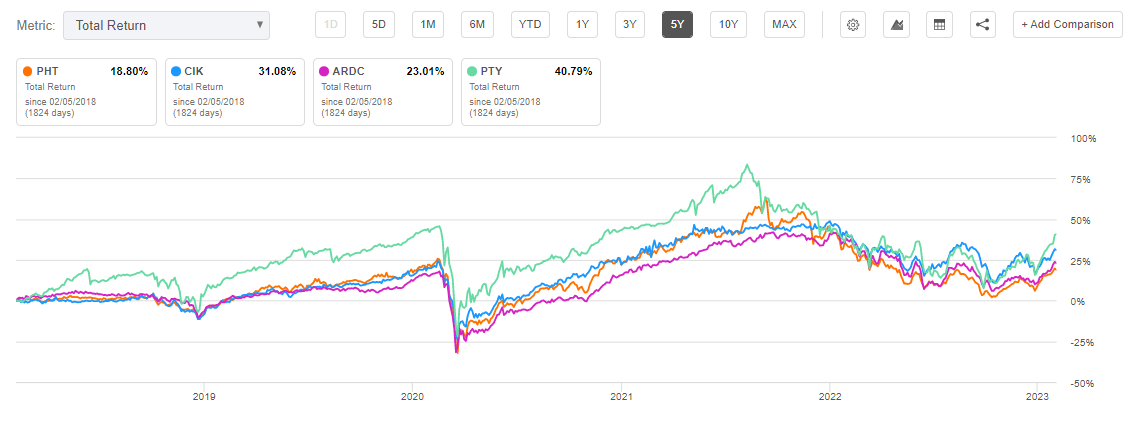

Longer term this tiering holds:

Total Return (Seeking Alpha)

PHT might not be a cohort 1 high yield CEF, but still performs fairly robustly.

Holdings

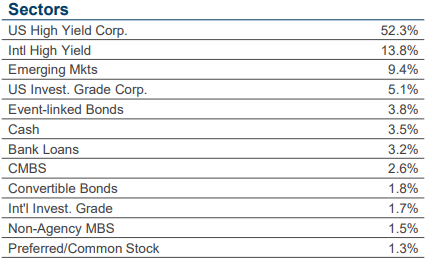

The fund focuses on high yield holdings:

Sectors (Fund Fact Sheet)

To note that the vehicle has a global approach, with sleeves dedicated to international high yield and emerging markets bonds. Also interesting to note is that the fund has catastrophe bonds in its composition (called ‘Event-linked Bonds’ here). Cat bonds provide for diversification within a portfolio.

Catastrophe bonds are a form of securities where insurers transfer risk from a catastrophe or natural disaster to investors. Insurers and reinsurers typically issue cat bonds through a special purpose vehicle. Cat bonds pay high interest rates and diversify an investor’s portfolio because natural disasters occur randomly and are not correlated with other economic risks. The incidence of hurricanes and tornadoes is largely unrelated to economic and financial activity. During the great financial crisis of ’08-’09, cat bond prices were virtually unaffected outside of liquidity bid/ask spreads.

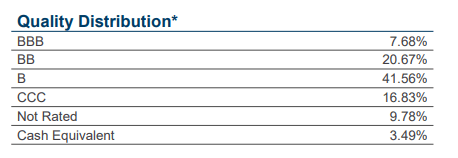

The fund has a middle-of-the-road credit composition:

Ratings (Fund Fact Sheet)

The ‘CCC’ bucket is a bit on the higher side above 10%, but nothing egregious. The multi credit asset build allows for diversification, and we like that approach in this fund.

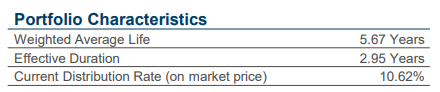

The story is similar when looking at the duration components for the fund:

Characteristics (Fund Fact Sheet)

All the analytics here are in the middle of the cohort from a build perspective, with the fund displaying middle of the cohort numbers.

Distribution

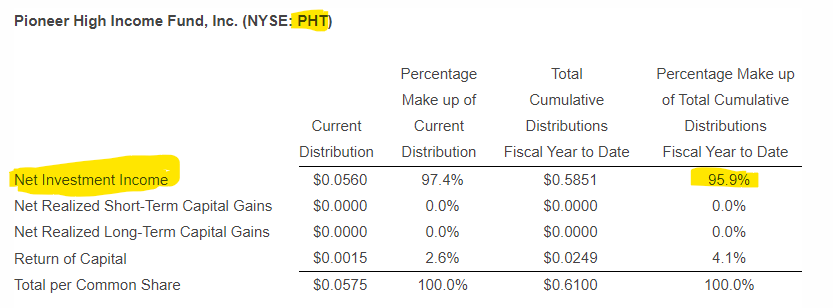

Given the substantial move up in rates and spreads, the fund’s collateral now provides the cash-flows to basically fully cover the dividend:

Distribution (Fund Section 19a)

The move up in all-in yields last year has been nothing short of breathtaking. Its result is an almost full coverage of dividend yields for many well-run high yield CEFs. It is important to ensure that dividend yields are covered when rates are at the highs. If not now, when will a fund actually be able to cover its distribution?

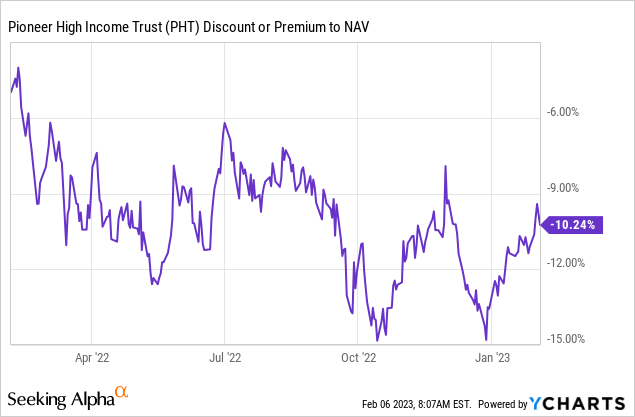

Premium/Discount to NAV

The CEF’s discount to net asset value has narrowed substantially with the market risk-on rally:

The fund has a high beta to risk-on / risk-off market set-ups. We can observe the high correlation between the discount to NAV and the wider market sentiment. This is one of those funds which when bought around a market bottom will provide another 10% tailwind from the discount to NAV narrowing.

Conclusion

PHT is a fixed income closed end fund. The vehicle is U.S. centric, but contains international high yield, emerging market debt and catastrophe bonds. The fund has had a robust performance in the past year, but it falls in a second tier when compared to premier CEFs such as CIK and PTY. With the substantial rise in all-in yields, the fund is now almost fully covering its 9.7% dividend yield. The vehicle tends to trade at a discount to NAV, and its discount has a high beta to market risk-off events. The fund is a Hold for now given the current run-up in prices, but it is a nice diversifier to a high yield portfolio to keep on one’s radar screen.

Be the first to comment