shaunl/iStock via Getty Images

Phillips Edison & Company (NASDAQ:PECO) is a multi-tenant retail real estate investment trust (“REIT”) that invests in grocery-anchored shopping centers across the country. This is a very defensive type of property, because around 70% of PECO’s rent derives from necessity-based tenants like grocers, quick service restaurants, medical offices, dollar stores, and pharmacies.

The stock remains fairly inexpensive at a price-to-core FFO of 14.9x based on 2022 core FFO per share of $2.27, or 14.6x based on the midpoint of 2023 core FFO per share guidance of $2.31.

On the other hand, investors would do well to remain disciplined in buying PECO, because this isn’t a high-growth REIT. In 2022, PECO generated core FFO per share growth of 3.7%, and the midpoint of 2023 guidance assumes 1.8% growth for this year.

PECO can be a defensive, modestly leveraged, sleep-well-at-night addition to a dividend growth portfolio, but it’s probably best to buy this one on dips. Thus, the goal of this article will be to show that:

- PECO is a worthy company to own for conservative dividend investors, and

- Investors should be careful not to overpay for it.

As part of the process of trying not to overpay for it, I’ll walk through my own thinking in determining a “buy under” price.

Defensive But Slow-Growing Grocery Landlord

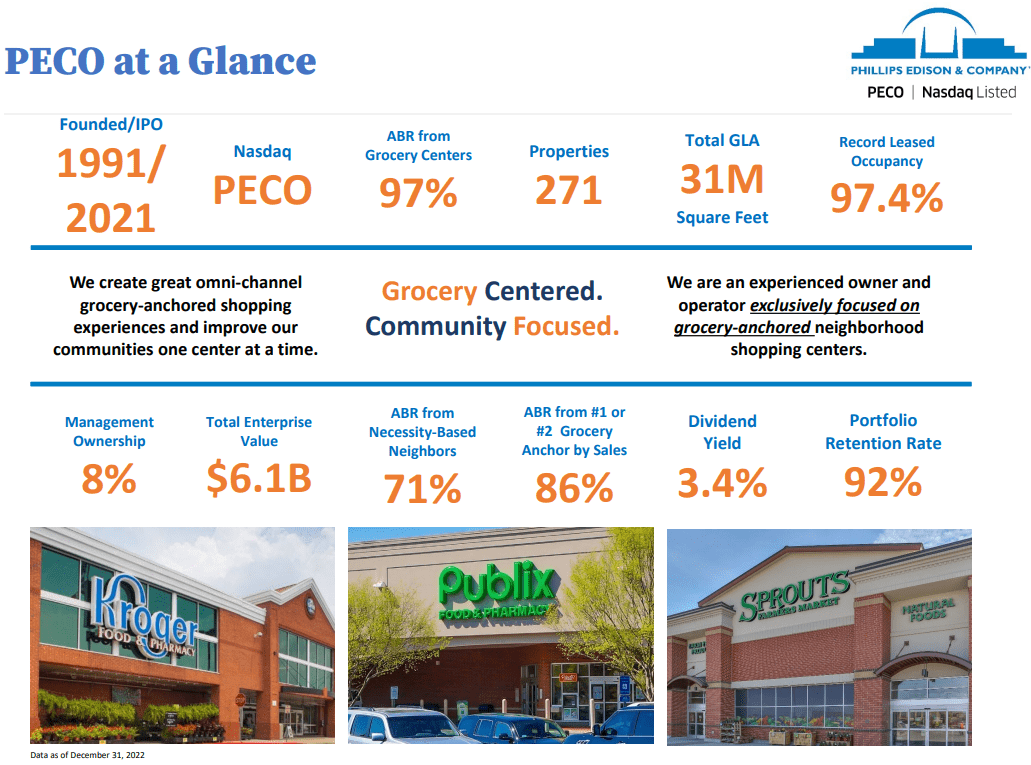

PECO owns 271 shopping centers across 31 states that are overwhelmingly (97%) “omni-channel grocery-anchored.” The point in stating “omnichannel” is to communicate that these are large, national or regional supermarket chains with built-out buy-online and curbside pickup platforms. They aren’t mom & pop grocers, if those even exist anymore.

PECO February Presentation

The portfolio is 97.4% leased (up from 96.3% at the end of 2021) at an average remaining lease term of 4.5 years.

Over 70% of rent comes from “necessity-based” tenants (or “neighbors,” as PECO quaintly calls them), and tenant retention is quite high at 92%.

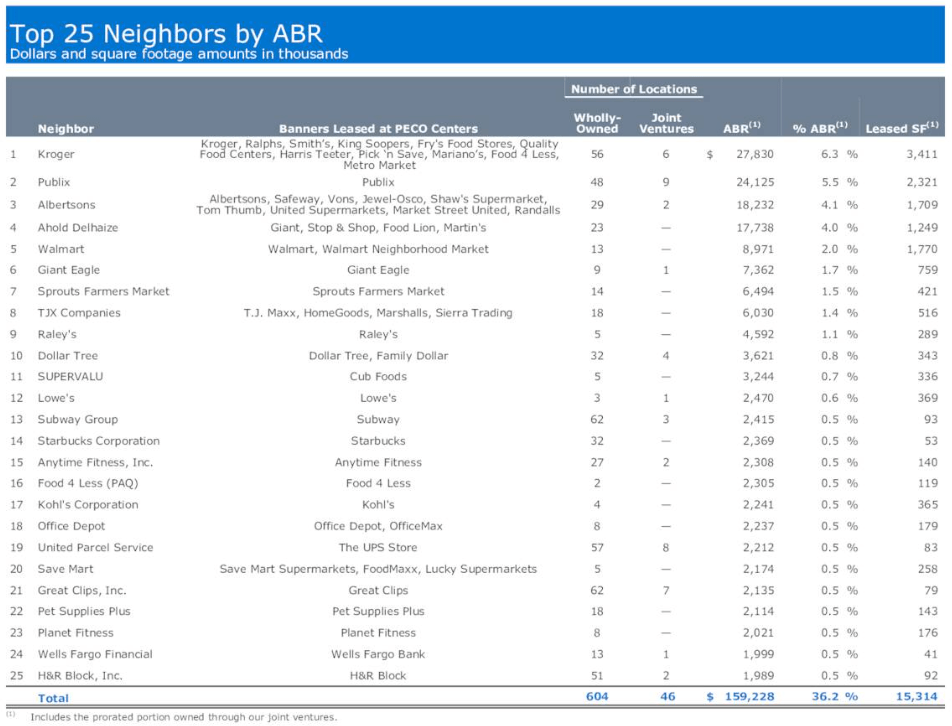

The top 25 tenants are all names that you would expect to see populating a shopping center, with a particular emphasis on grocers.

PECO Q4 2022 Presentation

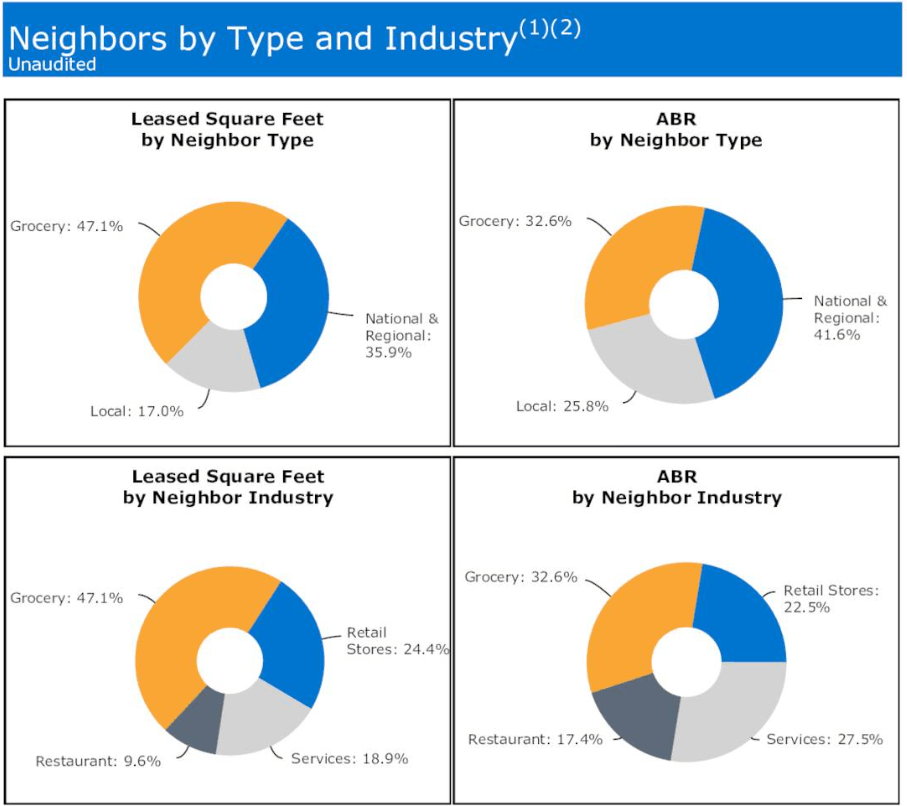

In fact, grocery stores account for around 1/3rd of PECO’s annual base rent, with other goods retailers (22.5%), services (27.5%), and restaurants (17.4%) rounding out the rest.

PECO Q4 2022 Presentation

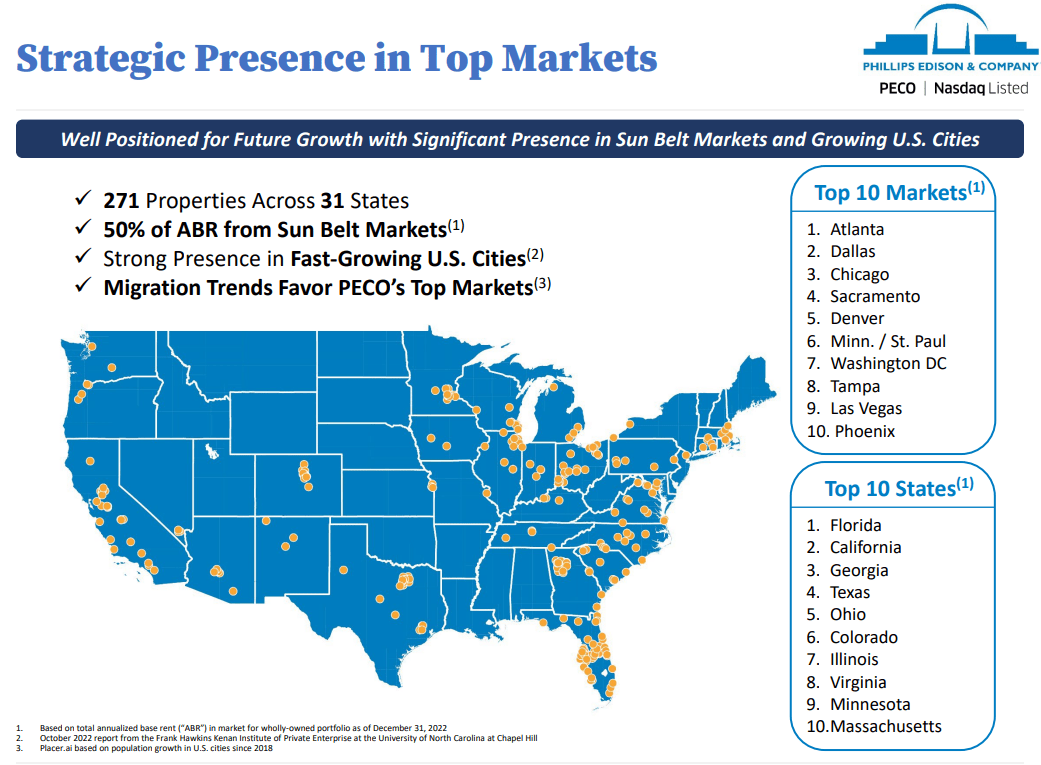

PECO is a national REIT and doesn’t really have a geographic focus. Its top 5 states by rental revenue are:

- Florida (12.0%)

- California (10.9%)

- Georgia (8.5%)

- Texas (8.0%)

- Ohio (5.8%)

PECO February Presentation

While there doesn’t appear to be much rhyme or reason for PECO’s locations, I don’t think there needs to be. Wherever there are population centers, there will be people. And people need to eat.

Moreover, PECO’s centers are overwhelmingly in suburbs, which have experienced an uptick in daytime population as work-from-home has caught on in the post-pandemic era.

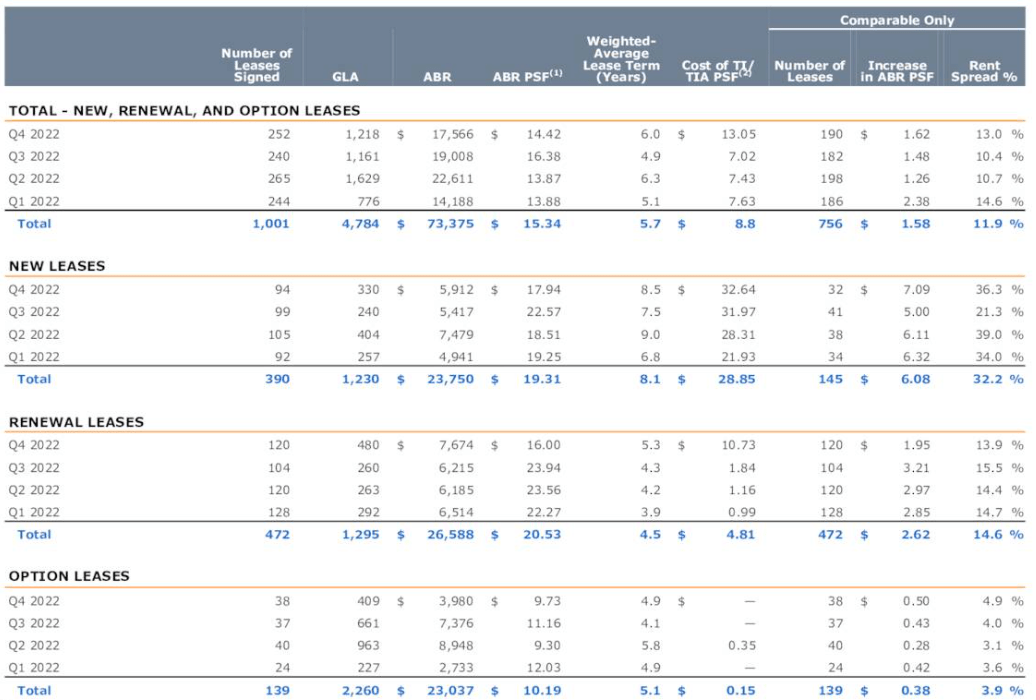

Given the essentiality of PECO’s centers and the high occupancy rate, it’s unsurprising to find that rent growth for new and renewal leases has been strong in the past year, delivering a blended rent spread of ~12% in 2022.

PECO Q4 2022 Presentation

That said, it’s important not to get too excited about these numbers. They are wonderful to see, but they need to be measured against the flat or low annual rent escalations in the part of the portfolio that didn’t have expiring leases in 2022.

Plus, for new leases, the REIT often has to pay fairly high tenant improvement costs to outfit the space for the incoming tenant. Those tenant improvement expenses get amortized over the life of the lease as operating expenses, which brings down the NOI growth.

Thus, the 12% rent growth on new and renewal leases in 2022 only translated into portfolio-wide same-center NOI growth of 4.5%.

| 2021 | 2022 | Q4 2022 | 2023e | |

| Same-Center NOI Growth | 8.2% | 4.5% | 2.8% | 3-4% |

A 3-4% same-center NOI growth rate would pretty much return PECO to its pre-pandemic growth rate. In 2019, the REIT turned in same-center NOI growth of 3.7%.

Total portfolio annual base rent per square foot increased 5.0% from year-end 2021’s $13.71 to year-end 2022’s $14.39.

On the plus side, this does indicate ample embedded mark-to-market rent growth to come in the future as leases expire in the next few years.

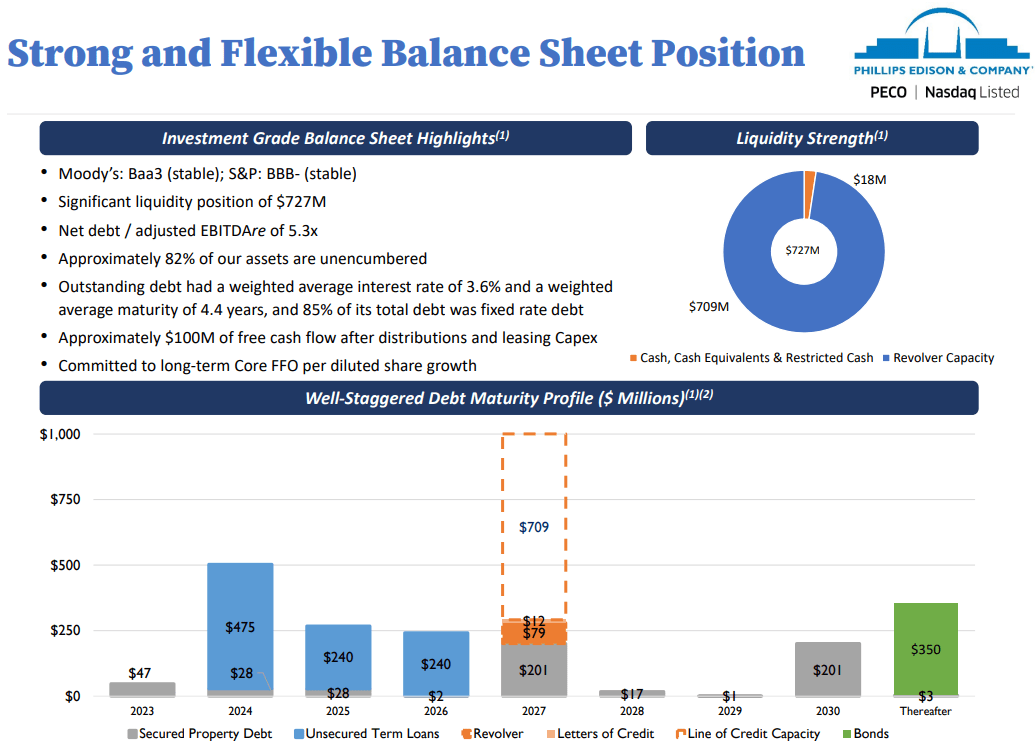

Solid Balance Sheet

PECO has done a great job of strengthening its balance sheet over the last few years. Net debt to EBITDA sat at 5.3x at the end of 2022, compared to 5.6x at the end of 2021 and 7.3x at the end of 2020.

The credit rating of BBB-/Baa3 is investment grade, but PECO appears to me to be on track to eventually get an upgrade.

PECO February Presentation

PECO does have $47 million in debt that matures this year and another ~$500 million next year, but it is a comfort to see that the REIT generates around $100 million in free cash flow after distributions and leasing capex (i.e. tenant improvements). This retained cash should help the REIT pay off debt, if need be, in order to avoid refinancing at significantly higher interest rates.

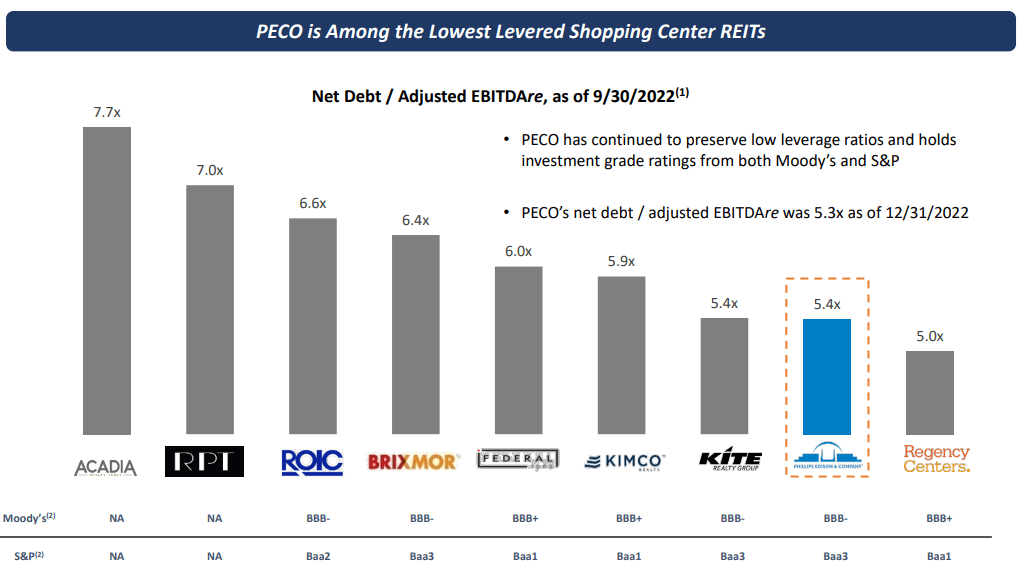

PECO’s level of leverage is the second lowest in the shopping center REIT peer group, as of Q3 2022.

PECO February Presentation

Only the blue-chip Regency Centers (REG), also mostly grocery-anchored, has lower debt-to-EBITDA.

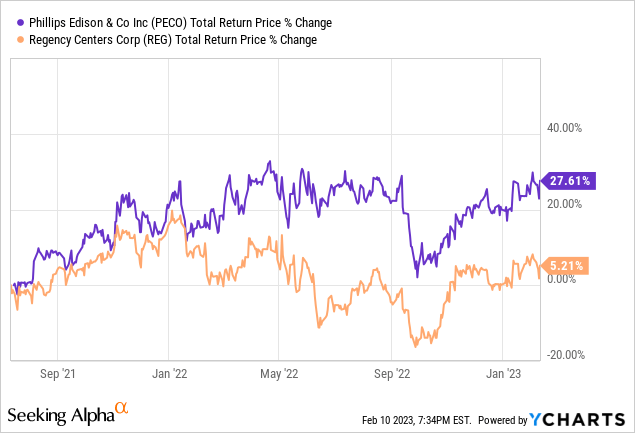

But it appears that PECO’s smaller size and more exclusive focus on grocery-anchored retail has been to its benefit since going public, as it has outperformed REG by a wide margin in terms of total returns.

And PECO has outperformed with a lower dividend yield than REG.

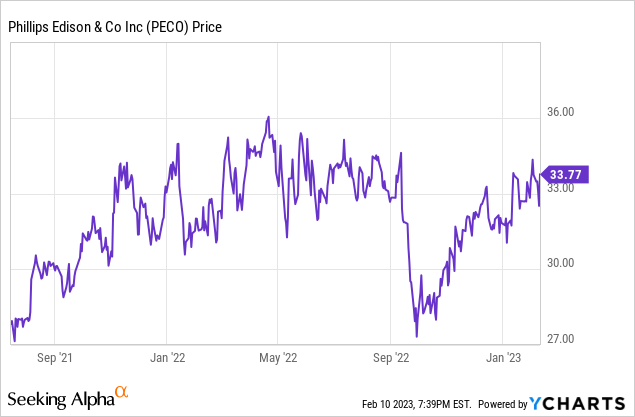

“Buy Under” Price

Since going public in 2021, PECO has vacillated between $28 per share and $36 per share. During that time, the REIT’s dividend yield went as low as 3.1% and as high as 4.0%.

Thus, the current dividend yield of 3.3% is on the low end of that spectrum.

If I wanted to buy this REIT, I would want to get a starting yield of at least 3.6%. That would mean I’d need to buy at no higher than around $31, or a price-to-core FFO of 13.65x.

At that price, I would view my cost basis in PECO as having some margin of safety in addition to the defensiveness of the REIT itself. The dividend yield may be slight, but it’s extremely safe, given the nature of the business and the ~49% payout ratio.

Be the first to comment