Baris-Ozer

Introduction

When last reviewing Phillips 66 (NYSE:PSX) early in 2022, their dividend growth restarted after a multi-year hiatus, as my previous article highlighted. Thankfully, the subsequent year was not disappointing for shareholders with a higher share price accompanying their dividend growth. As 2023 begins, they have recently announced their DCP Midstream acquisition and despite uncertainties surrounding its contributions to their future free cash flow, their dividend growth outlook remains very.

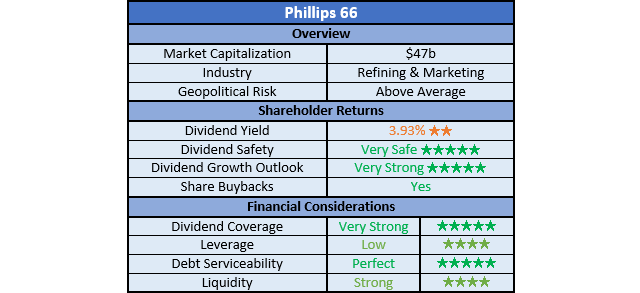

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

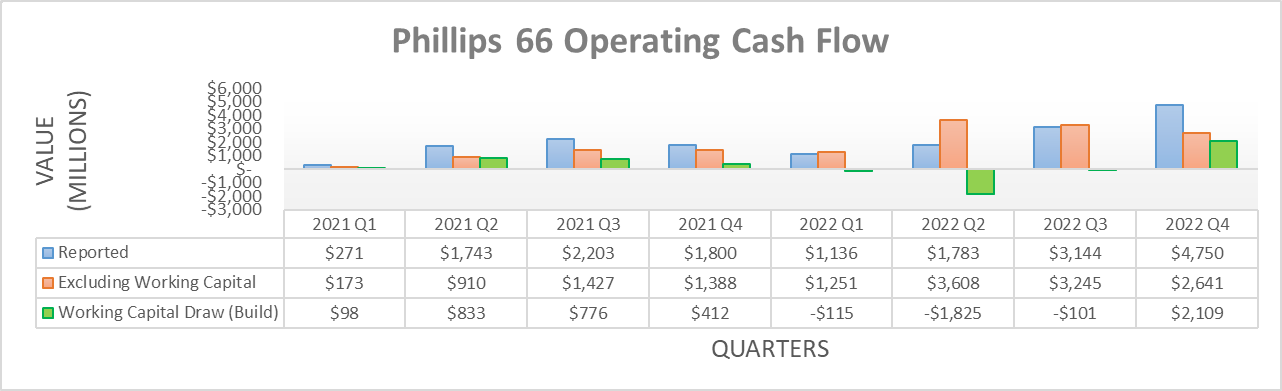

Following their strong recovery in 2021, it was nothing compared to what was laying just ahead in 2022 following the Russian invasion of Ukraine. As a result of refining margins surging to never-before-seen levels, their operating cash flow soared to a massive $10.813b, thereby easily eclipsing anything in their history, including their previous result of $6.017b during 2021. Accordingly, their free cash flow also followed in tandem with a record-setting result of $8.559b, which easily provided very strong coverage to their accompanying dividend payments of $1.793b.

Author

If reviewing their operating cash flow on a quarterly basis, it is easier to see the extent everything changed during the second quarter of 2022, directly after the Russian invasion of Ukraine. The resulting never-before-seen refining margins lifted their underlying operating cash flow that excludes working capital movements to $3.608b, which is truly massive for only one quarter. As for the third and fourth quarters, it is difficult to make any useful judgments versus earlier quarters because following the 17th of August 2022, the financial statements of DCP Midstream were consolidated as they took control after increasing their ownership stake, as per their Q3 2022 10-Q. That said, their respective underlying results of $3.245b and $2.641b were still massive even if viewed in isolation.

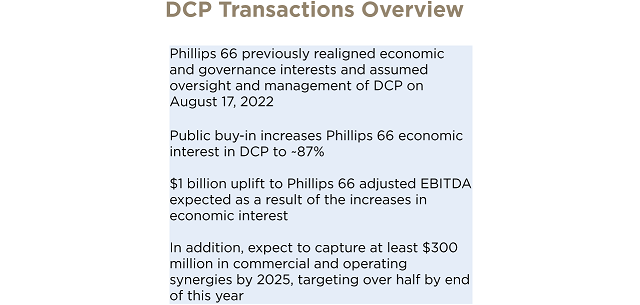

DCP Midstream Transaction Presentation

This circles around to the big news item, their acquisition of DCP Midstream in early 2023 that sees the remaining publicly owned units acquired. When looking at their transaction guidance, they state an additional contribution of $1b to their adjusted EBITDA with a further $300m to be forthcoming as synergies flow through by 2025. Even if ignoring the latter portion to create a margin of safety, the additional contribution in the short-term stands to help materially, especially when operating conditions normalize since midstream assets tend to be less sensitive to commodity prices.

When looking at their adjusted EBITDA results, during 2022 they posted a result of $15.09b whereas as during 2021, their result was only $5.921b, as per their Q4 2022 8-K. Whilst an additional $1b to the former would only have a minimal benefit of slightly less than 7%, it sees a far bigger benefit of circa 17% to the latter. Since their dividends must be affordable across a range of operating conditions, this helps raise their dividend growth outlook in the medium to long-term, which apparently remains a priority, as per the commentary from management included below.

“We’ll want to pay off some incremental debt, especially as we think about the impact of the DCP roll-up, but we should also be positioned to look at the cash returns to shareholders, both in the context of the dividend, we would expect to increase the dividend. This year, we remain committed to a secure, competitive growing dividend.”

-Phillips 66 Q4 2022 Conference Call.

It is very positive to see management is not losing sight of rewarding their shareholders with dividend growth. Nevertheless, given their commentary of wishing to pay off debt, I suspect 2023 will only see a small increase with bigger increases more likely to be forthcoming in 2024 and beyond. Not to mention, right now the extent they translate the additional adjusted EBITDA contribution from DCP Midstream into free cash flow is uncertain due to their guidance for 2023 lacking any information regarding their capital expenditure, as per slide sixteen of their fourth quarter of 2022 results presentation.

This lack of information further compounds the inherent volatility within the refining industry but at least judgments can be made elsewhere. Historically speaking, their dividend payments have not been burdensome or oversized relative to their operating cash flow, thereby creating a very strong dividend growth outlook, as their capital expenditure varies across the years. To this point, even back in 2021 when operating conditions were nowhere near as strong as 2022, their operating cash flow of $6.017b was still more than three times higher than their most recent annual dividend payments of $1.793b.

Even without any additional financial contributions from their DCP Midstream acquisition, the size of this gap means they can easily push their existing moderate circa 4% dividend yield far higher in the coming years. Generally speaking, adding stable assets into the mix should only increase their dividend growth outlook, as time will hopefully prove. That said, their DCP Midstream acquisition will also impose a burden upon their financial position, which should be considered.

Author

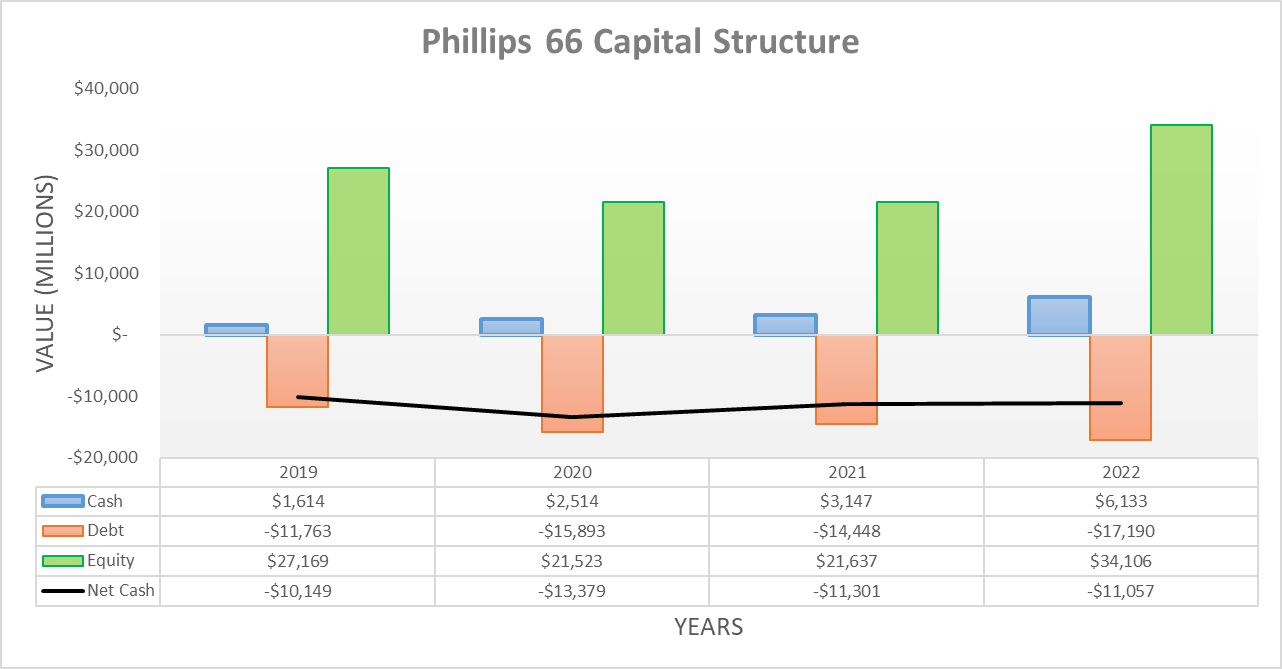

Despite their record-setting free cash flow during 2022, their net debt barely changed with the year ending at $11.057b versus its previous level of $11.301b at the end of 2021. This primarily resulted from the balance sheet of DCP Midstream being consolidated during the third quarter of 2022 when they first increased their ownership stake and took control, thereby effectively seeing the assumption of their debt.

When looking ahead, this now only leaves the $3.8b cost to acquire the remaining units the last of the burdens on the horizon. Since they are not issuing any equity, this would lift their net debt about one-third higher at circa $15b before subsequently declining as free cash flow fills their coffers but as noted earlier, the extent of this remains impossible to quantify.

Author

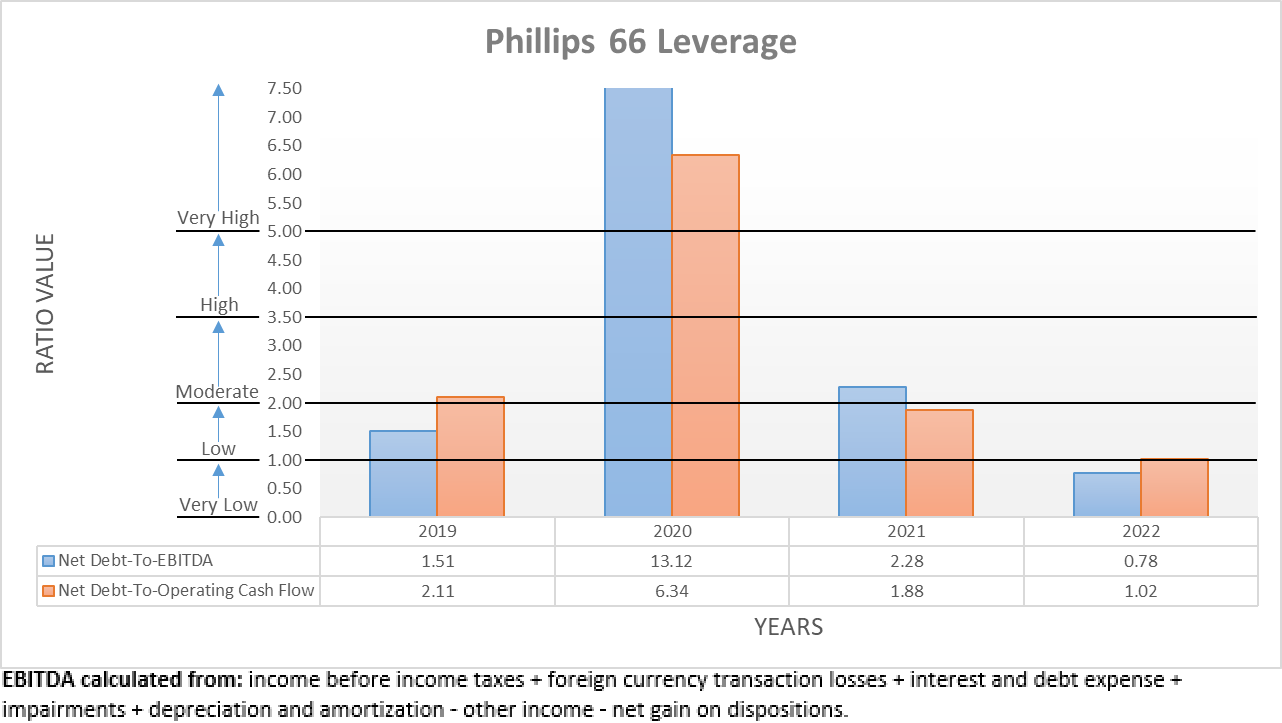

Even though the rate of future deleveraging is impossible to ascertain with certainty, thankfully we can still make informed views regarding any dangers of this acquisition. When 2022 ended, their net debt-to-EBITDA and net debt-to-operating cash flow were 0.78 and 1.02, respectively. The former is easily within the very low territory of beneath 1.00, whilst the latter is only ever-so-slightly above this threshold.

This creates a rock-solid base to absorb the burden of their DCP Midstream acquisition because even without any additional financial contributions, they can easily handle seeing these increase one-third higher. This would only see their respective net debt-to-EBITDA and net debt-to-operating cash flow reaching 1.04 and 1.36, which are both still within the low territory of between 1.01 and 2.00.

Admittedly, this comparison is helped along by their booming financial performance from 2022 but even without this help, their leverage would still be manageable. If their upcoming net debt of circa $15b were compared against their middle-of-the-road results from 2019 that as a reminder, include no additional financial contributions from DCP Midstream, it would leave their net debt-to-EBITDA and net debt-to-operating cash flow at 2.24 and 3.12, respectively. Whilst not necessarily ideal, they are still only in the moderate territory of between 2.01 and 3.50 and thus would not endanger their solvency nor their dividends, especially given their prospects to deleverage in the coming years.

Author

Similar to their leverage, their debt serviceability is already in a position to absorb the burden of their DCP Midstream acquisition. When 2022 ended, they saw perfect interest coverage with results of 20.30 and 17.47 when compared against their EBIT and operating cash flow, respectively. Even without any additional financial contributions from DCP Midstream, they could easily afford to shoulder another one-third higher interest expense without causing any problems.

Author

When it comes to assessing their liquidity, as it stands right now there is no data on their current assets and liabilities for the end of 2022 because we are still awaiting the release of their 2022 10-K. That said, thankfully their results for the third quarter are still sufficiently useful because their record-setting free cash flow should ensure nothing could have deteriorated materially in such a short length of time, especially given their current ratio of 1.30 and cash ratio of 0.34, which made for strong liquidity.

Upon completing their DCP Midstream acquisition, which management intends to fund via a combination of cash and debt. Depending upon how much is funded via the former, it might pull back their liquidity, although given the large size of their company and ability to generate free cash flow, it should remain adequate at a minimum. Nor should it give rise to any issues regarding future debt maturities, as they expect to retain their BBB+ credit rating, as per slide three of their DCP Midstream transaction overview presentation.

Conclusion

Since their financial position ended 2022 in a rock-solid state, it can easily absorb the burden of their DCP Midstream acquisition, even without any additional contribution. Whilst this acquisition should boost their free cash flow, especially during years with weaker refining margins, the extent remains uncertain. Thankfully, they still have a very strong dividend growth outlook and since this is on the minds of management, I believe that maintaining my buy rating is appropriate. Although at the same time, it would be prudent to remember 2023 may be a volatile year given the questionable economic outlook.

Notes: Unless specified otherwise, all figures in this article were taken from Phillips 66’s SEC Filings, all calculated figures were performed by the author.

Be the first to comment