RiverNorthPhotography/iStock Unreleased via Getty Images

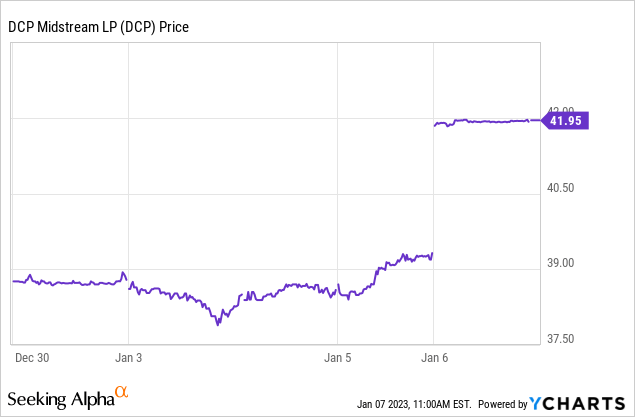

On Friday, Phillips 66 (NYSE:PSX) announced it had reached an agreement to acquire the remaining public common units of Denver-based DCP Midstream (DCP) for $41.75/unit – for an aggregate cash value of ~$3.8 billion. The price was a 20% premium as compared to $34.75/unit original offer PSX made back in August. However, the market had already anticipated that PSX was likely to raise the price as prior to the announcement DCP was already trading at $39.32:

Meantime, PSX closed Friday at $105.70 (+$2.68) as the broad market rallied on the back of economic data indicating the rising potential of a “soft landing” as opposed to a full-blown or harsh recession.

The Deal

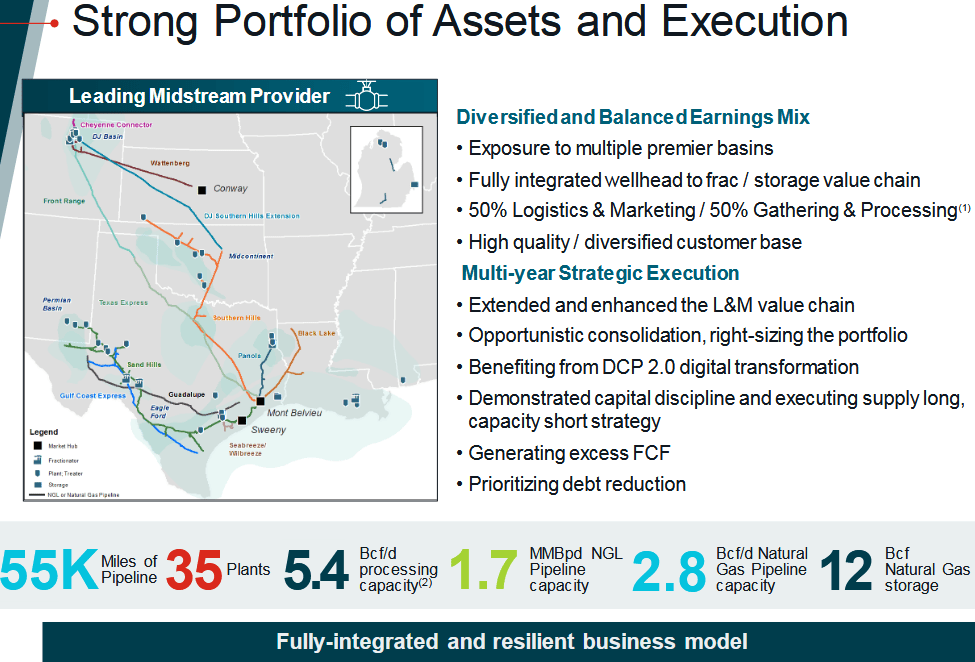

The following slide shows a summary of DCP’s assets:

DCP Midstream

Source: June J.P. Morgan Presentation

DCP is a major U.S. natural gas G&P (gathering & Processing) company and vaults PSX into the big-leagues in terms of NGLs production and natural gas processing (5.4 Bcf/d).

As far as I know, Phillips 66 has not published an estimated multiple as is customary with midstream deals. That said, there have been a lot of moving pieces here – including PSX’s $400 million payment and 35.75% of its stake in the Gray Oak pipeline to Enbridge (ENB) last year in return for ~15% of ENB’s stake in DCP. That left Enbridge with a 13.2% stake in DCP Midstream and reduced PSX’s interest in Gray Oak to 6.5%.

What we do know is that PSX estimates DCP will contribute an incremental $1 billion of annual adjusted EBITDA. Based on PSX’s 483 million shares outstanding as of the end of Q3, that equates to an estimated $2.07/share. On top of that, PSX estimates an additional $300 million in integration synergies by 2025, or an additional $0.62/share.

Note that Wouter van Kempen, the longtime CEO of DCP, and Sean O’Brien – DCP’s CFO and Vice President, both resigned last month – effective December 31st.

According to Reuters, the sweetened deal valued DCP at an estimated $8.7 billion. If we tack on the cash & assets PSX had previously transferred to Enbridge, and consider the $1 billion in estimated adjusted annual EBITDA, we get an estimated multiple just north of ~10x, which is typical for a midstream gas G&P (gatherer & processor). PSX expects to fund the transaction using a combination of cash & debt while retaining its investment grade credit rating (A3, BBB+). Note that PSX ended Q3 with $3.74 billion in cash and that the deal is expected to be immediately accretive.

The deal is expected to close in Q2 and, due to the quirkiness of the MLP structure (which is highly biased toward the GP, which PSX controls), does not require DCP shareholder approval. So, as suggested in the title, this is a done deal.

Furthermore, as I suggested in my previous article after Phillips 66’s offer to buy DCP, following the closure of this deal, I further expect PSX to simplify its operational and organizational structure by offering to buy-out Enbridge’s remaining 13.2% interest in DCP (see Phillips 66 Makes a Big Move, But Enbridge Benefits More). But just because – in my opinion – Enbridge has benefited more from this deal in the short-term, that doesn’t mean PSX isn’t going to extract excellent value out of DCP going forward – it certainly will.

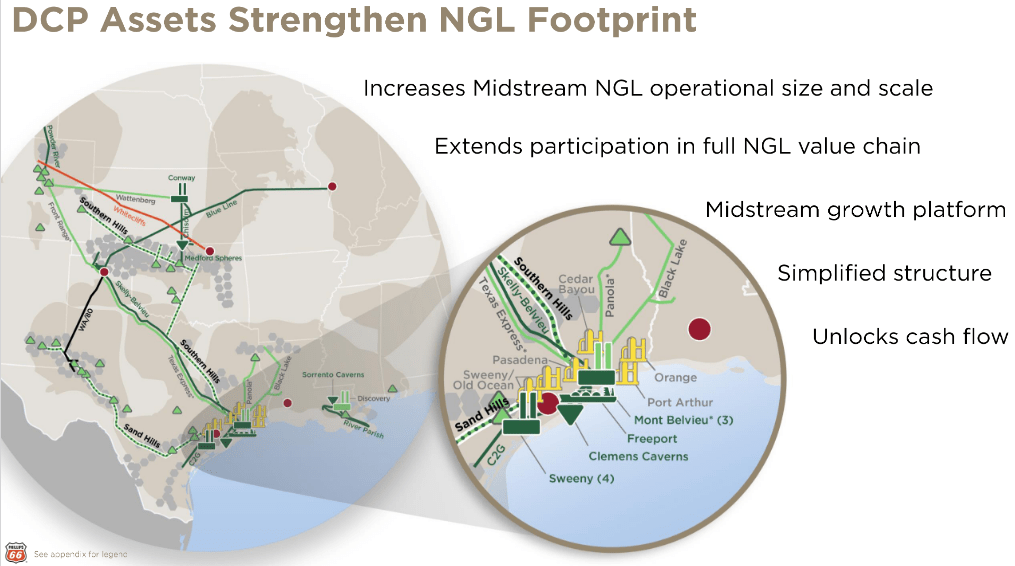

PSX’s willingness to pay-up for DCP in order to close the deal shows how much the company wanted to control DCP’s assets. That’s because the benefits of controlling its critical NGLs feedstock supply directly from the wellhead to its downstream assets (Sweeney fractionation, LPG exports, and chemicals) are clear and quite obvious:

PSX

Source: PSX/DCP Transaction Overview

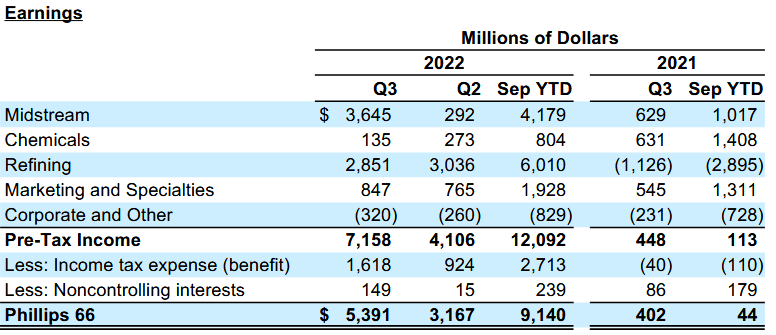

On the Q3 conference call, Phillips 66 reported quarterly results that included:

- Sweeny Hub fractionators average throughput was 429,000 bpd

- The Freeport LPG export facility loaded 249,000 bpd

For the first 9-months of 2022, note that DCP averaged 771,000 bpd of NGLs production. That being the case, it is clear that PSX will now control additional volumes of NGLs – above and beyond Sweeny demand – to either supply CPChem’s (PSX’s 50/50 chemicals JV with Chevron (CVX)) or to simply place onto the Texas Gulf Coast market.

It is also noteworthy that DCP reported $553 million of free-cash-flow over the first three quarters of 2022.

Earnings & Valuation

As I reported earlier on Seeking Alpha, Phillips 66’s earnings have rebounded sharply to the upside this year after a horrible 2021 (see PSX: The Coiled Spring Has Sprung):

PSX

As you can see, over the first 9-months of 2022, PSX earned $9.14 billion, or an estimated $18.92/share based on the 483 million shares outstanding at the end of Q3. Q3 earnings of $5.4 billion equated to a whopping $11.16/share.

PSX will report Q4 earnings on January 31st before the market opens. Current estimates are for PSX to deliver EPS of $4.57/share as chemicals and refining margins are expected to be considerably lower on a sequential basis. PSX should deliver in the neighborhood of $20/share of earnings for FY22.

As per Seeking Alpha, PSX’s forward P/E is only 5.4x and the stock pays a $3.88/share annual dividend – which is good enough for a current yield of 3.7%.

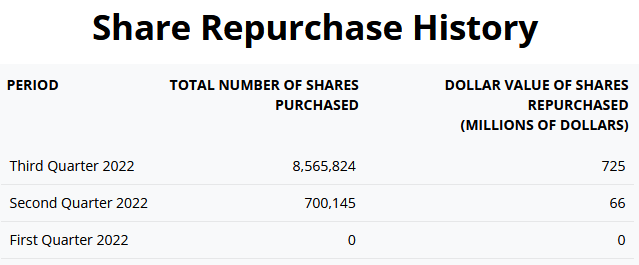

While the quarterly dividend was only increased $0.02/share in last year, note that PSX has started to ramp-up its share buybacks after suspending them in Q2 of 2020:

PSX

Given the company’s still arguably undervalued stock price, I suspect that investors can expect more of the same in 2023. That is, PSX will likely put a priority on stock buybacks. Indeed, during the previously reference Q3 conference call, note that based on the company’s very strong performance in 2022, CFO Kevin Mitchell said:

… I feel pretty confident that with where the balance sheet sits with the cash position we have, with the cash generation we have, we’ll be able to manage that in terms of — yes, we will want to subsequently reduce debt. But with the overall cash position, we should be in a position to continue to return significant amounts of cash to shareholders. So I’m not too concerned that the DCP transaction is going to negatively impact our ability to buy back shares.

Meantime, Jeff Dietert, PSX VP of Investor Relations, said Thursday at the Goldman Sachs Global Energy and Clean Technology Conference (see transcript here) that:

Last summer, we saw demand back close to 2019 levels and saw margins, frankly, I didn’t think we’d see and hadn’t seen historically … we expect gasoline and diesel to be tight again this summer.

Dieter pointed out that, since the pandemic, about 4.7 million bpd of refining capacity was taken out of the market and that diesel – in particular – is very tight. He noted that diesel inventories are currently 15% below the 5-year average while gasoline inventories are 7% below the five-year average. That is a primary catalyst for PSX going forward due to the fact that – as I have reported previously on Seeking Alpha – PSX has a considerably higher distillate yield as compared to its peers.

Returns

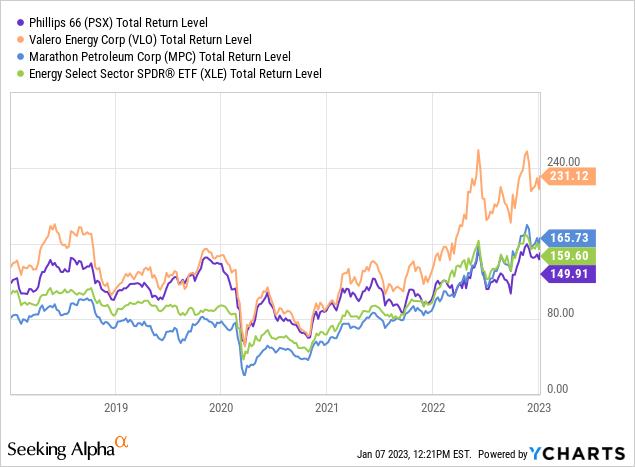

The following graphic compares PSX’s total returns with that of peers Valero (VLO), Marathon Petroleum (MPC), and the SPDR Energy ETF (XLE):

As can be seen, PSX has been the laggard of the group. However, this has not gone unnoticed by PSX’s new CEO Mark Lashier, who last year unveiled a plan to increase total returns to shareholders (see my Seeking Alpha Editor’s Pick How Phillip’s 66 New CEO Plans To Increase Shareholder Returns). The DCP transaction notwithstanding, the plan basically aims to return $10-$12 billion to shareholders from mid-2022 to year-end 2024. At the midpoint, that equates to ~22% of PSX’s current roughly $50 billion market-cap. The company plans to do this by increasing refining margins, lowering annual cap-ex, capturing value from wellhead to market (i.e. integrating DCP), and a relentless focus on cost-reductions – including headcount reduction.

Summary & Conclusions

While the various transactions to acquire DCP have muddied the waters a bit in terms of PSX’s short-term earnings reports, the basic foundation to take over the entire enterprise – including ENB’s remaining economic interest – appears to be on a solid footing going forward. That removes much of the uncertainty that has hovered over PSX since the DCP deal announcement last August. That being the case, investors are beginning to get a relatively clear line-of-sight into what the company’s financial performance potential will look like post the transaction and going into the second half of 2023 might be – including the DCP assets. Investors will gain more insights after the upcoming Q4 FY22 report on January 31st. Yet given that PSX stock is currently trading at such a low valuation level and has such an attractive 3.7% yield, investors shouldn’t wait on this one. I reiterate my BUY on PSX.

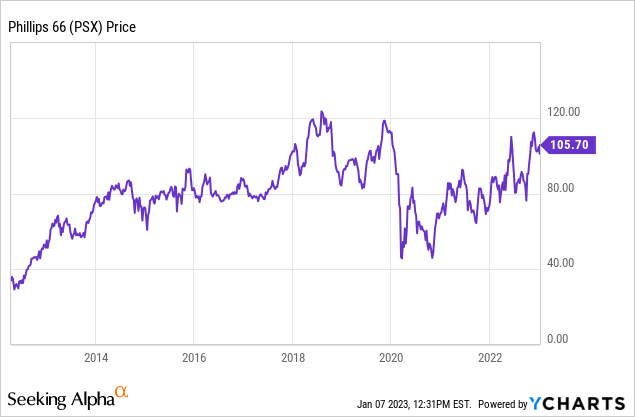

I’ll end with a stock price chart of PSX since its spin-off from ConocoPhillips (COP) in the spring of 2012 and note that the company – despite the dramatic and negative impact of the global pandemic – has grown the dividend at a CAGR of 18% since the spin-off:

Be the first to comment