snyferok/iStock Editorial via Getty Images

Investment Thesis

La-Z-Boy’s (NYSE:LZB) strong return and growth in the past five years is a result of both its strong brand and effective sales network and strategy. This strategy, however, may not work well in a weak consumer sentiment environment. With its weakening free cash flow, the company could have a slowdown in its growth and earnings more than currently priced in by the market. We see LZB stock’s recent jump as rich in premium and a chance to sell.

Company Overview

La-Z-Boy, formerly Floral City Furniture, was founded in 1927 and incorporated in 1941 in Michigan. The company is a global producer of reclining chairs and the second-largest manufacturer/distributor of residential furniture in the United States. According to its 10-K, it “manufactures, markets, imports, exports, and distributes retail upholstery furniture products under the La-Z-Boy ® , England, Kincaid ® , and Joybird ® tradenames. In addition, it imports and distributes retail accessories and casegoods furniture products under the Kincaid ® , American Drew ® , Hammary ® , and Joybird ® tradenames.” Its reportable operating segments include the Wholesale segment, the Retail segment, and Corporate & Other.

Strength

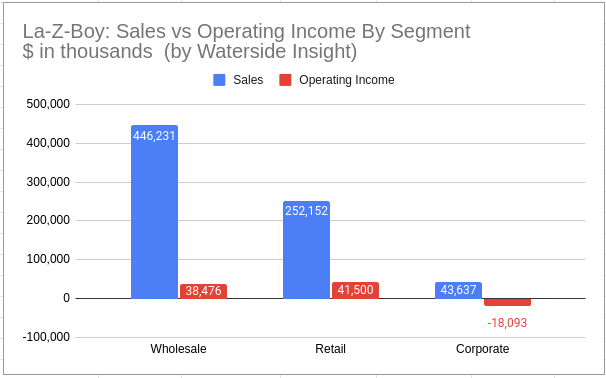

With 95 years of quality and craftsmanship, La-Z-Boy has a solid appeal as a quintessential American heritage and an iconic brand. The company sells its products through multiple channels: furniture retailers or distributors, directly to consumers through retail stores, or through its own website. It considers its network of 348 La-Z-Boy Furniture Galleries stores and 531 La-Z-Boy Comfort Studio as the centerpiece of its retail distribution strategy, as these locations have dedicated space to showcase its products. To understand why it calls this a centerpiece, we compare its sales with its operating income by segments, and can see retail segment’s contribution to operating income has out-proportionated its share in sales. Retail has almost half of Wholesale’s sales volume, yet it produced higher operating income in the latest quarter’s results.

La-Z-Boy Sales vs Operating Income by Segment (Calculated and Charted by Waterside Insight with data from the company)

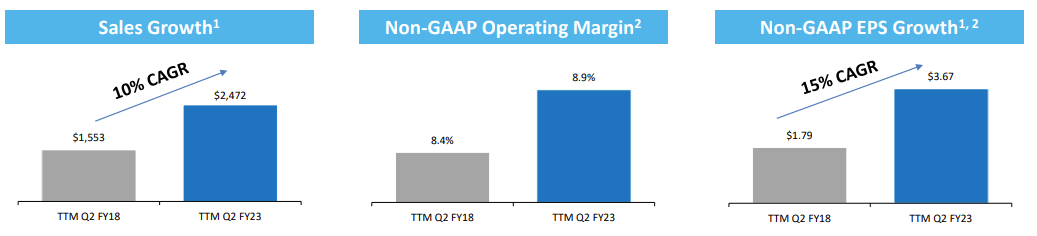

Armed with this sales strategy, La-Z-Boy has a strong track record of growth over the last five years.

La-Z-Boy Past 5 years Growth (Company Q3 presentation)

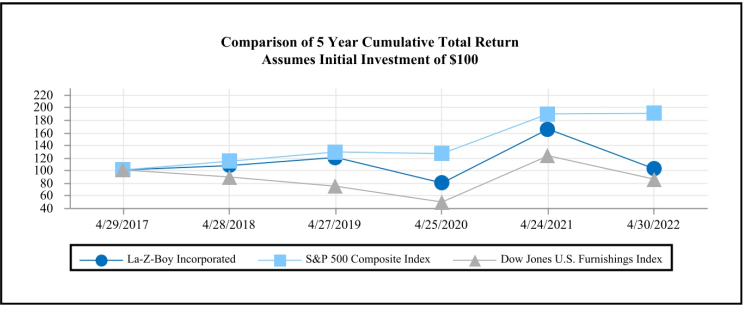

Its stock’s total cumulative return has also beaten the sector average and the broader market during these five years.

La-Z-Boy Past 5 years Total Cumulative Return (Company 2022 10K)

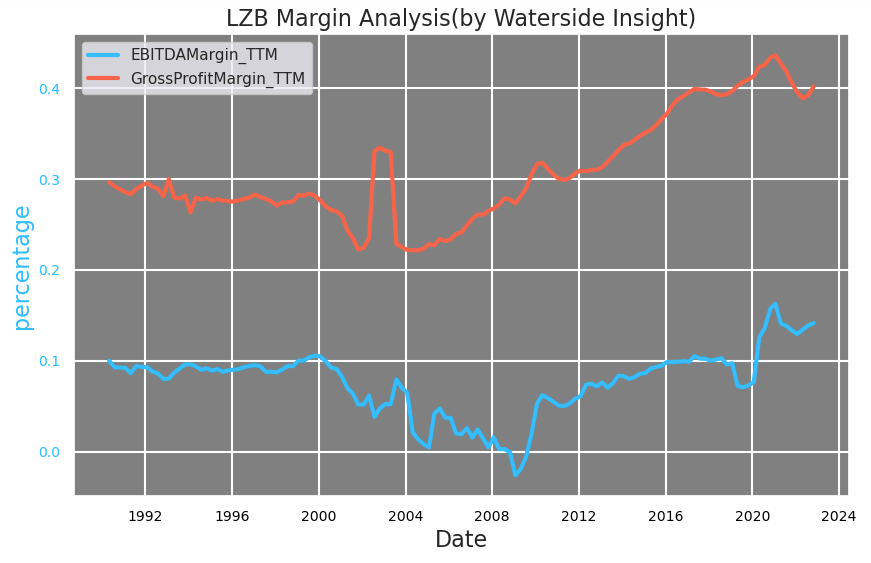

In recent quarters, La-Z-Boy’s margins have been hovering at a high level historically.

La-Z-Boy Margin (Calculated and Charted by Waterside Insight with data from the company)

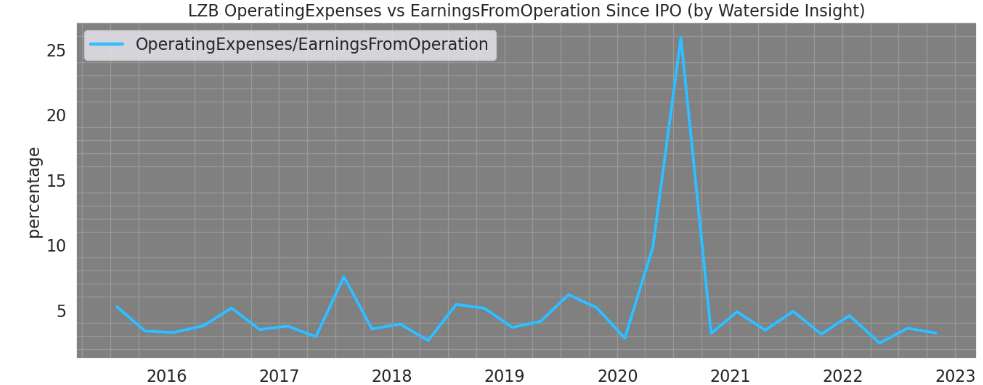

The company has strong and effective control over operating expenses. The operating expenses as a percentage of earnings from the operation have always been kept between 3x to 5x. This is a range that the company has maintained since at least 2015, and most importantly, this range didn’t trend upward. If we view the spike during the pandemic as a stress test of this control, we can see this ratio was quickly brought down and back to its normal range and has even drifted lower since.

La-Z-Boy Operating Expenses vs Earnings (Calculated and Charted by Waterside Insight with data from the company)

Weakness/Risks

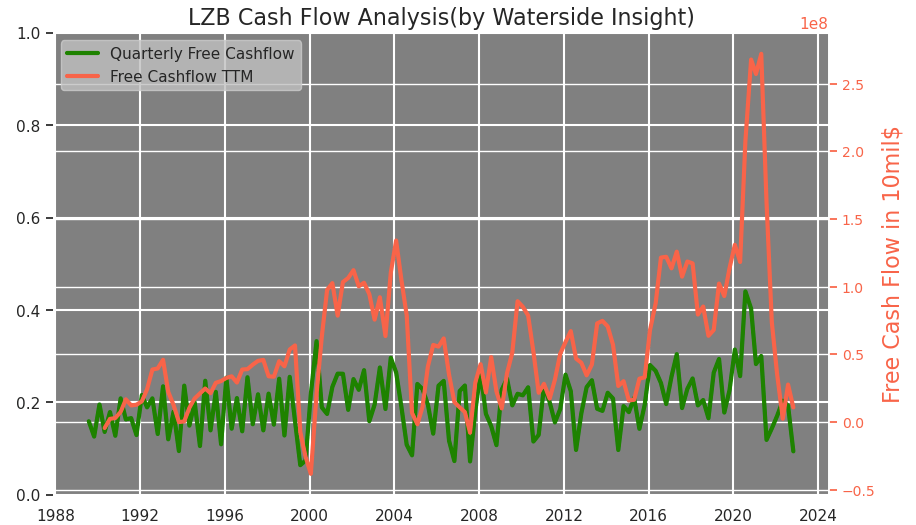

However, La-Z-Boy’s free cash flow has dropped to its lowest level lately.

lzb (Calculated and Charted by Waterside Insight with data from the company)

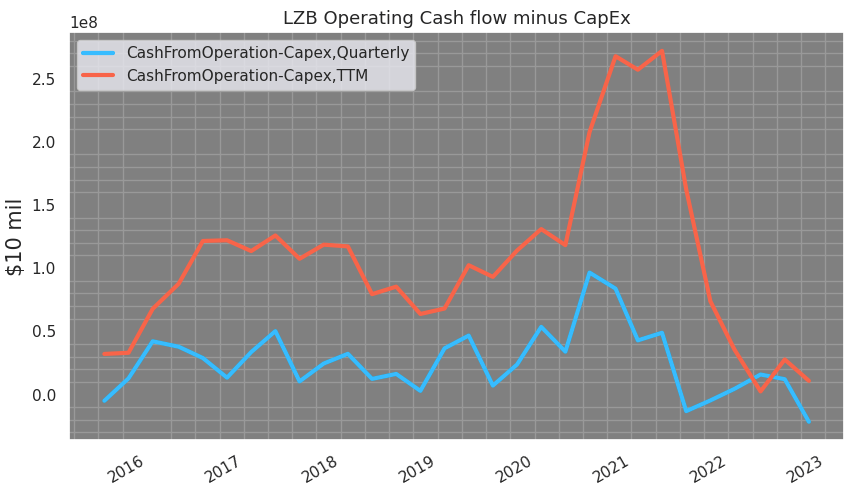

And if subtracting the capex spending, its quarterly operating cash flow has dropped negatively.

lzb (Calculated and Charted by Waterside Insight with data from the company)

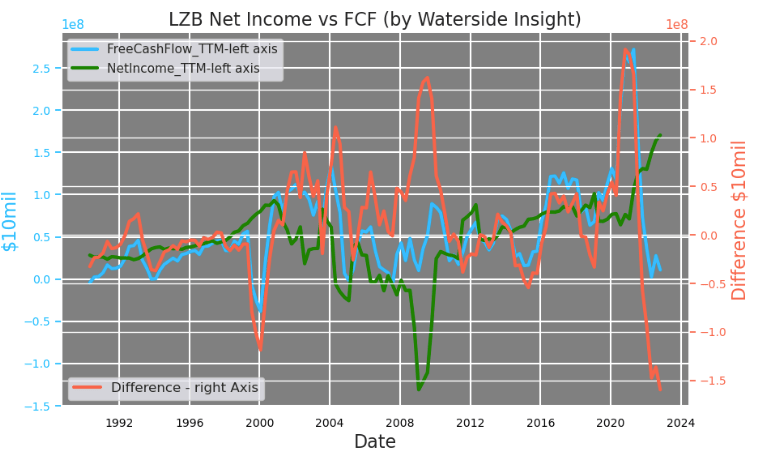

This drop is most noticeable when compared with net income. When you subtract net income from the free cash flow, that difference reaches the lowest level, as net income is still positive. If the two of them will converge, which direction would each of them take? If net income were to be lower, free cash flow would be hard to increase.

lzb (Calculated and Charted by Waterside Insight with data from the company)

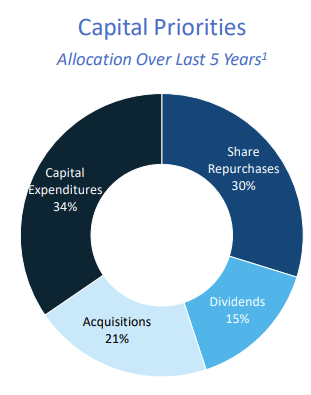

La-Z-Boy has a capital allocation strategy that 50% of the cash flow will be returned to shareholders. With its weakened free cash flow, the shareholder return will inevitably be impacted in 2023. Also, the company has an ongoing effort in its sales strategy to grow its company-owned retail business and leverage its integrated retail model to target a suitable geographic market. These acquisitions could slow down in the next 12 months.

La-Z-Boy Capital Allocation (Company Q3 presentation)

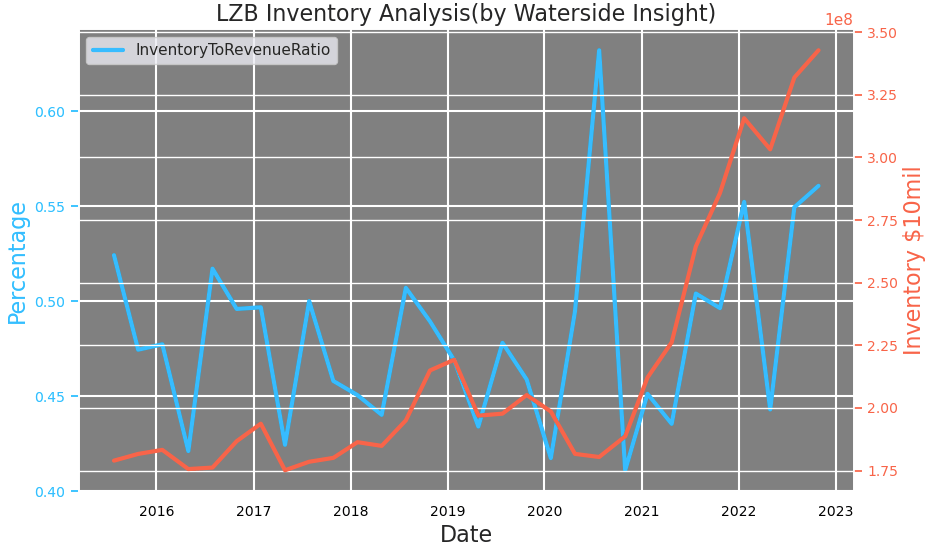

On the other hand, La-Z-Boy’s inventory has been piling up lately, on an absolute basis and on the basis as a percentage of the revenue. It is not hard to see the broader market slowdown of retail sales could impact its sales in a meaningful way, especially given its sales strategy that focuses on the retail segment, as we alluded to earlier.

La-Z-Boy inventory (Calculated and Charted by Waterside Insight with data from the company)

Financial Overview

La-Z-Boy Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

Valuation

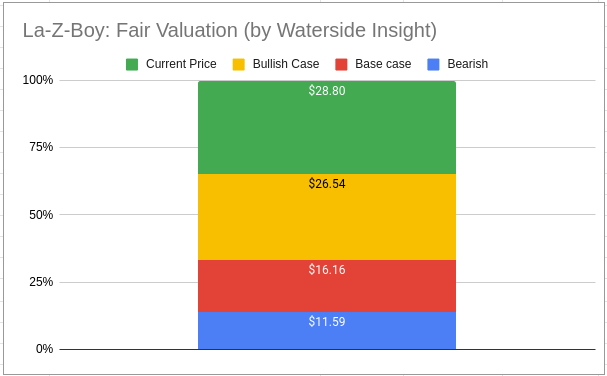

We take into account all the analysis above and use our proprietary models to assess the fair price of La-Z-Boy with a ten-year projection forward. In our bullish case, La-Z-Boy has weak cash flow growth in the near term, but stages a large comeback along with a broader economic recovery, and continues on a stable growth trajectory; it was valued at $26.54. In our bearish case, the company has a more extended period of near-term weakness, and its comeback was less than stellar, and although it still has stable growth, it cannot fully recover to its strong cash flow level in 2019 and 2020; it was valued at $11.59. In our base case, it has a similarly extended period of weakness in 2023 and 2024, but is able to roar back and continues with a stable growth pattern; it is valued at $16.16. The current price is higher than our top-end estimate.

La-Z-Boy Fair Valuation (Calculated and Charted by Waterside Insight)

Conclusion

La-Z-Boy has an iconic brand appeal, sufficient margin growth, and strong expense control. The company rightfully positions its earnings growth among retail consumers’ buying power. However, it has had a weakened cash flow in recent quarters that could impact both its shareholder return and its ongoing acquisition efforts. Combined with a potential slowdown in consumer purchasing momentum, its topline growth and earnings could also slow down. Our base case scenario is more of bearish and recommend a sell at the current price.

Be the first to comment