AndreyPopov/iStock via Getty Images

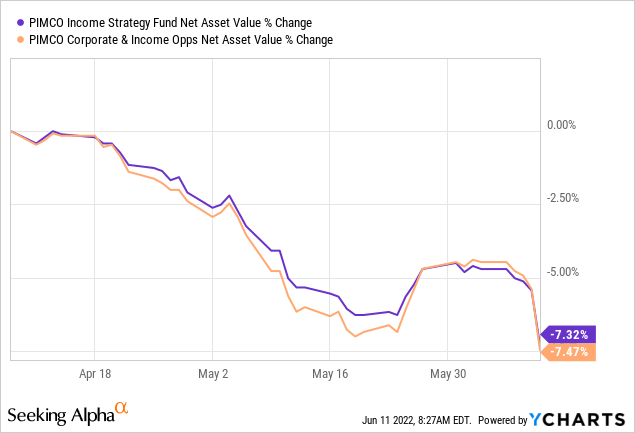

When we last covered PIMCO Corporate & Income Opportunity Fund (NYSE:PTY) and PIMCO Income Strategy Fund (NYSE:PFL), we told you why the funds offered a rather poor return outlook and investors would be better off looking elsewhere for yield. What has happened here is rather interesting as our thesis has played out perfectly as far as the NAV of these funds are concerned. The NAVs have dropped in almost identical fashion at a 45% annualized rate and are now about 7.5% lower than 2 months ago.

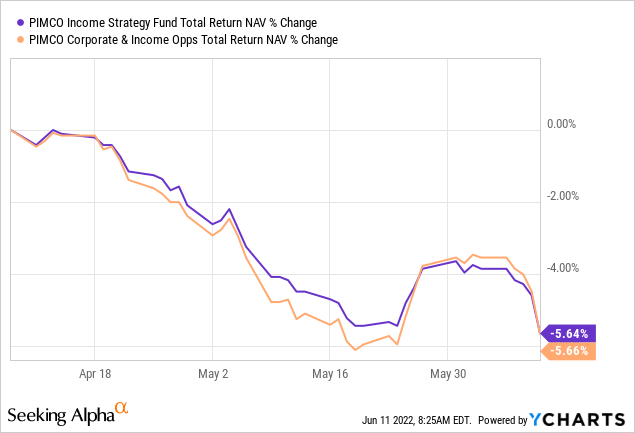

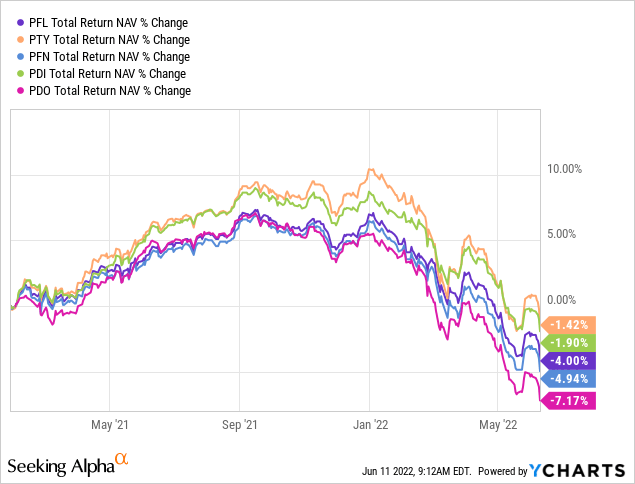

Total return, which includes the prized distributions, was also negative but obviously, less of an eye sore.

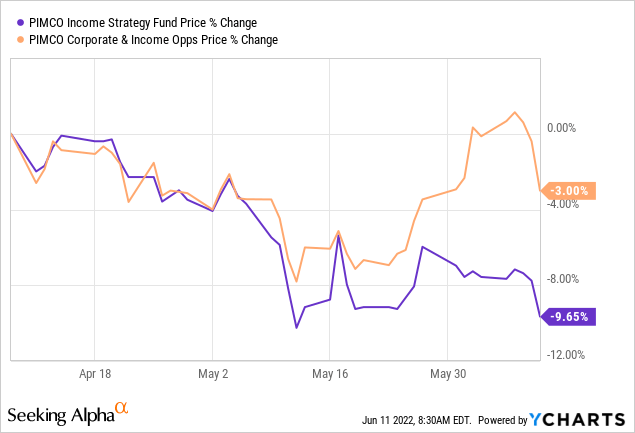

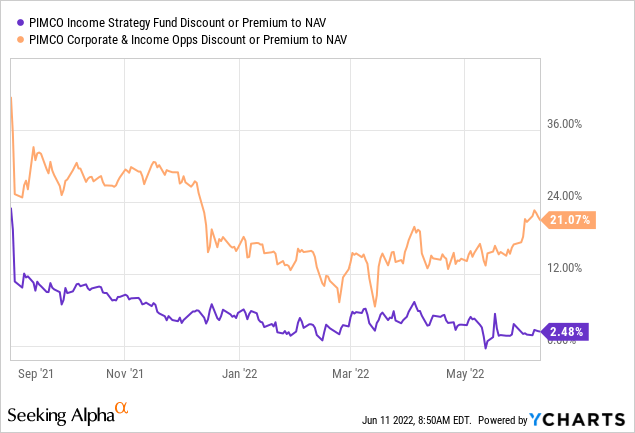

While those are the most important measures, we have seen a price distortion between the two.

PTY has moved down only 3% and stopped tracking PFL since mid-May. We look at the outlook for these two funds in light of the recent economic data.

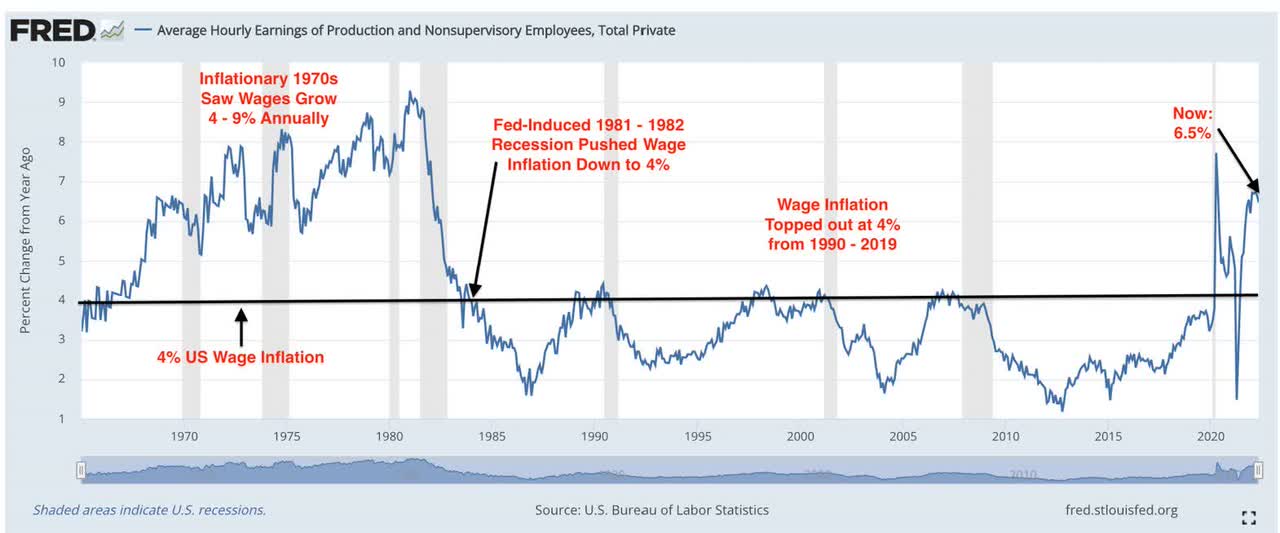

Wage Growth

The core of our thesis since June 2021 (see Abysmal Setups) has been that these funds are incredibly expensive in relation to their potential and investors will likely not see positive total returns for a long, long time. This has played out of course and the returns are quite bad over this time frame. Unfortunately, the macro environment has not improved for these funds.

The primary concern here is that the Federal Reserve is still grappling with unprecedented inflation. Wage growth has now jumped to 6.5% and that is an outlier level for sure.

FRED

In conjunction with a fortified balance sheet from COVID-19 stimulus savings, the consumer can tolerate high inflation for quite some time. Hence, the amount the Federal Reserve needs to raise has moved up even more.

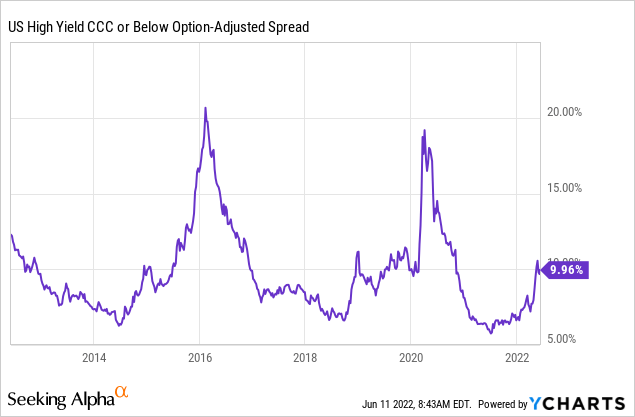

CCC Spread

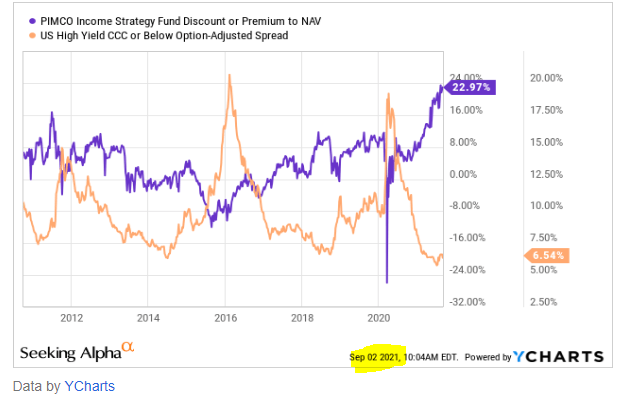

US High Yield CCC or below Option Adjusted Spread is a measure of distress in the bond market. This is one of our favorite indicators and one where we are also a little surprised at how it has played out. Back in September 2021, we showed you this chart alongside the premium to NAV for PFL.

Seeking Alpha Article Sep 3, 2021

Our commentary back then was as follows.

But if you are looking for an entry point, watch the High Yield CCC Option Adjusted Spread. When this meter blows up and we will likely get it in the next 12-24 months, it will go sailing past 10%. When that happens you can bet you will get all these funds at a discount to NAV.

Source: It Is Only A Flesh Wound, So Far

Guess where we are today?

The most interesting aspect here is that PFL investors have finally learned their lesson, but PTY investors seem to be rather blasé about this.

That puts PTY in the most unfortunate position where investors could easily see a 25% drop just by a modest further decrease to NAV and normalizing of this parameter.

Triple Threat From inflation

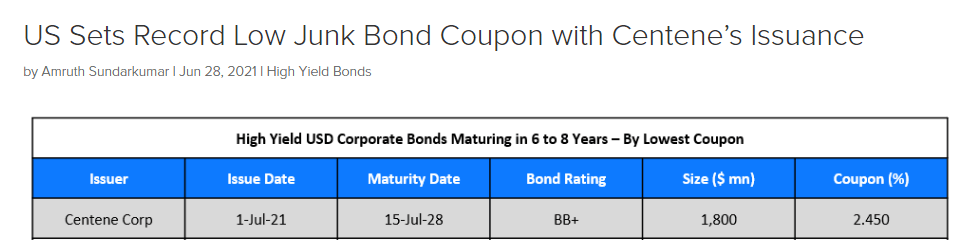

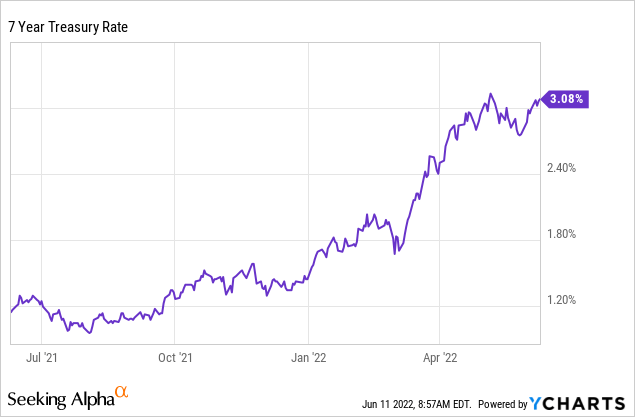

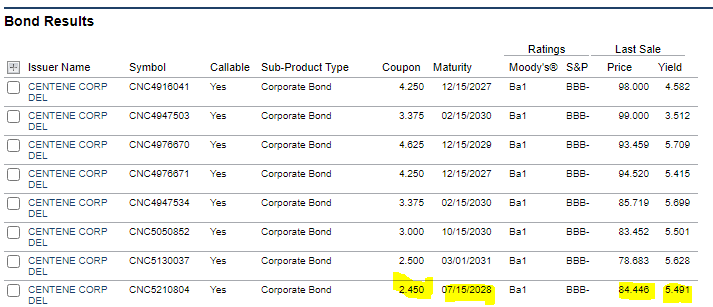

The latest core inflation numbers rattled the markets on Friday. Extremely high inflation is bad for junk bonds from multiple angles. The most obvious one is that higher risk-free rates require even higher rates for junk. A year back Centene (CNC) issued 2.45% junk bonds for 7 years.

Bond Value

Today the 7 Year Treasury yields more than that.

That CNC bond is down 16% in price and yields 5.5%.

FINRA

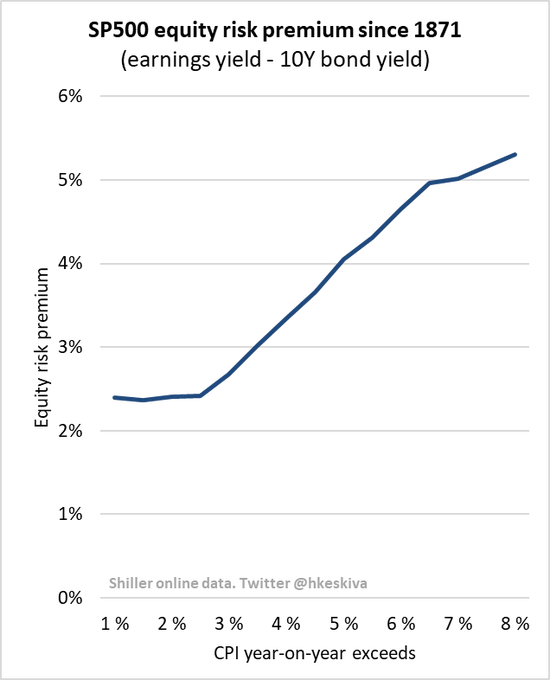

Higher inflation also makes equity issuance more expensive.

Shiller-Twitter

Junk bond issuing companies will find that equity issuance will be really hard in this environment.

Finally, higher inflation crushes margins and this is the most dangerous of the three. High yield issuing firms have very little cushion and margin pressures can kill them very quickly. When the likes of Walmart (WMT) and Target (TGT) cannot maintain margins, one can only imagine the distress in the lower ranks.

Verdict

We don’t see a lot of relief for PFL holders and the most likely path forward is still for very poor returns. We are maintaining a “hold/neutral” rating as the fund is better priced than PTY and we think positive total returns in the 3-4% annual range are probable from here. PFL also has less leverage than PTY and that also works in its favor.

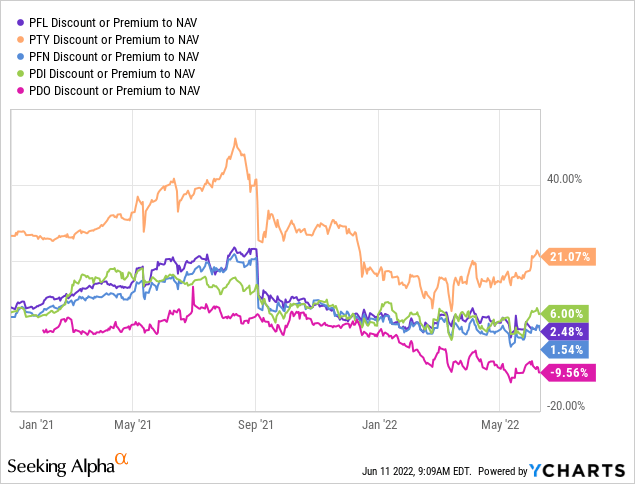

In the case of PTY, the complete disregard for the current environment gets us to downgrade this to a “Strong Sell”. On medium time frames, PTY offers the worst risk-reward among the PIMCO funds we cover. The premium stands out as outlandish when we throw in PIMCO Income Strategy Fund II (PFN), PIMCO Dynamic Income Fund (PDI) or PIMCO Dynamic Income Opportunities Fund (PDO).

While total returns on NAV have been right on top of the pack for the last 18 months, the differences have not justified the lofty premium.

The bulk of the investors minted in this era have expected a “Fed Put”, while we are getting a completely different message today. The Fed Put has become the Fed Collar. We believe we are entering the final few months of the selloff and it will likely end with PTY and PFL at a discount to NAV. We would exercise caution and look for buying opportunities down the line.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment