Kevin Brine

Competitors Are Gaining Ground

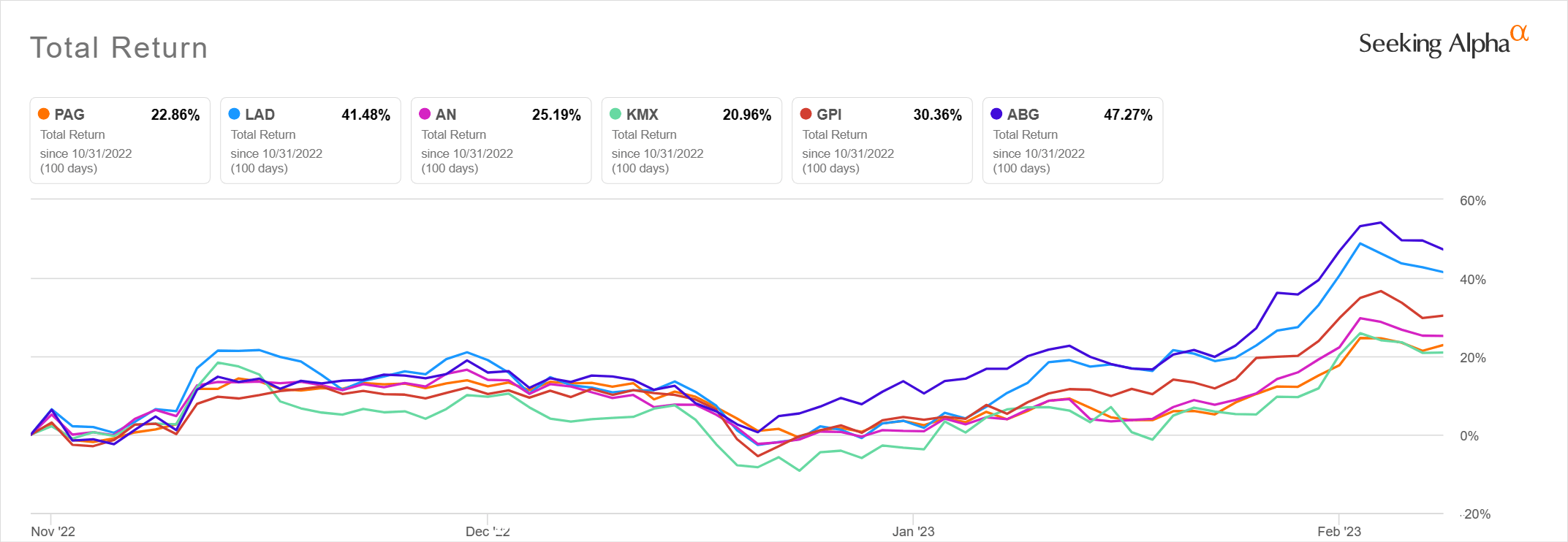

Since I wrote about Penske Automotive Group (NYSE:PAG) in October, the stock has returned almost 23%. Perhaps the Hold rating was too harsh, but most of its competitors have done even better.

Seeking Alpha

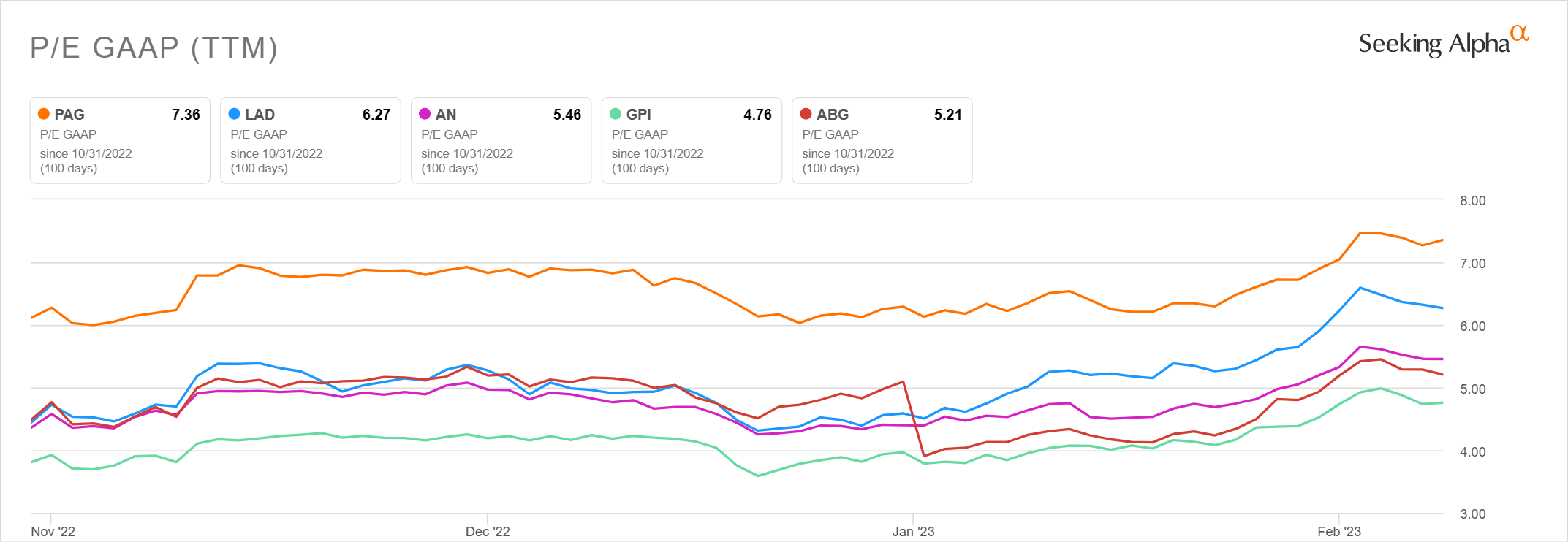

Despite the lag in stock performance, Penske is still one of the most highly valued on a P/E basis, even though it looks cheap compared to the overall market.

Seeking Alpha

As I have mentioned in earlier articles, Penske is different from its peers due to its luxury brand focus, truck sales and leasing business, and foreign exposure, particularly the UK. This diversification can be helpful as it gives the company more ways to win, but it can be a drag when some segments underperform. The used car business and UK dealership exposure is costing Penske right now while other parts of the business are doing well. Let’s take a look at how the peculiarities of Penske are either helping or hurting right now.

Advantages And Disadvantages

Luxury Brand Focus

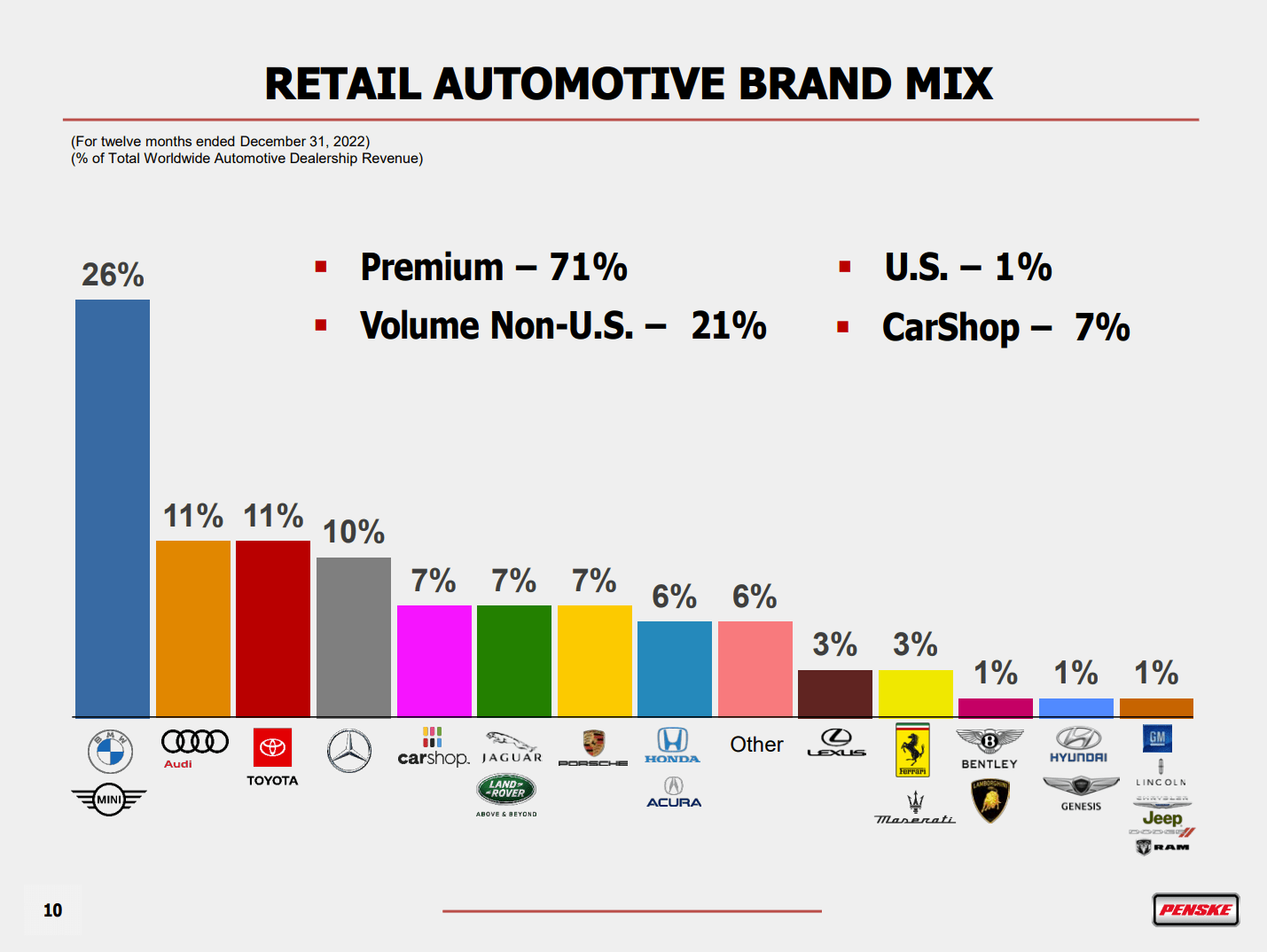

Penske’s auto dealerships are heavily focused on premium brands, with 71% of sales concentrated in this area, including 26% with BMW.

Penske Automotive Group

This brand mix is a huge advantage for Penske right now. When the supply chain is limited for the automakers, they tend to direct the parts that they do have into their most profitable models. Also, when the economy slows down, the premium car customer is the last to be affected. CEO Roger Penske noted this on the earnings call.

… I think the premium customer right now, affordability hasn’t hit them, obviously, even with higher interest rates. But what’s driving our margins and our success, again, certainly is supply. And when you think about what we’re getting, they’re building the best cars they have with the highest margins for not only the factory, the OEM, but also for us. And I think that growth continues to be strong …

Truck Sales

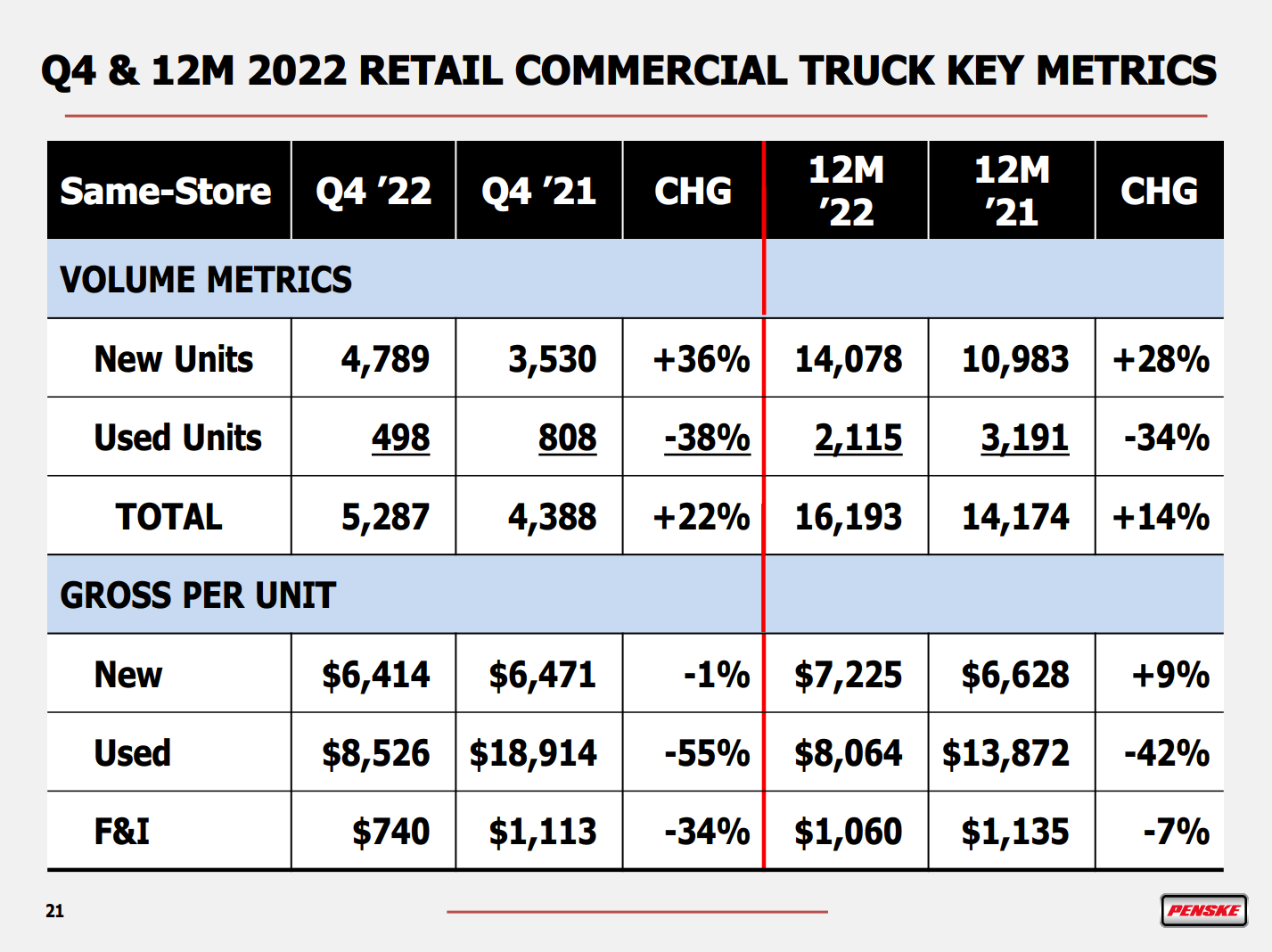

The truck sales business continues to be strong. On a same store basis, Penske increased unit sales 36% in 4Q compared to the same quarter last year. This represents accelerating sales growth when you look at the full year growth rate of 28%.

Penske Automotive Group

Looking at the growth on an overall, rather than same store basis, is even more impressive. Penske added 4 truck dealerships in 2022. With truck sales from the new dealerships added in, unit sales were 5,181 in 4Q (42.8% growth) and 17,932 in FY 2022 (37.9% growth). Penske currently prefers truck over car dealerships as acquisition targets due to their cheaper valuations and lower costs to upgrade once purchased. Roger Penske made these comments on the earnings call:

As we look at the truck side, the multiples have been less than they are on the auto side, point number one. Point number two, the CapEx requirements, i.e., tile, furniture, et cetera, we don’t have that on the truck side. So to me, the CapEx requirements are significantly less when you’re talking about typically buying a U.S. dealership.

Sales look strong going forward. Penske also noted that 75% of these sales were Class 8 commercial trucks. On an industry-wide basis, the forecast for North American sales for 2023 is 294,000 and the backlog today sits at 244,000 units, representing 10 months of sales. Penske’s allocation of Class 8 trucks from the manufacturer for the year is already sold out.

Truck Leasing

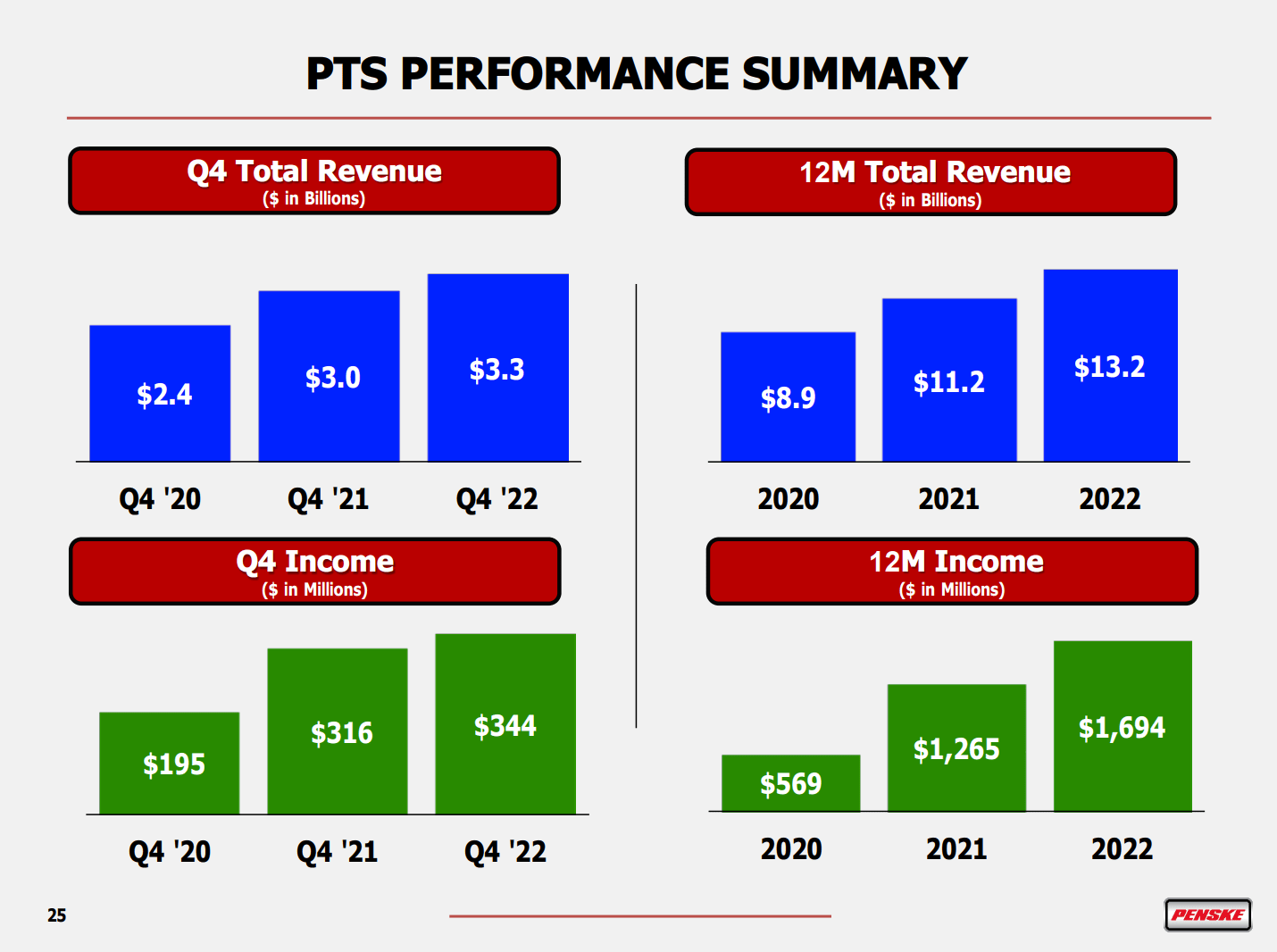

The truck leasing business, Penske Transportation Solutions, is 28% owned by PAG and accounted for as an equity investment. The business currently has a fleet of 414,000 trucks and plans on expanding this to 500,000 by 2025. This business has been a steady grower and makes up over 1/4 of PAG’s pretax income.

Penske Automotive Group

Used Car Sales

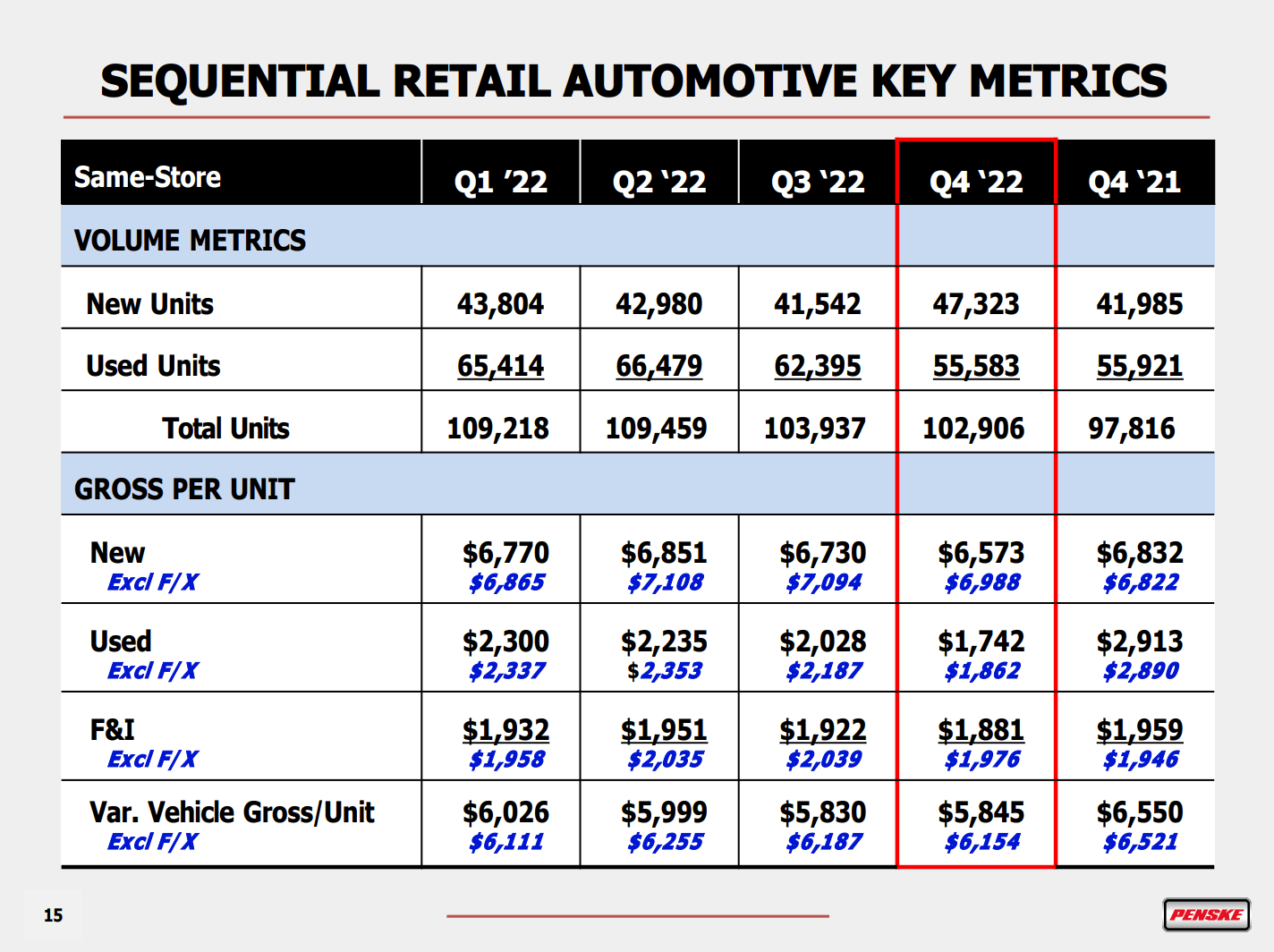

The used car business is currently a big headwind for Penske. The supply chain for new cars is finally normalizing, resulting in higher unit sales and more cars on the lot (25 days of sales vs. 21 at the end of 2021). Used car sales are still at the lowest number of the past 5 quarters and used car gross margins are down 40%, much worse than new car margins.

Penske Automotive Group

Penske has historically counted on returning leased vehicles as a key source of used car supply. The lower volume of new car sales in 2021 and early 2022 has created a lag effect, constraining used car supply. Customers are also preferring to buy rather than lease. As Roger Penske noted on the call,

I think that lease penetration is down significantly due to — certainly, when we look at residual support and also some of the support we get from the finance companies. And when you look at it in real numbers, 55% of our premium was leasing prior to maybe the last 12 to 18 months. And our overall, from a Penske perspective, was 34%. We’re down to 11%.

Used car inventories were 53 days of sales at the end of 2022, still tighter than 60 days at the end of 2021. Used car sales can become more attractive in the future, but the supply picture will need to improve.

UK Dealerships

The obvious downside to foreign dealerships in a strong dollar environment is the negative foreign exchange impact. As noted in the earnings release,

Foreign currency exchange negatively impacted revenue by $1.0 billion, income from continuing operations before taxes by $38.0 million, income from continuing operations attributable to common stockholders by $29.4 million, and earnings per share by $0.40.

This is about a 3.5% hit to revenue and a 2% hit to pre-tax income and EPS.

Used car supply has also been particularly difficult in the UK. The US CarShop stores were able to self-source 73% of their inventory in 2022 but in the UK this figure was only 37%.

As the Fed gets closer to the end of its tightening cycle in the US, the dollar may finally start to weaken. Also, Penske noted an improvement in CarShop sales in January along with availability.

Capital Management

Penske does not include a cash flow statement in their earnings release, and the 10-K is not out yet. However, noting that cash balance is basically unchanged from last year, we can observe that the company is maintaining a very strong balance sheet while providing best-in-class capital returns to shareholders.

In 2022, Penske spent $393 million on acquisitions, including 9 car dealerships, 2 truck dealerships, and 2 open points for future car dealerships. They also spent $283 million on capex. These two investing usages of cash totaled to almost the same amount as in 2021.

The company spent $154 million on dividends in 2022. Penske continue to grow the dividend each quarter, most recently a $0.04 increase to $0.61 payable on 3/1/2023. Penske greatly expanded its share buybacks in 2022, spending $887 million and reducing share count by an impressive 11%.

Penske increased its inventory and receivables by $554 million but also increased payables, including floor plan debt, by $528 million. Going back to the income statement for a minute, I should note that floor plan interest expense is tied to short term rates and has become much more significant this year. In 4Q 2022, it was 6.6% of operating income, up from 0.8% in 4Q 2021.

We see that after all this capex and M&A activity, high capital return to shareholders, and negligible change in working capital, Penske’s long-term debt went up only $148 million. With a total of $1.6 billion in debt (not including floor plan) the company has very low leverage of 0.8 x EBITDA.

Looking forward, I predict Penske will continue raising its dividend by at least $0.04 each quarter. I expect similar M&A and capex levels as well. Buybacks may be lower than 2022’s high level in order to avoid adding debt at higher interest rates. Still, the CFO often mentions that the company has “the ability” to increase leverage to 4x EBITDA if a growth opportunity came up, although I personally would not like to see this happen.

Conclusion

Penske Automotive stock had a strong return over the past quarter. It remains at a higher valuation than most of its peers even though the peers’ stocks had an even stronger quarter. Penske’s premium brand focus, its truck business, and its international diversification make it a unique company, however. The used car business and UK dealerships are a drag on the company at the moment. This underperformance is being offset by a strong truck business, even as some of the negative factors could improve this year anyway.

Penske is an excellent stock here for an income investor as it appears to have the capability to continue increasing its dividend each quarter. However, following the big run up in share price, PAG stock could be due for a breather, and I would suggest waiting for lower levels before adding.

Be the first to comment