8vFanI

Are you familiar with the Business Development Company industry? Known as BDC’s, these firms lend money to privately held companies, which also have co-sponsors, such as VC groups and hedge funds. We’ve covered several BDC’s in our weekend articles, and this week we’re covering PennantPark Floating Rate Capital (NYSE:PFLT), a BDC under the Pennant Park Investment Advisors Group platform.

Profile

PennantPark Floating Rate Capital seeks to make secondary direct, debt, equity, and loan investments. It focuses on companies that are owned by established middle market private equity sponsors with a track record of supporting their portfolio companies. The fund seeks to invest through floating rate loans in private or thinly traded or small market-cap, public middle market companies. It primarily invests in the U.S., and to a limited extent non-U.S. companies. The fund typically invests between $2M to $20M. It also has PSSL, The PennantPark Senior Secured Loan Fund. (PFLT site.)

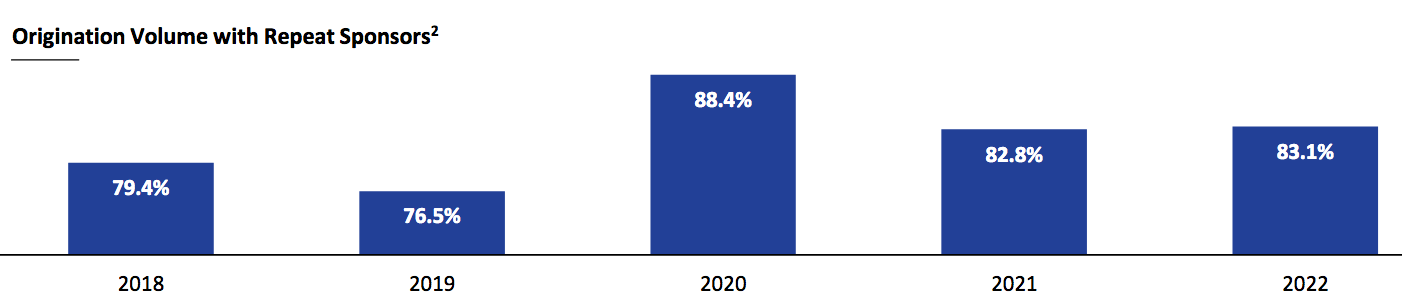

PFLT is a lender to 160+ portfolio companies across 90+ sponsors. Since 2018, over 75% of PennantPark’s deals have been with repeat sponsors:

PFLT site

Dividends

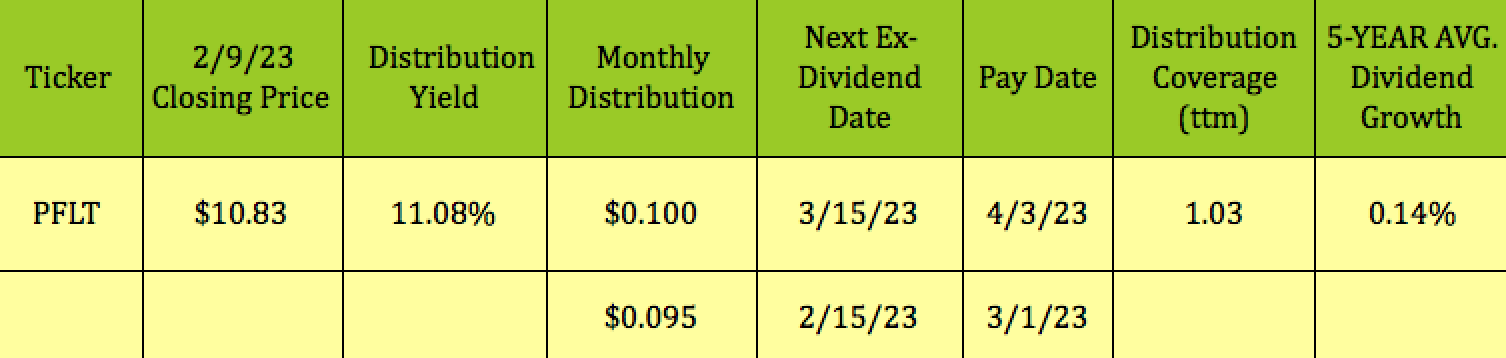

Management just raised its monthly distribution by 5%, to $.10 from $.095, where it had been since November 2018, hence the low 0.14% 5-year dividend growth rate.

There’s one more payout at the old $.095 rate, going ex-dividend on 2/15/23. NII/Distribution coverage is fair, at 1.03X.

Hidden Dividend Stocks Plus

Holdings

PFLT focuses on high-growth middle market companies in 5 key sectors: Business Services, Consumer, Government Services, Healthcare, and Software/Technology. The core middle market generally has lower leverage, higher yields, and a better recovery rate.

The target companies have EBITDA of $10-$50M, with 1st Lien leverage of 4-5.5X. PFLT’S average investment size is ~$9.4M – its debt portfolio has a 10.0% yield at cost. 87% of its investments are 1st Lien, with 13% in Subordinated Debt, and Preferred & Common Equity.

Its top 10 industry exposures account for ~55% of its portfolio, with Professional Services being its biggest exposure, at 8.8%, followed by Media, at 7.3%, Personal Products, at 6.8%, and IT Services, at 6.3%:

PFLT site

PFLT also has a JV investment fund, PSSL, with Kemper, which focuses on middle market, directly originated 1st lien loans. PSSL had total investments of $759.69M, and a 10.9% yield on investments as of 12/31/22. Management is targeting a $1B portfolio size for PSSL.

PFLT site

PFLT had 3 non-accruals out of 126 different companies, representing 1.9% of the portfolio at cost and 0.6% at market value, as of December 31.

Interest Rate Impact

PFLT’s management reckons that its interest income will rise by $.14/share for each 1% rise in interest rates. In the quarter ending 12/31/22, its interest income rose 23%, from $16.86M to $20.74M, or ~$0.086/share.

PFLT 10Q

Earnings

PFLT’s fiscal year ends on 9/30. The table below represents calendar periods – Q4 2022 was PFLT’s 1st fiscal period for 2023. Revenue growth has been strong in calendar year 2022, rising ~25%, with a ~19% jump in Q4 ’22 (period ending 12/31/22).

Net Investment Income rose ~8% in Q4 ’22 but was down -5% in calendar year 2022. Cutting into NII was much higher interest expense, which rose $3.4M in Q4 ’22, up 48.5%.

NII/Share fell 9% in Q4 ’22, from $.33 to $.30; and was down -13% during calendar year 2022, due to a 16% rise in the share count. NAV/Share declined 11%, to $11.30, as of 12/31/22, vs. $12.70 a year earlier:

Hidden Dividend Stocks Plus

PSSL had big top-line growth in the quarter ending 12/31/22, with total investment income up 67%. However, NII was down -23%, to $3.47M, vs. $4.51M a year earlier:

PFLT 10Q

New Business

PFLT invested $65.6M in 4 new and 29 existing portfolio companies, with a weighted average yield on debt investments of 11.2 %, in the 3 months ended 12/31/22. Sales and repayments of investments for the same period totaled $63M.

This was much lower than the 3 months ended December 31, 2021, in which PFLT invested $335.1M in 16 new and 36 existing portfolio companies with a weighted average yield on debt investments of 7.8%. Sales and repayments of investments for the same period totaled $238.4M.

Performance

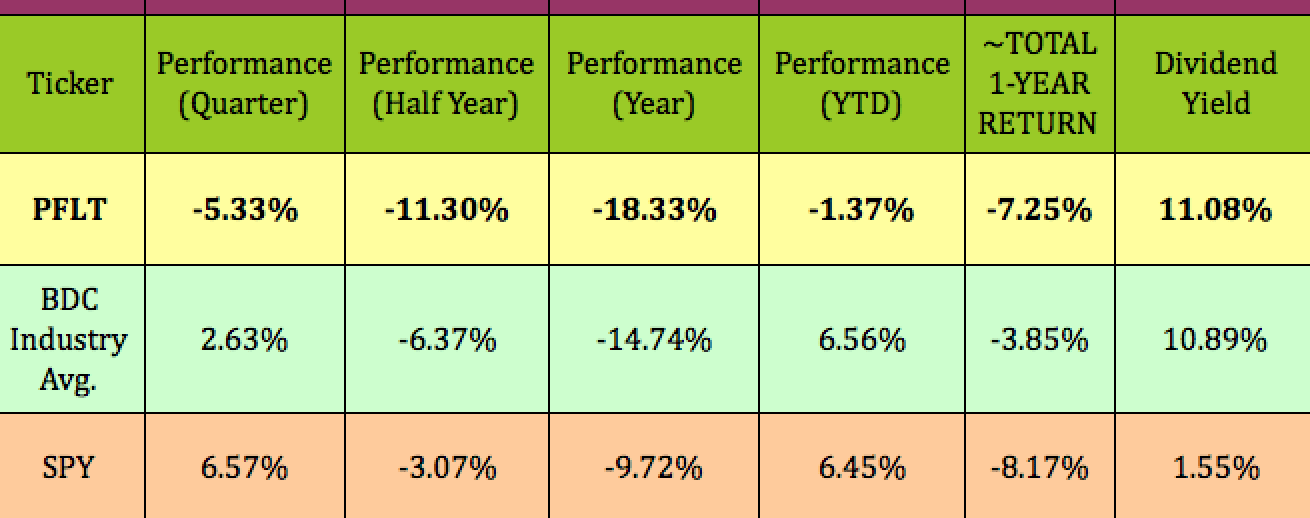

In this era of rising interest rates, you’d think that the market would have given a floating rate BDC like PFLT quite a boost, but that hasn’t been the case – PFLT has lagged the BDC industry and the S&P 500 (SP500) over the past year, half year, and quarter:

Hidden Dividend Stocks Plus

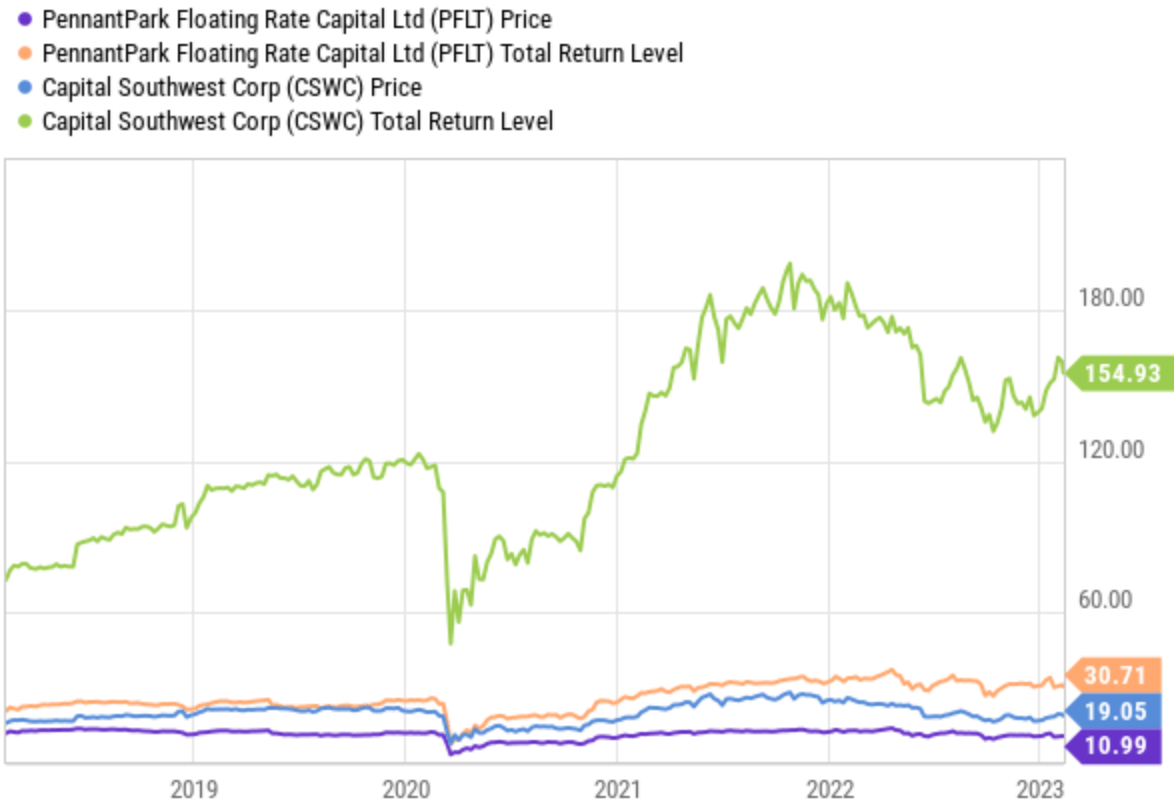

We compared PFLT’s 5-year total return to that of Capital Southwest, another BDC, we covered in an article last weekend.

PFLT doesn’t fare too well in this comparison – CSWC’s total return was ~5X PFLT’s:

YCharts

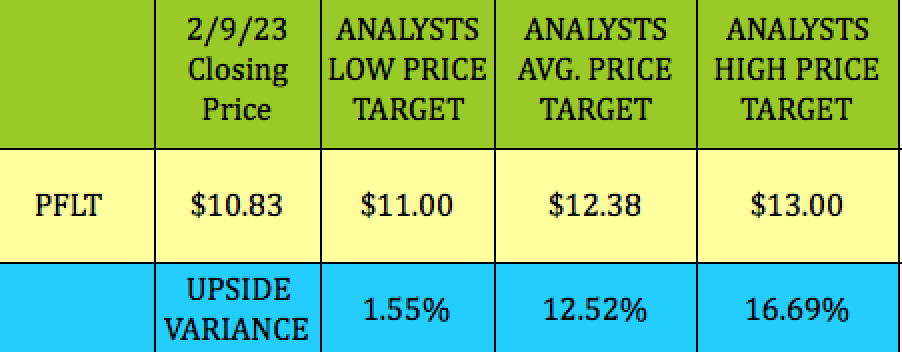

Analysts’ Price Targets

At its 2/9/23 $10.83 closing price, PFLT is 1.5% below the $11.00 lowest price target, and 12.5% below the average $12.38 price target. Its price targets have come down since August, when they ranged from $12.50 to $14.00.

Hidden Dividend Stocks Plus

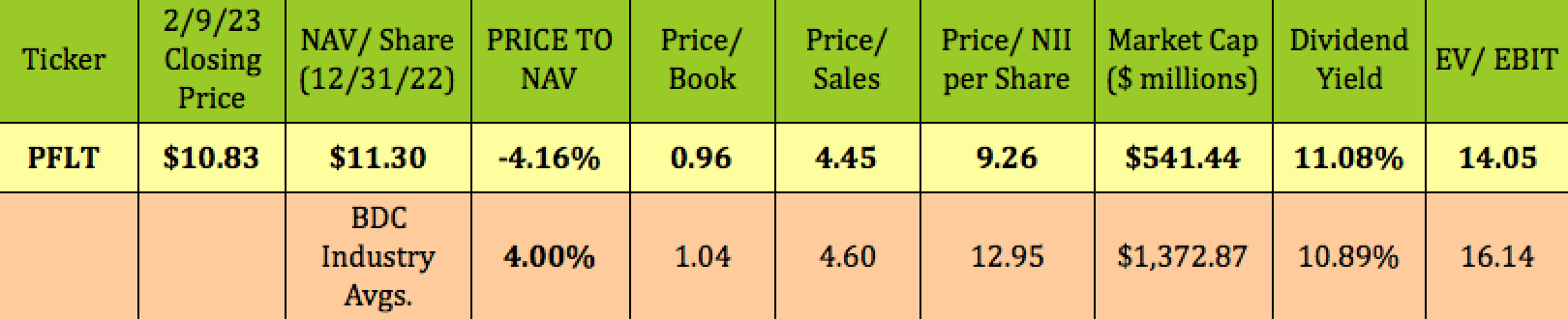

Valuations

At $10.83, PFLT is selling at a 4% discount to NAV, vs. the 4% premium to NAV industry average. It’s also selling at a cheaper P/NII per Share valuation of 9.26X, vs. the 12.95X BDC industry average. Its ~11% dividend yield is roughly in line.

Hidden Dividend Stocks Plus

Profitability & Leverage

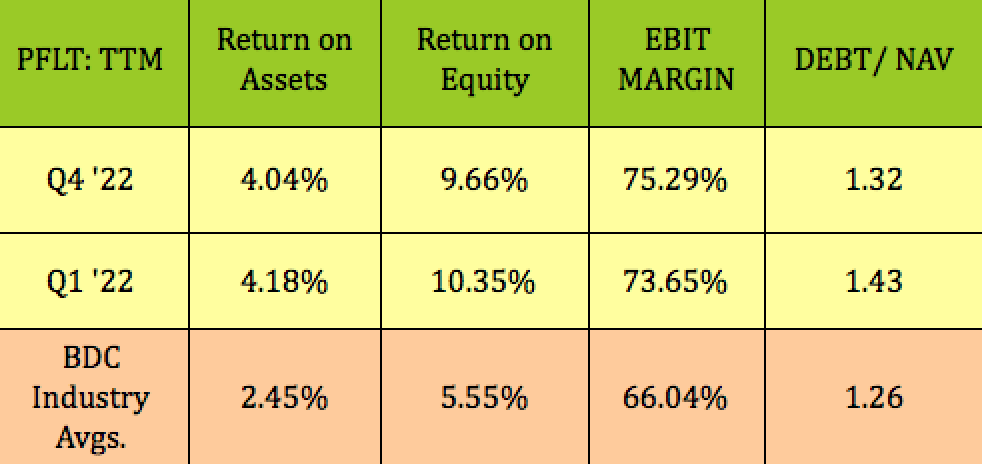

ROA and ROE have both fallen a bit since calendar Q1 2022, but both are still above BDC industry averages. PFLT’s EBIT Margin has improved, to ~75%, and is also above average. Debt/NAV leverage has decreased a bit, and is roughly in line with the 1.26X BDC average.

Hidden Dividend Stocks Plus

Debt & Liquidity

The total asset base shrank 4.7% over the past 4 calendar quarters, dropping to $1,226.68M, whereas total debt shrank ~9%, improving the Asset/Debt ratio to 1.8X. EBIT was roughly flat, but the rise in Interest expense caused PFLT’s Interest coverage ratio to drop from 2.97X to 2.52X.

Hidden Dividend Stocks Plus

PFLT issued 4.25M shares in January 2023, which raised $48M.

PFLT had ~$53M in cash, and had $166.8 in credit availability, as of 12/31/22. PSSL had cash equivalents of $52.9M.

As of 12/31/22, PFLT’s debt consisted of $197M on its Credit Facility, ~$256M in 2023 and 2026 Notes, and ~$226M in Asset-Backed Debt, due 2031:

PFLT site

Parting Thoughts

While PennantPark Floating Rate Capital has “floating rate” in its name, it seems that it isn’t benefiting as much as some other BDC’s from rising rates. The additional share issue in January is also a ~9% dilution. The distribution hike was a positive move, but, we’re passing on PFLT for now, in favor of other BDC’s.

If you’re interested in other high yield vehicles, we cover them every Friday and Sunday in our articles.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment