SBDIGIT/E+ via Getty Images

Where investors should allocate their money?

Fed appeared to keep raising interest rates and may have kept them there for the rest of 2023, at or above 5%. Therefore, we think that in 2023, the majority of businesses may experience uncertainty.

In this environment, investors, in our opinion, should allocate funds to three types of stocks:

(1) stable cash flow stocks,

(2) stable and high dividend stocks, and

(3) growth stock with positive cash flow.

In our opinion, Peloton Interactive, Inc. (NASDAQ:PTON) is about to match both (1) and (3).

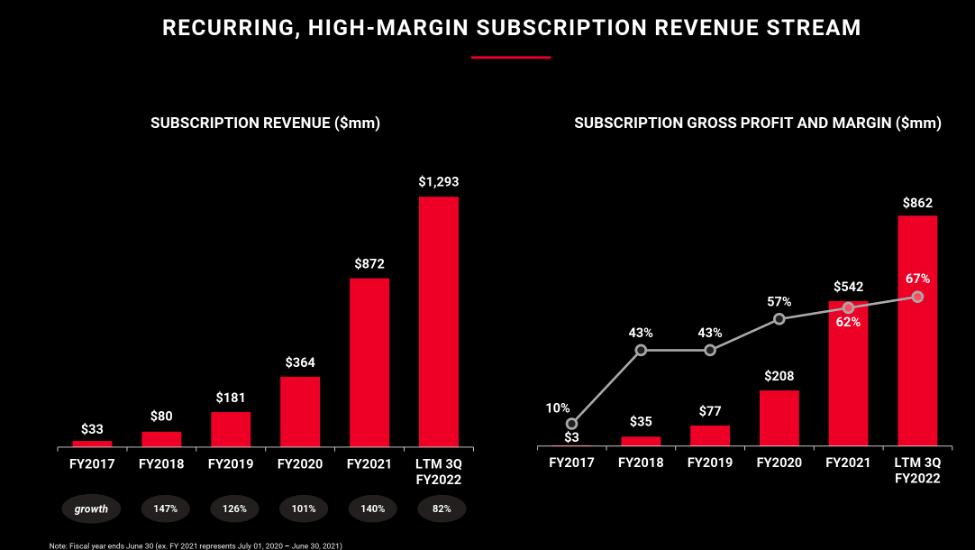

Peloton continues to grow subscription revenue year over year.

Peloton subscription revenue stream (Company’s presentation)

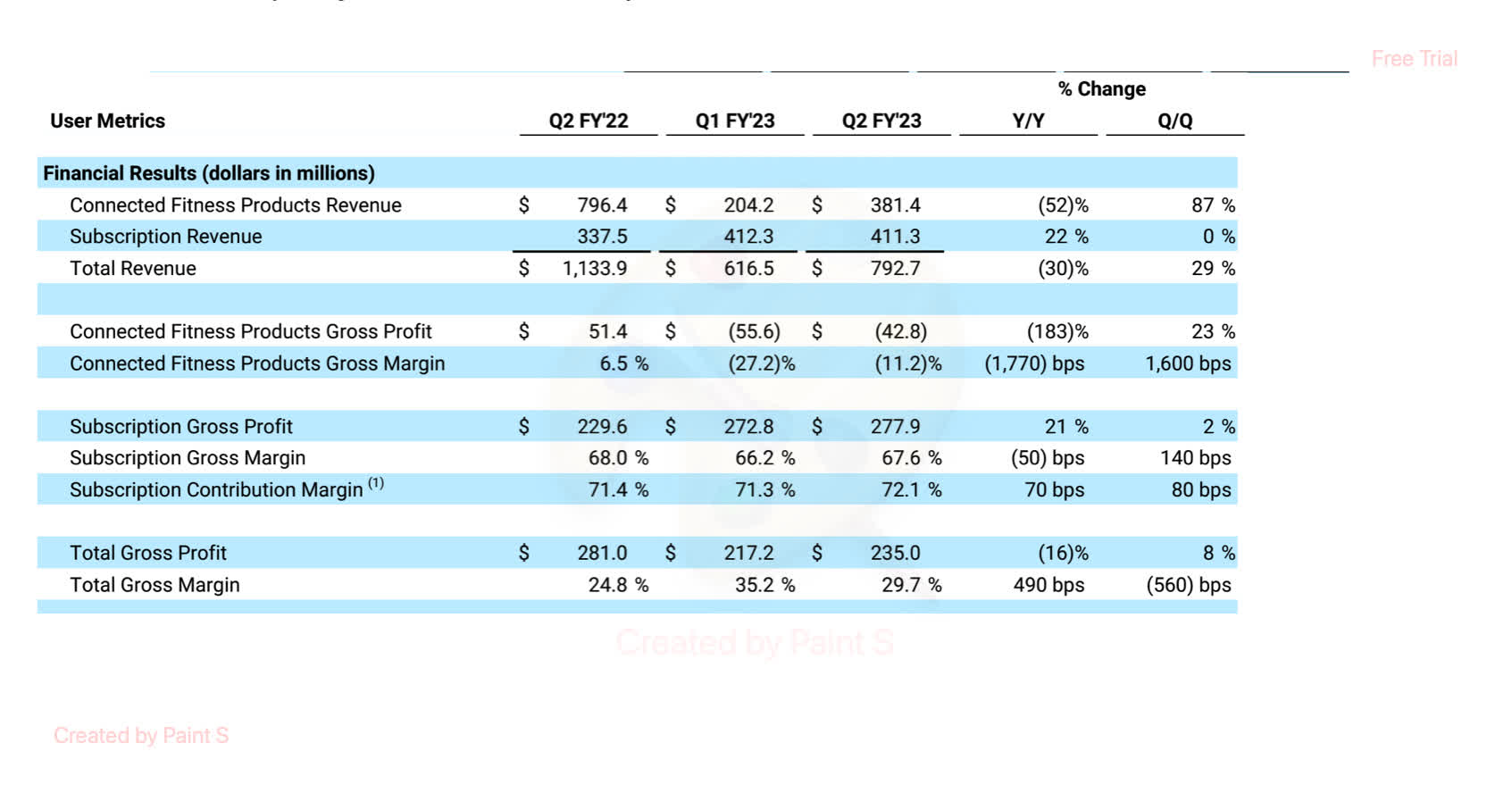

Its subscription business now makes up the majority of the gross margin, surpassing product revenue.

Revenue and gross margin breakdown (Company’s filing)

Given that the firm has a $5 billion market valuation, we think that the current market is pricing it as a growth business that has been discounted because of its poor cash flow. Hence, we believe that this company’s fundamentals are sound, and its steady cash flow from subscription business supports it moving forward.

In addition, according to management, the loss is decreasing and will soon reach cash flow breakeven in two quarters. As a result, PTON stock ought to be relatively safe in comparison to other growth stocks and offer sufficient potential.

Myth Vs. Fact

In the last three years, Peloton’s stock has gone through a spectacular boom and crash, and it is frequently mocked as one of those epidemic winners. Looking at the metrics below, fact could, however, speak louder than words.

Shining operating metrics

Relatively low churn rate

While Peloton had a monthly turnover rate of primarily around 1% before the epidemic, and even after the outbreak is gone, the peak churn rate is only at 1.4%, it took Netflix over 10 years to reduce its monthly churn rate from 10% to under 2%.

number of member and churn rate (Company’s filing)

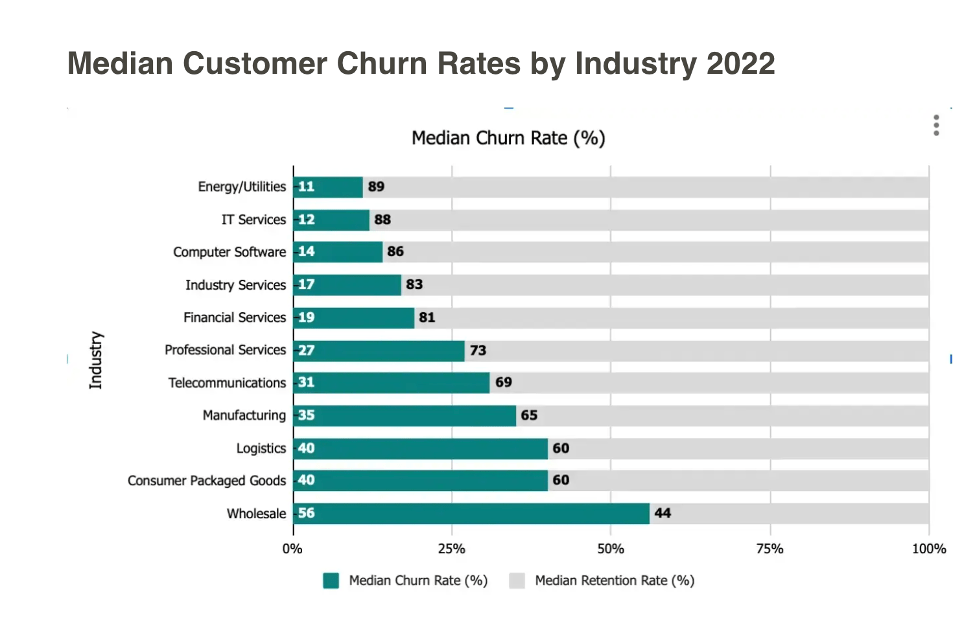

According to CustomerGauge, the annual median churn rate for energy/utilities will be 11% in 2022, which is the lowest among industries. Recalculating Peloton’s annual churn rate, we find that it was roughly 10% prior to the epidemic. Can you believe Peloton consumers appreciate the service and remain loyal to it the same way you remain loyal to your energy provider? Even after the epidemic, it peaked at 16.8% before falling to 13.2%. It is akin to computer software or IT services, which continue to be at the very top of the ranking chart.

Customer churn rates by Industry (CustomerGauge)

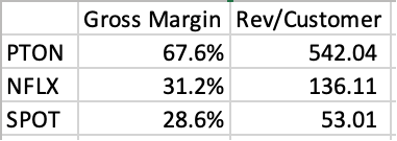

Significantly high gross margin and Revenue per customer

Investor can see that Peloton ranks first in both gross margin and revenue per customer when compared to the below subscription stocks, Netflix (NFLX) and Spotify (SPOT). Peloton customers spend $542 year on average, roughly four times what Netflix and ten times what Spotify users do.

Ratio and metric (Company’s filing)

It is because (1) people are willing to spend more for exercise than other people are, (2) Peloton’s content production costs are significantly lower than others’ and could be reused much more frequently than others.

The majority of Peloton’s customers care about their health

A Peloton client recounted his story in the Peloton official Facebook page, describing how he grew tired with the product after three months and returned to it after buying new monitors, only to get bored once more shortly after. And only when he decided to return after realizing he had a serious health problem. He eventually started using frequently.

This testimony demonstrates the reality that people exercise for a variety of reasons, but those who exercise for health reasons stand to gain the most from Peloton’s goods and services.

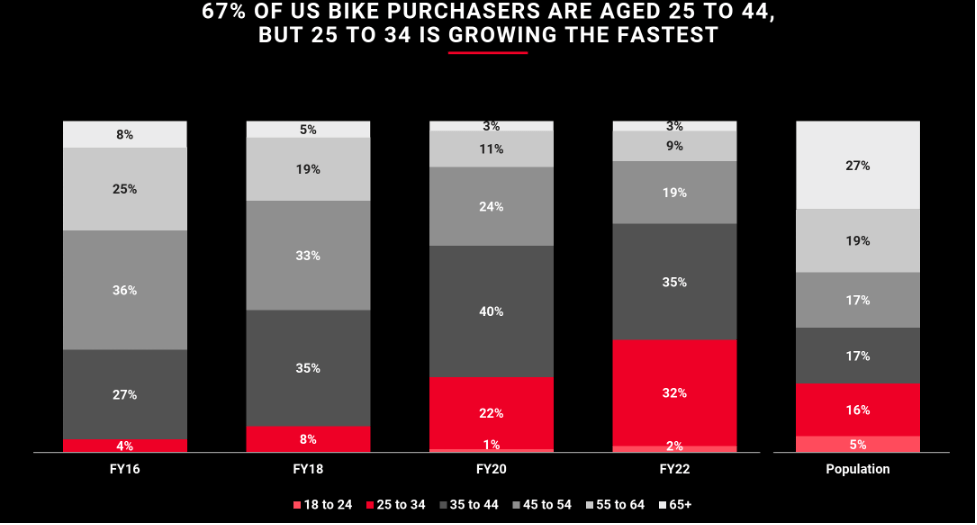

Age 25-44 account for 67% of US bike purchases, according to Peloton, and 35 and above account for nearly 79%.

US biker purchasers by ages (company’s presentation)

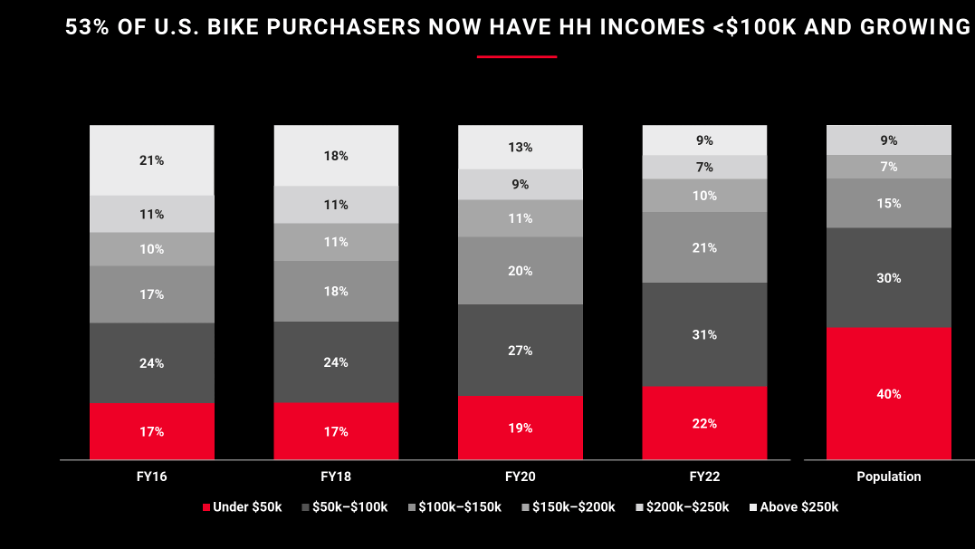

Also, 61% of US bike purchase have income over $50K.

US bike purchasers by income (company’s presentation)

It supports our premise that Peloton’s primary target market is those who are concerned about their health. They prioritize health and are prepared to pay for it.

Convenience, tracking and community

These consumers’ problems were actually resolved by Peloton by giving them the chance to (1) work out on demand and without the burden of travel and (2) keep track of their health status and rank exercise output with others.

Travel is a problem for traditional gyms. Running near your home with a fitness tracker can help you reach the first and a portion of the second goals, but it won’t provide you a clear picture of how you compare to your peers in terms of health. People who are concerned about their health want to monitor more than just the number; they also want to know how they are doing compared to the group and whether they are improving over time. I’ll say that fitness trackers and watches have some potential competition risk for Peloton, but it’s not a huge issue because (1) they don’t have a set exercise routine to make the leaderboard really work, and (2) they are built for other purposes as well, like phone calls, messaging, music, and so on, making it not concentrate on the fitness.

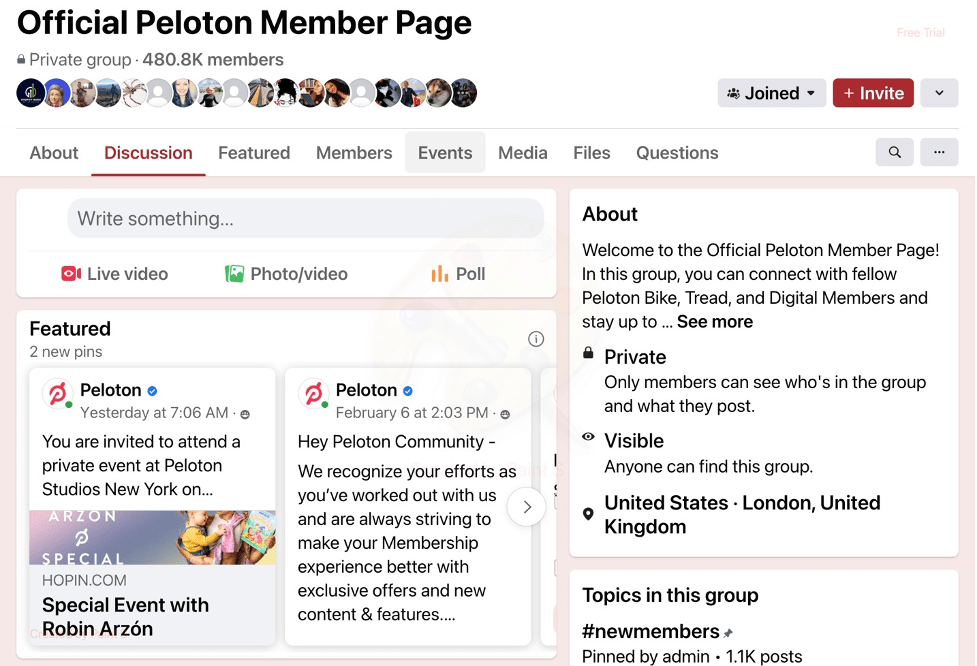

Community is a great way to witness the testimony

Establishing a Facebook page gives customers the opportunity to share their experiences with others, which is crucial for those looking for a solution to a health condition.

Peloton Facebook page (Facebook)

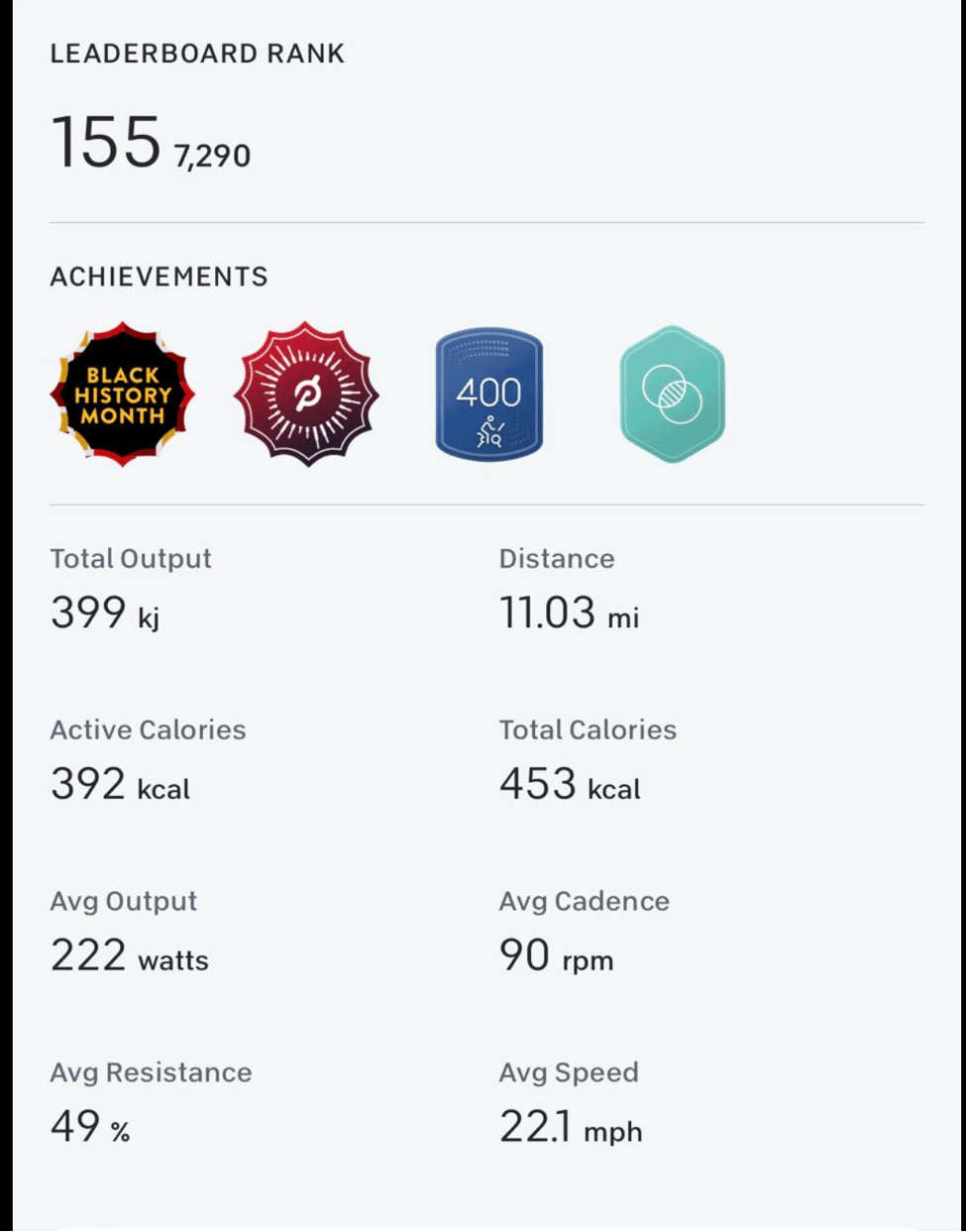

Additionally, the introduction of leaderboards offers clients a fantastic opportunity to assess their development inside a specific training environment. For identical reasons, many are prepared to pay and train for marathons. They desire to maintain their health, experience success, and be aware of how they rank among their peers. We believe that as Peloton’s community expands, the value of the leaderboard ranking may increase.

Peloton Leaderboard Rank (Company’s filing)

Healthcare TAM is larger than that of fitness

Therefore, if you consider Peloton to be a fitness company, the company estimates that there are just 185 million fitness members worldwide. That TAM is comparatively tiny. Not to mention, individuals visit fitness centers for a variety of reasons, including social, physical development, and others. From this angle, Peloton may have a lot of competition. However, if you consider Peloton as a healthcare provider. According to the National Library of Medicine, around one in three persons worldwide have numerous chronic diseases (MCCs). In this light, the TAM is significantly larger.

Currently, people typically choose one of the following treatments for chronic conditions: take medicines or exercise. Typically, a doctor or hospital can only offer you advise when it comes to exercising. We think Peloton’s introduction of health data tracking and community greatly aids certain people in getting over their exercise inertia and developing a long-lasting exercise regimen through the subscription service. That, in our opinion, is what actually explains the high retention rate and what motivates peloton enthusiasts.

Management’s turnaround story

Many clients use Peloton solely to work out as a substitute for the gym during the pandemic. These clients now have other options if they only want to exercise after the pandemic. And it’s true that management erred by expanding their manufacturing since they miscalculated the demand. After the pandemic, when people started leaving the house again, the churn increased to 1.4%.

The management has acknowledged that they underestimated demand, but they are nonetheless confident that they are still fulfilling the interests of their core clients. This is why their turnaround strategy includes starting to roll out new items like guides and rows and outsourcing production to a different company. The ideal approach, in our opinion, at this point is to emphasize cardio more, provide more product options, and provide tools for customers who exercise for health reasons to log and monitor their exercise. We believe that they might eventually widen the peloton community and build the final moat for the business.

Valuation

Assuming Peloton only captures 1% of the chronic condition client market (0.33% of total world population). 3% terminal growth rate, 18% WACC, and a free cash flow margin of 15% are assumed. Through Discount Cash Flow analysis, we get at a 14 billion equity value, which has a potential 178% return on the present price.

In its 10-K, Peloton stated that around 10% of their sales originated from the international market. Therefore, if we estimate that 90% of subscribers are in the US, we arrive with a market share of about 0.8% in the US. Our estimate of 1% of the global population with chronic conditions(0.33% of total global population) looks conservative. Investors should only consider the valuation to be expensive if the free cash flow margin falls below 5%, according to the following sensitivity analysis of the free cash flow margin and WACC.

Sensitivity analysis for WACC and FCF% (LEL Investment)

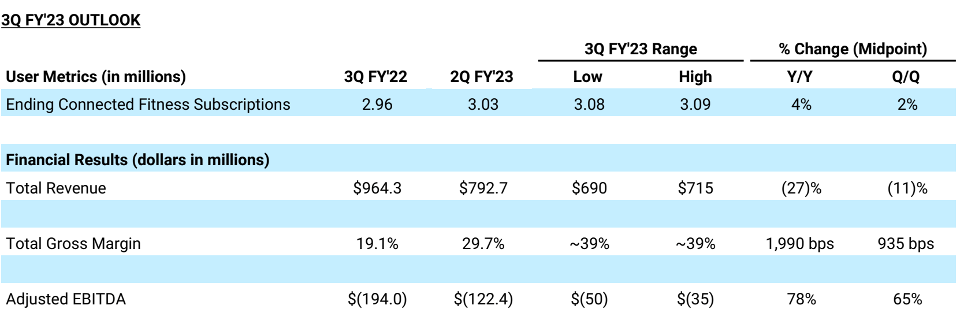

According to the company’s 3Q earnings report, there is a strong trend toward reducing the Adjusted EBITDA loss and improving margin expectations. Additionally, the company anticipates that in the upcoming fiscal year it will attain cash flow breakeven and resume worldwide growth (within 6 months). In our opinion, it is now appropriate to add to and build up a position in this stock.

Management outlook (Company’s filing)

Timing

We believe that an earnings report demonstrating improvements in (1) free cash flow, (2)connected fitness subscriber addition, and (3)low churn rate would persuade investors to support the company’s recovery strategy.

In addition, the subscription business’ steadfast success has already given some fundamental investors significant confidence to buy in this quarter. We think this subscription stock could potentially be favored by the market even as macro uncertainty persists. The stock could therefore increase even before the company reports higher profitability and overseas growth.

Risk

Competition risk

Since most other organizations place a greater emphasis on fitness than healthcare at this time, we feel that the danger of competition is rather low. Therefore, we believe Peloton is still in the early stages of revolutionizing the healthcare sector.

Oversea expansion risk

The valuation is based on the company’s performance in international expansion. Peloton’s revenue climbed nearly thrice, from 82 million in 2020 to 322 million in 2022, as a result of its successful expansion into Germany, the United Kingdom, and Canada. The risk of enlargement is minimal at this time. Investors, however, need to pay strict attention to progress.

Cash flow risk

However, we can observe that management made a decision to close its factory, outsource manufacture to a third party, and focus on inventory management. Inventory turnover ratio increased from 1.77x to 2.3x, and inventory declined from a peak of 1.5 billion in 2Q22 to 709 million in 2Q23.

Inventory, COGS and ratio (Company’s filing)

Although we believe that the overall light asset approach is effective, the cash flow risk should be monitored. Hence, any decrease in shares because of a cash flow shortfall could also be considered another entry.

Be the first to comment