Joe Raedle

Few companies have been as troubled this year as Peloton (NASDAQ:PTON). After spending much of the pandemic dealing with supply chain issues in the wake of unprecedented demand, Peloton struggled with the opposite problem: waning demand in the post-COVID world as people resumed normal routines and gyms re-opened. It also suffered serious reputational damage from the recall of its treadmill products that still lingers in the minds of some consumers.

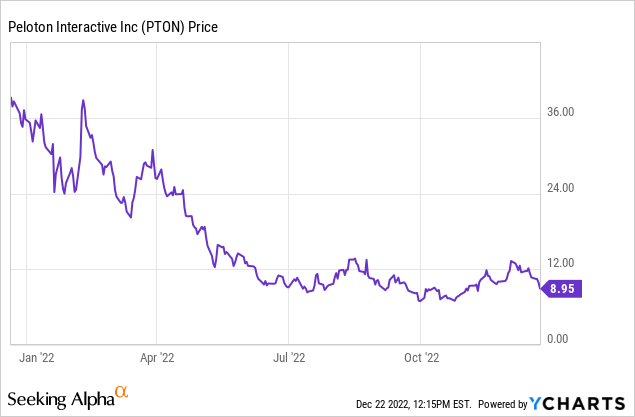

Year to date, shares of Peloton have shed 75% of their value. Amid the wiping-off of billions of dollars of market value, I finally think there is some salvage value in this stock:

I am bullish on this name. While there is certainly near-term executional risk as Peloton continues to roll out its turnaround plan, I think the stock’s ultra-low valuation provides safety cover for investors who are willing to shoulder the near-term volatility.

Here, in my view, are the reasons to be bullish on Peloton:

- Fitness as a Service – At its IPO, Peloton was mainly a low-margin hardware vendor. Subscriptions made up barely one-fifth of the company’s revenue: now, it’s well over half. Subscriptions are also clocking in at a 70%+ gross margin, and churn is very low in the ~1% range. Over time, the company’s strategy seems to be to use hardware as a gateway product to get subscribers through the door. Once investors start viewing Peloton as more of a subscription/software company, its valuation multiple will slide up.

- A subscription for everyone – Peloton has three tiers of membership: a $13 app-only membership, a mid-tier $24 “Peloton Guide” subscription, and the full-on $44/month All Access subscription. These offerings help broaden Peloton’s appeal to both casual and dedicated workout enthusiasts.

- Economies of scale – Outside of hardware production, Peloton’s largest expenses are in content production (hiring fitness instructors and paying for music licensing rights). As the company’s subscriber base swells, these fixed costs will dwindle as a percentage of revenue.

- Secular tailwinds – Health and fitness have become top-of-mind buzz topics, and Peloton remains a status-symbol purchase. In addition, hybrid lifestyles and hybrid schedules (working partially at home, and partially at the office) have encouraged many to have at-home fitness options. In other words, the fact that gyms have reopened doesn’t necessarily crowd out the utility of a Peloton at home.

Stay long here: there are plenty of catalysts to lift Peloton higher in 2023, which we’ll discuss in detail next.

The growing importance of subscriptions

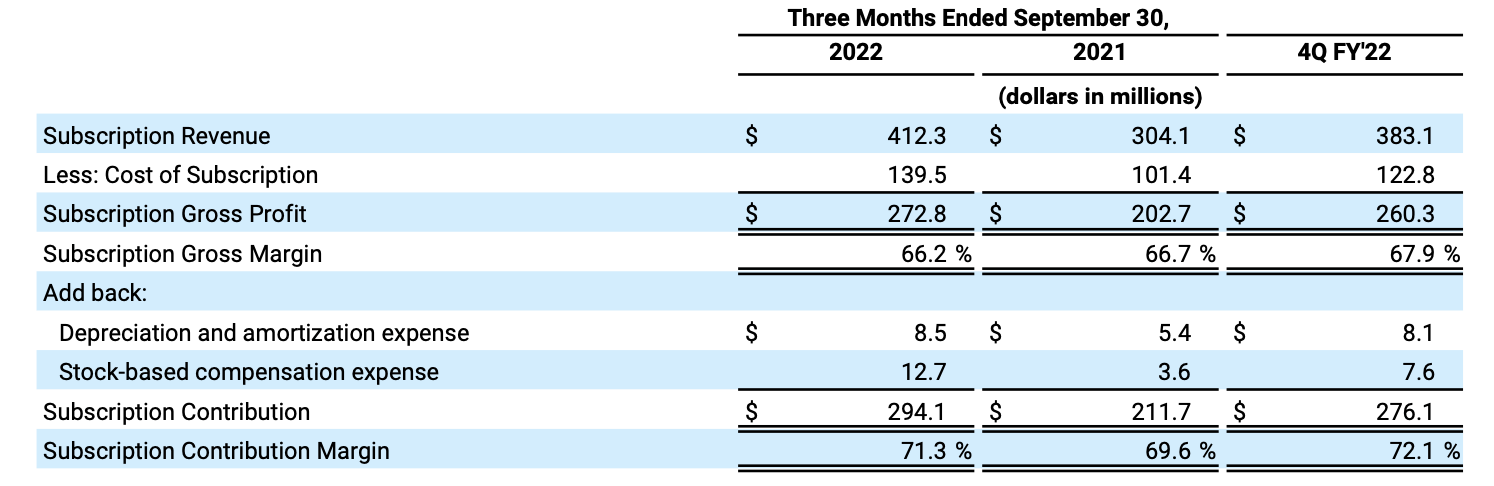

In Q1, Peloton achieved a stunning 36% y/y growth rate in subscription revenue to $412.3 million. Subscriptions accounted for 67% of overall Q1 revenue – versus just 38% in the year-ago quarter, when the company was still catching up to red-hot hardware demand.

Peloton Q3 highlights (Peloton Q3 shareholder letter)

The growth in subscription revenue is driven both by a 19% y/y increase in overall connected fitness subscriptions to 2.97 million, as well as a price increase (recall that in August of this year, the company raised its All Access subscription to $44/month, a hefty jump from a prior price of $39/month. The company justified this increase by noting that in 2014 at its outset, the company was producing less than 400 classes per month with only six instructors; now, it has 54 instructors producing more than 1,000 classes per month).

In spite of this price increase, churn of 1.1% has remained basically flat to historical levels. This further elevates the argument that Peloton is becoming more of a stable-ARR software company.

Note that the company is guiding to 3.0 million Connected Fitness subscribers in Q2, adding 27k net-new subscribers for the December quarter – up from just 7k in the September quarter.

The rise in subscription revenue is also a key driver of margins. In itself, subscription contribution margins (a pro forma margin measure, excluding stock comp) are up 170bps y/y to 71.3%. Secondarily, the mix shift into subscriptions versus hardware has Peloton’s overall company gross margins up to 35.2% in Q3, up 260bps y/y.

Peloton subscription margins (Peloton Q3 shareholder letter)

This, on top of a deep restructuring that has overall Peloton headcount at slightly over half of its 2021 peak (per the New York Times), has helped Peloton slim down its adjusted EBITDA loss in Q3 to just -$33.4 million: a near-breakeven -5.4% margin, a twenty-four point improvement versus -29% in the year-ago Q3.

Peloton adjusted EBITDA (Peloton Q3 shareholder letter)

Peloton Row and channel partnerships

Just because Peloton is focusing more on subscription revenue doesn’t mean the company isn’t still pushing to expand its hardware products reach as well.

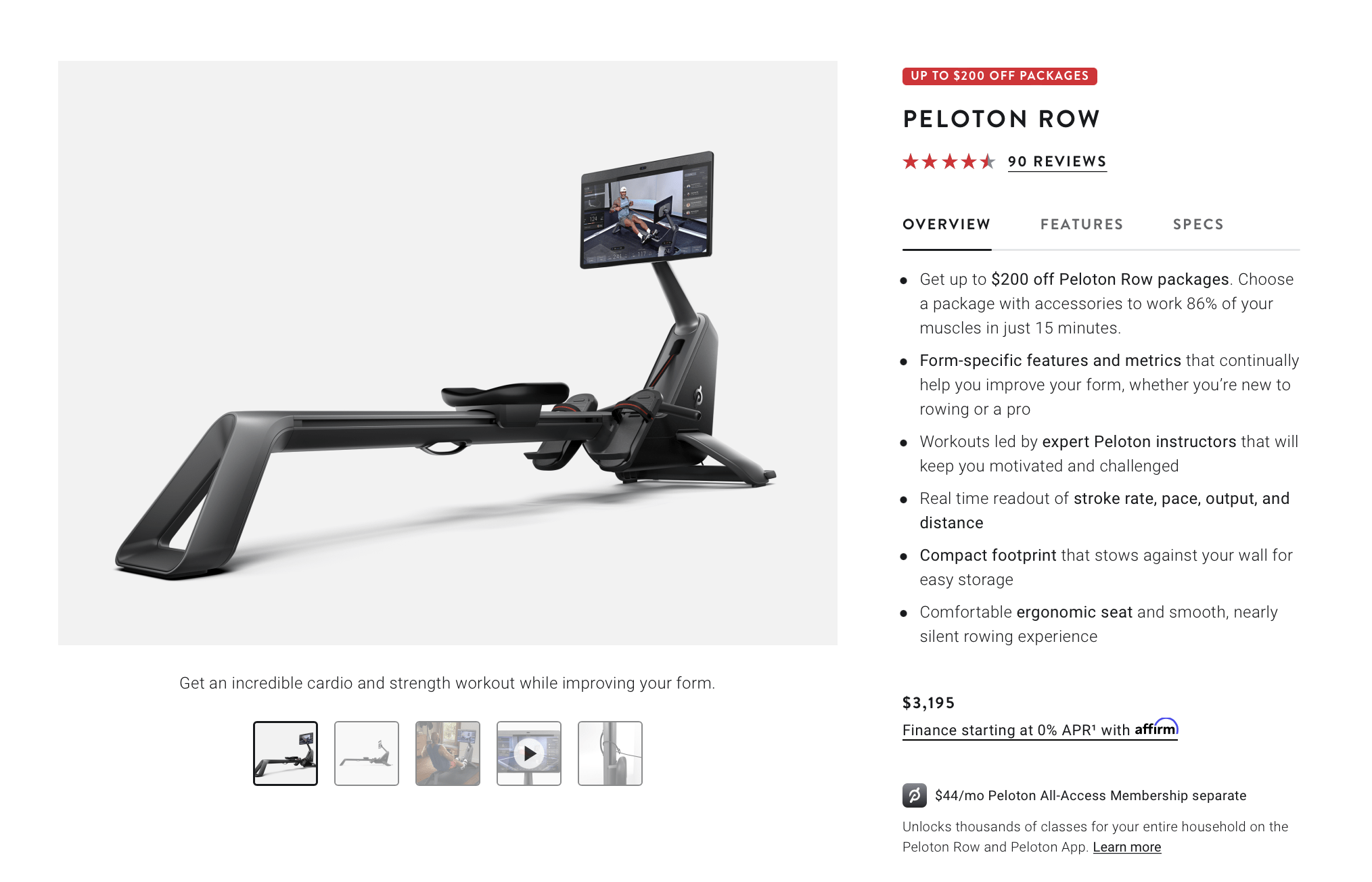

This fall, the company unveiled the new $3,195 Peloton Row, a perfect companion alongside the company’s bike and treadmill products.

Peloton Row (Peloton.com)

Per CEO Barry McCarthy’s comments on the Q1 earnings call, the company is experiencing high demand for the now-constrained Peloton Row, and management expects the category to continue growing over time.

With respect to Row, I think Tom Cortese and his team can be justifiably proud in having reinvented the Row category like they reinvented the bike category with the Connected Fitness content. The good news and the bad news about Row is for this fiscal year, we expect to be inventory constrained and they have more demand than we will have units to sell, and we’re working to address those issues.

But at least for the moment, it’s been critically quite well received. We have just rolled it out through all of our showrooms as of yesterday, in a limited number, like 16. And so I expect the demand for Row to continue to grow as we increase people’s exposure and the opportunity to get on and try it and see what’s mass about it.”

Peloton has also deepened its channel relationships. Peloton products, as of November (after the end of the second-quarter report), are now available in over 100 DICK’s Sporting Goods (DKS) stores. The company also announced that Peloton bikes will now be featured at every Hilton (HLT) hotel in the United States, with free 90-day trial subscriptions offered to Hilton Honors members.

Valuation and key takeaways

At current share prices just under $9, Peloton trades at a market cap of just $3.02 billion. After we net off the $938.5 million of cash and $992.1 million of debt on the company’s most recent balance sheet, Peloton’s resulting enterprise value is $3.07 billion.

For the current fiscal year, meanwhile, Wall Street analysts are expecting Peloton to generate $2.67 billion in revenue. If we take a conservative approach and assign no value to the company’s zero/low-margin hardware revenue, and assume a 67% revenue mix on the year (flat mix to Q1, and a ~$447 million quarterly subscription revenue run rate compared to $412 million in Q1), we arrive at $1.79 billion subscription revenue for the year and a multiple of just 1.7x EV/FY23 expected subscription revenue.

To me, that is a very safe multiple worth buying.

Be the first to comment