Michael Vi

Thesis

We highlighted in our post-earnings update that investors should capitalize on the dip in Palantir Technologies Inc. (NYSE:PLTR) stock, even as the market was concerned with the significant slowdown in its government growth cadence.

However, PLTR was caught in the recent broad market downdraft, sending it down further as it underperformed the market. As a result, PLTR last traded close to its June lows, giving investors another fantastic opportunity to add more aggressively.

We are confident that PLTR has already formed its long-term bottom in May, which should hold resiliently through the recent pullback. Furthermore, the rapid sell-off in PLTR over the past month is consistent with moves to force capitulation for the weak hands who chased the summer rally.

Therefore, we urge investors to hold their positions resolutely, given the battering and more attractive valuation. Palantir could continue to experience near-term downside volatility, given its downward momentum. However, we urge investors to look ahead. We surmise the reacceleration in its revenue growth should lift buying sentiments and its operating leverage.

As a result, we deduce the stars are pretty much aligned for investors to consider adding more exposure, riding the potential next wave up with the broad market.

Too Much Fear, But Palantir’s Valuation Held Steadily

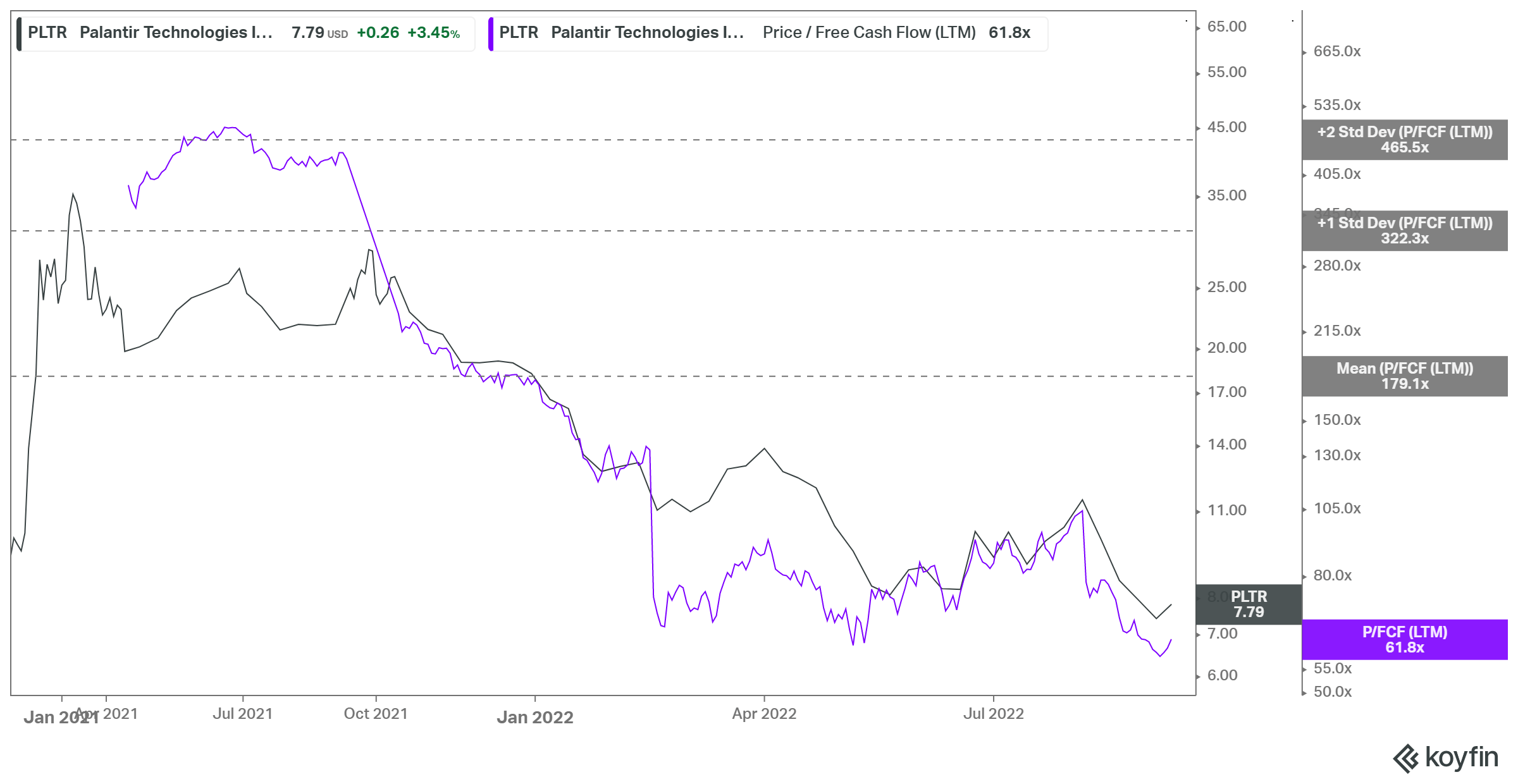

PLTR TTM FCF multiples (koyfin)

PLTR last traded at a TTM free cash flow (FCF) multiple of 61.8x, close to its lows in May. Even though it still traded at a discernible premium, given its growth profile, that level has been supported robustly. As a result, the battering from PLTR’s August highs has improved its valuation remarkably, as it collapsed nearly 38% to its August lows. We surmise that a further fall is unlikely, as Palantir is projected to recover its FCF margins through FY24.

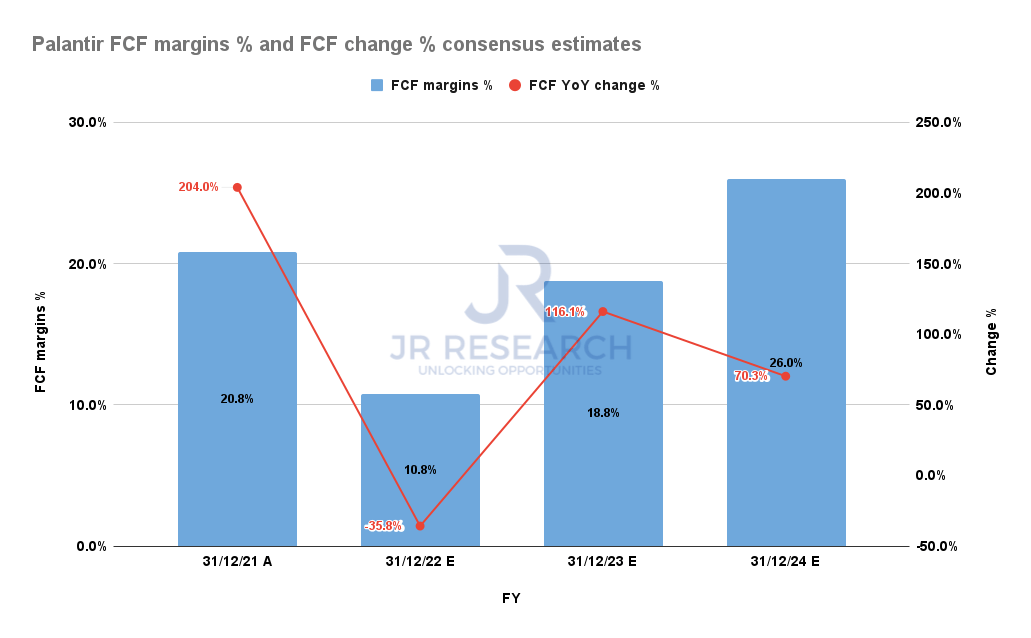

Palantir FCF metrics consensus estimates (S&P Cap IQ)

Furthermore, even the neutral consensus estimates suggest that Palantir’s malaise is not structural but likely transitory, given the challenging enterprise IT environment in H1’22. Palantir has also been impacted by forex headwinds, given its ex-US revenue exposure of nearly 39% in Q2. Coupled with the worsening macro headwinds in Europe, we believe investors adjusted their expectations on Palantir’s recovery cadence through FY23.

As a result of the market’s and Street’s pessimism, Palantir would have much easier comps to lap in FY23. Moreover, as seen above, Palantir’s FCF growth is expected to bottom in FY22 before growing by 116% in FY23. Therefore, we are confident that these estimates suggest that Palantir’s competitive moat has not been eroded but merely a momentary slowdown in deal closures.

Furthermore, Palantir’s platform also demonstrated its effectiveness and capability in the recent California wildfires. Major utility players depended on Palantir’s platform to manage their risks. Citi (C) highlighted in a recent commentary:

There’s a lot to do to mitigate fire risks. [Palantir] offers what it calls operational artificial intelligence to help manage the complexity. Palantir’s technology even creates a meta-constellation of satellites that aggregates and analyzes imagery to help utilities and first responders. – Barron’s

We believe Palantir’s unique role as a leading AI/ML platform has few close competitors. Forrester also corroborated our conviction as it rated Palantir a clear leader in the Forrester Wave: AI/ML Platforms, Q3 2022. It accentuated: “Palantir is rooted in building data-driven intelligence applications for complex, high-value government and commercial use cases.”

Hence, we believe the momentum in those large contract deals would accrue to Palantir as macro headwinds subside. It’s our conviction that macro headwinds have already reached their peak hawkishness, as we explained in our recent articles on the ProShares UltraPro QQQ ETF (TQQQ) and the ARK Innovation ETF (ARKK). Therefore, we deduce that the broad environment should be more conducive for high-growth stocks like PLTR moving ahead.

Is PLTR Stock A Buy, Sell, Or Hold?

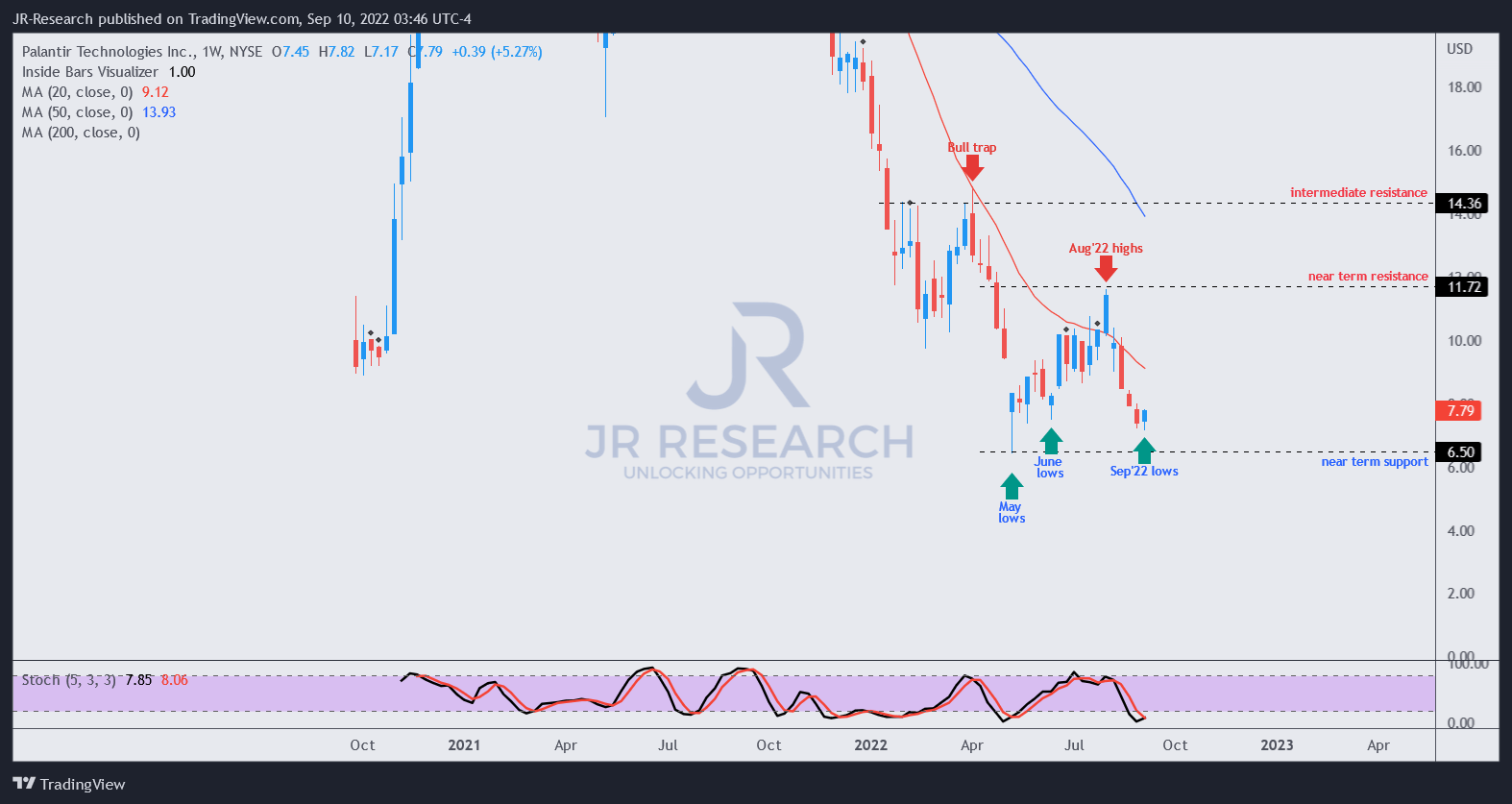

PLTR price chart (weekly) (TradingView)

PLTR’s price action remains constructively configured even as it closes in on its June lows. As seen above, PLTR’s rapid selldown has created a bear trap (indicating the market denied further selling downside decisively), predicated against June lows.

Therefore, if PLTR can continue to base robustly in the next few weeks, we surmise that the sellers are likely getting exhausted. However, investors are encouraged to layer in, given the potential downside volatility.

Notwithstanding, we like the price action, coupled with oversold momentum indicators. Therefore, we postulate that PLTR is well-positioned to stage its bottoming process, corroborated by our assessment of its valuation and improved FCF profitability, as discussed earlier.

As such, we reiterate our Buy rating on PLTR.

Be the first to comment