Scott Olson

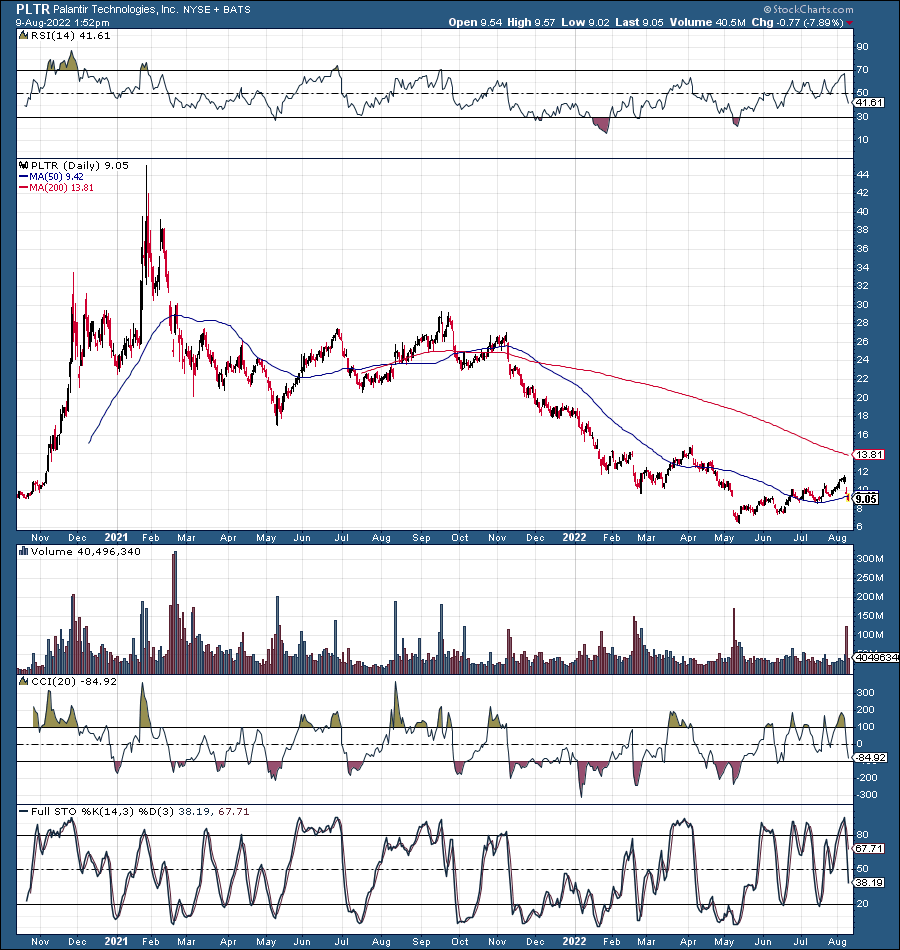

Palantir Technologies Inc. (NYSE:PLTR) is taking over the world, and you’re worried about one earnings announcement? Instead of posting a small profit of three cents per share, Palantir reported a loss of one cent per share. Many investors did not take the news well, and Palantir ended Monday’s session down by about 14%. Additionally, Palantir dropped by another 8% by late Tuesday’s session.

PLTR (StockCharts.com)

Moreover, Palantir’s stock is still down by about 80% from its ATH, floating around its IPO price from almost two years ago. However, Palantir is a high-growth company with a highly long growth runway. Furthermore, Palantir demonstrates substantial profitability potential and should become increasingly profitable with time. Also, as a Palantir investor, I am more focused on the 250% YoY increase in the U.S. commercial customer count rather than the one-cent loss.

Palantir is a rapidly growing monopolistic-style company that has the potential to take over the world. No, not literally, but Palantir’s software products and services are being adopted by more and more agencies and companies in the U.S. and globally. Therefore, Palantir should continue expanding operations, growing revenues, and increasing profits as the company advances. This dynamic should lead to increased demand for the company’s shares, and Palantir’s stock price should appreciate considerably in the coming years.

Palantir is a monopolistic, high-growth company with a remarkably long growth runway and massive profitability potential. Moreover, Palantir has a significant competitive advantage – the U.S. government. U.S. government agencies prefer Palantir, and for a good reason. Before Palantir’s solutions, agency databases were “siloed,” forcing users to search specific databases individually. Now, everything is linked together using Palantir. For example, thanks to Palantir, the FBI can access critical data from a police department without going through miles of red tape.

There is some mystery about what Palantir does and what makes the company unique. In essence, Palantir’s software combines various operational elements, making them work seamlessly and safely. Palantir could also be viewed as the master of data, and critical information, a remarkably profitable business in this age. Many market participants are too busy “counting pennies” rather than concentrating on the future.

I’ve said that Palantir does not need to be profitable now because specific companies (like Palantir) can increase profitability when their growth potential begins running out. For now, it does not matter if Palantir makes a modest profit or reports a slight loss in the greater scheme of things. It is enough that Palantir demonstrates the potential for significant profitability down the line. For now, Palantir should continue focusing on growing customer count, increasing revenues, hiring and retaining top talent, and providing the best products and services in its industry.

Furthermore, Palantir has worked closely with numerous government agencies for years, adding to the perception that Palantir is the most trustworthy company in its space. Thus, we see the continuous growth and increased interest in Palantir’s solutions from commercial clients. Around this time last year, Palantir only had 39 corporate clients in the U.S.; now, that number is 119. In addition, Palantir’s products are very sticky and have high switching costs. Therefore, once on Palantir’s software, a company should become a long-term consumer of Palantir’s products and services.

Q2 – Better Than The Initial Reaction

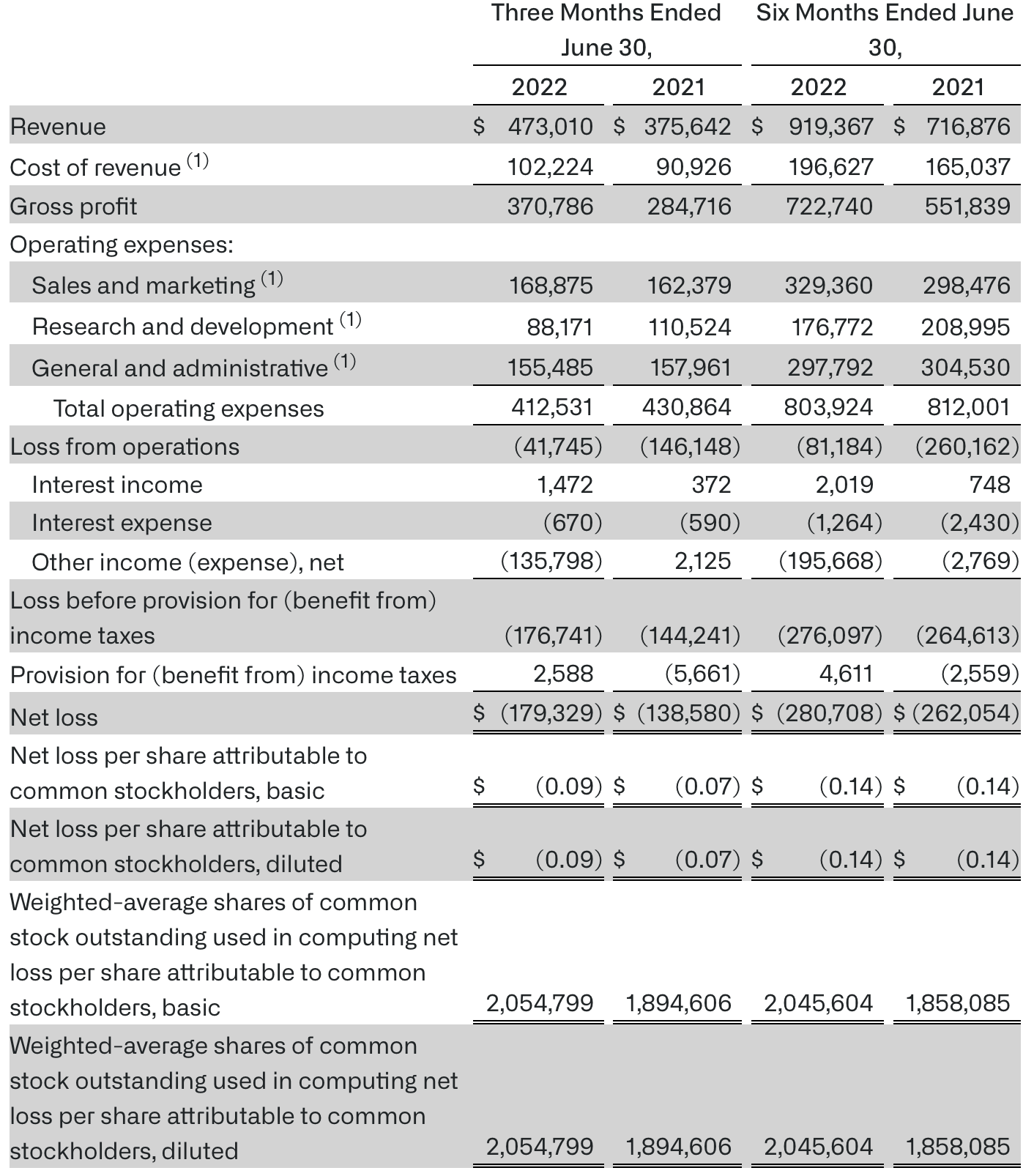

Statement of Operations

Statement of operations (Investors.palantir.com )

We continue seeing robust revenue growth while the cost of revenue declines. YoY revenues jumped by 26%, but the cost of revenue increased by only 12%. Gross profit came in at $370.8 million, surging by 30% YoY. Therefore, we see Palantir becoming increasingly profitable with scale. This trend of higher profitability is constructive and should continue, becoming more pronounced as the company continues expanding operations and revenues in future years.

Additionally, we see a positive trend of lower operating expenses. Sales and marketing grew slightly, R&D declined, and SG&A expenses were roughly flat YoY. In general, operating costs fell by 4% YoY. Additionally, stock-based compensation continues declining, dropping by more than 30% YoY. The adjusted operating margin came in at 23%. The adjusted gross margin came in at approximately 80.8% for the quarter, demonstrating remarkable profitability and massive earnings potential.

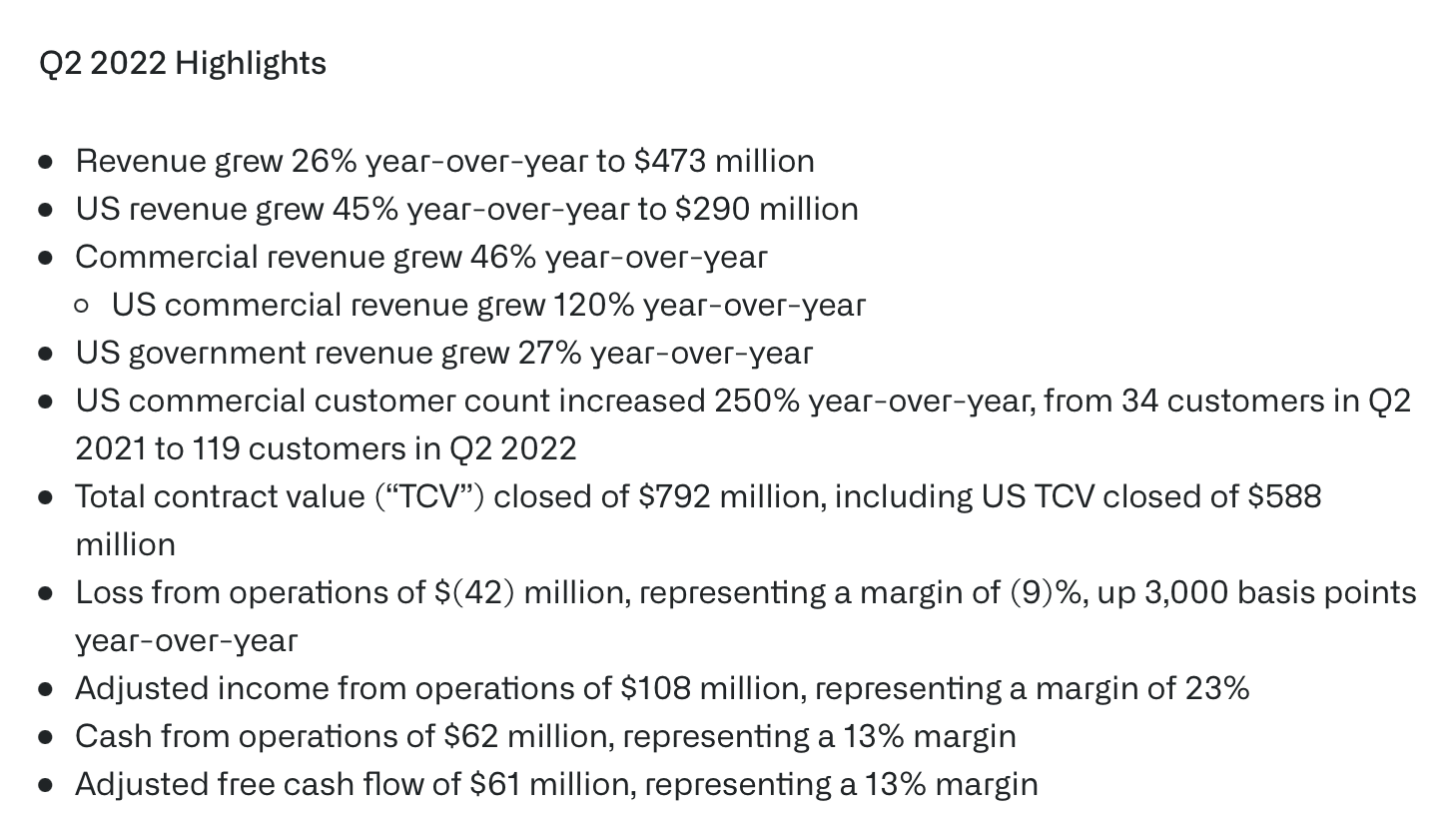

Q2 – Remarkable Highlights

Q2 highlights (Investors.palantir.com )

We saw robust YoY revenue growth, with an ever higher 45% growth rate in the U.S. Palantir’s commercial business is performing excellently, growing revenues by 46%, with outperformance in the U.S., increasing revenues by a whopping 120% in that crucial market. Moreover, the U.S. commercial customer count exploded by 250% YoY, illustrating incredible demand for Palantir’s products and services and implying significant future growth and widespread adoption for Palantir.

Palantir Could Achieve Widespread Adoption

Karp, Palantir’s CEO, said that Palantir remains focused on the long term, and so should you if you’re a Palantir shareholder.

“We are working towards a future where all large institutions in the United States and its allies abroad are running significant segments of their operations, if not their operations as a whole, on Palantir.” – Alex Karp.

We must consider that Palantir is in the very early stages of its operations, growth, and profitability. Yet, the company offers the top products and services in its space. If it did not, Palantir probably wouldn’t be the contractor of choice for the U.S. government, including the DOD, CIA, NSA, and other intelligence agencies. Moreover, Palantir probably wouldn’t be seeing such spectacular growth in the corporate space if its competitors had the upper hand. Furthermore, we see that Palantir has significant competitive advantages. Thus, we can conclude that Palantir could achieve widespread adoption in the corporate world. Suppose Alex Karp is right and large government, civil, and corporate institutions of the U.S. and its allies run significant portions of their operations on Palantir. In that case, the sky is the limit, and Palantir’s stock price should advance significantly in the coming years.

Here’s what Palantir’s financials could look like in the future:

| Year | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

| Revenue $ | 2b | 2.6b | 3.4b | 4.4b | 5.7b | 7.3b |

| Revenue growth | 30% | 30% | 30% | 30% | 28% | 25% |

| Forward P/S ratio | 7 | 8 | 9 | 9 | 8 | 8 |

| Price | $9 | $14 | $21 | $27 | $32 | $40 |

Source: The Financial Prophet

Palantir is trading around seven times forward sales estimates, and the P/S multiple could expand as the company advances. Palantir has a log growth runway, and the company’s revenue growth could be around 30% in the coming years. In comparison, Nvidia (NVDA) has slower growth projections, and the stock trades at about 14 times next year’s sales estimates. Valuations of ten times sales and higher are widespread in the hardware and software industries.

Even Microsoft (MSFT), a mature software company, trades at approximately nine times forward sales, more expensive than Palantir. Therefore, we see that Palantir is relatively cheap and could experience multiple expansion as the company advances in future years. Thus, as Palantir continues increasing revenues and improving profitability, its stock could reach the $40 – 50 range within several years.

Risks To Palantir

Despite my bullish outlook for Palantir, market participants should consider several potential risks associated with this investment. While the growth story is strong at Palantir, shares are not cheap by traditional metrics. Furthermore, the company’s earnings are still minimal and may not increase as much as I envision. Moreover, if the company’s growth picture were to turn less bullish, the stock could head in the wrong direction. For instance, if Palantir lost favor with the government or had a data breach, the stock could experience a notable decline. Please consider these and other risks carefully before investing in Palantir.

Be the first to comment