Drew Angerer

As corporations and institutions continue to grow in size, and at the same time begin to adapt to the new reality in which capital becomes scarce while the geopolitical uncertainties create new possibilities for additional supply chain disruptions, it becomes crucial for them to ensure that their software runs uninterrupted and is constantly up to date. While the migration of their data into the cloud in recent years helped them to digitize their processes and scale their operations, the changing environment now forces them to look for solutions that would make sure that their businesses could weather any upcoming challenges with relative ease.

That’s where Palantir Technologies Inc.’s (NYSE:PLTR) Apollo comes into play. As a standalone product, Apollo is able to autonomously deploy custom-made software and security updates to various environments of different organizations in real time, which ensures the safety and continuous operation of critical systems of Palantir’s clients. Thanks to this, Apollo could be considered a one-of-a-kind solution for big organizations that rely on the continuous deployment of software and security updates to run their global operations in challenging environments. As a result, there’s a real possibility that as the total addressable market for such a solution increases with each year, Palantir would be able to continue to expand its business even in the current turbulent environment, which could lead to the appreciation of its shares in the long run.

The Power of Apollo

A lot of the discussions about Palantir focus on highlighting the advantages of the company’s two major platforms Gotham and Foundry, which could are considered to be operating systems for governmental organizations and commercial enterprises that are used for data integration and big data analytics. While both of those platforms have been major drivers of growth for Palantir’s business in recent years, and I have extensively covered them in my other articles in the last few months, Apollo has been considered a silent third platform of the company that wasn’t discussed as much as the others. However, there’s a possibility that this could change soon, as Apollo has all the chances to scale Palantir’s business in the foreseeable future and help it to accelerate the onboarding of new clients.

To understand what Apollo really is it’s better to take a look at how Palantir describes itself. In its latest 10-Q report, Palantir stated the following:

Apollo is a cloud-agnostic, single control layer that coordinates ongoing delivery of new features, security updates, and platform configurations, helping to ensure the continuous operation of critical systems.

At first, Palantir built Apollo for in-house use to help the company to speed up the process of integrating Gotham and Foundry into the organizations of its new clients. As an automated platform for continuous deployment, Apollo evolved to become a standalone product in 2021 and is now able to be used within third-party platforms to provide updates for custom-built software solutions in virtually any environment. As a result, Apollo gives Palantir the ability to substantially increase the number of new clients, as it could successfully deploy custom-built updates with relative ease.

That’s why in his letter to shareholders, Palantir’s CEO Alex Karp has been stressing the importance of Apollo for Palantir and how it could be as important for the business as Gotham and Foundry are by saying the following:

We believe that the demand from large enterprises for a software delivery and maintenance solution that is platform agnostic will be as significant as the demand for the underlying data integration and analytical capabilities themselves.

One of the biggest advantages of Apollo is that it replaces the need for its potential customers to build in-house continuous integration/continuous delivery (CI/CD) capabilities. Instead, the potential customers are able to focus on developing the software itself and then outsource the deployment of that software to Palantir without increasing their headcount whatsoever.

What’s also important to mention is that Palantir recently received an impact level 6 accreditation from the Department of Defense, which makes it possible for government contractors to use the company’s solutions to store, share and interact with data of the highest level of authorization. Therefore, Palantir is only one of the few companies along with Microsoft Corporation (MSFT) and Amazon.com (AMZN) with the highest clearance level in the world, which gives its platforms, and Apollo in particular advantage against other platforms offered by different businesses in the DevOps and CI/CD space.

What we also know is that Apollo has already been able to deploy software and security updates in over 500 independently-released microservices across over 300 different environments. At the same time, there’s also a possibility that those numbers are gradually increasing with each quarter, as Palantir continues to aggressively sign new customers and at the end of Q2 its customer count increased to 304, up from 169 a year ago.

What’s Next?

Considering the capabilities of Apollo, the two major questions that investors could have in mind are how much revenue the platform is generating and what is its total addressable market. The first question is hard to answer because Palantir doesn’t disclose the exact amount of revenue that each platform generates. However, we do know that aggressive growth in new customers occurred after Apollo has been released as a standalone product in 2021. At the same time, the fact that Palantir’s CEO Alex Karp is saying that the demand for a software delivery and maintenance solution will be the same as the demand for a data integration platform could lead us to the conclusion that Apollo is going to have a greater impact on the business in the future.

As for the second question, we do know that Apollo is mostly a deployment solution for organizations that conduct their operations in the cloud. However, Apollo’s main advantage is that in essence, it’s a cloud-agnostic solution, and as a result, it can deploy software and security updates to entirely different environments that operate within multiple cloud platforms with relative ease. That’s why Apollo could be considered a supercloud solution. Wikibon describes superclouds as follows:

Supercloud describes an architecture that taps the underlying services & primitives of hyperscale and other clouds to deliver additional value above and beyond what’s available from a single public cloud provider. A supercloud delivers capabilities through software, consumed as services, and must span multiple cloud platforms, inclusive of on-prem clouds and edge installations.

Considering that with each year the number of cloud vendors and cloud platforms increases and the overall cloud computing market is expected to grow at a CAGR of 17.43% by the end of the decade and be worth $1.6 trillion, it’s safe to assume that the demand for a supercloud solution such as Apollo is also going to increase. As a result, there’s a high possibility that Alex Karp would be right in his belief that there could be a significant demand for a solution such as Apollo in the future.

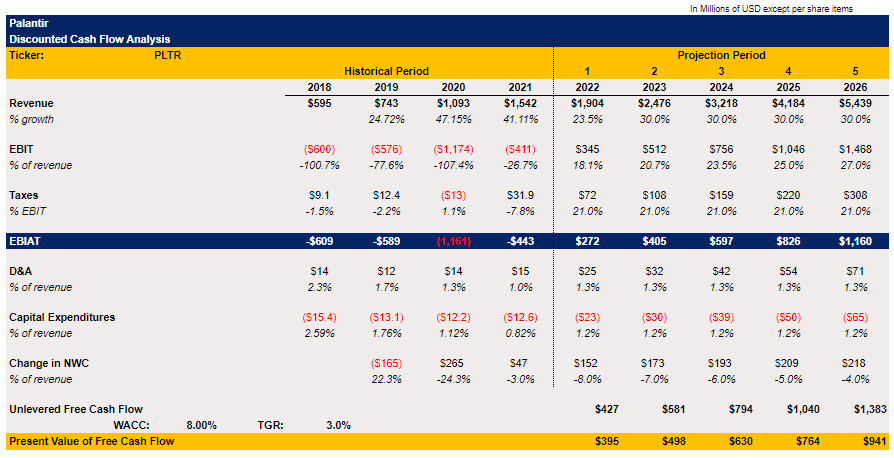

That’s why I decided to slightly update my DCF model. In September, my DCF model showed that Palantir’s fair value is $10.03 per share, which represents an upside of ~25% from the current levels. That model assumed that Palantir’s top line would grow at 23.5% in FY22 and at 25% Y/Y in the following years, below the management’s initial forecast of annual growth of 30% Y/Y through 2025. That model could be considered as a base-case scenario under which Palantir is still undervalued.

However, if Apollo manages to help Palantir aggressively scale its business in the future, then it makes sense to create an additional optimistic scenario under which the company grows at a greater rate. That’s why in this new model the revenue is forecasted to increase by 23.5% Y/Y, while in the following years the top-line growth increases to the management’s initial forecasts of an annual growth rate of 30%. All the other metrics remain the same as in the previous model where WACC is 8%, while the terminal growth rate is 3%.

Palantir’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

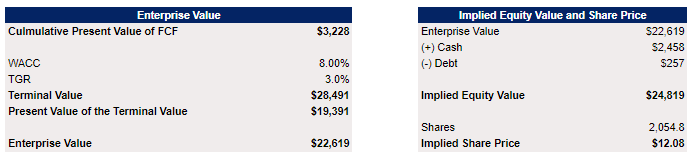

According to this more optimistic model, Palantir’s enterprise value appears to be $22.6 billion, while its implied share price is $12.08 per share, which represents an upside of ~50% from the current market price and creates a buying opportunity for long-term investors.

Palantir’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

Risks

One of the downsides of Palantir is its high level of secrecy. Due to working with governmental agencies, the company can’t disclose various contracts and relationships that it has with its clients. As a result, we don’t know exactly how much revenue the company generates from each client. However, what’s worse is that the company has also been actively investing in various SPACs last year. As a large portion of SPACs depreciated since the beginning of this year due to the worsening macroeconomic environment, there’s a risk that Palantir could generate greater than expected losses from them in the foreseeable future. Even though the company closed its SPAC program earlier this year, the lack of transparency prevents investors from knowing how much the investments that were made in 2021 generated returns or lost capital, which could lead to weaker performance of the overall business than previously expected.

The other problem of Palantir is that as a growth stock, there’s a real possibility that it could continue to depreciate or trade at distressed levels for as long as the Federal Reserve continues to increase interest rates to tame the rising inflation. As a result, while Palantir is undervalued at the current levels, it could remain to be undervalued for a while due to things that are outside of its control.

The Bottom Line

We’ve entered a new period of global decoupling in which supply chains are being reorganized at the same time as the geopolitical uncertainties create new macroeconomic risks to organizations and institutions. As a result, in times like these, it becomes crucial to have a solution such as Apollo, which ensures that corporations and enterprises are able to deploy all the necessary software and security updates that make it possible for them to continue to operate in the current challenging environment with relative ease. That’s why Palantir’s CEO Alex Karp might be correct when he states that the demand for a solution such as Apollo could be as significant as the demand for other data analytics solutions that the company offers.

At the same time, considering that Palantir trades below its fair value both in the optimistic and in the base-case scenarios, long-term investors might use this as an opportunity to increase their exposure to the company at the current levels, as there’s an indication that Apollo could greatly improve the business’s performance in the foreseeable future.

Be the first to comment