Floriana/iStock via Getty Images

Given the excessive inflation, now sitting at 8.6% in the US, a war in Eastern Europe, commodity price shocks and widespread volatility in the global economy, we think Palantir (NYSE:PLTR) will find itself in pole position. With its robust balance sheet and path to profitability, we think it is also positioned to get significant tailwinds from productivity gains in terms of AI / Deep Learning and Machine Learning.

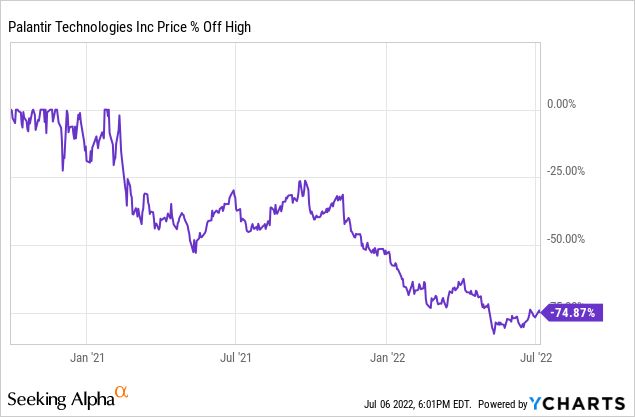

Moreover, Palantir is one of the few software companies that has stood the test of time, actually weathering recessions such as the 2008 global financial crisis and a subsequent liquidity crunch. As VCs pull back liquidity from unicorns that are only now appearing to be vaporware in a tightening monetary cycle, we will explain why Palantir might be worth taking a position in after falling nearly 75% since last year.

The Overlooked Tailwinds

We believe that the inherent value of AI and Machine Learning/ Deep Learning in the workplace is often underestimated by other analysts, and therefore expect that Palantir could see much more upside in the future than is currently reflected in its share price.

In particular, we track sentiment on sites such as Metaculus, a U.S. reputation-based massive online prediction request and aggregation engine. Briefly, it is a system whereby a community can vote on certain topics and gain points for giving accurate predictions (or lose points for giving inaccurate ones).

It should become particularly important, since studies have shown that the wisdom of crowds is in fact far more accurate than individual sense or even expert predictions. Metaculus also states that research is indicating that:

With the right incentives and feedback, groups of people can make remarkably accurate predictions of the probability of future events.

Metaculus succeeded, and in turn has a rather remarkable and accurate track record so far since its inception in 2015. And while Palantir’s shares have slumped, numerous forecasts about AI, computing, deep learning and machine learning have meaningfully shifted to a shorter time frame.

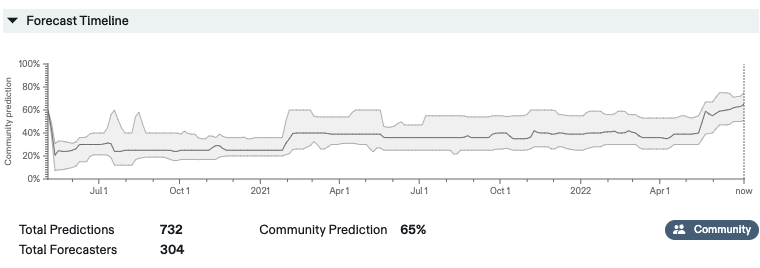

One prediction, which looked at whether a computer will be able to pass a Turing test in 2029, is now 65% likely, compared to only about 25% 2 years ago. The criteria set here for the Turing test included, for example, the machine’s ability to carry on a 6-hour chat conversation, where the jury would not be able to differentiate.

Metaculus

The main reasons cited for shrinking timelines were first and foremost Google’s (GOOG) (GOOGL) Pathways Language Model (PaLM), which recently announced its findings of its new mind-boggling 540 billion parameter AI model. This model was even described as outperforming the average performance of humans who had to solve the same tasks.

Other developments, such as Google’s Minerva, announced a few days ago, have contributed to the shortened schedule. Minerva is Google’s internally developed neural network, with the ability to answer mathematical questions among other complex topics.

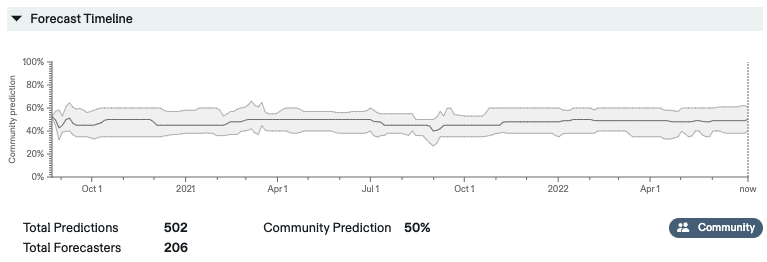

We also believe that AI, Deep Learning and Machine Learning will make a meaningful contribution to the amount of revenue generated by services that offer the software in general. For example, one forecast attempts to gauge whether the systems in the GPT line will be able to generate more or less than US$1BN in revenue by 2025. GPT is best known for its GPT-3 language models, which are capable of procuring human-like text at stunning levels.

Metaculus

The confidence that the GPT line alone is capable of bringing in US$1BN within a few years comes primarily from estimates that OpenAI can already generate US$125M or more in annual revenue as of last year. In fact, some companies, such as CopyAI, Copysmith and others, have already started full-scale businesses around these models and have already gained a lot of traction.

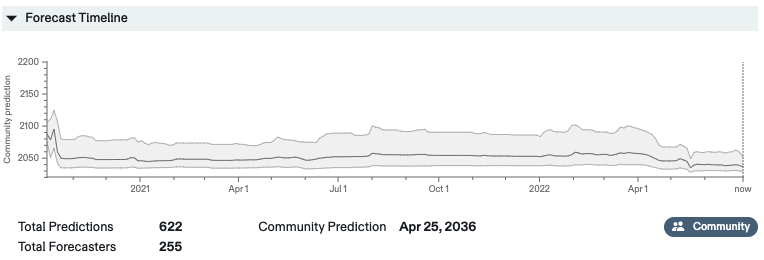

Recent breakthroughs have even led forecasters to adjust their timeline when it comes to Artificial General Intelligence, believing it will be achievable by April 3036. According to the definition of AGI, an intelligent agent should be able to understand or learn any intellectual task that a human can also do.

About 2 years ago, forecasters predicted this would be reached earlier by 2050. That’s 14 years in a matter of 2 years of new developments. That means that while AI / DL / ML is evolving, analysts and the public are still grossly underestimating its development and impact.

Metaculus

If AGI were feasible, its effect on productivity would be almost guaranteed to be exceptional: according to another forecast, the Vanguard Information Technology ETF (VGT) would post a 3400% gain between now and 2040 if AGI became a reality by then.

As such, we believe that Palantir is primed to benefit from the tailwinds of AI / DL / ML since it is in a unique position compared to the competition when it comes to their business model of unique integration and having a foothold in the major institutions / government agencies.

This is especially true as the safety, security, and operability/integrability of AI will become more important as the technology evolves.

Palantir Stock – In Search of a Reasonable Valuation

Palantir is arguably an attractive investment at present in a period of slower growth or recession, as Palantir is considered to be vital in many organizations. Most importantly, the stability and quality of Palantir’s revenue streams may be overlooked, as government is also usually the last to cut back on essential services.

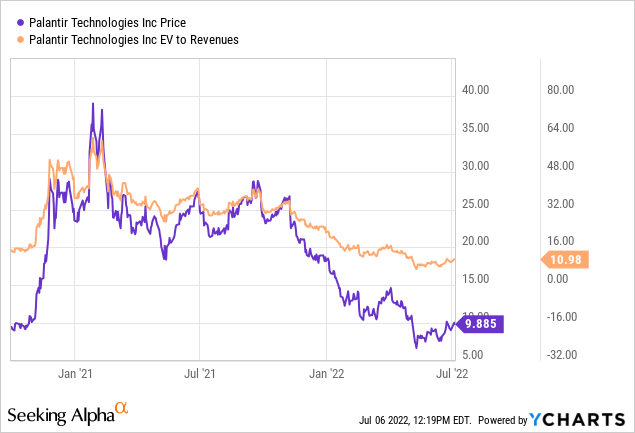

Palantir is considered a buy by us on a relative valuation basis, as its EV/Revenue multiple is below the industry average for Software, specifically for systems and applications. The industry average for EV/Revenue is about 12.84, compared to Palantir at 10.98.

While this in itself is an overarching advantage, the biggest difference comes from Palantir’s exceptional revenue growth, which the management team promises to be at least 30% over the next 3 years.

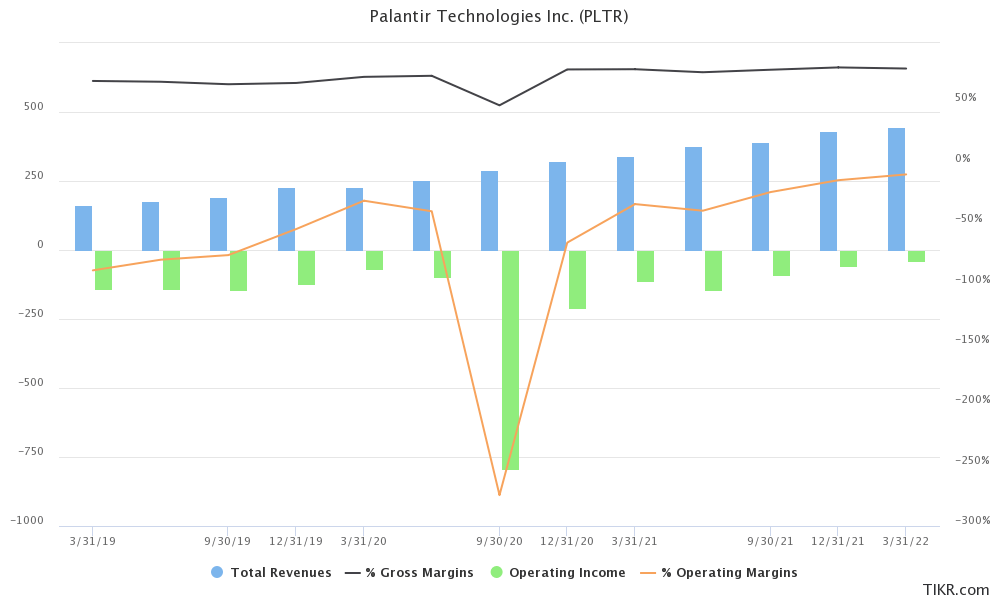

In our view, this is achievable, judging by Palantir’s past revenue growth, which was 41.1% year-on-year in 2021. If Palantir could achieve this growth rate, it would significantly outperform the broad software market, which is expected to grow by about 10-12% from now until 2030. In addition, Palantir has US$2.52BN in cash and cash equivalents, which gives Palantir an edge as it does not have to worry about raising additional capital anytime soon.

The most important aspect that Palantir still needs to get in line is the actual bottom line profitability on a GAAP basis. Albeit showing a very positive trend, margins went from negative 33.4% in the first quarter of last year to negative 8.8% in the first quarter of this year. If this trend continues consistently in this historical direction, Palantir should become GAAP profitable sooner than later.

TIKR Terminal

To illustrate, if Palantir were able to grow its revenues at a 30% CAGR, it would generate US$16.35BN by 2030. If Palantir is able to grow its net margins to the industry average of 19.66%, it will generate US$3.21BN in net income. Using a relatively conservative earnings multiple of 20, as the software sector has historically traded at much higher multiples, Palantir would reach a market capitalization of US$64.29BN.

In terms of price per share, that would equate to $31.41 per share, or a CAGR of 13.82% relative to the current share price, which remains a fairly significant alpha relative to other benchmarks such as the S&P 500.

Red Flags, Risks & Management Trickery

The main reason we decided not to give Palantir a “Strong Buy” rating has to do primarily with some of the red flags we see when it comes to financial reporting, combined with a general lack of transparency that management occasionally exhibits.

While Palantir cannot be entirely blamed for being transparent about contracts, since they have to abide by NDAs, we think there is room for improvement. For example, in their last earnings call, we feel that almost every question was either evaded or somewhat answered with an incomplete answer.

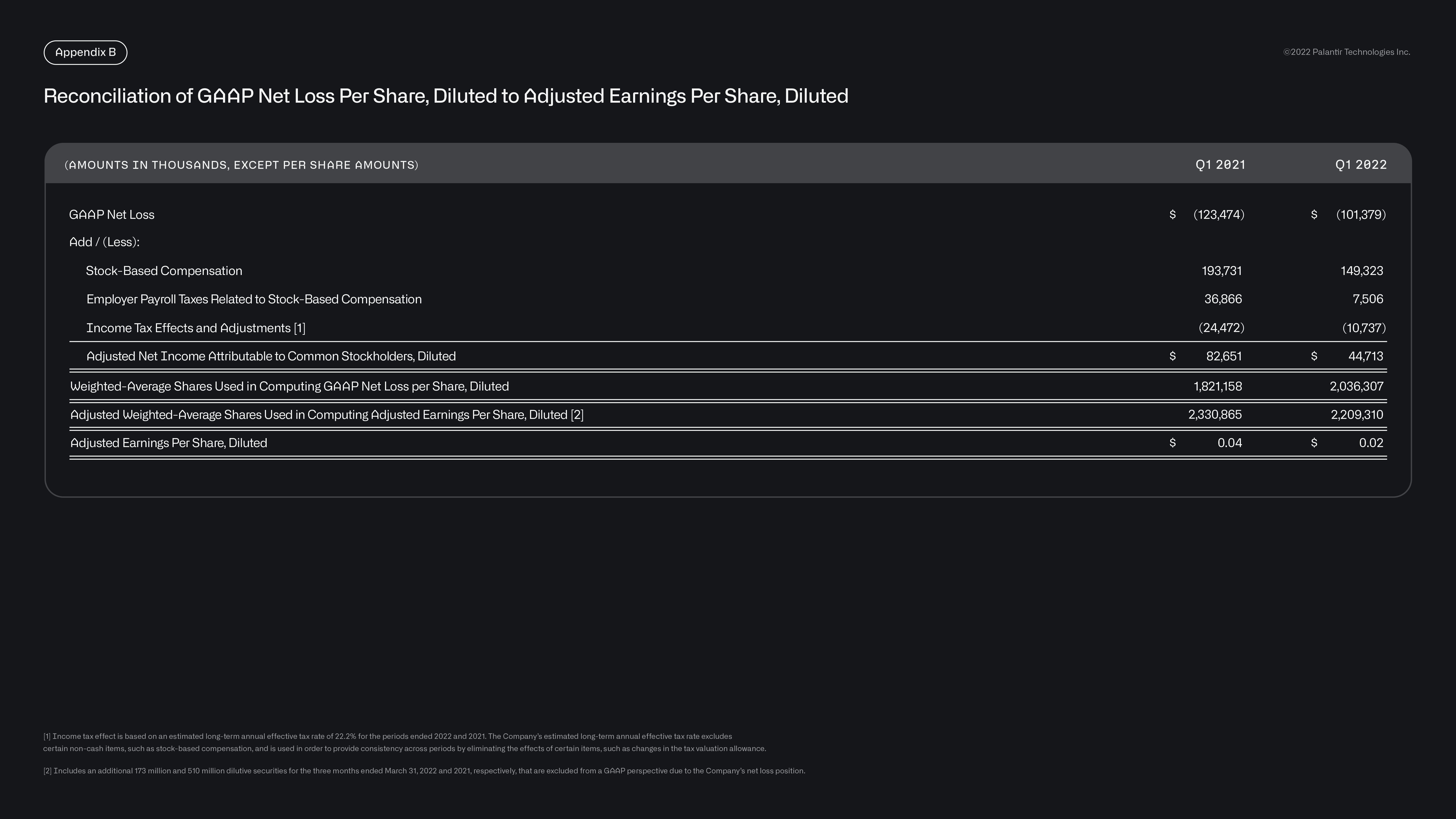

An analyst asked if the company is striving to become GAAP profitable, to which management completely dodged the question and replied that, looking back, their operating margins have improved. After which they replied that they had recorded US$424M in “Adjusted” free cash flow. For us, it is as much of a red flag when management makes their financial statements deceptive and less readable by using almost exclusively non-GAAP financial measures.

Palantir IR

Palantir is also happy to use these non-GAAP measures, for example fully discounting share-based compensation, when we believe it is an essential part of the company’s functionality. After all, employees need to be paid, and might not have joined the company if compensation was not included in their employment contract.

One analyst even asked how they are trying to limit share dilution, to which management again made a very vague statement to show that there was almost no dilution, when we can clearly see that the number of shares outstanding has increased.

TIKR Terminal

But to get back to the main point, management never really answered the question of when they would become profitable under GAAP. Not even an estimate. In Palantir’s presentation, we also saw that they liked to express how their “TAM” was growing with their products, which was a sign to us that the company would rather refrain from talking about profitability and performance and rather try to paint a rosy picture.

Palantir IR

Some of Palantir’s documents and presentations are also often too complicated in our opinion, and much is explained in far too complicated a way when it should be explainable in layman’s terms to people who are only involved in finance. And in this case, we would very likely offer him the advice that Albert Einstein and Peter Lynch once gave us that:

If you can’t explain it simply, you don’t understand it well enough (- Einstein A.)

And even that:

If you can’t explain to a 10-year-old in two minutes or less why you should buy a stock, you shouldn’t own it. (- Lynch P.)

We believe that management sometimes forgets that it is explaining its business to investors, not to other experts in the field of software or data, and therefore should not use jargon in every sentence or excessively complicate matters.

Another factor we see as a risk is the decline in annual state revenue growth, even though the amount of state revenue per customer has increased. The management team mentioned that these revenues will accelerate in the second half of the year, with acceleration already seen in the second quarter prior to the earnings conference.

Palantir IR

The Bottom Line

In the short term, we expect Palantir may be subject to some additional pressure as the company is not yet generating GAAP profitability and remains as a somewhat speculative play. However, in the long term, we believe Palantir definitely has the ability to generate significant alpha above broad-based benchmarks.

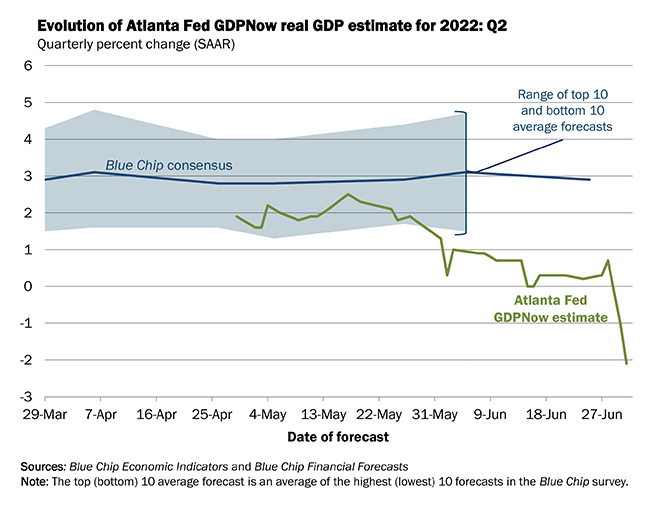

We also believe Palantir is uniquely positioned to weather a variety of macroeconomic headwinds, such as a likely earnings recession, as it can be viewed as a vital service with a high quality of revenue stream. This is likely to become even more important while the Atlanta Fed’s GDPNow forecast is for Q2 GDP of -2.1%.

It should be noted that the GDPNow forecast is a purely quantitative measure that can be changed or revised later by the Federal Reserve itself. On paper, negative GDP in Q2 would be the second consecutive decline in GDP growth and would already lead the U.S. into a technical recession. Combined with a spread between the 10-year and 2-year Treasury yields that is sitting inverted at -0.06%, could mean that we are in for a lot more pain soon.

Atlanta Fed

And perhaps investors are actually underestimating the tailwinds Palantir will enjoy with the advent of AI, deep learning, machine learning, and overall productivity gains from these new technologies.

Seeking Alphas Quant currently rates Palantir a “Sell,” citing weakness in earnings revisions, valuation and momentum, although these factors are likely to improve significantly as Palantir continues to show tremendous growth.

Be the first to comment