Michael Vi

Shares of Palantir (NYSE:PLTR) soared close to 19% in extended trading yesterday after the software analytics company presented its fourth-quarter earnings sheet. There were a number of notable take-aways from Palantir’s earnings release, the most important one was that the company achieved its first-ever quarterly profit on a GAAP basis. Palantir also beat top and bottom line estimates as the firm executed well in the fourth-quarter and continued to add a lot of new clients to its business. The outlook for FY 2023, however, was deeply disappointing at it indicates a further slowdown of the company’s (commercial) business!

Palantir’s accomplishments in Q4’22

Palantir beat expectations on the top and bottom line in the fourth-quarter which was generally regarded as much better than expected. Palantir generated $509M in revenues in Q4’22 which beat the average prediction of $502M. Adjusted earnings per-share were also better than expected at $0.04 compared to $0.03 expected.

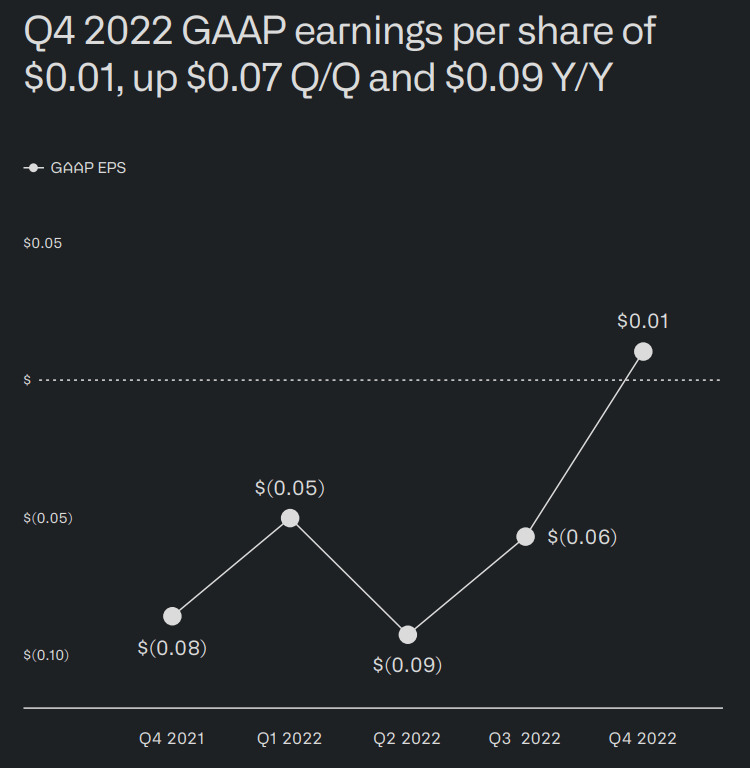

There were a number of important take-aways in Palantir’s fourth-quarter earnings sheet. For the first time in the company’s history, Palantir reported a net profit based on a GAAP basis… which is most likely the top reason that explains Palantir’s strong price action in extended trading. The company’s financial statements showed a $31M GAAP profit for the fourth-quarter which is clearly a milestone achievement for the software analytics company as it has struggled to generate profits for a long time. What the Q4’22 earnings report achieved more than anything was to prove to investors that Palantir is operating a valid business model that has the potential to deliver distributable earnings to shareholders. Although Palantir was only slightly positive with GAAP earnings of $0.01 per-share in Q4’22, it was a big win for the software company.

Source: Palantir

Palantir generated 18% top line growth in Q4’22, driving by the government segment, and reported total revenues of $509M. In third-quarter, Palantir grew its revenues at a 22% rate so the firm unfortunately saw a quarter over quarter revenue deceleration. The government segment grew revenues 23% year over year to $293M while the commercial segment saw its revenues go up by 11% year over year to $215M. The commercial segment saw its third straight quarter of revenue deceleration in FY 2022 which is having an impact on Palantir’s growth projections for the current fiscal year, but the company continued to do very well regarding customer acquisition.

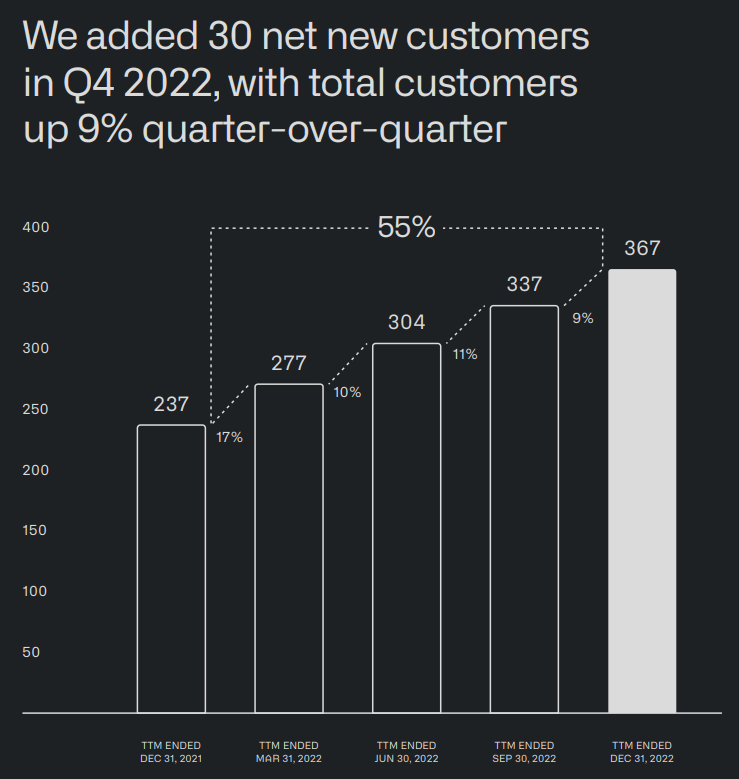

Customer acquisition and monetization

Strong financial results have been made possible by Palantir’s ability to sign up new clients that use its Foundry platform. Palantir’s Foundry products allow customers to centralize and streamline their data bases which aids the decision making process and delivers analytics insights. In the fourth-quarter Palantir added 30 new clients to its portfolio which brought its total customer count (government and commercial) to 367 by the end of the year, showing 55% year over year growth. It is this (commercial) customer acquisition growth — the commercial segment grew its customer base 77% year over year — that Palantir has been able to grow its revenues at double digit rates and finally achieve GAAP profitability.

Source: Palantir

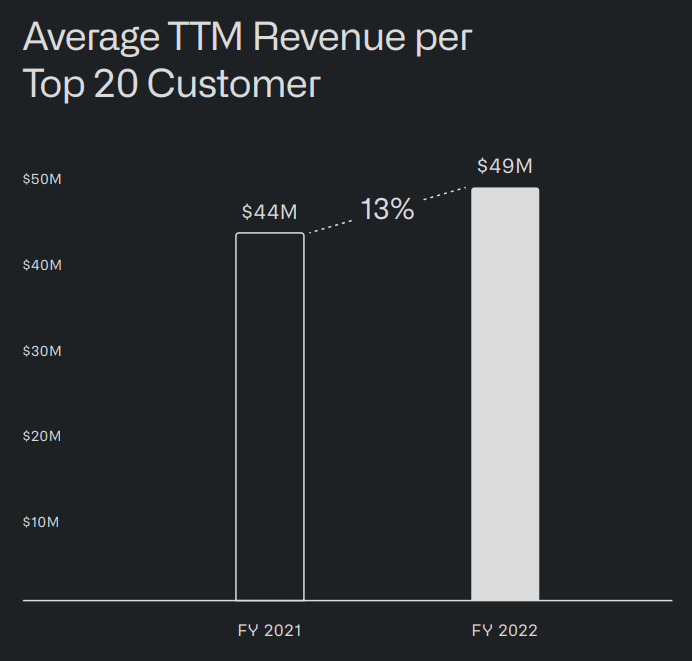

Additionally, Palantir keeps making progress by upselling its customers. The average top 20 customer spent $49M on Palantir’s products and services in the last twelve months, showing an increase of 13% year over year. With improving customer monetization, top customers become more valuable and continue to make an outsized revenue contribution for Palantir.

Source: Palantir

Outlook for FY 2023

Palantir generated 24% year over year top line growth in FY 2022 and total revenues of $1.91B… which fell into Palantir’s expected revenue range of $1.9-$1.902B. The company achieved 41% revenue growth in FY 2021 and this revenue growth is expected to slow down further this year.

For FY 2023, Palantir guided for $2.180-$2.230B in revenues, implying just 16% year over year growth. In FY 2021 and FY 2022 Palantir stated a revenue growth goal of about 30% annually (until FY 2025) which the software company clearly does not see as an achievable target anymore. The implied revenue growth rate falls short of Palantir’s longer term growth projections by about 50% which is the reason why I am not changing my rating on Palantir (which is currently “hold”). Palantir also said that it expects FY 2023 to be its first-ever profitable year.

Palantir’s valuation

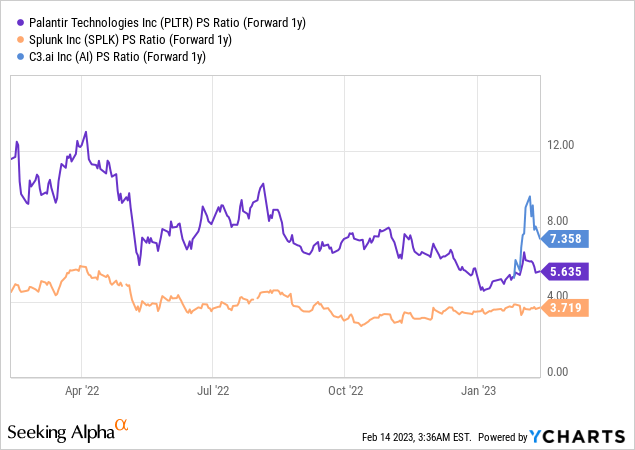

Palantir has achieved a great success by achieving GAAP profitability in Q4’22, but the growth outlook is a problem because Palantir is chiefly valued based off of its revenue growth potential. The software company is currently trading at a P/S ratio of 5.6 X and with just 16% top line growth expected this year, there are likely going to be more investors going forward that will question the price tag that the market places on Palantir’s growth… after the initial excitement about Palantir’s GAAP profits wears off. Compared against other software analytics companies like Splunk (SPLK) and C3.ai (AI), PLTR stock is not the most expensive in the industry, but it clearly isn’t cheap.

Risks with Palantir

The big risk for Palantir remains its top line growth. The guidance for FY 2023 implies only 16% revenue up-side which compares unfavorably to Palantir’s longer term goal to achieve 30% annual revenue growth. A slowdown in the commercial business is also a risk factor that could make the already existing problem of decelerating revenue growth worse. What is also a potential risk factor is a resurgence of inflation which could force companies to reduce their spending on software products and result in weaker customer monetization for Palantir going forward.

Final thoughts

I generally like Palantir and the company legitimized its business model by posting its first-ever GAAP profit in the fourth-quarter. Customer acquisition and monetization also continued to look good overall, although commercial revenue growth continued to decelerate for a third consecutive quarter.

What was less than impressive, however, was the guidance for FY 2023 which reflects slowing business momentum in commercial and which is the reason why I believe buyers should be careful here and not run after the stock price.

With just 16% projected revenue growth, Palantir falls way short of its longer term growth projection of 30% top line growth annually. I believe the poor revenue forecast should weigh more heavily than expected GAAP profitability in FY 2023 largely because Palantir is still valued as a “growth stock”. My rating on Palantir (“hold”) remains unchanged!

Be the first to comment